Yield Versus Value: The Structural Trade-Off at Atrium Mortgage Investment Corp

A 7.8% dividend yield supported by stable payouts, yet constrained by limited capital efficiency and muted earnings growth.

Investment Thesis: High Income Appeal Offset by Structural Return Constraints

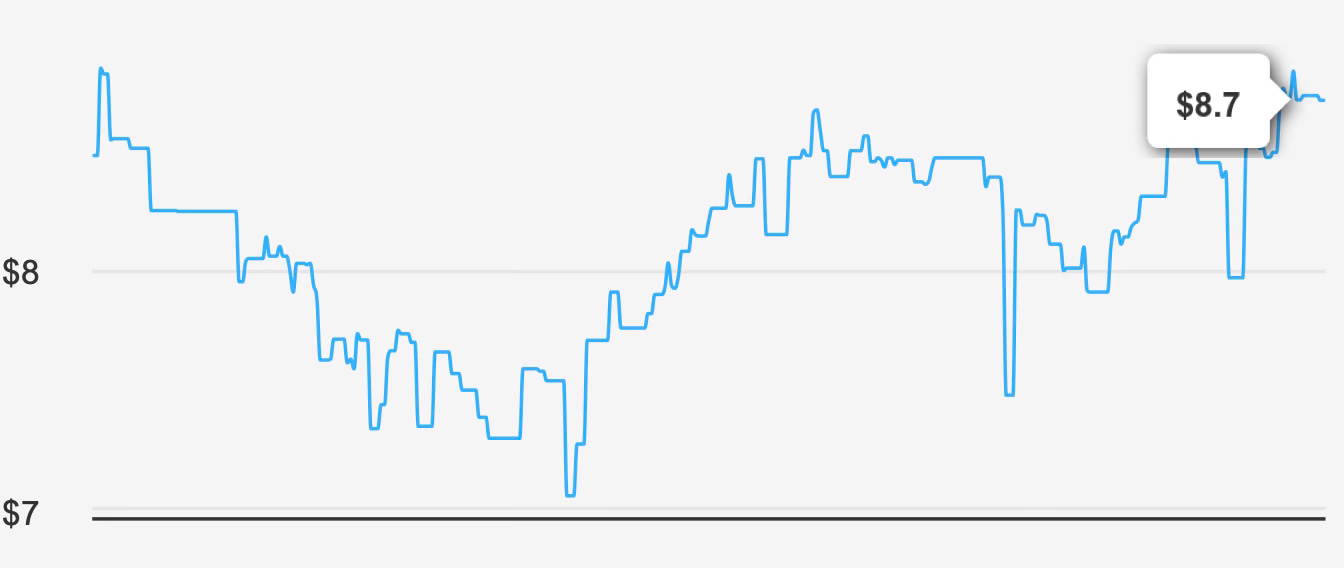

Atrium Mortgage Investment Corp operates as a Canadian mortgage investment corporation focused on commercial real estate financing across urban centers in Ontario and Western Canada. At a current share price of $8 and a market capitalization of $417.04 million, the company offers an income-oriented profile anchored by a forward dividend yield of 7.8%. On the surface, that yield appears compelling in today’s market environment, particularly within the banking and alternative lending space.

However, the underlying economics present a more complex picture. The company’s intrinsic value is estimated at $5.555, implying a negative margin of safety of 56.6% at current levels. While valuation metrics alone do not dictate future performance, such a wide disparity between price and intrinsic value suggests that the market may be assigning a premium to the stock despite muted growth and structural return challenges.

Over the past five years, revenue has grown at an annualized rate of 8.0%, with 10-year revenue growth moderating to 3.4%. Earnings growth has been even more restrained. Annual EPS has compounded at just 3.2% over five years and 1.8% over ten years. This places the company below the industry’s projected 6% long-term growth trajectory, indicating limited competitive acceleration.

The investment case, therefore, centers on income rather than growth. Yet even that income stream carries constraints, given a payout ratio hovering near full distribution of earnings and a capital allocation profile that has not consistently generated returns above its cost of capital. Investors seeking durable dividend compounding may find the underlying return structure insufficient to support long-term expansion.

Earnings Momentum & Profitability Trends

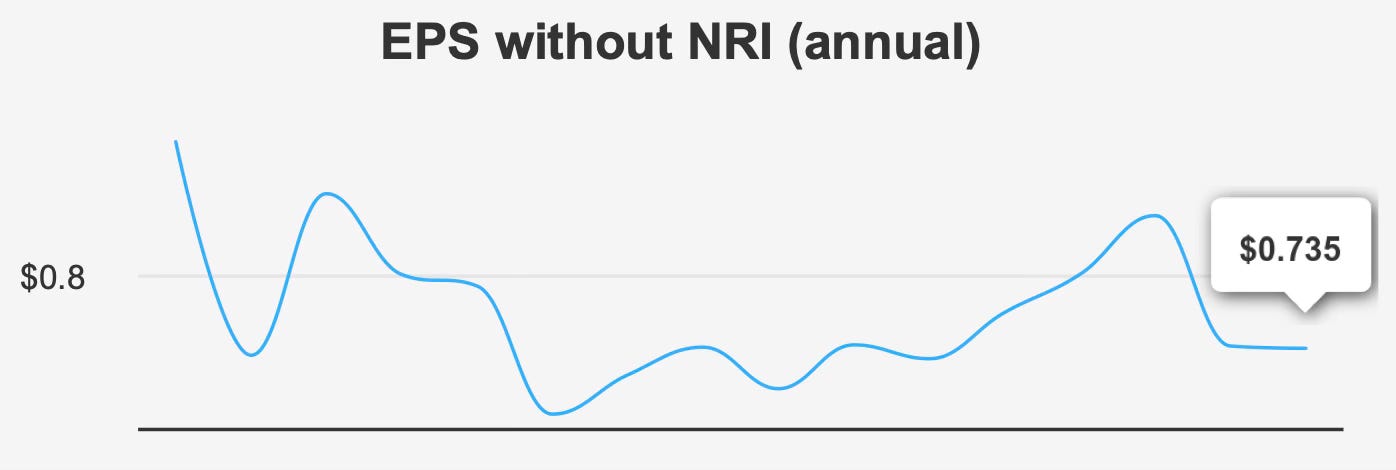

Recent quarterly results underscore the lack of earnings momentum. For the quarter ended September 30, 2025, EPS excluding non-recurring items came in at $0.181. That figure declined from $0.198 in the prior quarter and from $0.192 in the same quarter last year, representing an 8.6% sequential contraction and a 5.7% year-over-year decline.

While one quarter does not define a long-term trend, the pattern aligns with the company’s broader growth stagnation. Analysts project next fiscal year EPS at $0.813, with revenue expected to reach $61.66 million by the end of 2025 before edging slightly lower to $61.21 million in 2026. The absence of forward revenue expansion reinforces the view that earnings growth may remain constrained without structural change.

Profitability metrics present deeper concerns. Over the last five years, median return on invested capital has been 0.0%, materially below the median weighted average cost of capital of 9.4%. That spread implies that incremental investments have not generated economic value. When ROIC consistently trails WACC, shareholder value creation becomes difficult, regardless of headline earnings stability.

Return on equity offers a more balanced perspective. The five-year median ROE stands at 9.6%, with the current level at 9.6%, modestly exceeding the current WACC of 8.9%. While this indicates that equity capital is producing returns slightly above its cost, the absence of positive ROIC suggests inefficiencies in broader capital deployment. In practical terms, equity returns are being sustained, but not at a level that supports meaningful internal compounding.

Gross margin remains reported at 0%, signaling no profit after cost of goods sold. For a mortgage investment entity, this accounting presentation warrants careful interpretation, yet it still highlights operational tightness.

Capital allocation trends further complicate the earnings picture. The company’s 10-year buyback ratio stands at –6.9%, indicating net share issuance rather than repurchase. Over the past year alone, the ratio was –7.3%. Share dilution at a time of modest earnings growth dampens per-share expansion and reduces the organic compounding effect investors typically seek in dividend-paying financial firms.

Taken together, the earnings profile reflects stability but not acceleration. Growth exists, but at a subdued pace and without clear evidence of improving capital productivity.

Dividend Profile & Sustainability

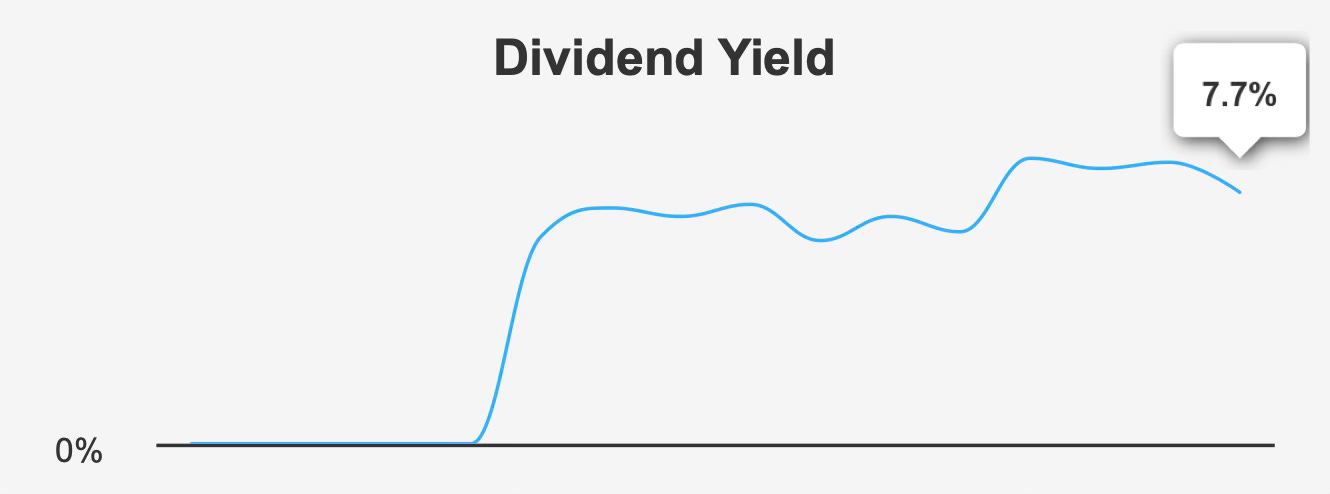

The dividend remains the central pillar of the investment thesis. Atrium has maintained consistent payments, with the most recent quarterly dividend set at CAD 0.0775 per share. The forward yield of 7.7% positions the stock among higher-yielding income securities within its sector.

Dividend growth, however, has been negligible. Over the past five years, dividend growth has averaged just 0.1%. Forecasted dividend growth over the next three to five years is projected at 0.0%, suggesting that management does not anticipate expanding distributions in the near term.

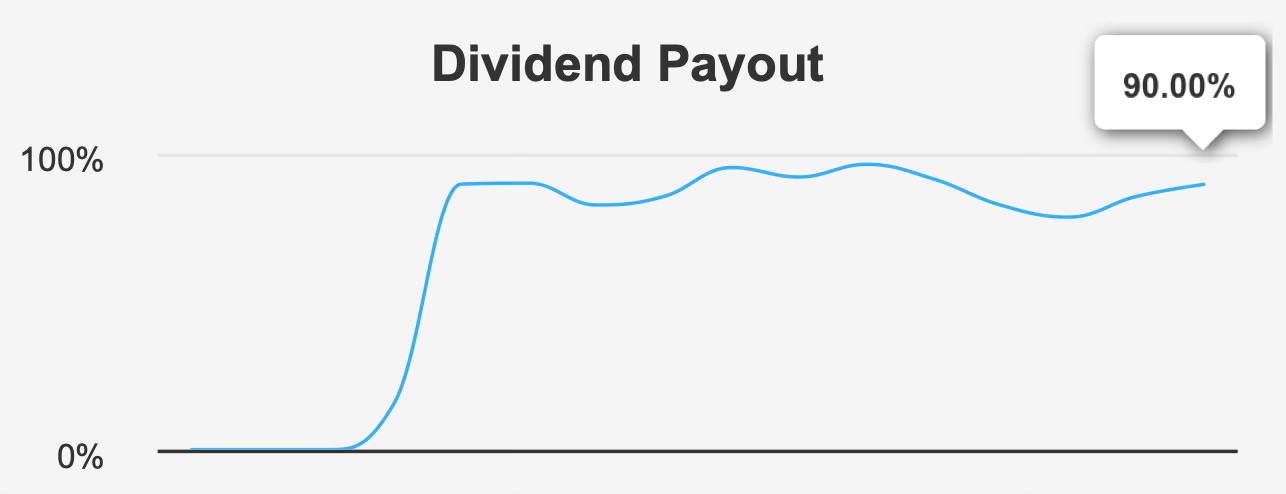

The payout ratio stands at 90%, with dividend coverage of 1.11x. While technically covered, that margin leaves limited room for earnings volatility. Historical payout ratios have hovered around 100% over the past decade, indicating a long-standing policy of distributing most available earnings rather than retaining capital for reinvestment.

This approach can support high yield in stable environments, but it reduces flexibility. Should earnings decline further, dividend sustainability could come under pressure. Conversely, absent stronger earnings growth, material dividend increases appear unlikely.

The next ex-dividend date is February 27, 2026, with payment scheduled for March 12, 2026. The regularity of these distributions reinforces management’s commitment to income investors, yet the structural payout ratio limits optionality.

In essence, the dividend appears stable but static. Investors purchasing shares today are effectively locking in yield rather than participating in a growing income stream.

Valuation Analysis: Premium Pricing Despite Limited Economic Value Creation

At $8 per share, the stock trades above its calculated intrinsic value of $5.555, implying a negative margin of safety of 56.6%. Although valuation is never precise, such a disparity signals that the market may be prioritizing yield over underlying capital efficiency.

The company’s price-to-earnings ratio is near a three-year high, indicating that the multiple investors are willing to pay for each dollar of earnings has expanded even as earnings momentum has softened. Similarly, the price-to-sales ratio is approaching its three-year peak while revenue per share has declined over the past year. This combination suggests valuation expansion unsupported by accelerating fundamentals.

A key concern in valuation analysis is the gap between ROIC and WACC. With ROIC at 0.0% versus a 9.4% median WACC, the company is not generating economic profit. In traditional discounted cash flow frameworks, sustained ROIC below WACC compresses intrinsic value over time unless growth materially improves.

While the forward dividend yield of 7.8% may justify some premium in income-focused markets, valuation should reflect both income durability and reinvestment returns. Given stagnant revenue projections and limited dividend growth, the case for multiple expansion appears constrained.

In practical terms, investors are paying a historically elevated earnings multiple for a business delivering modest growth and limited capital efficiency. That imbalance tilts valuation risk to the downside unless operational improvements emerge.

Risk Assessment & Capital Structure Considerations

Risk factors extend beyond valuation. The company currently benefits from a lower tax rate, which has supported earnings. However, this advantage may not be permanent. A reversion toward higher tax levels could compress net income and strain dividend coverage.

The payout ratio of 0.90 leaves little buffer for earnings volatility. Any downturn in real estate markets or credit performance could directly affect distributable income. The balance sheet is characterized by high levels of debt, and although debt-to-EBITDA is not provided, commentary points to weaker balance sheet strength relative to conservative benchmarks.

The Piotroski F-Score of 7 indicates generally sound financial health, suggesting that liquidity, leverage, and operational efficiency metrics are within acceptable bounds. Meanwhile, a Beneish M-Score of –2.51 implies a low probability of earnings manipulation, reinforcing financial reporting credibility.

However, liquidity in the stock itself presents practical risk. Average daily trading volume over the past two months has been 6,574 shares, with a recent daily volume of just 501 shares. Such limited liquidity can widen bid-ask spreads and increase price volatility, particularly for institutional participants.

Institutional ownership stands at 4.23%, reflecting modest professional investor participation. Insider ownership is reported at 0%, and there have been no insider buy or sell transactions over the past 3, 6, or 12 months. The absence of insider ownership may raise alignment concerns, although compensation structures can vary.

Revenue per share has declined over the past year, while both PE and PS ratios are near recent highs. That divergence introduces additional downside sensitivity should fundamentals weaken.

On the positive side, government contract revenue has grown from $19,000 in 2018 to $30,000 in 2022, a cumulative increase of 57.9%. While the absolute figures are small relative to total revenue, the upward trajectory reflects incremental diversification.

Patent activity has fluctuated between 2017 and 2022, with filings peaking at 25 in 2021 before moderating to 18 in 2022. Though not central to the mortgage investment thesis, this activity suggests intermittent innovation initiatives.

Overall risk is characterized less by operational instability and more by structural limitations: high payout ratios, capital returns below cost of capital, valuation expansion, and limited liquidity.

Final Assessment

Atrium Mortgage Investment Corp offers a clear income proposition. A forward yield of 7.8%, consistent quarterly distributions, and generally stable earnings provide a foundation for income-oriented portfolios. Financial reporting quality appears solid, and operational discipline is reflected in a Piotroski score of 7.

Yet beneath the yield lies a more constrained growth and return profile. EPS growth has been modest, revenue projections are flat, and return on invested capital has failed to exceed the cost of capital. Share dilution further tempers per-share expansion. With the stock trading above its intrinsic value and valuation multiples near multi-year highs, investors appear to be paying a premium for yield stability rather than growth.

For long-term dividend investors seeking rising income and economic value creation, the combination of a 90% payout ratio, flat dividend growth outlook, and subdued capital returns may limit total return potential. The stock may continue to serve income-focused holders comfortable with elevated yield and moderate risk, but the margin of safety appears narrow at current levels.

In sum, Atrium Mortgage Investment Corp represents a high-yield security with structural growth limitations. Income is present and presently covered, yet sustainable compounding will likely require either improved capital efficiency or a reset in valuation expectations.