Why Mondelez Is a Dividend Gem in a Priced-Down Market

Exploring resilient brands, stable earnings, and a rare valuation opportunity for income-focused investors.

Investment Thesis: Durable Brands, Income Potential, and a Rare Entry

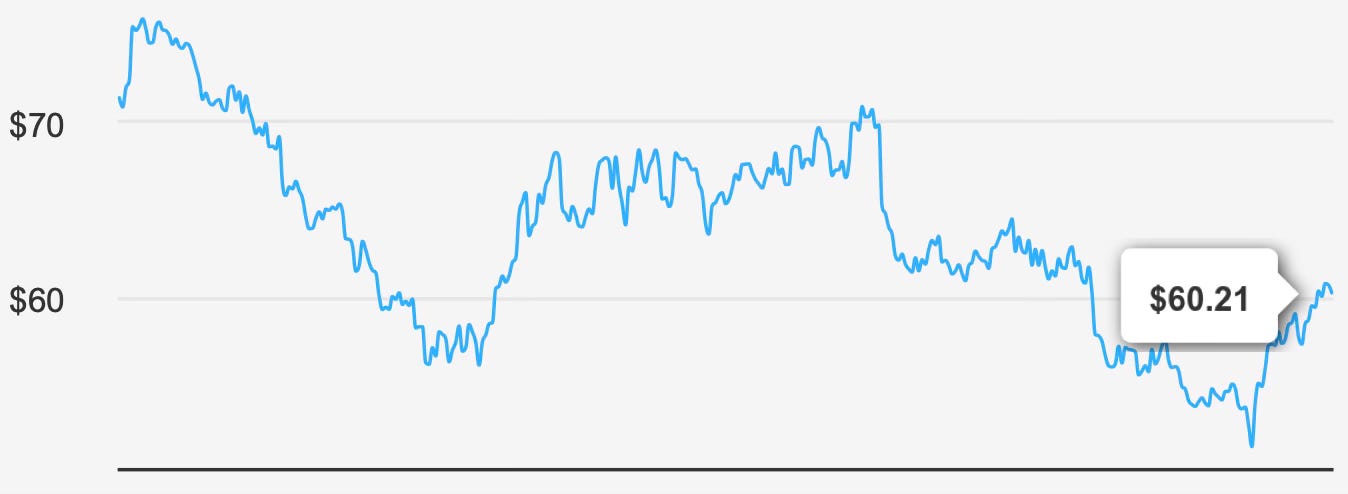

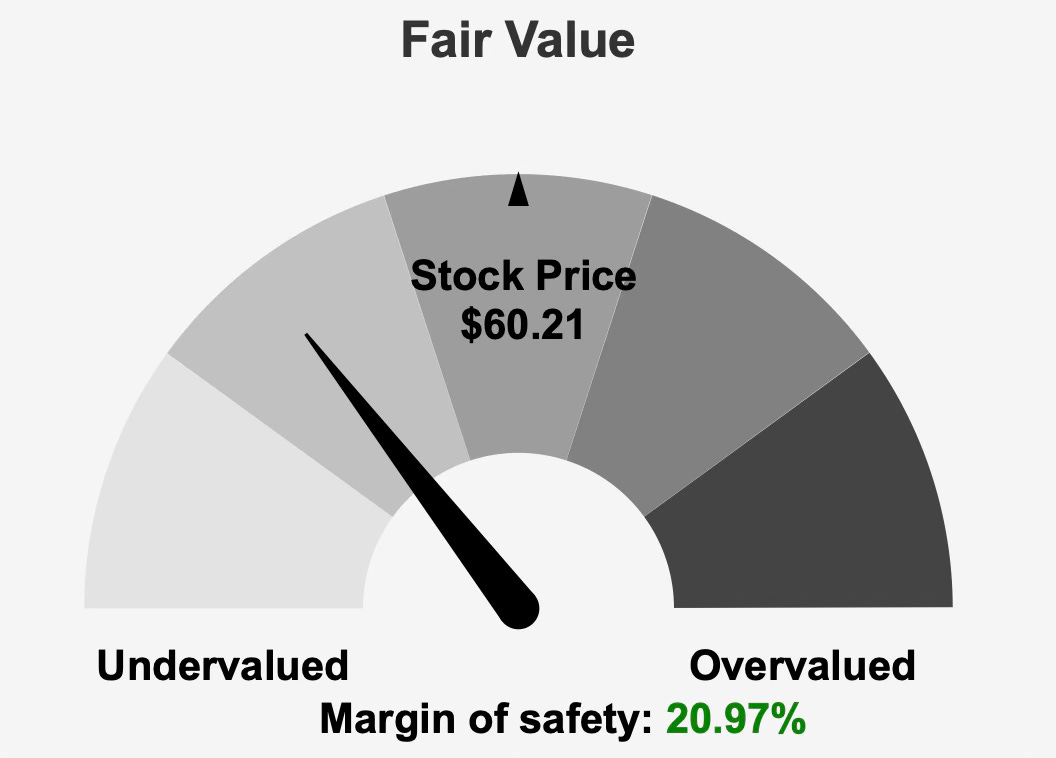

Mondelez International MDLZ 0.00%↑ presents a compelling income-oriented opportunity built on globally entrenched brands, resilient category exposure, and a valuation that has compressed to levels rarely available for a business of this quality. At a share price around $60, the stock trades well below an intrinsic value estimate of $76.2, implying a margin of safety of roughly 21%. This discount reflects investor concern around margin pressure and elevated leverage rather than any fundamental deterioration in demand or brand equity.

The company’s portfolio remains structurally defensive. Biscuits account for nearly half of revenue, chocolate contributes just under one-third, and the remainder is spread across gum, candy, beverages, and grocery. These categories benefit from habitual consumption and strong brand loyalty. Geographically, more than one-third of revenue comes from Europe, roughly one-third from developing markets, and the balance from North America, providing diversification across consumer cycles and currency regimes. This footprint reduces dependence on any single economic environment and supports relatively stable cash generation across cycles.

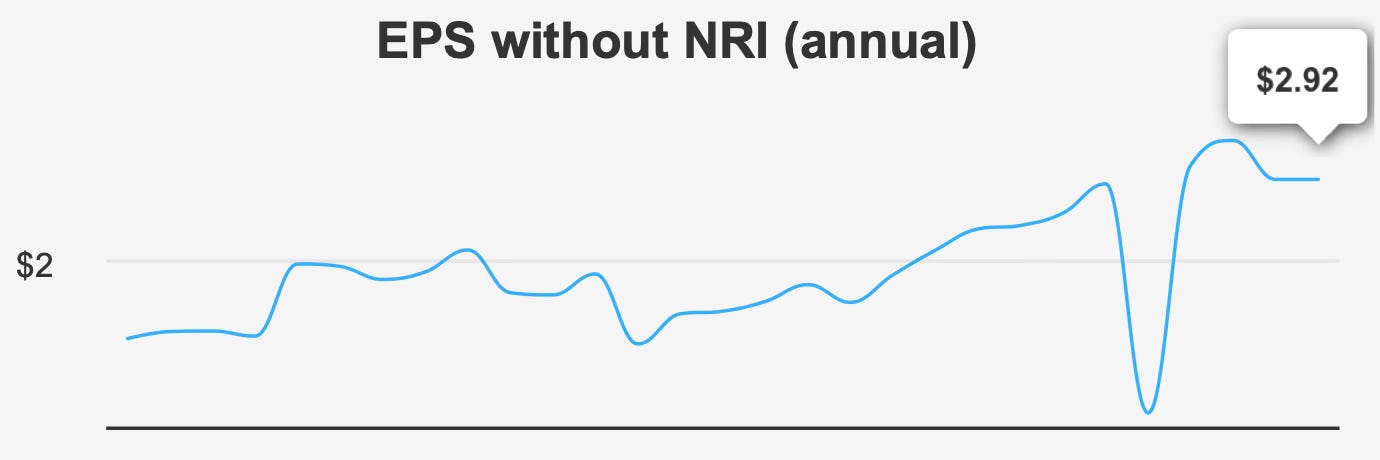

While near-term profitability has softened, Mondelez continues to compound earnings on a multi-year basis. EPS excluding non-recurring items has grown at a 10.7% annual rate over the past five years, a marked improvement over the 2.5% pace achieved over the past decade. This acceleration reflects portfolio streamlining and more disciplined capital allocation since the company’s 2012 separation from Kraft. Share repurchases have further supported per-share growth, with about 2.8% of shares retired over the past year, cushioning EPS even as margins have compressed.

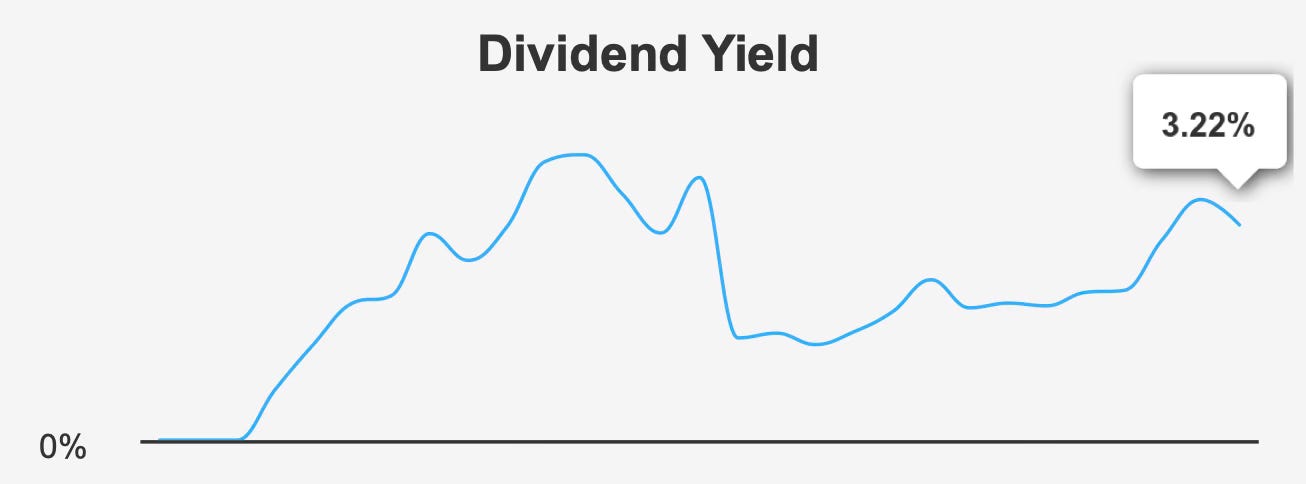

For dividend investors, the current setup is particularly attractive. The forward yield of 3.3% stands well above the company’s 10-year median of just over 2.0%, offering a higher starting income level than long-term shareholders have historically received. Importantly, this elevated yield stems from valuation compression rather than an aggressive payout policy. The dividend profile has matured into a credible income anchor within consumer staples, supported by consistent growth and a payout ratio that remains below long-term norms.

The investment case therefore combines valuation support, durable category exposure, and an income stream that continues to compound at a healthy pace. While leverage and margin trends warrant monitoring, the current price already embeds a meaningful degree of skepticism. For patient investors seeking dependable income with moderate long-term appreciation potential, Mondelez offers a rare entry point into a high-quality franchise at a discounted valuation.

Earnings Momentum & Profitability Trends

Recent results underscore the tension between steady demand and softer profitability. In the fourth quarter of 2025, EPS excluding non-recurring items reached $0.72, modestly below the prior quarter’s $0.73 but up from $0.65 a year earlier, confirming continued year-over-year earnings momentum. Diluted EPS, which includes all items, declined to $0.51 from $0.57 in the prior quarter, reflecting the impact of non-operational factors rather than a collapse in underlying performance.

Revenue trends remain constructive. Revenue per share increased to $8.1 from $7.5 sequentially, pointing to continued demand strength across Mondelez’s core snack categories. Looking forward, earnings are expected to continue expanding, with EPS projected to reach $3.1 next year and $3.4 the following year. Revenue is forecast to approach $42.4 billion by 2028, suggesting mid-single-digit top-line growth remains achievable even in a more normalized pricing environment.

Profitability, however, has been under pressure. Gross margin in the most recent quarter was 28.4%, well below the five-year median of 38.2% and the 10-year median of 39.1%, highlighting the cumulative effect of input cost inflation and competitive pricing dynamics. Operating margins have also declined at an average rate of 5.7% annually over the past five years. These trends indicate that Mondelez has prioritized defending volume and market share, even at the expense of near-term margin performance.

Despite these headwinds, the company’s longer-term earnings trajectory remains intact. EPS excluding non-recurring items has compounded at 10.7% annually over the past five years, demonstrating that margin compression has not derailed the broader growth profile. The contrast with the 10-year EPS growth rate of 2.5% underscores that Mondelez has entered a more favorable earnings phase in recent years, reflecting improved operational discipline and portfolio focus.

Capital returns have provided incremental support. The 2.8% reduction in share count over the past year has amplified per-share growth, partially offsetting margin pressure. While buybacks at elevated leverage levels require caution, they signal management’s confidence in the company’s ability to generate sufficient cash flow through the cycle. Even modest stabilization in margins would materially enhance earnings leverage over the next several years.

Dividend Profile & Sustainability

Mondelez has established itself as a credible dividend growth story within consumer staples. The dividend has compounded at a 10.2% annual rate over the past five years, with a three-year growth rate of 9.7%. The most recent quarterly increase to $0.50 per share from $0.47 reflects management’s confidence in the durability of cash flows despite margin pressure.

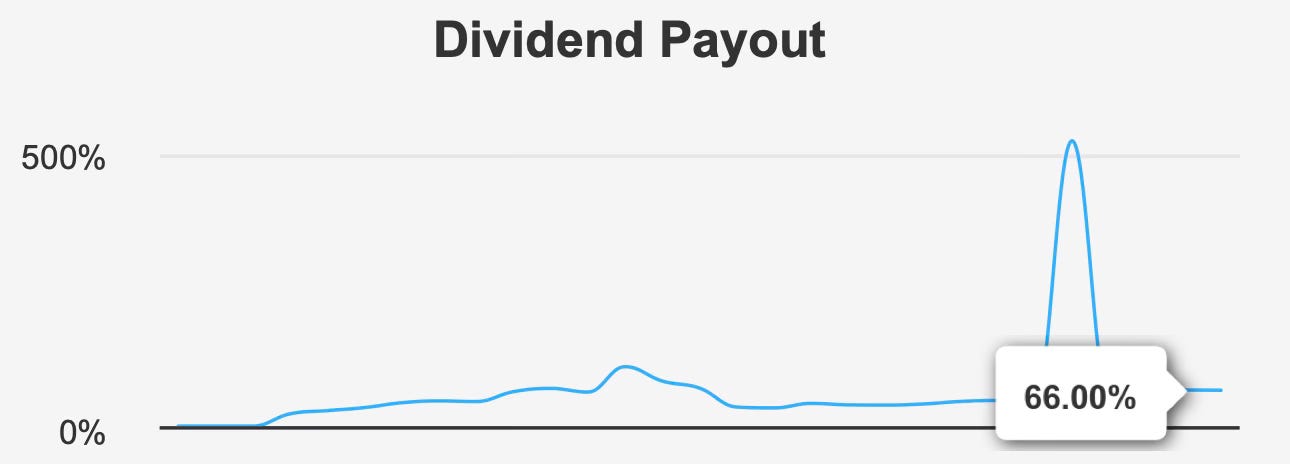

At the current share price, the forward dividend yield of 3.3% stands well above the company’s long-term norm, providing an unusually attractive income entry point. This elevated yield is a function of valuation compression rather than payout expansion. The payout ratio of 66.0% remains below the 10-year median, indicating that dividend growth continues to be supported by earnings rather than by stretching the payout policy.

Dividend coverage of 0.97 suggests coverage is adequate but not excessive, reinforcing the importance of stable operating cash flows in sustaining growth. While coverage is tighter than that of some peers, Mondelez benefits from relatively predictable demand and strong brand equity, which support consistent cash generation.

Looking ahead, dividend growth is expected to moderate to around 8.5% annually over the next three to five years. This moderation reflects a more balanced approach to capital allocation as the company manages leverage and navigates margin normalization. Even at this pace, the dividend would continue to outgrow inflation, reinforcing Mondelez’s appeal as a long-term income compounder rather than a static yield vehicle.

The company’s payment schedule remains predictable, with the next ex-dividend date set for December 31, 2025, and the corresponding payout on January 14, 2026. This consistency enhances the stock’s suitability for income-focused portfolios that value reliability alongside growth. The principal constraint on dividend flexibility remains leverage, with debt-to-EBITDA at 4.4. While this level does not threaten the dividend in the near term, it reduces financial flexibility and reinforces the importance of disciplined capital management.

Valuation: Discounted Price, Margin of Safety, and Forward Growth Potential

Mondelez trades at a valuation that reflects skepticism around margins and leverage rather than a structural reassessment of the franchise. At around $60, the stock sits roughly 21% below an intrinsic value estimate of $76.2, offering a meaningful margin of safety. This discount is notable for a business with globally entrenched brands and stable demand characteristics.

Earnings multiples illustrate the distortion created by near-term margin pressure. The trailing P/E of 32.0x sits well above the 10-year median of 22.3x, but this reflects depressed trailing earnings rather than an elevated share price. The forward P/E of 19.6x presents a more normalized picture, implying that as margins stabilize, the stock’s valuation should revert closer to historical norms.

Other valuation measures reinforce the case for relative undervaluation. The trailing price-to-sales ratio of 2.0x stands below the 10-year median of 2.7x, indicating that investors are paying less for each dollar of revenue than they have historically. The price-to-free-cash-flow ratio of 24.2x also compares favorably with the 10-year median of 27.0x, suggesting that cash flow is being valued more conservatively than in prior cycles. The price-to-book ratio of 3.0x sits in line with historical norms, indicating that asset-based valuation has remained stable even as earnings multiples have fluctuated.

Enterprise value metrics further contextualize the valuation. The trailing EV/EBITDA of 19.5x is close to the 10-year median of 19.1x, suggesting that the market continues to value the operating franchise in line with historical averages despite near-term profitability pressure. Analyst price targets clustered in the mid-$60s imply more modest upside than intrinsic value estimates, reflecting lingering caution around margins and leverage. Even so, the current valuation embeds a level of pessimism that appears disproportionate to the company’s long-term earnings and dividend growth potential.

Risk Assessment & Capital Structure Considerations

The central risks for Mondelez relate to profitability trends and balance sheet leverage. Gross margins have declined at an average rate of 4.4% per year, while operating margins have fallen by 5.7% annually over the past five years. These trends highlight ongoing cost pressures and competitive dynamics that, if persistent, could limit earnings growth and free cash flow expansion.

Financial leverage amplifies these concerns. With debt-to-EBITDA at 4.4, Mondelez carries higher leverage than is typical for consumer staples peers, constraining balance sheet flexibility. The Altman Z-score of 2.3 places the company in the “grey zone,” indicating moderate financial stress. While this does not imply imminent distress, it underscores the importance of monitoring leverage and liquidity, particularly if margin recovery proves slower than expected.

Valuation risk remains tied to earnings volatility. The trailing P/E near 32.0x reflects compressed margins, and any further deterioration in profitability could weigh on sentiment even if the underlying franchise remains intact. That said, financial reporting quality appears strong, with a Beneish M-score of -2.4 suggesting a low likelihood of earnings manipulation, providing confidence in the integrity of reported results.

Ownership structure offers a measure of stability. Institutional investors hold about 87.3% of outstanding shares, reflecting sustained professional interest in the franchise. Insider ownership remains modest, and there has been no insider trading activity over the past year. Liquidity can fluctuate meaningfully, with recent trading volume well below the two-month average, and a dark pool index of 34.5% indicating that a sizable share of trading occurs off-exchange. These dynamics may influence short-term price behavior but are unlikely to alter long-term valuation outcomes for patient investors.

Final Assessment

Mondelez combines durable brand strength with a dividend profile that has matured into a credible long-term income engine. The stock’s valuation has compressed to levels that offer a meaningful margin of safety, lifting the forward yield to 3.3% and creating an attractive entry point for income-oriented investors. Earnings momentum remains intact despite margin pressure, and consensus forecasts point to continued growth over the next two years.

The risks are tangible. Elevated leverage and declining margins limit financial flexibility and require careful monitoring. However, these concerns appear to be well recognized by the market and reflected in the current valuation. The company’s global footprint, habitual consumption categories, and disciplined capital returns provide a stabilizing foundation that supports both earnings and dividends through the cycle.

For long-term investors seeking dependable income with moderate capital appreciation potential, Mondelez offers a rare blend of valuation support and dividend growth within consumer staples. The current setup favors patience, with the prospect of steady income today and incremental upside as margins normalize and valuation multiples recover over time.