Walmart: Durable Franchise, Fragile Valuation

Reliable cash generation and dividend safety collide with stretched multiples

Investment Thesis: Exceptional Business Quality Confronts a Severely Overextended Share Price

Walmart WMT 0.00%↑ stands as one of the most operationally consistent companies in global retail. Since its founding in 1962, the company has evolved into the world’s largest retailer, operating more than 10,700 stores and serving roughly 270 million customers each week. Fiscal 2025 sales exceeded $680 billion, underscoring the scale advantages that continue to shape its competitive moat.

The business model remains fundamentally defensive. Nearly 60% of U.S. revenue comes from groceries, a category largely insulated from economic cycles, while general merchandise contributes roughly a quarter of domestic sales. International operations, anchored in Mexico and expanding in India, provide geographic diversification but do not fundamentally alter the low-margin, high-volume nature of the company’s earnings engine.

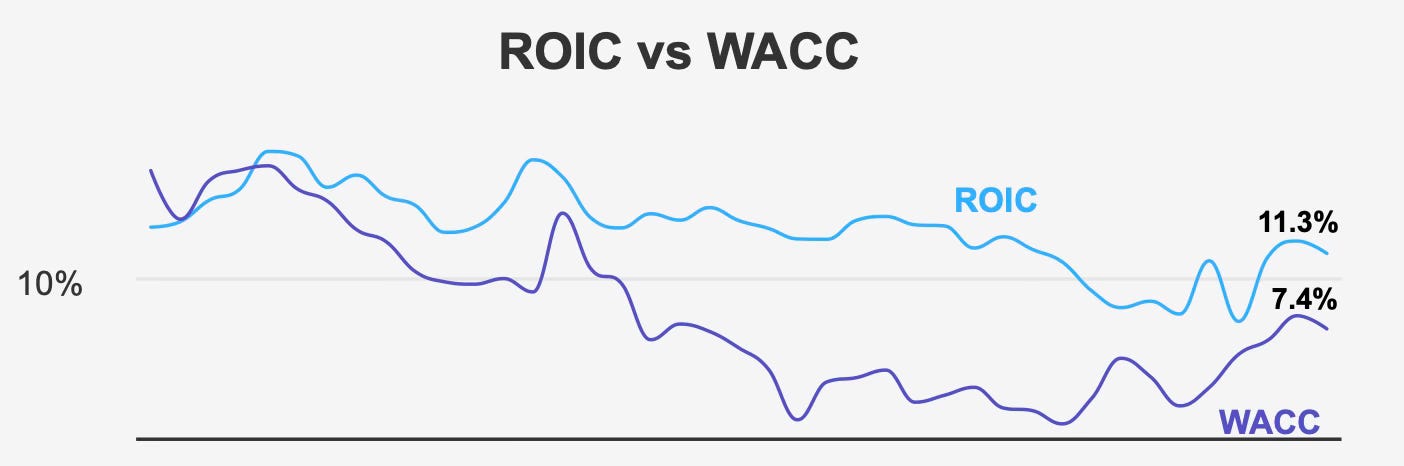

Operationally, Walmart continues to demonstrate economic value creation. Its recent return on invested capital of 11.3% exceeds its weighted average cost of capital of 7.35%, maintaining a healthy spread and confirming disciplined capital allocation. The five-year median ROIC of 10.92% and a five-year median return on equity of 17.37% reinforce a long-standing pattern: Walmart does not grow rapidly, but it compounds reliably.

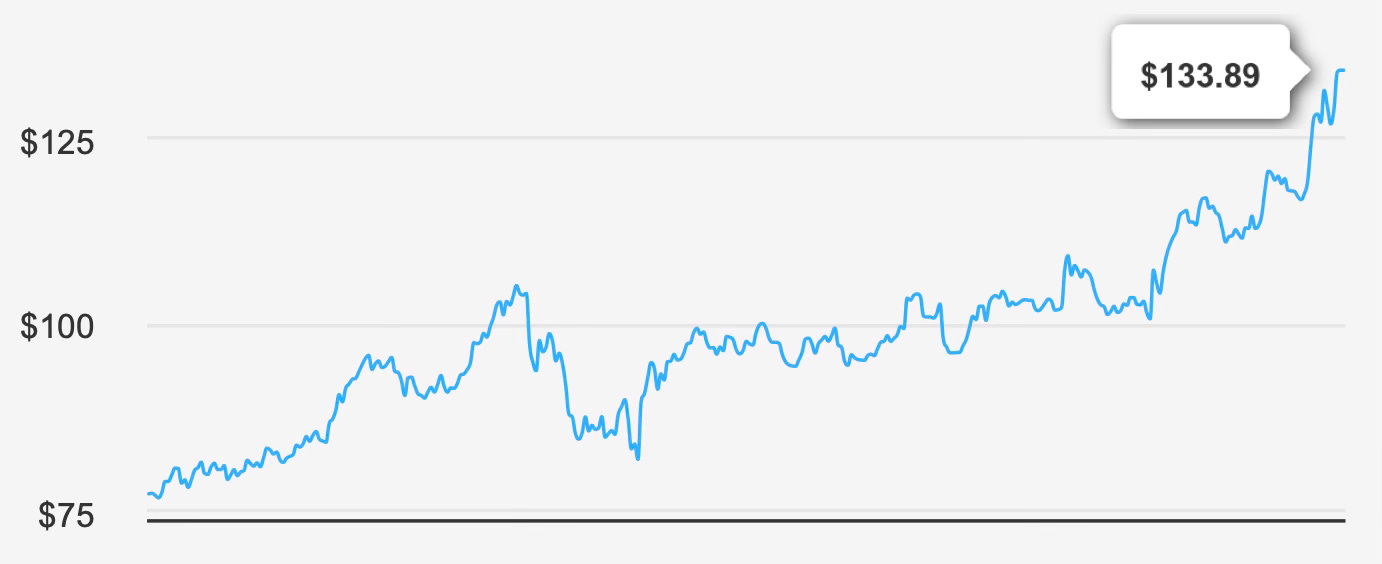

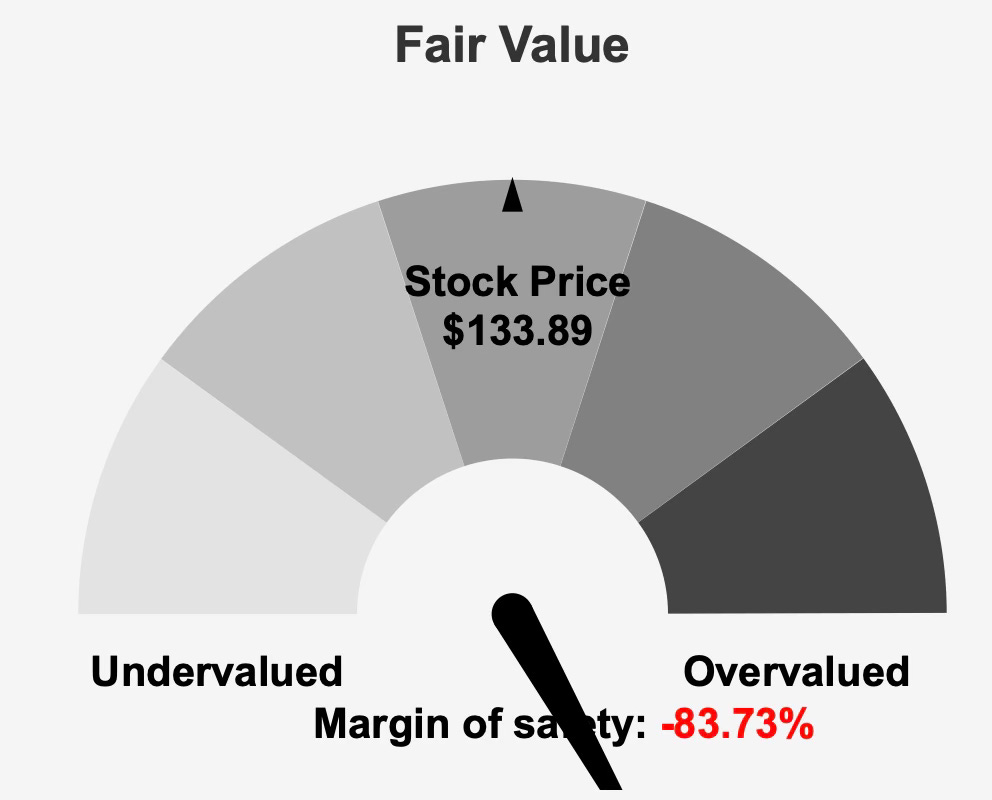

However, the investment case is increasingly defined not by the strength of the enterprise but by the price investors are paying for it. The stock trades around $133 while intrinsic value is estimated at $72.87, implying an 83.7% negative margin of safety.

In other words, the core question is no longer whether Walmart is a high-quality business — it clearly is — but whether the market is pricing it as if it were a high-growth company rather than a mature defensive retailer.

The dividend investor must therefore evaluate Walmart through two opposing realities: an exceptionally stable cash-generating franchise and a valuation that already assumes near-perfect execution for years to come.

Earnings Momentum & Profitability Trends

Walmart’s earnings trajectory reflects a mature company that continues to expand gradually rather than cyclically. In the quarter ending October 31, 2025, adjusted EPS came in at $0.62, improving from $0.58 a year earlier despite declining from $0.68 in the previous quarter. Diluted EPS followed a similar pattern, rising to $0.77 year over year but falling sequentially from $0.88.

This pattern illustrates Walmart’s earnings structure: consistent but not explosive. Revenue per share climbed to $22.406 from $22.131, reinforcing a steady top-line progression rather than sudden expansion.

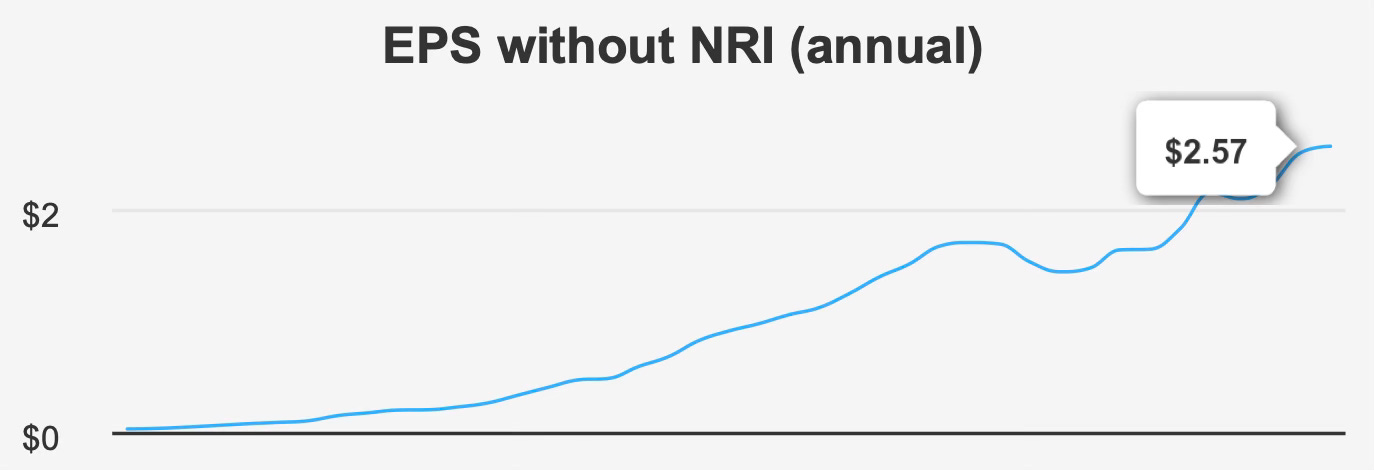

Over longer periods, the trend becomes clearer. Adjusted EPS has compounded at 7.9% annually over five years and 5.1% over ten years — respectable growth for a retailer of its scale but far from the growth profile implied by premium multiples.

Profitability metrics show the real strength of the franchise. Gross margin reached 24.91%, closely aligned with both the five-year median of 24.83% and the ten-year median of 24.98%. Stability at this level is significant in retail, where margins typically compress during inflationary periods.

Capital allocation further supports earnings consistency. Walmart repurchased approximately 0.8% of shares over the past year, with a decade-long average buyback rate near 1.9%. These repurchases steadily enhance per-share growth without materially increasing financial risk.

Forward expectations remain modest but dependable. Analysts project revenue of $712.7 billion in 2026 and $748.0 billion in 2027, while EPS is expected to reach $2.885 next year and $2.947 the year after.

Taken together, Walmart exhibits the characteristics of a high-quality mature compounder: steady margins, incremental growth, and predictable earnings progression. What it does not exhibit is acceleration. Growth is measured in mid-single digits, not double digits.

For valuation purposes, that distinction is critical.

Dividend Profile & Sustainability

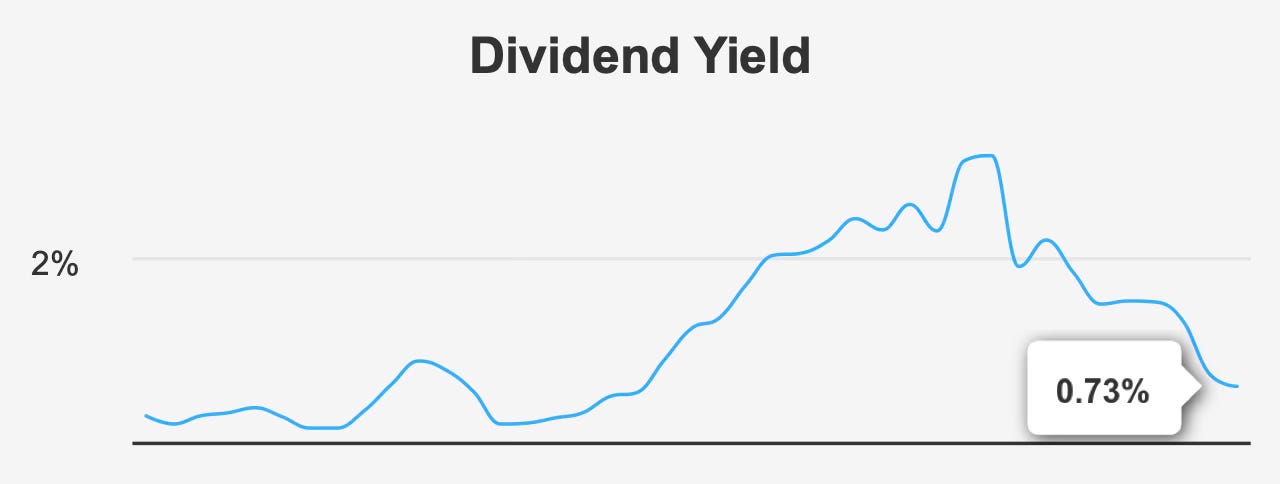

Walmart’s dividend is defined by durability rather than yield. The forward dividend yield stands at 0.7%, well below its ten-year median of 1.62%.

The company recently paid $0.235 per share quarterly, up from $0.2075 a year earlier, reflecting gradual increases consistent with its historical pattern.

Over the past five years, dividend growth averaged 2.9%, accelerating modestly to 4.2% over three years. Analysts expect dividend growth around 7.6% over the next three to five years, supported by rising earnings and conservative payout practices.

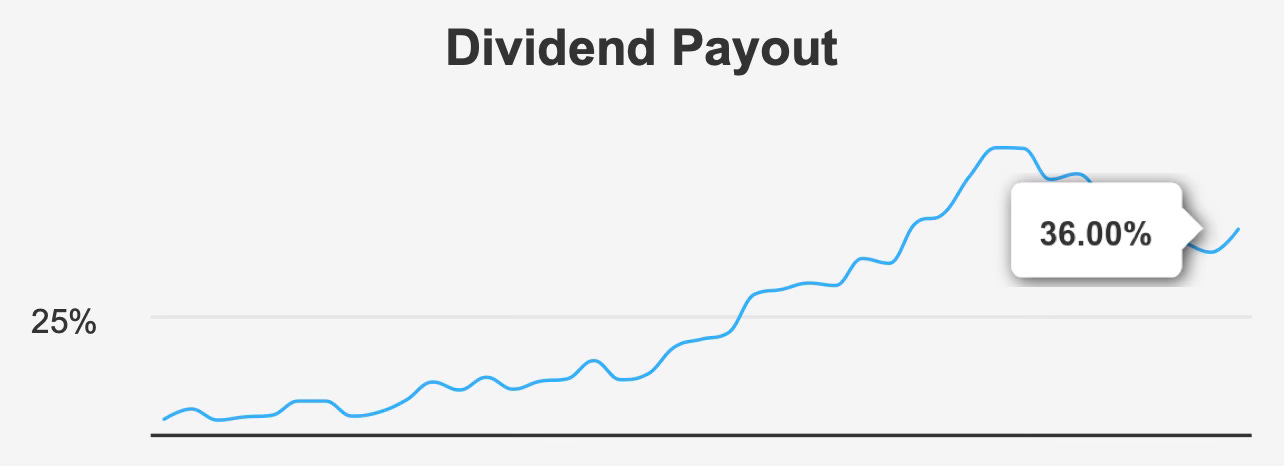

The payout ratio of 36% remains comfortably below typical defensive sector thresholds, while dividend coverage stands at 3.13x.

This matters more than the yield itself. Walmart’s dividend is not designed to maximize income today; it is designed to persist indefinitely. The company retains sufficient capital to fund store investment, e-commerce expansion, and share repurchases without stressing its balance sheet.

Debt metrics reinforce this stability. Debt-to-EBITDA of 1.45 indicates low leverage and strong servicing capacity, particularly within the retail industry.

In practical terms, Walmart’s dividend profile suits investors prioritizing reliability over income. The payment is exceptionally safe, modestly growing, and unlikely to be cut even in recessionary environments. The trade-off is a yield that currently offers limited immediate return.

The dividend is therefore an attribute of financial strength rather than a primary investment attraction at current pricing.

Valuation: Premium Multiples Reflecting Perfection Rather Than Probability

The valuation picture is stark. Walmart trades near $133 compared with an intrinsic value estimate of $72.87, implying an 83.7% negative margin of safety.

Multiple expansion explains this gap.

The trailing P/E sits at 46.8x and forward P/E at 45.2x, both far above the ten-year median of 29.4x.

Enterprise valuation metrics show similar expansion. EV/EBITDA of 24.0x is close to its decade high of 24.14x and substantially above the median of 13.7x.

Balance sheet valuation also reflects aggressive pricing. Price-to-book of 11.1x nearly matches its historical peak and exceeds the median of 4.82x, while price-to-free-cash-flow of 70.6x is more than triple the long-term median of 21.3x.

These figures collectively indicate that investors are currently valuing Walmart less like a mature defensive retailer and more like a high-growth consumer platform.

Yet the company’s fundamentals — mid-single-digit revenue growth and high-single-digit earnings growth — have not materially changed.

Analyst price targets near $118 suggest limited upside from current levels, reinforcing the notion that valuation expansion, rather than earnings acceleration, has driven recent share performance.

For long-term dividend investors, valuation is particularly important because income returns accumulate slowly. Paying excessive multiples significantly reduces total return potential even if the business performs well.

In Walmart’s case, the quality of the enterprise is undeniable. The issue is that the price assumes continued premium status indefinitely.

Risk Assessment & Capital Structure Considerations

Despite valuation concerns, Walmart’s fundamental risk profile remains low.

Financial health metrics support this view. An Altman Z-Score of 6.65 signals strong creditworthiness, while a Piotroski F-Score of 8 indicates operational efficiency.

The Beneish M-Score suggests low risk of earnings manipulation, reinforcing confidence in reported results.

Liquidity is also robust, with average daily trading volume around 33.7 million shares, providing efficient market entry and exit.

Operationally, Walmart continues expanding technological capability. Patent filings rose from 64 in 2016 to 158 in 2023, highlighting ongoing investment in automation and logistics infrastructure.

However, market-based risks are elevated.

Insider activity shows 75 sell transactions over twelve months with no purchases, suggesting internal caution toward valuation levels.

The dividend yield near a decade low also indicates investor enthusiasm has driven price ahead of income generation capacity.

Thus, business risk is minimal, but valuation risk is substantial. Investors face potential multiple compression even if operating performance remains strong.

Final Assessment

Walmart represents a textbook example of a high-quality company that may still be a poor investment at the wrong price.

Operationally, the company excels. It generates returns above its cost of capital, maintains consistent margins, grows steadily, and supports a very safe dividend backed by conservative leverage. Few global businesses match its combination of scale, resilience, and reliability.

For dividend stability, Walmart ranks among the strongest corporations in the public markets.

Yet valuation fundamentally alters the investment outcome. Trading roughly 84% above intrinsic value and at historically elevated multiples across earnings, cash flow, and book value, the stock embeds optimistic assumptions about long-term growth that exceed its demonstrated trajectory.

The result is asymmetry. Downside from valuation normalization is meaningful, while upside depends largely on continued investor willingness to pay a premium for stability.

For long-term dividend investors, Walmart today is less an income investment and more a capital preservation asset priced like a growth stock.

The business remains excellent. The dividend remains secure. The expected returns, however, appear constrained.

In practical terms, Walmart currently fits best on a watchlist rather than a buy list — a company to own at the right price, but not necessarily at this one.