Verizon Communications: High Yield, Low Growth - Income Stability at a Full Price

Evaluating sustainability, balance sheet pressure, and valuation discipline in a slow-growth telecom

1. Investment Thesis: A High-Income Telecom Franchise Trading Above Its Fundamental Worth

Verizon Communications VZ 0.00%↑ operates one of the largest wireless networks in the United States, serving roughly 94 million postpaid and 20 million prepaid phone customers. Wireless services generate approximately 75% of total service revenue and nearly all operating income, anchoring the company’s financial stability. Its fixed-line footprint reaches about 30 million homes and businesses, including roughly 20 million Fios fiber locations, and the recent Frontier acquisition adds network reach to another 15 million locations and 11 million broadband customers.

This scale creates a durable cash-flow engine rather than a growth enterprise. Over the long term, Verizon’s revenue has expanded at only 0.6% annually over five years and 0.3% over ten years, reflecting a mature market structure. The wireless industry’s expected expansion of roughly 4% annually over the next decade provides moderate support, but competitive intensity and saturation limit the company’s ability to translate sector growth into outsized shareholder returns.

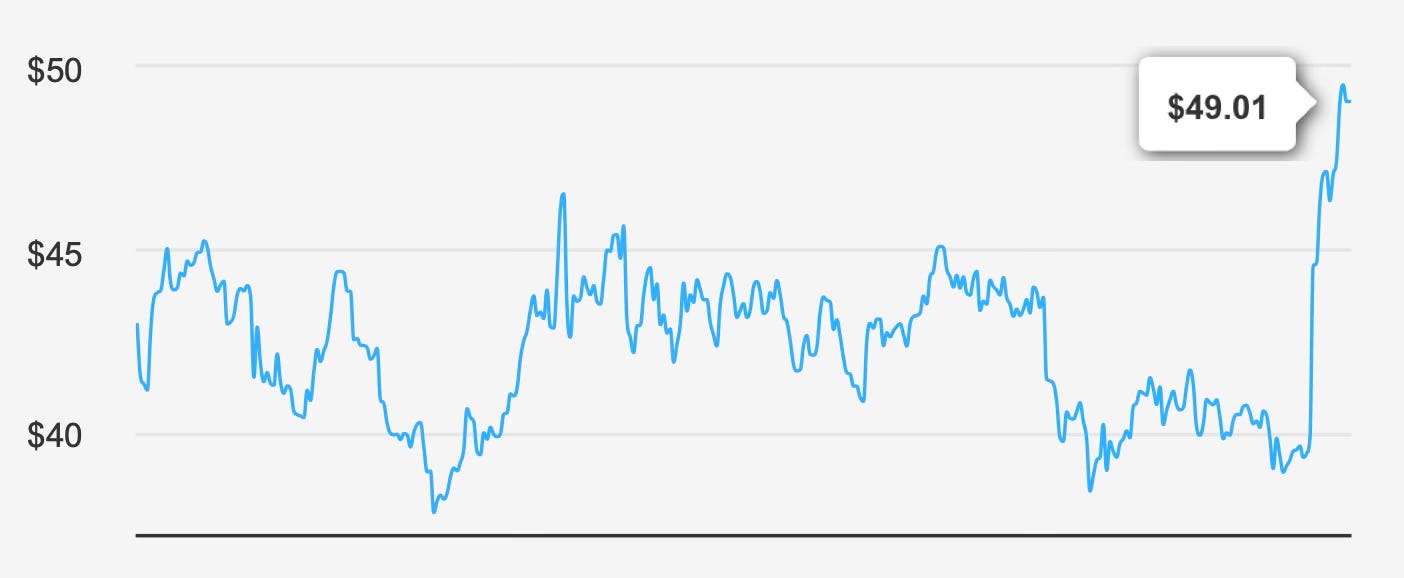

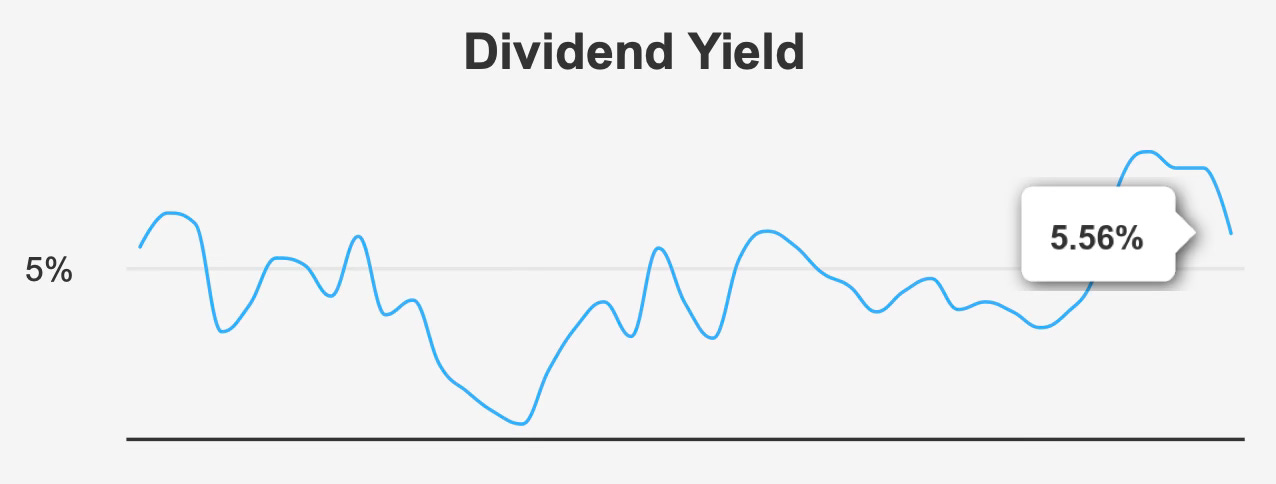

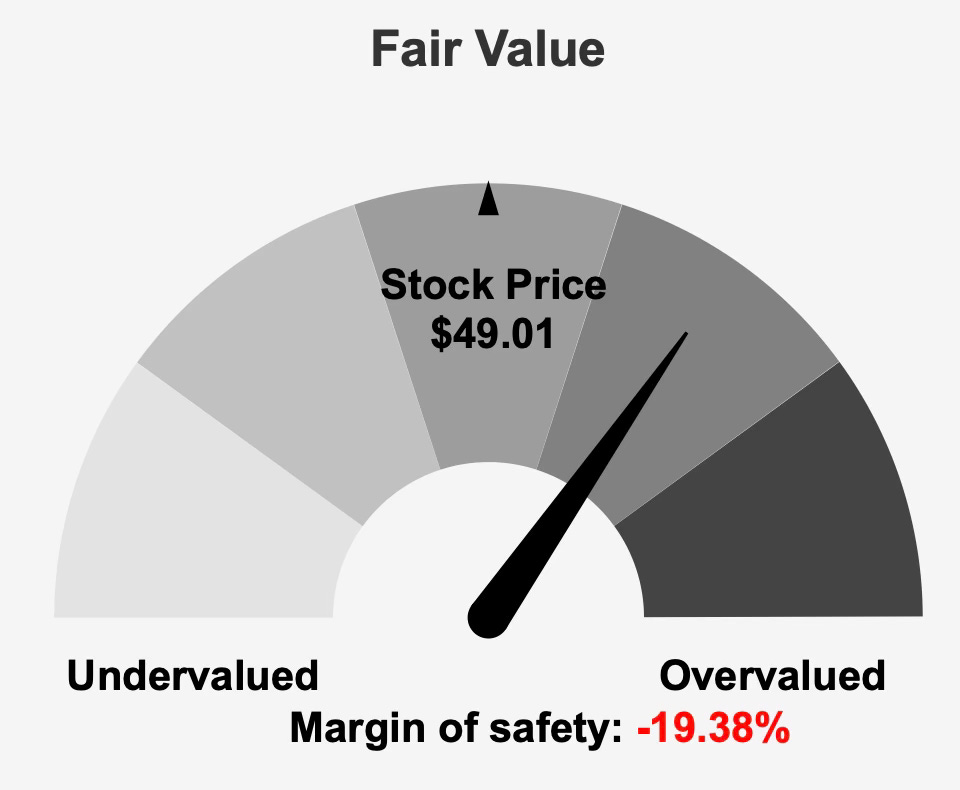

The stock’s primary appeal is income. At a forward dividend yield of 5.76%, Verizon offers one of the higher yields among large-capitalization telecom equities. Yet the investment case becomes complicated when valuation and growth intersect. The shares trade around $49 versus an intrinsic value of approximately $41.05, leaving a negative margin of safety near 19.4%.

In other words, investors are paying a premium for stability rather than acquiring it at a discount.

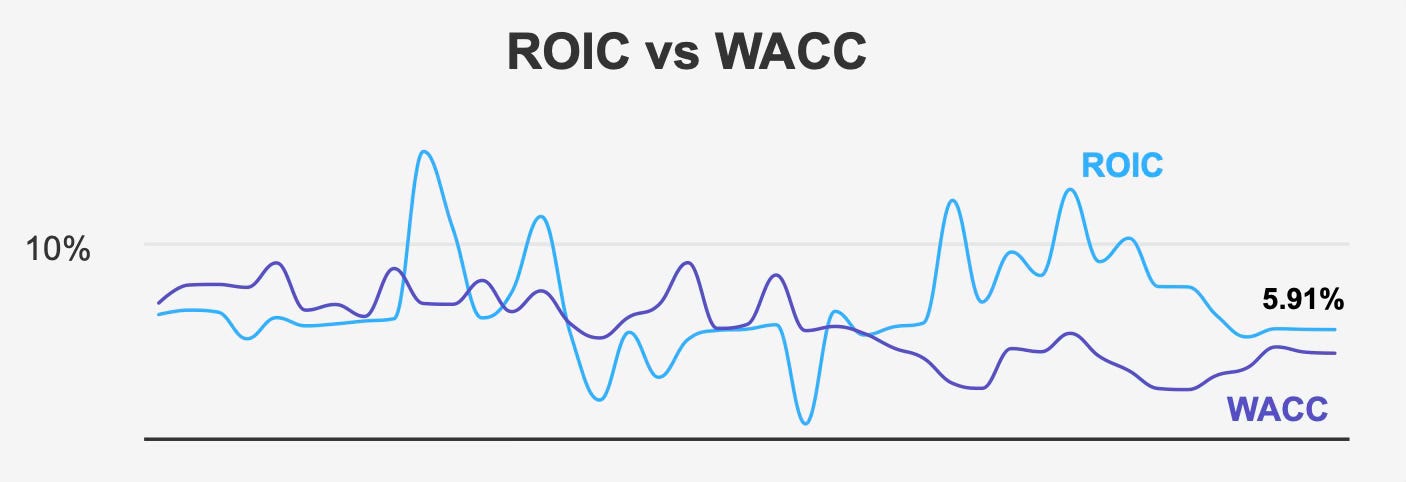

The company’s financial efficiency remains respectable. Return on invested capital of 5.92% exceeds the weighted average cost of capital of 4.78%, demonstrating economic value creation despite modest growth. However, this spread is narrow, implying that incremental investments add value slowly rather than compounding aggressively.

For dividend investors, Verizon represents a classic income-centric security: predictable operations, steady demand, and dependable cash generation. But the absence of growth and limited valuation buffer mean total return potential depends heavily on the dividend itself rather than capital appreciation.

The investment thesis therefore rests on a single trade-off — dependable yield versus limited upside.

2. Earnings Momentum & Profitability Trends

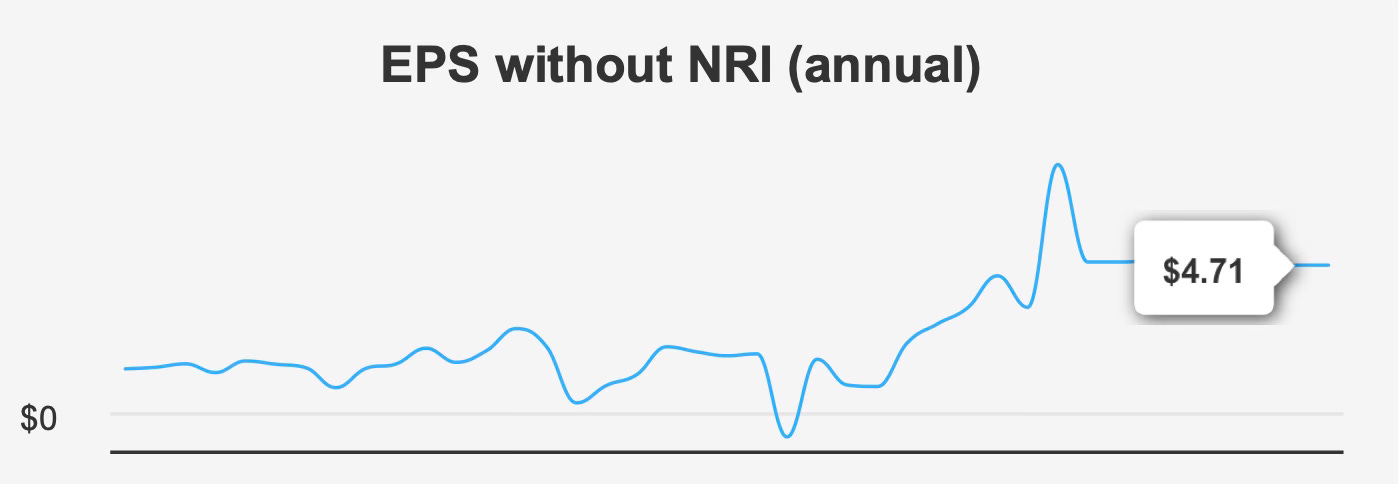

Recent earnings trends illustrate the company’s maturity. Fourth-quarter 2025 adjusted earnings per share were $1.09, down from $1.21 in the prior quarter and slightly below $1.10 a year earlier. Diluted earnings fell more sharply to $0.55 from $1.17 in the previous quarter and $1.18 year-over-year.

Over longer periods, earnings growth has been stagnant. The five-year EPS compound annual rate declined by 3.1%, while the ten-year growth rate averaged only 0.4%. These figures confirm that Verizon’s profitability profile resembles a utility-like cash generator rather than a compounding growth company.

Revenue trends reinforce this conclusion. Revenue per share increased sequentially to $8.589 but showed only marginal improvement from $8.437 a year earlier. The business expands slowly even when customer numbers remain large and stable.

Margins remain steady rather than improving. Gross margin stands at 58.9%, consistent with the five-year median yet below the decade peak of roughly 60.1%. Meanwhile, operating margin has declined at an average annual rate of 2.1% over five years, suggesting gradual cost pressure in a capital-intensive industry.

Capital allocation provides mixed signals. Verizon has not meaningfully reduced its share count; the one-year buyback ratio of negative 0.2% and ten-year ratio of negative 0.4% indicate net share issuance rather than repurchases. Consequently, earnings per share are not benefiting from financial engineering, leaving operational performance as the primary driver of per-share growth.

Looking forward, analysts project earnings improvement to approximately $4.821 next fiscal year and $5.146 the following year. These expectations imply modest recovery rather than acceleration — consistent with a mature telecom stabilizing after heavy investment cycles.

Despite slow growth, profitability quality remains acceptable. Return on equity has averaged about 18.3% over five years, indicating efficient use of shareholder capital relative to peers in capital-intensive infrastructure industries.

Overall, earnings momentum is stable but uninspiring. Verizon generates reliable profits, yet the trajectory resembles inflation-level expansion rather than real compounding. For dividend investors, this matters less for payout stability but significantly for long-term purchasing-power growth.

3. Dividend Profile & Sustainability

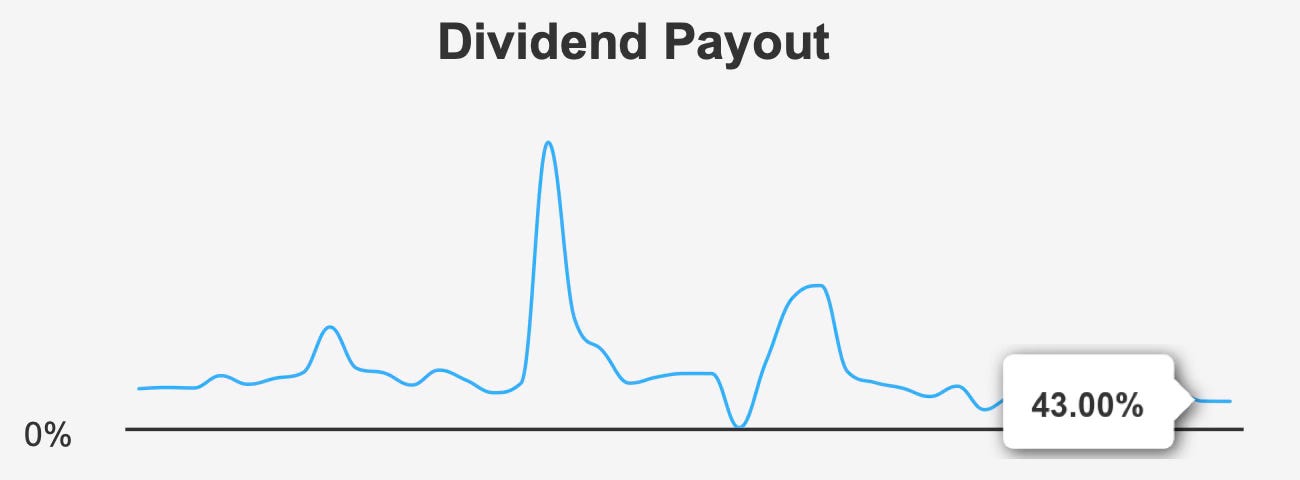

The dividend remains the central component of the investment case. With a forward yield of 5.56%, Verizon offers substantial income relative to broader equities. The payout ratio of roughly 43.0% and coverage near 1.98x suggest the dividend is presently well supported by earnings.

However, historical growth has been weak. The dividend declined at an average annual rate of 2.2% over five years and fell 7.5% over three years. These figures highlight the key distinction between high yield and growing income: Verizon offers the former, not the latter.

Management’s outlook is more optimistic, with projected dividend growth of approximately 11.5% over the next three to five years. That expectation likely reflects anticipated earnings stabilization and moderate revenue expansion rather than structural business transformation.

Debt levels play a decisive role in sustainability. Debt-to-EBITDA stands at 3.81, elevated though manageable for a telecom operator. The leverage limits flexibility — the company can support the current payout comfortably but cannot aggressively expand it without balance sheet improvement.

The payment schedule remains predictable. The next ex-dividend date is April 10, 2026, with payment on May 1, 2026. Consistent quarterly distributions reinforce the company’s income-oriented profile.

In summary, the dividend appears secure but not rapidly growing. Investors receive steady income, yet long-term income expansion depends on modest earnings recovery rather than structural growth. The stock behaves more like a bond substitute than a dividend compounder.

4. Valuation: Market Price Reflects Stability Rather Than Opportunity

Valuation presents the central challenge for prospective investors. At approximately $49, the shares trade meaningfully above intrinsic value of about $41.05, implying a negative margin of safety near 19.4%.

Traditional multiples appear reasonable at first glance. The trailing price-to-earnings ratio around 12.1x sits close to the decade median of 11.8x, while the forward multiple of roughly 10.0x suggests modest earnings improvement. Enterprise value to EBITDA near 7.8x aligns almost perfectly with its long-term norm.

Yet these seemingly fair multiples must be interpreted in context. When a business exhibits near-zero real growth, even average valuation levels can represent overpayment because future returns rely almost entirely on income rather than expanding earnings power.

The price-to-book ratio of about 2.0x sits well below its historical median of 3.4x, which may appear attractive. However, book value for telecom operators is heavily influenced by depreciating infrastructure, limiting the usefulness of that metric for return expectations.

Analyst price targets around $49.84 cluster near the current market price, reinforcing the view that the stock is fairly valued relative to prevailing sentiment but not discounted relative to intrinsic worth.

For dividend investors, valuation determines long-term income return. Buying a 5.8% yield at a premium reduces forward yield on cost if earnings stagnate. The stock therefore offers income reliability but limited valuation upside.

5. Risk Assessment & Capital Structure Considerations

Verizon’s risk profile is shaped primarily by leverage and industry structure rather than business volatility.

The Altman Z-score of 1.31 places the company in the distress zone, signaling elevated financial risk within a two-year horizon despite stable operations. Telecom infrastructure requires continuous capital investment, and leverage magnifies cyclical pressure even in defensive industries.

Operational trends reinforce caution. Operating margins have declined approximately 2.1% annually over five years, indicating persistent cost pressure. Meanwhile, valuation ratios such as price-to-sales and price-to-earnings sit near recent highs, suggesting limited downside protection if performance weakens.

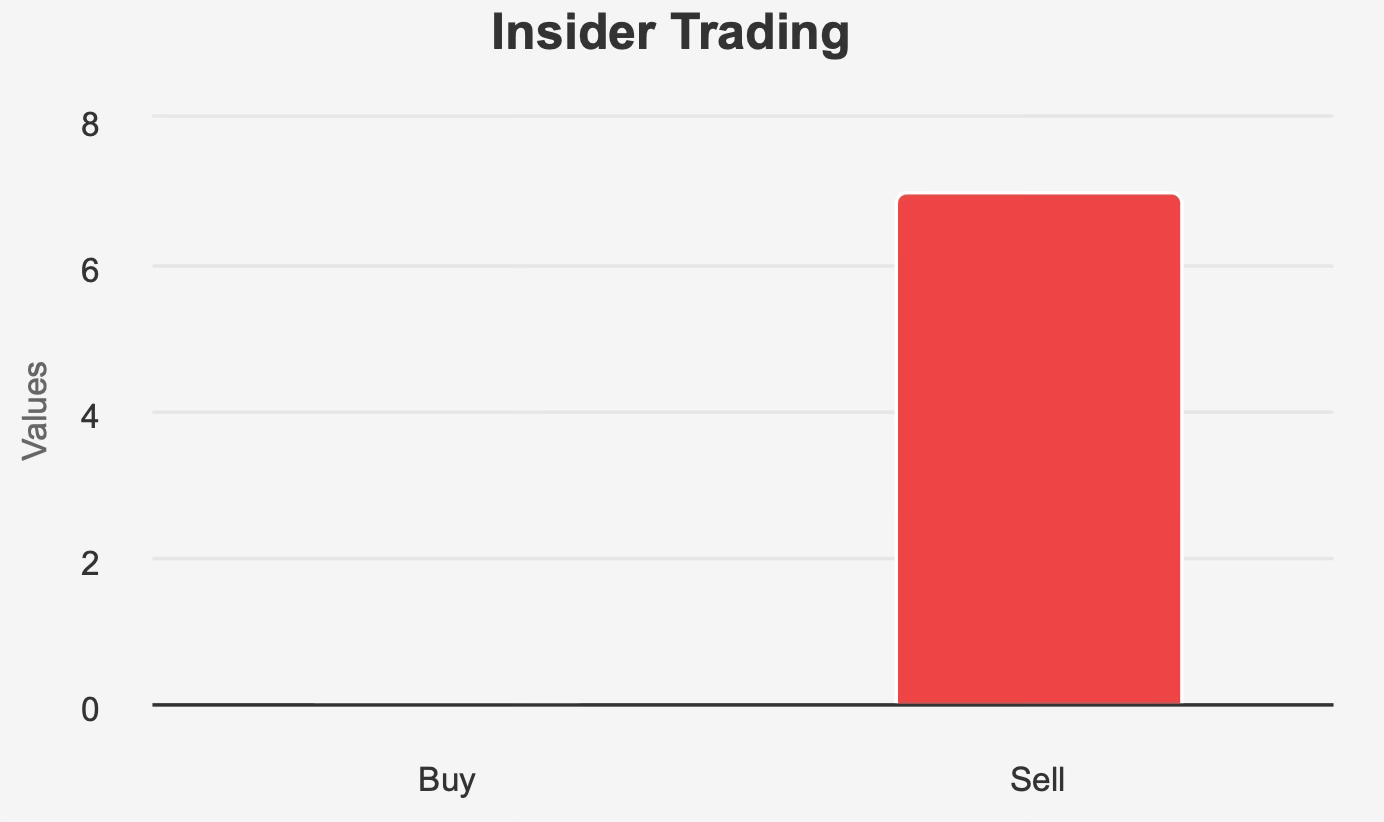

Insider behavior also warrants attention. Over the past year, insiders executed seven sales and no purchases, implying limited internal conviction at current pricing. Institutional ownership remains strong at 66.5%, but insider ownership is only 0.06%, reducing alignment with shareholders.

On the positive side, accounting quality appears reliable, with a Beneish M-Score of −2.69 indicating low manipulation risk. Liquidity is robust, with average daily trading volume around 33.2 million shares, supporting market stability.

Another emerging uncertainty involves government contracts, which peaked above $1.45 billion in 2023 but are projected to decline significantly by 2026. This shift may modestly pressure revenue diversification.

Overall, risks are not existential but structural: leverage, slow growth, and pricing competition in a saturated industry.

Final Assessment

Verizon Communications represents a dependable income security rather than a total-return compounder. Its nationwide network scale, stable profitability, and strong customer base provide consistent cash generation capable of supporting a dividend yield near 5.8%. The payout ratio around 43% and adequate coverage confirm near-term sustainability.

However, long-term investors must balance stability against valuation and growth constraints. Revenue expansion is minimal, earnings growth historically flat, and leverage elevated. While the company generates returns above its cost of capital, the spread is narrow, limiting intrinsic value compounding.

The most significant concern is valuation discipline. With the shares trading meaningfully above intrinsic value, investors are effectively prepaying for safety. In such cases, total return largely equals dividend yield, leaving little margin for appreciation or protection against interest-rate competition.

Consequently, Verizon suits investors prioritizing predictable income and low volatility rather than those seeking rising purchasing power or capital growth. The stock functions best as a yield anchor within a diversified portfolio, not as a primary engine of long-term wealth creation.

The overall outlook supports a neutral stance: a reliable dividend supported by stable operations, offset by modest growth and limited valuation upside.