UnitedHealth Group: A High-Yield Opportunity Trading at a Deep Discount

A Market Leader Trading Like a Problem Child

Investment Thesis: Deep Value Meets Durable Income

UnitedHealth Group UNH 0.00%↑ stands as one of the largest private health insurers globally, serving roughly 51 million members as of December 2024, including approximately 1 million outside the United States. That scale is not just impressive on paper; it underpins pricing power, administrative leverage, and bargaining strength across providers and pharmaceutical partners. In healthcare, size matters — and UnitedHealth has it in abundance.

The company’s structure is equally important. Its core insurance operations are complemented by the Optum franchises, creating a vertically integrated platform spanning pharmacy benefits, outpatient care, and advanced analytics. This combination allows UnitedHealth to capture value across multiple points of the healthcare chain rather than relying solely on underwriting margins. In practice, that diversification dampens volatility and enhances earnings durability — a critical feature for dividend-focused investors.

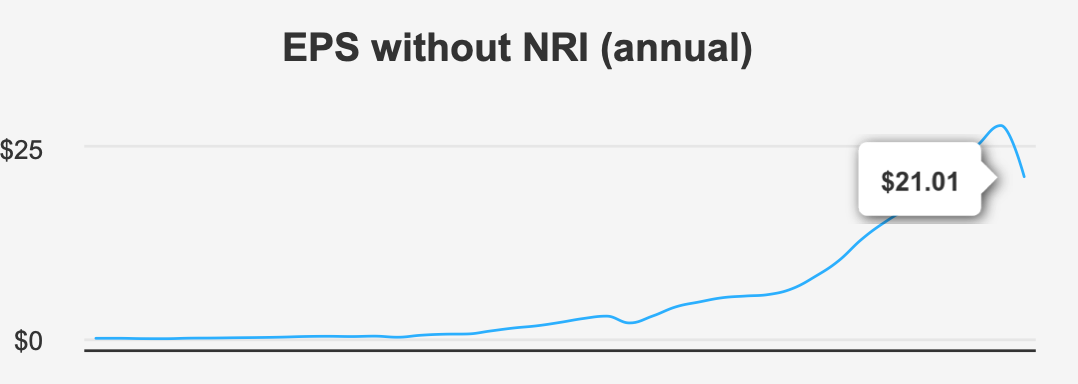

From a growth standpoint, the company has compounded revenue at 12.1% over the past five years and 11.7% over ten years. Earnings have expanded even faster, with EPS (excluding non-recurring items) compounding at 13.5% over five years and 17.6% over a decade. That spread between revenue and earnings growth reflects operating leverage and disciplined capital allocation — traits that don’t happen by accident.

2. Earnings Momentum & Profitability Trends

The most recent quarter, ending September 30, 2025, was more challenging. EPS excluding non-recurring items declined to $2.92 from $4.08 in the prior quarter and from $7.15 a year earlier. Diluted EPS followed suit, coming in at $2.59 versus $3.74 in Q2 and $6.51 year-over-year. Sequential weakness deserves attention, especially in a sector where investors prize predictability.

That said, revenue per share increased to $124.63 from $122.66 in Q2 and $108.41 the prior year. Top-line momentum remains intact, suggesting that margin pressure — rather than demand erosion — is driving the earnings compression. Gross margin has compressed to 19.7%, the lowest level in a decade and below the 10-year median of 23.8%. A declining margin profile, particularly at an average rate of –1.4% annually over three years, warrants monitoring.

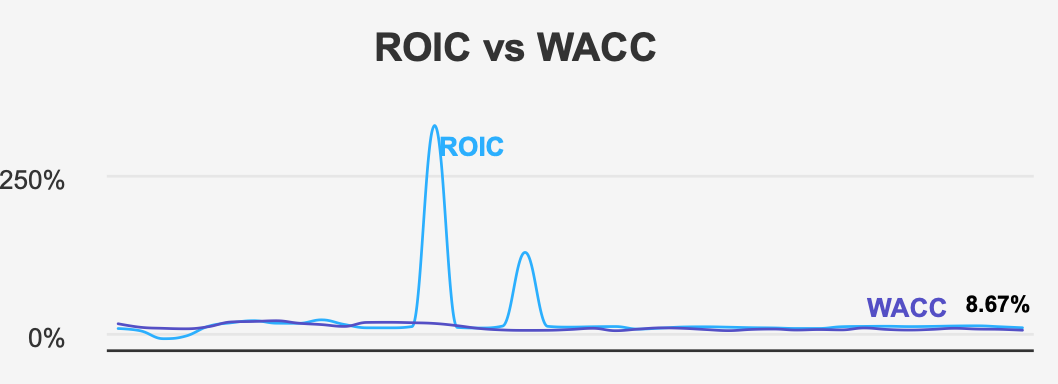

Encouragingly, returns on capital remain healthy. The most recent ROIC stands at 8.7%, comfortably above the current WACC of 4.8%. Over five years, median ROIC was 10.9% against a WACC of 6.2%, indicating sustained value creation. A 5-year median ROE of 25.2% reinforces that capital efficiency remains a core strength. Even in a tougher margin environment, the company is still generating economic profit.

3. Dividend Profile & Sustainability

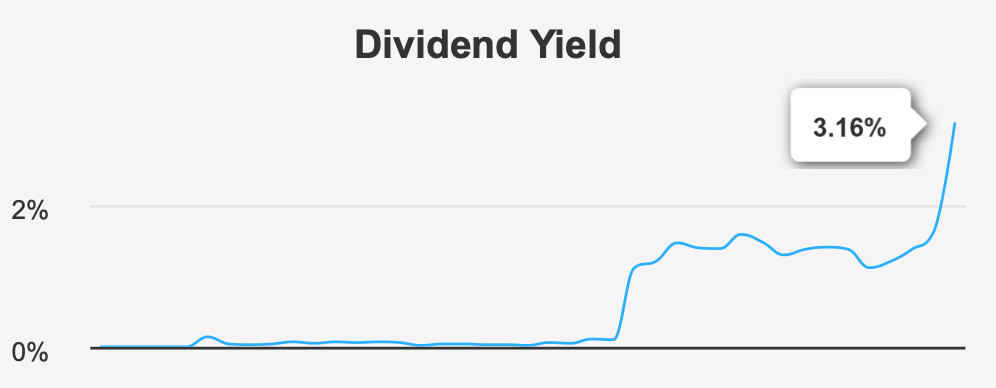

For income-oriented investors, UnitedHealth’s dividend record is compelling. The forward dividend yield stands at 3.2%, supported by a quarterly dividend of $2.21 per share. Over the past five years, dividends have grown at 14.6%, with a 3-year growth rate of 13.5%. That pace is robust, especially within a mature healthcare industry projected to grow at roughly 5–6% annually over the next decade.

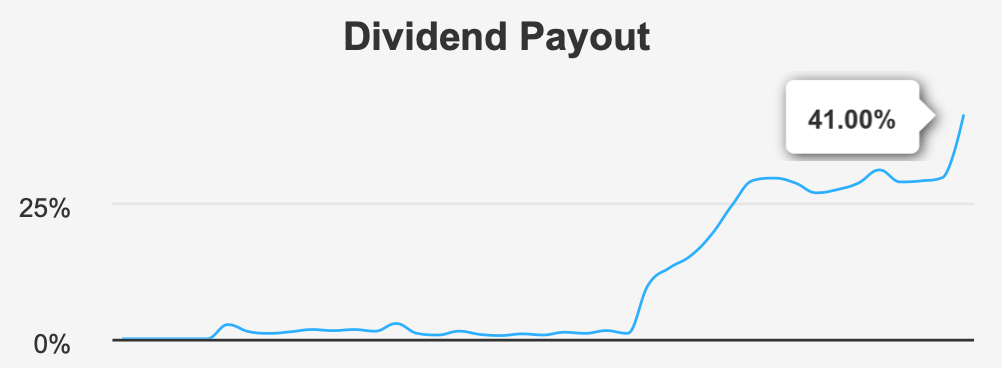

The payout ratio sits at 41.0%, well below historical peaks and medians, indicating room for continued distributions. Dividend coverage stands at 2.2x, suggesting earnings comfortably support current payments. Debt-to-EBITDA is 2.6x — moderate leverage, but manageable within the context of consistent cash generation.

Share repurchases also contribute to shareholder returns. The 1-year buyback ratio was 1.9%, notably above the 10-year average of 0.4%. That incremental reduction in share count enhances per-share metrics and strengthens dividend sustainability over time. Looking ahead, dividend growth is expected to moderate to roughly 4.4% over the next three to five years — a slowdown, yes, but still aligned with long-term earnings expansion.

4. Valuation: A Rare Compression in a Quality Franchise

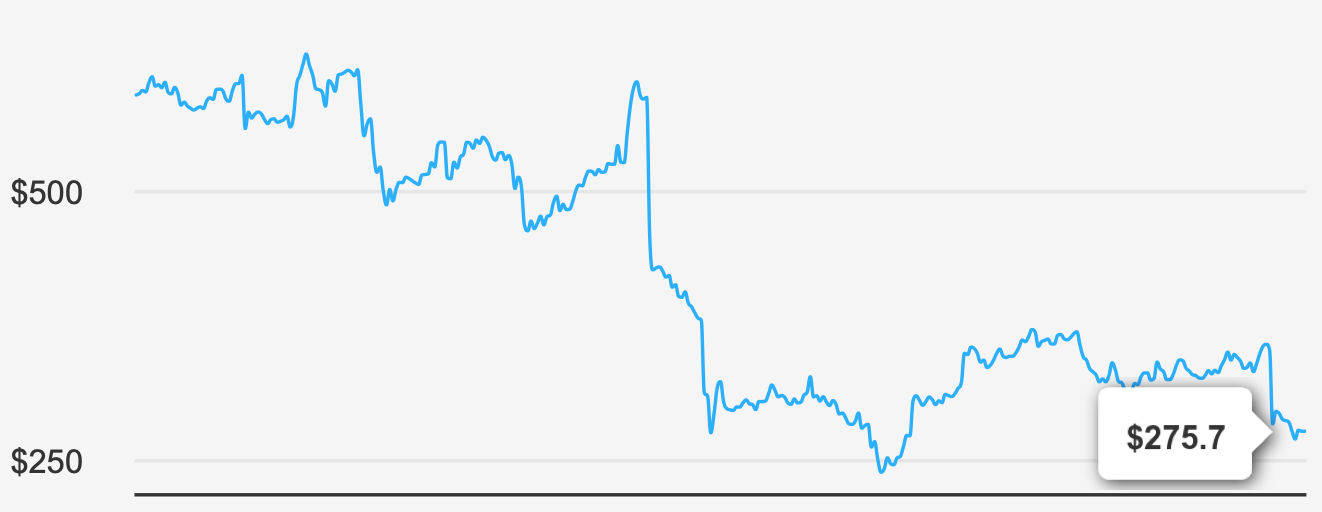

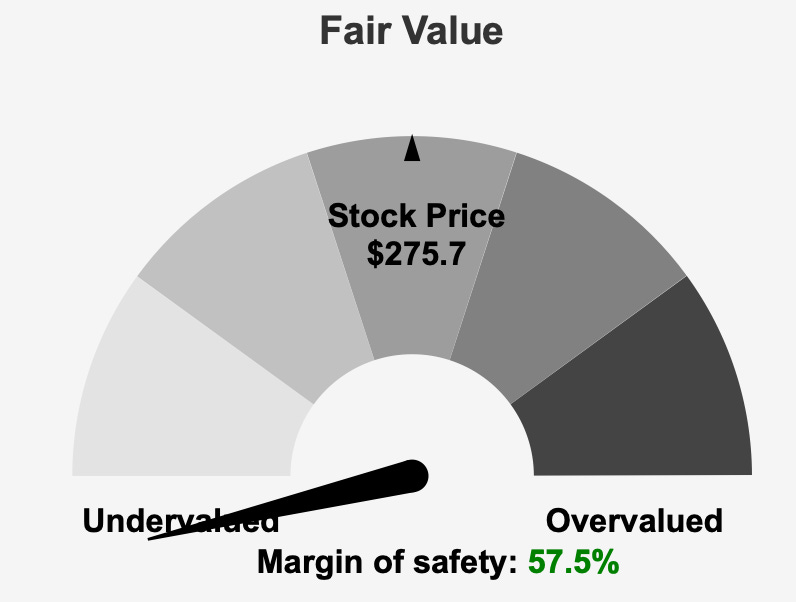

At a current price of $275 and a market capitalization of $249.74 billion, UnitedHealth trades at 14.4x trailing earnings and 15.4x forward earnings. Both sit well below the 10-year median P/E of 21.9x. For a company with double-digit historical EPS growth and durable competitive positioning, that multiple compression is notable.

Other valuation measures tell a similar story. The EV/EBITDA ratio of 10.1x compares favorably to the 10-year median of 14.1x. Price-to-sales stands at 0.6x versus a 10-year median of 1.2x. The price-to-free-cash-flow ratio of 14.5x and price-to-book of 2.6x are both near historical lows. Collectively, these metrics suggest that the market is pricing in a more pessimistic scenario than long-term fundamentals might justify.

An intrinsic value estimate of $648.72 implies a 57.5% margin of safety relative to the current price. While price targets have recently drifted lower to $366.62 from $398.75 a month prior, analyst sentiment remains broadly constructive, with 30 ratings still positive. In short, valuation reflects caution — perhaps excessive caution — rather than structural deterioration.

5. Risk Assessment & Capital Structure Considerations

No equity is without risk. Over the past three years, UnitedHealth increased its long-term debt by $30.1 billion. Combined with contracting gross margins, this raises legitimate questions about financial flexibility. The Altman Z-score of 2.73 places the company in the so-called grey zone. It does not signal distress, but it is not pristine either.

Offsetting these concerns are strong quality indicators. A Piotroski F-score of 7 reflects solid operational health, while a Beneish M-score of –2.26 suggests a low likelihood of earnings manipulation. Institutional ownership stands at 82.6%, reinforcing confidence among large investors. Insider activity has been modestly positive over 12 months, with five buys versus two sells.

Liquidity remains strong, with recent daily volume of 10,211,082 shares compared to a two-month average of 9,175,675. The Dark Pool Index of 32.7% indicates meaningful institutional participation.

Final Assessment

UnitedHealth Group combines durable scale, historically strong capital returns, and a shareholder-friendly dividend policy. Margins have tightened and debt has risen, yet economic value creation persists, and valuation has compressed materially. Trading at 14.4x earnings with a 3.2% yield and a 57.5% margin of safety, the stock reflects elevated caution.

For long-term dividend investors willing to tolerate near-term volatility, the risk-reward profile appears asymmetric. The market is pricing in uncertainty; the fundamentals suggest resilience.