Pricing Power vs. Price Risk: A Dividend Investor’s Dilemma in Altria

A resilient dividend franchise trading above its intrinsic worth

1. Investment Thesis: A Durable Cash-Flow Franchise Trading Above Its Economic Value

Altria MO 0.00%↑ remains one of the most structurally predictable businesses in the public equity market. Its core operations — cigarettes, smokeless tobacco, cigars, and reduced-risk nicotine — generate stable demand characteristics that have historically translated into dependable earnings growth and unusually high margins. The company maintains leading positions across its categories, including the dominant cigarette brand in the United States, while also holding equity stakes in adjacent industries such as brewing and cannabis.

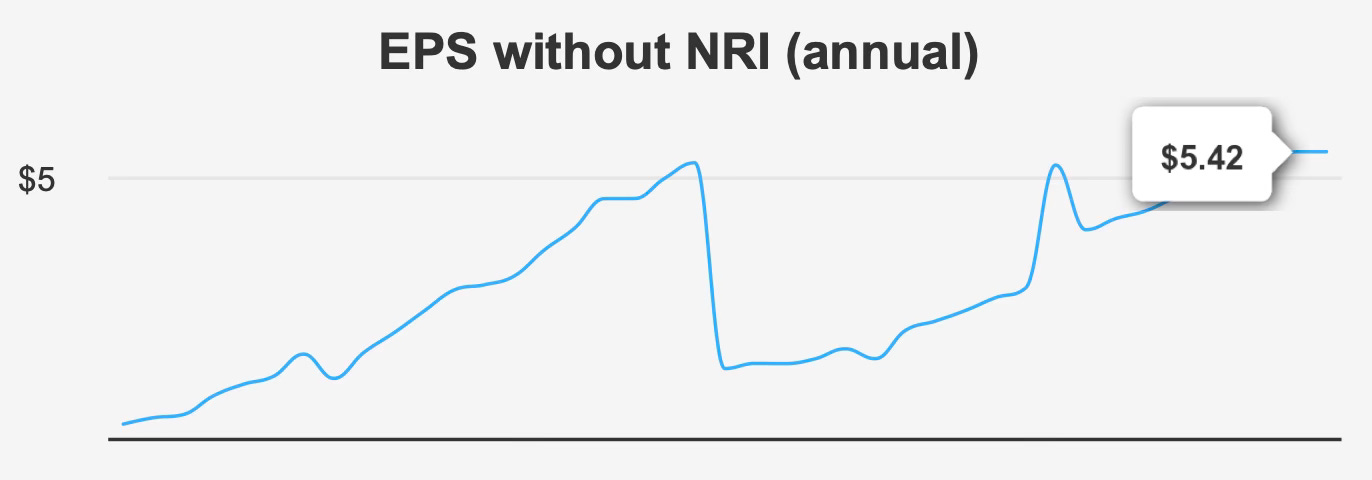

The investment case therefore begins with quality rather than growth. Revenue expansion has been modest over long periods, increasing roughly 1.3% annually over five years and 2.3% over ten years. Yet earnings have compounded faster, with adjusted EPS expanding at a 4.2% five-year rate and 5.4% over ten years. The difference reflects a classic tobacco model: pricing power, cost discipline, and capital returns offset declining consumption volumes.

Recent operating performance reinforces that pattern. The most recent quarter delivered adjusted EPS of $1.30 compared with $1.29 a year earlier. Revenue per share also edged higher year-over-year. While quarter-to-quarter earnings fluctuated, the longer trend remains steady rather than cyclical.

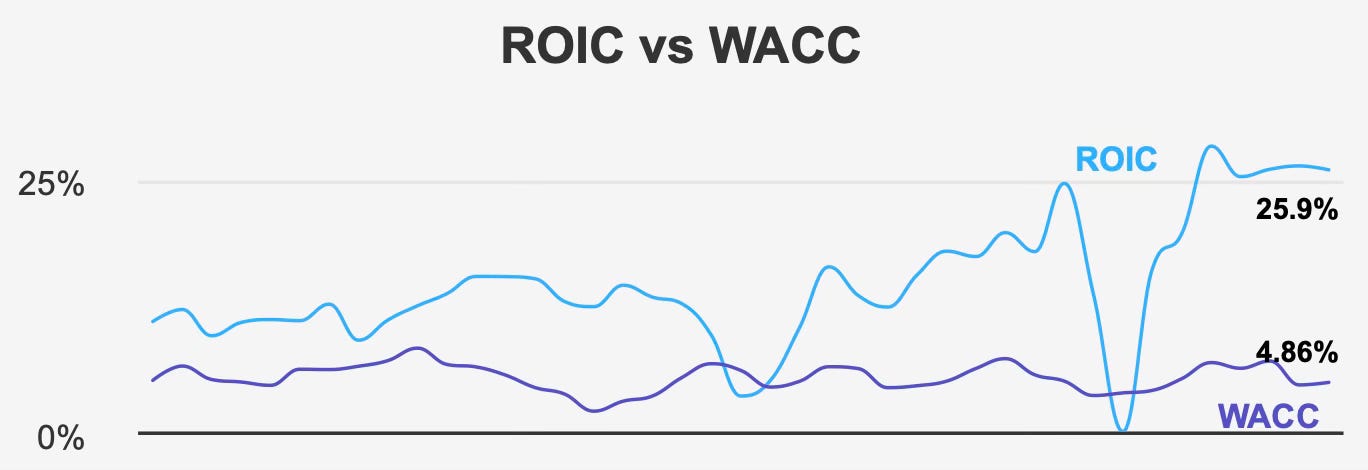

From an economic standpoint, the company produces extraordinary returns on capital. Current return on invested capital sits near 25.9%, far above its cost of capital around 4.9%. That spread signals durable competitive advantage. Businesses rarely sustain a roughly twenty-point economic profit gap unless pricing power is embedded in the industry structure.

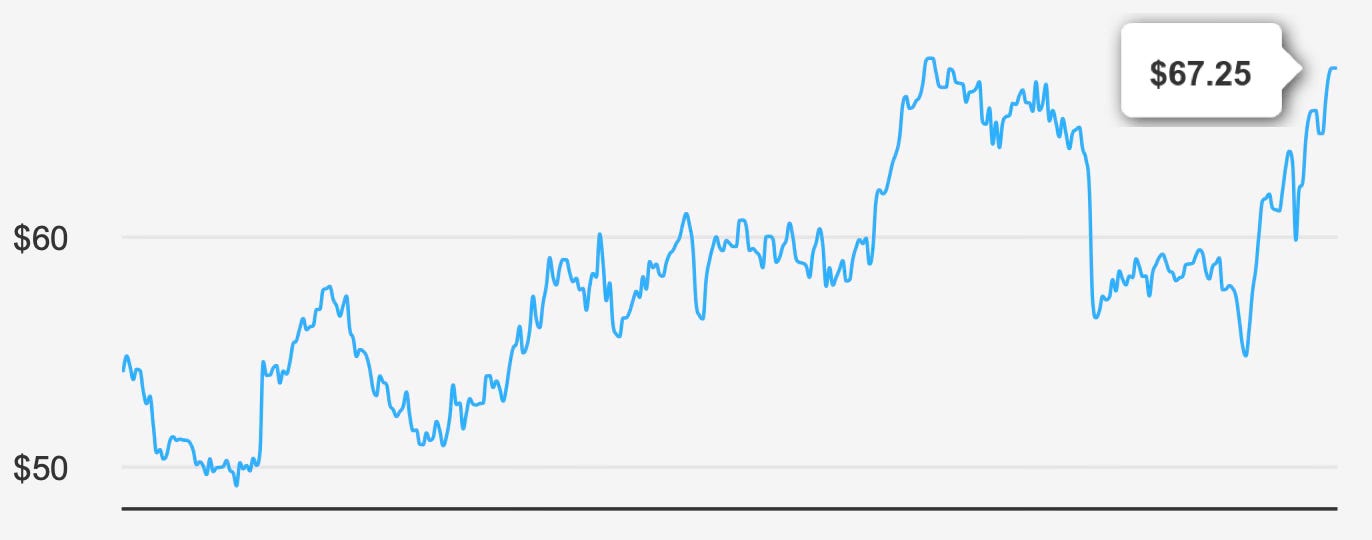

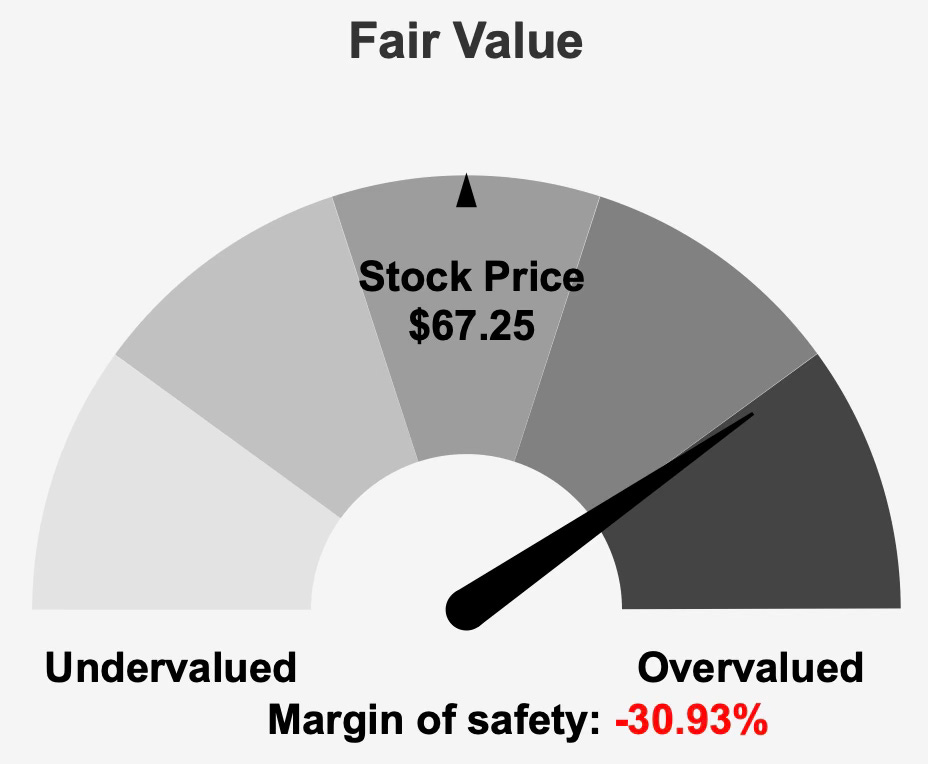

The challenge is valuation rather than quality. With shares trading around $67 against an intrinsic value estimate near $51, investors currently pay roughly 31% above fair value. The market is capitalizing stability at a premium multiple despite modest growth expectations. Over the next decade, industry growth is expected to average 3–4% annually, aligning with the company’s historical earnings trajectory.

The core thesis therefore resolves into a simple contrast: Altria is a stable, highly profitable enterprise, but the stock price already assumes the stability. Dividend investors are effectively choosing between dependable income and long-term capital efficiency.

2. Earnings Momentum & Profitability Trends: Margin Expansion Compensating for Slow Revenue Growth

Altria’s operating model relies less on expansion and more on optimization. That becomes evident in its margin structure. Gross margin recently reached 72.2%, the highest level in a decade and meaningfully above both five-year and ten-year medians. The improvement demonstrates that declining unit volumes have been offset through price increases and operating efficiency rather than market share gains.

This margin strength is central to understanding earnings stability. Revenue growth remains subdued, but earnings continue to advance gradually because the business extracts greater profit from each unit sold. The company’s return on invested capital — nearly 26% — confirms the economic effectiveness of this approach. It also explains why earnings grow faster than revenue over long periods.

Capital allocation reinforces the earnings trajectory. Over the past year, share count declined by roughly 1.0% and by about 2.2% annually over five years. These buybacks quietly amplify per-share growth even when operating income expands slowly. Analysts currently expect earnings around $5.57 next year and approximately $5.82 the following year, implying continued mid-single-digit progression rather than acceleration.

In practical terms, Altria’s earnings model is best described as engineered stability. Revenue barely grows, margins gradually expand, and share count slowly contracts. The combination produces predictable per-share earnings gains, but it also caps upside potential. The company is not transitioning into a faster-growing business; it is refining an already mature one.

The takeaway for dividend investors is subtle but important. Earnings visibility is high, yet growth elasticity is low. The business supports dependable income growth, but rarely surprises positively over extended cycles.

3. Dividend Profile & Sustainability: High Yield Supported by Earnings, Not Expansion

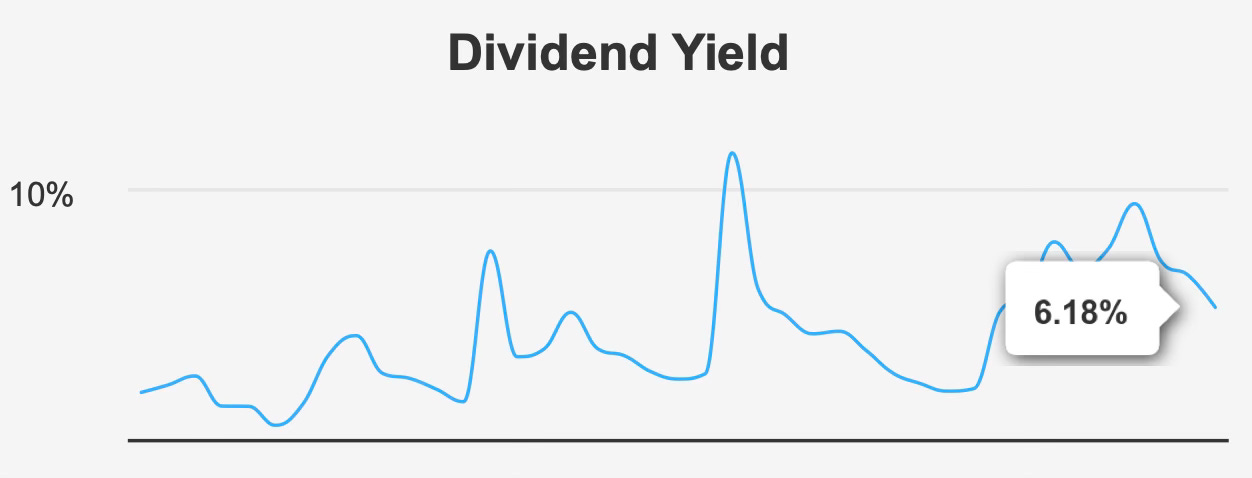

The dividend remains the primary reason investors own Altria. The forward yield stands near 6.2%, positioned slightly below its historical median yet still elevated relative to most equity income alternatives. The company recently raised its quarterly payout to $1.06 from $1.02, continuing a long pattern of incremental annual increases.

Dividend growth has closely mirrored earnings growth. Both three-year and five-year dividend growth rates are roughly 4.2%, with forward expectations near 4.35%. This alignment is intentional. Management distributes most earnings rather than reinvesting for expansion, effectively turning operating profit into shareholder income.

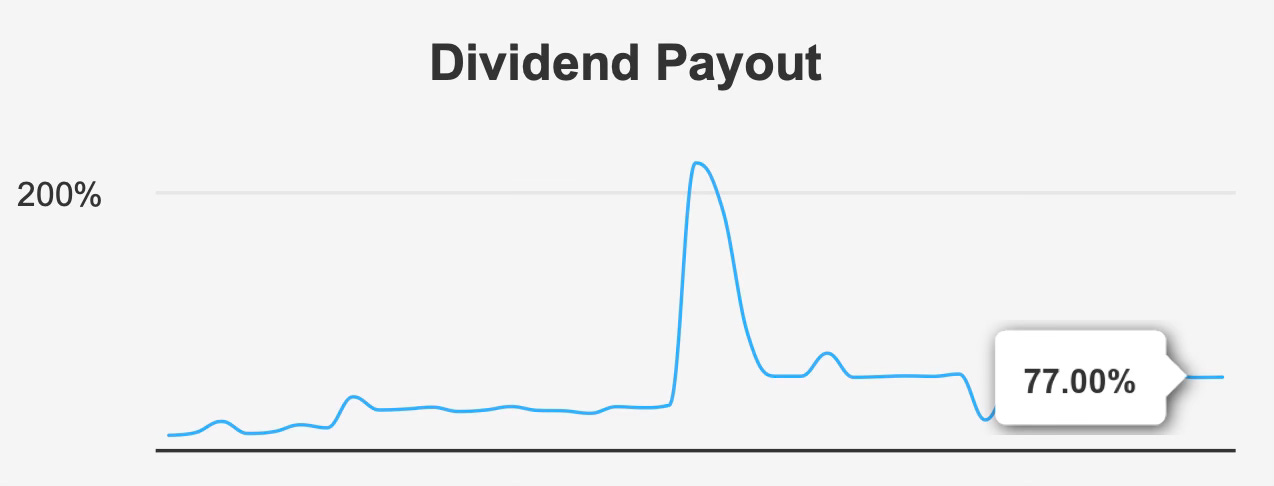

Coverage appears acceptable but not conservative. The payout ratio stands near 77%. This level is typical for tobacco firms but leaves limited buffer against earnings declines. In stable environments the dividend remains secure; under structural pressure it would rely on pricing power rather than retained earnings.

Debt also plays a role in sustainability. Net leverage around 2.4x EBITDA is manageable and consistent with a mature cash-flow business. The company does not require aggressive borrowing to fund distributions, which strengthens the reliability of payments.

The dividend’s durability ultimately depends on economic profit rather than balance sheet flexibility. Because return on capital materially exceeds cost of capital, the firm consistently produces excess cash. As long as that relationship persists, the dividend should remain intact.

However, investors should distinguish sustainability from growth. The payout is dependable, but growth will likely remain tied to mid-single-digit earnings expansion. This is a yield-anchored investment, not a compounding one.

4. Valuation: Paying a Premium Price for a Predictable Stream of Income

The valuation question is straightforward: investors are paying for certainty.

Shares trade around $67 while estimated intrinsic value is roughly $51, implying a negative margin of safety near 31%. The market effectively assigns a stability premium to the company’s earnings stream.

Multiples reinforce the conclusion. The trailing P/E sits near 16.3x versus a ten-year median around 13.3x. Free-cash-flow valuation also appears elevated, with price-to-FCF around 12.5x compared with historical levels near 11.6x. Even sales-based valuation is stretched, with price-to-sales exceeding its long-term norm.

The forward P/E near 12.0x suggests earnings growth will partially normalize valuation over time, but only if growth materializes. With expected growth in the mid-single digits, multiple compression could offset dividend returns for new buyers.

Importantly, analyst price targets average roughly $63, below the current trading price. The market has already priced in anticipated stability and income appeal. Upside therefore depends on either faster growth or higher multiples — neither strongly supported by current fundamentals.

For long-term investors, valuation determines outcome more than business quality. A stable company purchased above intrinsic value often produces satisfactory income but mediocre total returns. Altria fits that description precisely.

5. Risk Assessment & Capital Structure Considerations: Stable Financials, Structural Industry Constraints

Financial risk is relatively low. An Altman Z-score around 4.6 indicates minimal bankruptcy probability, while a Piotroski score of 7 reflects solid operating condition. Earnings manipulation risk also appears low based on accounting metrics. These measures confirm that the balance sheet supports the dividend rather than threatens it.

Operational risks stem from industry structure rather than financial fragility. Revenue growth has slowed and long-term expansion prospects remain limited. The company depends on pricing power to offset declining consumption. That strategy has worked historically, but it inherently caps growth potential.

The payout ratio also limits flexibility. At roughly 77%, most earnings are distributed rather than reinvested. This enhances income predictability but reduces adaptability if industry conditions shift.

Institutional ownership above 62% indicates confidence from large investors, yet also means the shareholder base is income-oriented. Such ownership structures tend to stabilize price volatility but rarely support sustained multiple expansion.

Overall risk therefore divides into two categories: low financial risk and moderate long-term return risk. The business is unlikely to collapse, but the investment may underperform if purchased at an excessive valuation.

Final Assessment

Altria represents one of the clearest examples of a high-quality income company whose stock price reflects that quality. The business produces exceptional returns on capital, stable earnings growth, and dependable dividends supported by strong margins and manageable leverage.

However, long-term investment success depends not only on business strength but also on entry price. With shares trading materially above intrinsic value and above historical valuation norms, investors are effectively prepaying for reliability.

The dividend remains attractive and likely secure, growing roughly in line with earnings at around 4–5% annually. Yet total return expectations appear limited. The yield provides income, but valuation compression could offset much of it over time.

For existing shareholders, the stock functions well as a hold-for-income asset. For new investors, the absence of a margin of safety reduces prospective long-term returns.

In short, Altria remains a strong company but currently a weak purchase. The investment case favors patience — waiting for valuation, not fundamentals, to improve.