PPG Industries: Durable Dividend Growth Backed by Economic Value Creation

A global coatings leader trading near fair value with disciplined capital allocation and low financial risk

Investment Thesis: Economic Value Creation, Global Scale, and Disciplined Capital Allocation Support Long-Term Dividend Growth

PPG Industries PPG 0.00%↑ operates as a global coatings leader serving automotive, aerospace, construction, and industrial markets. Following the acquisition of selected Akzo Nobel assets, the company strengthened its position as the world’s largest coatings producer, reinforcing scale advantages across a diversified global footprint. Less than half of revenue now originates from North America, underscoring a broad geographic mix and meaningful exposure to international end markets.

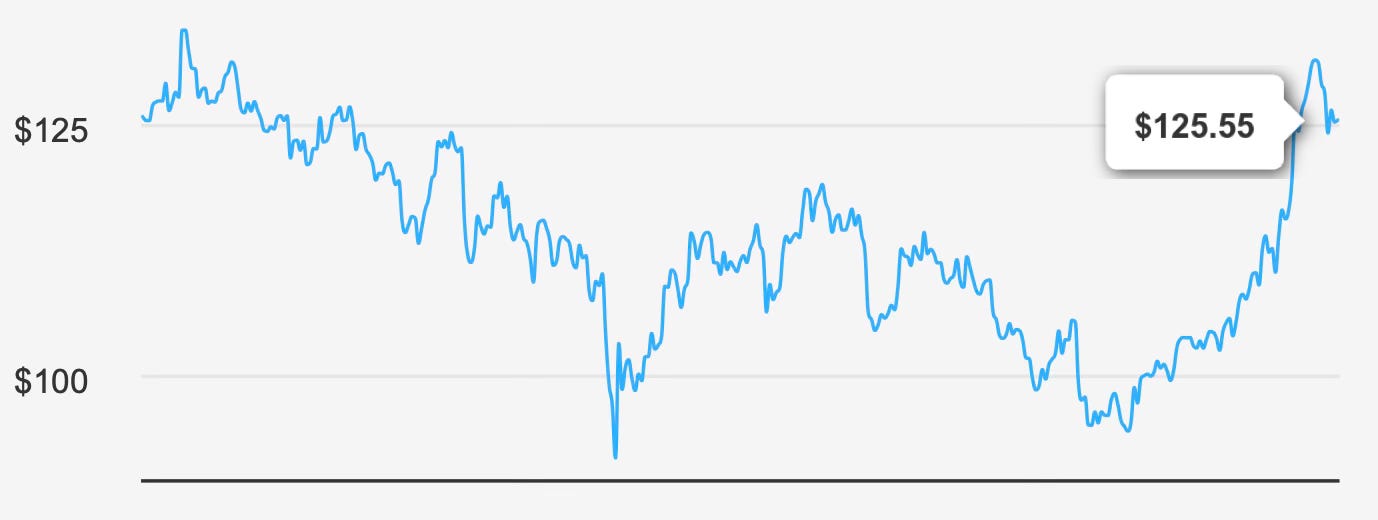

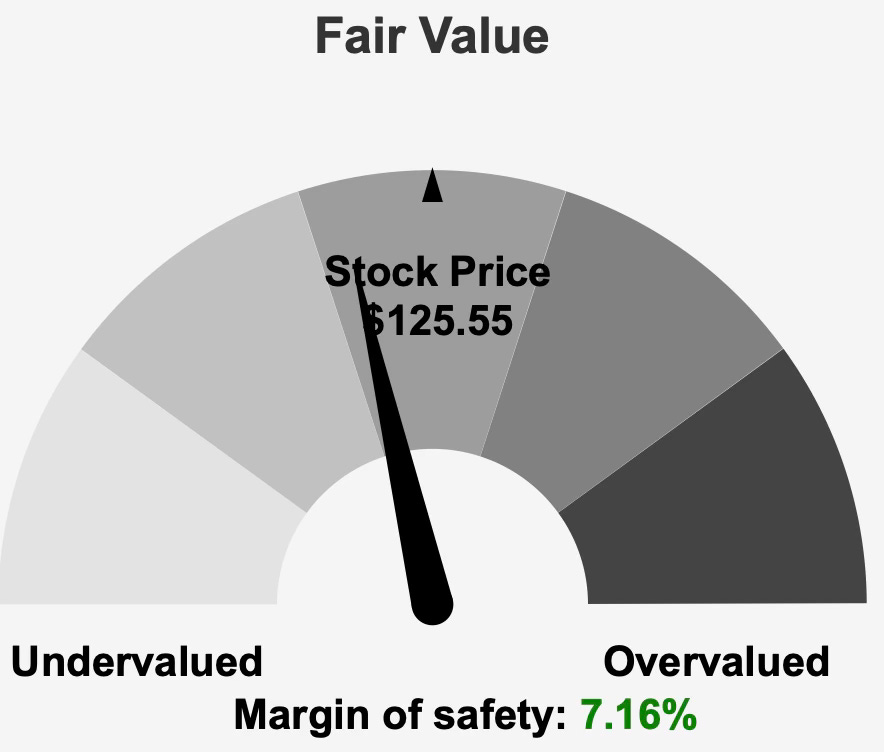

At a current share price of $125 and a market capitalization of $28.17 billion, the stock trades modestly below its intrinsic value estimate of $135.23, implying a 7.2% margin of safety. While not deeply discounted, the valuation suggests reasonable entry conditions for long-term investors seeking stable dividend growth anchored by durable competitive positioning.

The company’s long-term growth profile has been steady rather than aggressive. Revenue has expanded at a 2.4% compound rate over five years and 2.9% over ten years, reflecting the cyclical but resilient nature of coatings demand. Earnings growth has modestly outpaced top-line expansion, with EPS excluding non-recurring items advancing at a 5.2% CAGR over five years and 3.6% over ten years. Industry forecasts call for approximately 4.5% annual growth over the coming decade, broadly consistent with the company’s historical trajectory.

What distinguishes PPG 0.00%↑ is not rapid growth, but disciplined capital allocation and sustained value creation. The firm has consistently generated returns on invested capital above its cost of capital, reinforcing its ability to compound shareholder value through cycles. That combination — moderate growth, operational discipline, and capital return — forms the core of the long-term dividend thesis.

Earnings Momentum & Profitability Trends

Recent quarterly results reflect near-term earnings variability against a steady longer-term backdrop. EPS excluding non-recurring items came in at $1.51, down from $2.13 in the prior quarter and $1.62 in the comparable year-ago period. Reported diluted EPS was $1.33, compared with $2.00 in the previous quarter. Revenue per share of $17.38 declined from $18.02 sequentially but improved relative to $16.02 a year earlier.

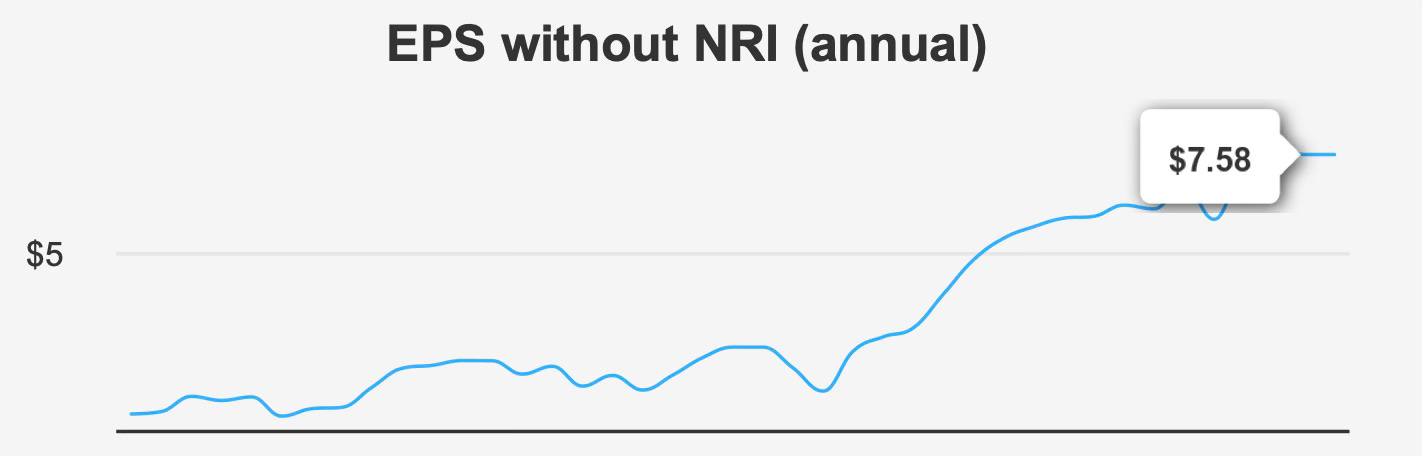

These short-term fluctuations do not materially alter the broader earnings profile. Analysts project next fiscal year EPS of $7.62, rising to $8.27 the following year. Revenue is expected to reach $16,405.73 million in 2026 and expand toward $17,453.19 million by 2028, reflecting steady mid-single-digit earnings progression supported by operational efficiencies and ongoing geographic expansion.

Profitability metrics reinforce the company’s resilience. Gross margin for the latest quarter stood at 41.3%, modestly above the five-year median of 40.4%, though below the 10-year peak of 46.3%. While margins have compressed from historical highs, they remain structurally healthy, suggesting pricing power and cost discipline remain intact.

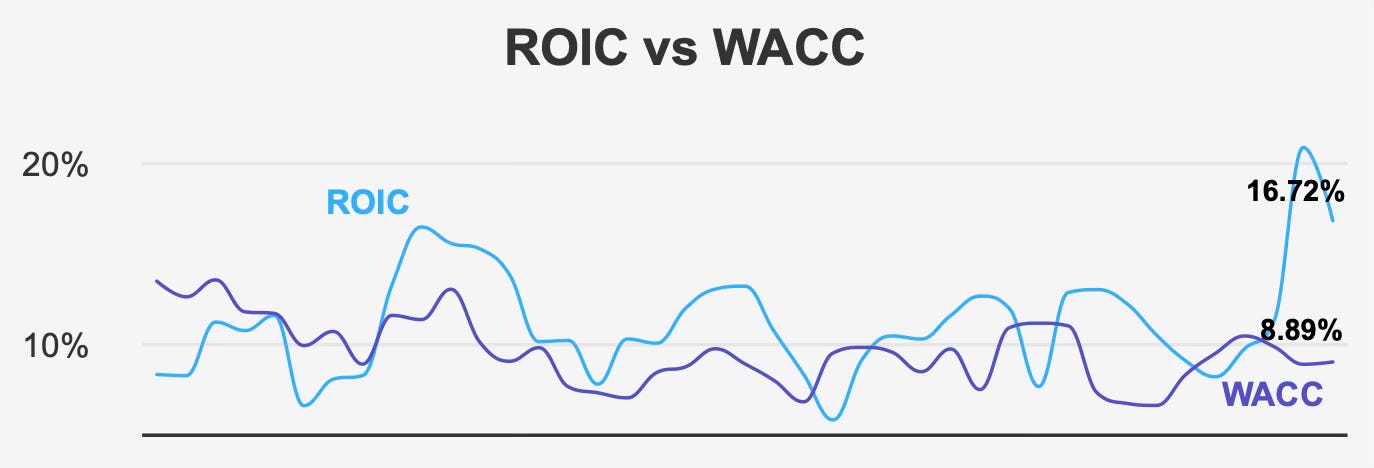

The most compelling evidence of value creation lies in capital efficiency. The current ROIC of 16.7% meaningfully exceeds the 8.9% weighted average cost of capital. Even on a median basis, five-year ROIC of 9.6% surpasses the five-year median WACC of 9.4%, indicating consistent economic profit generation. Over the past decade, ROIC reached a high of 20.8%, compared with a 10-year median WACC of 9.1%, underscoring sustained spread generation across cycles.

Return on equity further supports the profitability narrative. ROE stands at 21.4%, above its five-year median of 17.6%, reflecting effective use of shareholder capital without excessive leverage.

Share repurchases have also contributed to per-share growth. The one-year buyback ratio of 2.4% compares favorably to the five-year average of 1.0%, indicating an acceleration in capital return during periods of earnings fluctuation. By reducing share count, management has supported EPS growth even amid uneven operating momentum.

Collectively, while quarterly volatility persists, long-term earnings durability and disciplined capital deployment remain intact.

Dividend Profile & Sustainability

PPG’s dividend profile reflects steady growth supported by prudent payout management and an exceptionally strong balance sheet.

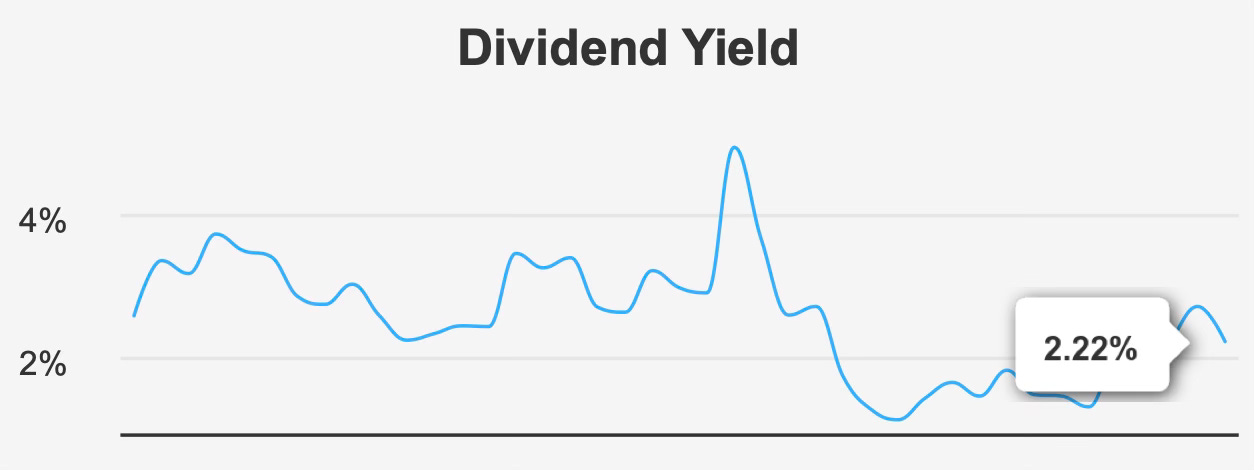

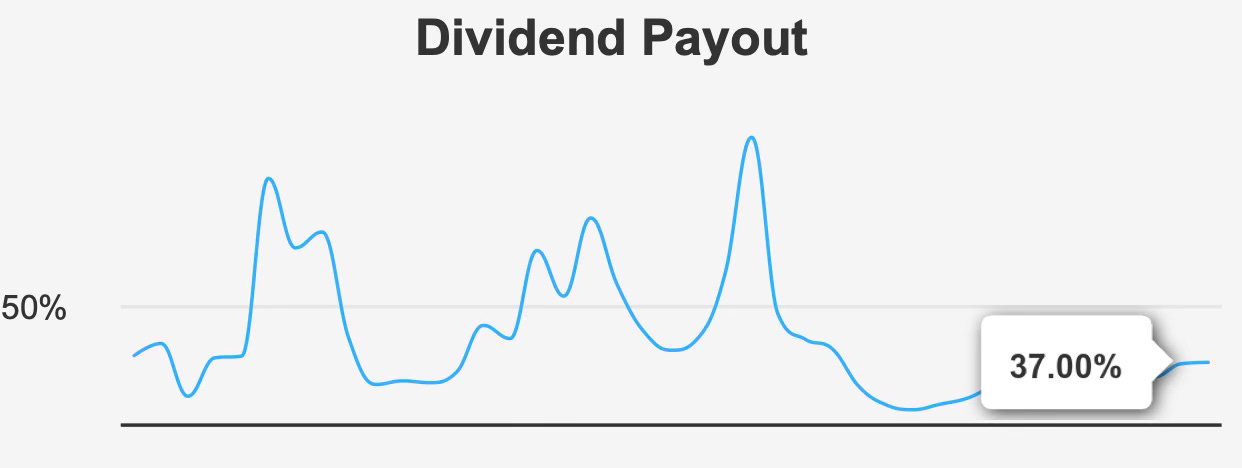

The forward dividend yield stands at 2.22%, competitive within the chemicals sector, though below the 10-year high of 2.86%. The payout ratio of 37.0% remains conservative, providing flexibility for continued increases even in periods of moderate earnings pressure. Dividend coverage stands at 2.5x, reinforcing the margin of safety embedded in the distribution.

Dividend growth has been consistent rather than aggressive. Over the past five years, the dividend has grown at a 5.7% annual rate, with a 4.7% rate over three years. The most recent quarterly increase from $0.68 to $0.71 per share signals ongoing commitment to shareholder returns. Forward projections call for approximately 5.2% dividend growth over the next three to five years, closely aligned with historical trends and earnings expectations.

Balance sheet strength materially enhances dividend sustainability. Debt-to-EBITDA is reported at just 0.05, an exceptionally low level of leverage that provides significant financial flexibility. The Altman Z-score of 5.52 signals strong financial stability, while a Piotroski F-Score of 8 reflects solid profitability, liquidity, and operating quality. The Beneish M-Score of -3.12 indicates low probability of earnings manipulation, further reinforcing financial transparency.

With such modest leverage and ample coverage, the dividend appears well protected. Even in a slower-growth environment, the conservative payout ratio and strong cash generation capacity should support continued annual increases.

The next ex-dividend date is May 11, 2026, with a prior ex-dividend date recorded on February 20, 2026, and payment scheduled for March 12, 2026, reflecting a consistent quarterly distribution cadence.

For income-focused investors, the appeal lies less in yield magnitude and more in durability, discipline, and steady compounding.

Valuation: Discounted Relative to Historical Multiples with a Modest Margin of Safety to Intrinsic Value

At $125.55 per share, PPG trades modestly below its intrinsic value estimate of $135.23, implying a 7.2% margin of safety. The valuation profile suggests fair value with slight upside potential rather than a deep value opportunity.

On earnings, the trailing P/E stands at 18.1x, below the 10-year median of 24.2x. The forward P/E of 15.7x aligns closely with the 10-year low of 15.0x, indicating a compression in valuation relative to historical norms. This lower forward multiple suggests the market is pricing in moderate growth expectations rather than expansionary assumptions.

Enterprise value to EBITDA of 12.1x sits below the 10-year median of 15.0x, reinforcing the notion that shares are trading at a reasonable operating multiple. Price-to-free-cash-flow of 24.4x is slightly above the 10-year median of 22.7x but remains dramatically below the 10-year high of 103.9x, suggesting valuation from a cash flow perspective is neither stretched nor distressed.

The price-to-sales ratio is 1.79 and near its one-year high, which may indicate limited near-term multiple expansion potential. Additionally, the dividend yield sits at a one-year low, reflecting recent price strength.

Analyst sentiment appears stable, with 27 ratings and price targets clustering near the current trading range. Targets have edged higher over the past three months, signaling modestly constructive outlooks rather than aggressive re-rating expectations.

Overall, valuation appears balanced. Multiples have compressed relative to long-term averages, yet the margin of safety remains modest. Investors are paying a reasonable price for steady mid-single-digit growth and durable value creation.

Risk Assessment & Capital Structure Considerations

The risk profile presents a mix of constructive fundamentals and selective cautionary signals.

Insider activity shows four selling transactions totaling 115,217 shares over the past three months, with no insider purchases during that period. Insider ownership stands at 0.78%, relatively low by historical corporate standards. While insider selling can reflect diversification rather than deteriorating fundamentals, the absence of buying may temper short-term sentiment.

Institutional ownership, by contrast, is substantial at 86.15%, suggesting strong participation from long-term capital allocators. Trading liquidity remains robust, with average daily volume over the past two months of 2,155,045 shares compared to current daily volume of 1,535,150 shares. A Dark Pool Index of 57.0% indicates significant institutional trading activity, often associated with strategic positioning rather than speculative flows.

From a financial stability perspective, risk appears limited. The Altman Z-score of 5.52, low leverage, and strong coverage ratios collectively indicate a resilient capital structure. The company’s ability to sustain ROIC above WACC further supports long-term stability.

Government contract revenue has shown variability, rising from $44.3 million in 2021 to $56.8 million in 2022 before declining to $37.5 million in 2023. Projections of $50.7 million in 2024 and $51.1 million in 2025 suggest recovery, though a sharp drop to $6.6 million in 2026 highlights potential revenue lumpiness in that segment. Given the company’s global scale, these fluctuations are unlikely to materially impair overall results but may introduce short-term variability.

The stock’s proximity to its one-year high and a dividend yield at a one-year low suggest limited immediate valuation cushion. However, balance sheet strength and disciplined capital allocation significantly mitigate structural risk.

Final Assessment

PPG Industries represents a steady, value-creating industrial compounder rather than a high-growth story. Revenue growth has historically tracked in the low-single-digit range, while disciplined cost management, share repurchases, and capital efficiency have supported mid-single-digit earnings expansion.

The company consistently earns returns on invested capital above its cost of capital, reinforcing long-term economic value creation. A conservative 37.0% payout ratio, 2.5x dividend coverage, and negligible leverage underpin dividend sustainability and support projected growth near 5% annually.

Valuation appears reasonable at 18.1x trailing earnings and 15.7x forward earnings, both below long-term medians. The 7.2% margin of safety relative to intrinsic value suggests fair value with modest upside potential rather than deep undervaluation.

Risks include insider selling, near-term earnings variability, and limited multiple expansion potential at current price levels. However, financial strength, institutional ownership, and durable competitive positioning offset these concerns.

For long-term dividend investors seeking stability, moderate growth, and disciplined capital allocation, PPG offers an attractive, low-risk holding. While the stock does not present a compelling deep-value opportunity, it remains well suited for portfolios prioritizing consistent income growth and economic value creation over cyclical upside.