Pfizer Inc: High Yield, Low Expectations

A dividend-rich pharma giant offering income stability, with limited upside at current valuations.

Investment Thesis: Income Stability Backed by Scale and Discipline

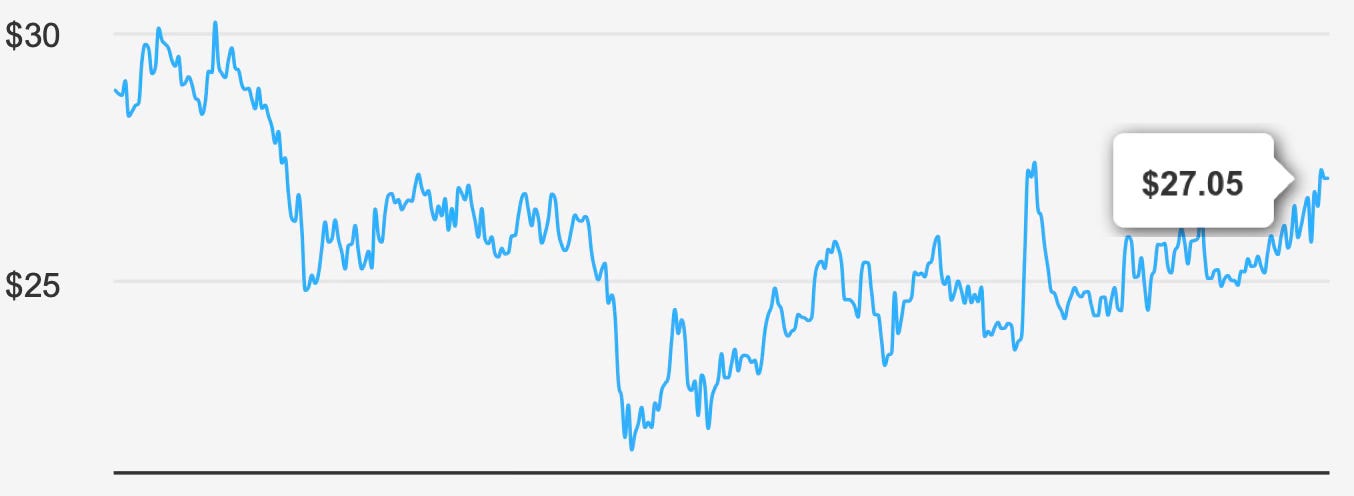

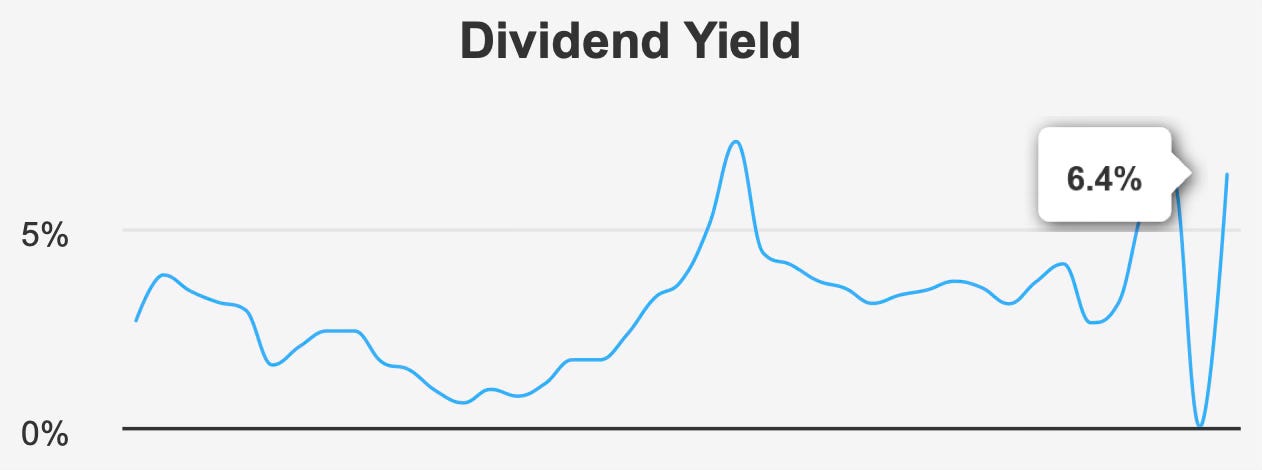

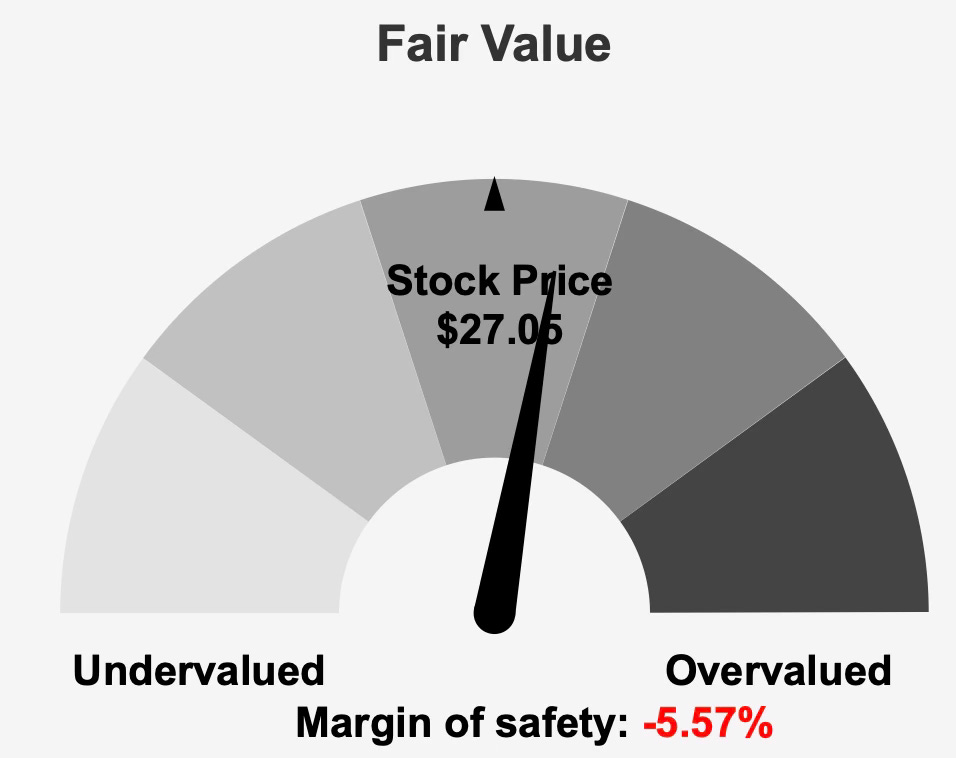

Pfizer Inc. PFE 0.00%↑ enters 2026 as a mature, income-oriented holding whose appeal rests on the durability of its global portfolio rather than near-term growth acceleration. At roughly $27 per share and a market capitalization of $153.8 billion, the stock trades modestly above its assessed intrinsic value of $25.62, implying a negative margin of safety of about 5.6%. This positioning frames the investment case clearly. Investors are accepting limited valuation support in exchange for an elevated forward dividend yield of 6.4%, materially above the company’s 10-year median yield of 3.9%. The return profile is therefore anchored in income generation rather than valuation upside.

The operating base remains broad and resilient. Annual sales of roughly $60 billion are supported by a diversified mix of prescription medicines and vaccines, with international markets contributing around 40% of total revenue and emerging markets representing a meaningful growth component within that mix. Established products such as Prevnar 13, Vyndaqel, and Eliquis continue to underpin cash flow, providing stability as pandemic-related revenues unwind. This portfolio breadth reduces dependence on any single therapy area and supports predictable operating cash generation.

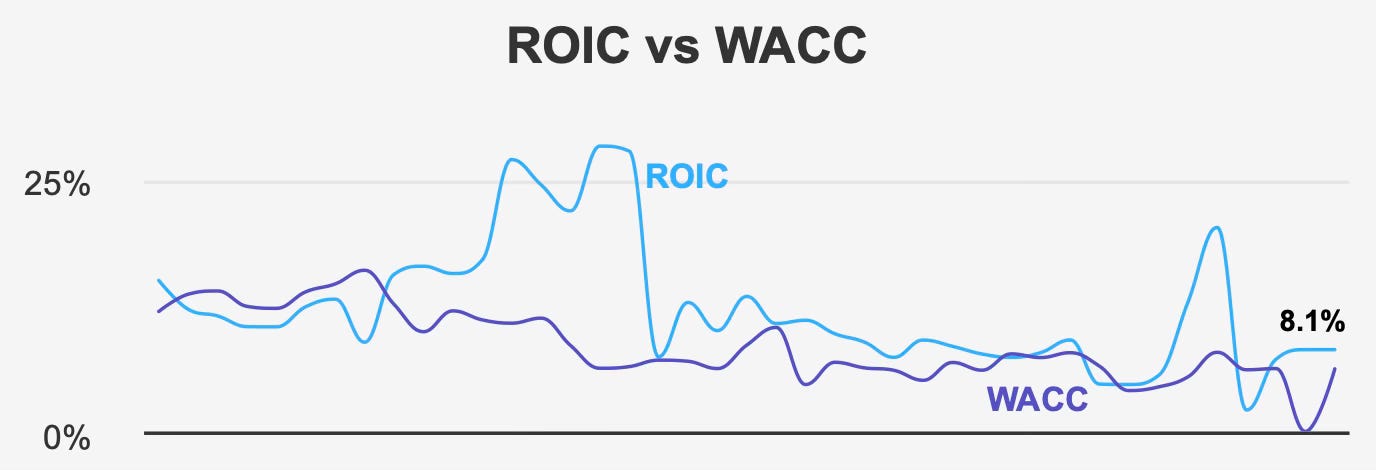

Capital efficiency remains a central pillar of the thesis. Current return on invested capital of 8.1% exceeds the cost of capital of roughly 6.2%, and the five-year median spread between the two measures has been consistently positive. This confirms that core operations continue to create economic value even as growth moderates. The implication for investors is that the dividend is funded by operating performance rather than balance sheet strain. With a payout ratio of 56.0% and manageable leverage, the income stream appears sustainable under current conditions.

The principal trade-off lies in valuation. With intrinsic value below the market price and valuation multiples near long-term norms, upside from re-rating appears limited. Total returns are therefore likely to be driven primarily by dividends and modest earnings normalization rather than by multiple expansion. For long-term income investors, that trade-off can be acceptable, but it sets expectations for restrained capital appreciation.

Earnings & Profitability: Normalization with Margin Pressure

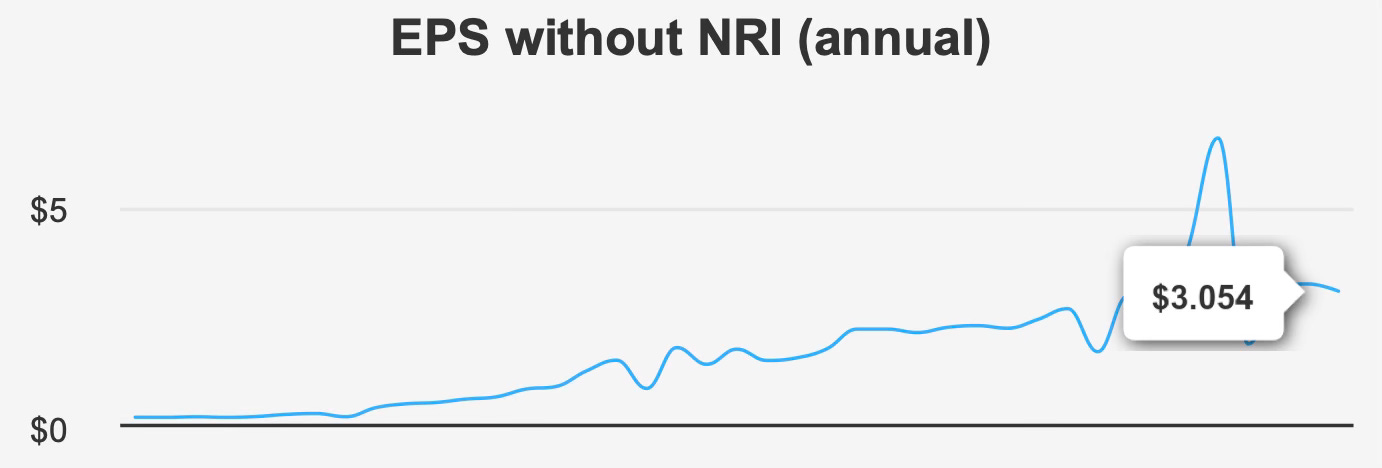

Recent earnings reflect a transition from pandemic-era distortions toward a more normalized operating profile. Fourth-quarter 2025 EPS excluding non-recurring items was $0.66, slightly below the prior quarter’s $0.69 but above $0.63 in the comparable quarter of 2024. On a diluted basis, earnings were –$0.29, highlighting volatility tied to one-off items and portfolio adjustments. Revenue per share of $3.09 edged down from $3.12 a year earlier, reinforcing the theme of stabilization rather than renewed top-line momentum.

Longer-term growth has been modest. Over five years, EPS excluding non-recurring items compounded at roughly 0.5% annually, while the ten-year rate of about 4.7% reflects the tailwind from earlier product cycles. Forward estimates point to EPS of around $2.05 in fiscal 2026, followed by $2.04 the year after, suggesting near-term earnings stability rather than acceleration. Revenue projections imply a gradual decline from about $61.0 billion in 2026 to roughly $55.0 billion by 2028, as pandemic-related demand fades and competitive pressures persist.

Profitability remains strong in absolute terms, though margins have normalized. Gross margin of 74.3% in the latest quarter sits below the decade peak of 80.3% but remains well above the five-year median of 66.1%. This level of margin underscores the inherent pricing power of branded pharmaceuticals. However, the multi-year trend of margin compression, with average annual declines of about 4.0% in gross margin and 4.4% in operating margin over five years, points to structural headwinds from mix shifts and competitive intensity. These pressures cap organic earnings growth unless offset by successful pipeline execution.

Capital allocation has been conservative. Share buybacks have been minimal in recent years, with one-year and three-year buyback ratios of –0.3%, indicating slight net dilution. The ten-year buyback ratio of 1.1% reflects more active repurchases in earlier periods, but current priorities favor balance sheet management and dividend stability. This approach aligns with the company’s income-oriented shareholder base but limits per-share earnings growth from financial engineering.

Relative to industry expectations of roughly 5.8% annual growth over the next decade, the company’s near-term revenue outlook appears cautious. The earnings profile is best characterized as stable but subdued, reinforcing the role of the stock as an income anchor rather than a growth vehicle.

Dividend Profile & Sustainability: High Yield, Modest Growth

The dividend remains the core of the investment case. The quarterly payout of $0.43 per share has been maintained consistently, supporting a forward yield of 6.4%. This yield reflects both disciplined capital returns and a share price that embeds tempered growth expectations. Over the past five years, dividend growth averaged 3.0%, with a three-year rate of 2.5%. Forward growth expectations of around 2.0% over the next several years signal a conservative posture designed to preserve balance sheet flexibility.

Coverage remains adequate. The payout ratio of 56.0% provides room to absorb moderate earnings volatility, while dividend coverage of 0.79 suggests free cash flow is sufficient but not abundant relative to distributions. The predictability of the quarterly schedule, with the next ex-dividend date in late January 2026 and payment in early March, reinforces the stock’s appeal to income-focused investors seeking reliability over aggressive growth.

Leverage warrants monitoring but does not threaten dividend sustainability under current conditions. Debt to EBITDA of 3.9 places leverage toward the upper end of a moderate range for a mature pharmaceutical company. Importantly, returns on invested capital continue to exceed the cost of capital, indicating that debt is employed within a value-creating framework rather than eroding shareholder returns. The dividend’s sustainability is therefore more dependent on operational resilience than on incremental balance sheet expansion.

For portfolio construction, the dividend profile offers a stabilizing income stream with limited growth but high starting yield. While dividend growth is unlikely to outpace inflation materially, the current yield compensates by delivering immediate income, making the stock suitable for investors prioritizing cash flow stability.

Valuation: Fair Pricing Limits Upside

Valuation metrics position the stock as fairly valued to modestly overvalued on an intrinsic basis. At around $27 per share versus intrinsic value of $25.62, the negative margin of safety of roughly 5.6% suggests limited downside protection. The trailing P/E of 19.9x sits modestly above the long-term median of 15.9x, indicating that the stock is not trading at a deep discount to historical norms. The forward P/E of 9.1x reflects expectations for earnings normalization, but this compression is driven more by forward earnings recovery than by market re-rating.

Enterprise and cash flow multiples reinforce the fair value assessment. EV/EBITDA of 12.9x aligns closely with the long-term median of 12.9x, while price to free cash flow of 14.9x sits essentially at its historical midpoint. The price-to-book ratio of 1.7x, closer to the lower end of the historical range, offers some valuation support, though book value is less central to assessing pharmaceutical economics than cash generation.

Analyst price targets cluster near current levels and have drifted modestly lower in recent months, reinforcing the view that upside is constrained absent a material improvement in growth prospects. Valuation therefore supports the stock as an income holding but offers limited scope for multiple-driven appreciation.

Risk & Capital Structure: Margins, Leverage, Execution

Operational risks center on margin compression and revenue normalization. Multi-year declines in gross and operating margins highlight the challenge of replacing high-margin pandemic revenues with equally profitable products. Revenue per share has trended lower over the past three years, and forward projections point to a gradual top-line contraction through 2028. These dynamics heighten reliance on pipeline execution to stabilize growth.

Financial risk remains moderate. An Altman Z-score of 2.16 places the company in the grey zone, warranting monitoring but not signaling acute distress. This is balanced by a Piotroski F-score of 7, indicating solid financial health, and a Beneish M-score of –2.47, suggesting a low likelihood of earnings manipulation. Together, these indicators support confidence in reported financials even as operational headwinds persist.

Ownership and trading dynamics add context. Insider ownership of 0.28% and limited recent insider activity point to neutral internal sentiment, while institutional ownership of 64.1% reflects strong participation by large investors. Trading liquidity is robust, with recent volumes above 46 million shares and a two-month average exceeding 51 million. Dark pool activity of 31.8% underscores significant institutional involvement, which can influence short-term price movements without altering fundamentals.

External revenue sources have normalized sharply. Government contract revenue, which exceeded $14 billion in 2021 and $18 billion in 2022, has fallen markedly, with projections near $352 million by 2026. This reversion underscores the fading of extraordinary pandemic demand and increases the importance of core commercial performance. Recent congressional trading activity, which saw sales that outperformed the S&P 500 over short windows, offers anecdotal insight into timing rather than a fundamental signal.

Final Assessment

The stock offers a clear value proposition as a high-yield, low-volatility income holding. The dividend is well supported by operating cash flow, a manageable payout ratio, and a business model that continues to generate returns above the cost of capital. Management’s conservative approach to dividend growth and capital allocation favors sustainability over aggressive expansion, aligning with the expectations of long-term income investors.

Valuation, however, limits upside. With the stock trading modestly above intrinsic value and multiples near historical norms, capital appreciation potential appears constrained. Earnings momentum is stabilizing but subdued, and margin pressures alongside revenue normalization place a premium on successful pipeline execution. In this setting, total returns are likely to be driven primarily by dividends rather than by re-rating.

For income-focused investors, the stock functions well as a portfolio anchor, providing dependable cash flow and defensive characteristics. For those seeking growth or valuation-driven upside, the current pricing offers little margin of safety.