PepsiCo Dividend Review: Quality Compounding Priced for Stability

Solid Earnings Momentum and Capital Efficiency Offset by Fair Valuation

Investment Thesis: A High-Quality Consumer Franchise Trading Near Assessed Fair Value

PepsiCo, Inc. PEP 0.00%↑ operates from a position of global scale and brand strength, combining category leadership in savory snacks with a top-tier global beverage franchise. Convenience foods contribute approximately 58% of total revenue, while beverages account for the remaining 42%, creating a balanced revenue mix that reduces dependence on any single product line. International markets represented 40% of both total sales and operating profits in 2024, reinforcing the company’s diversified earnings base.

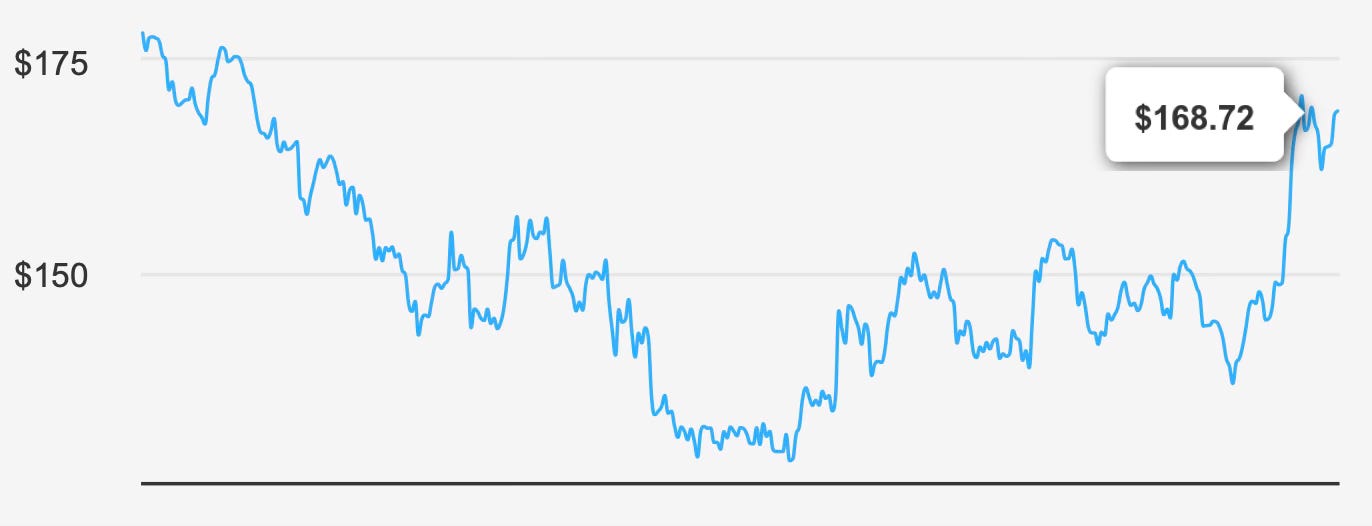

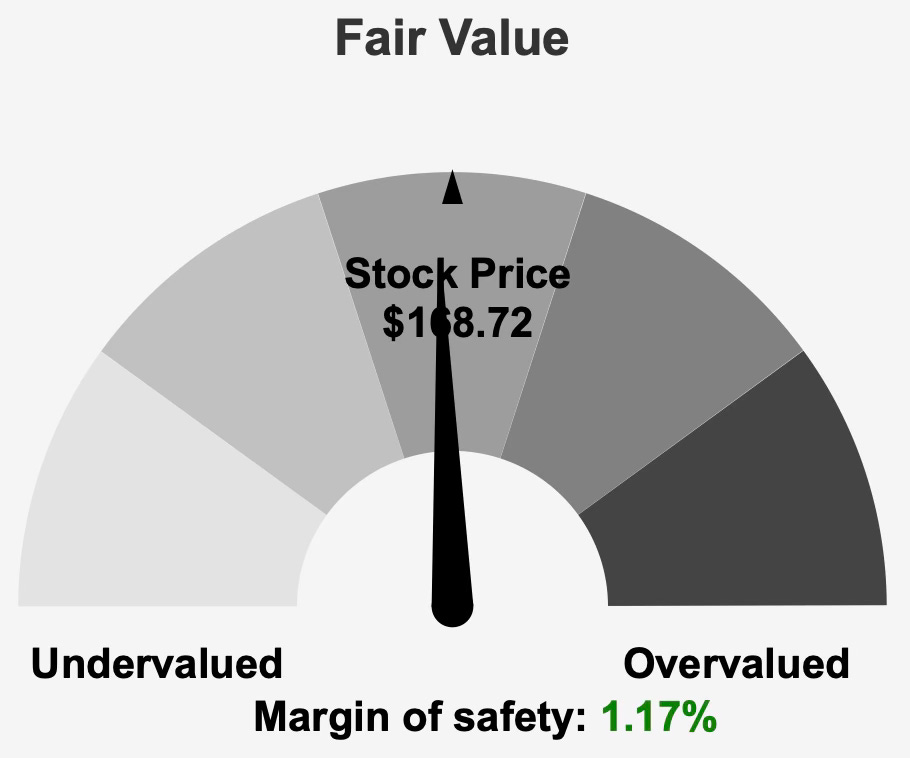

At a current price of $168, the stock trades just below its intrinsic value estimate of $170.71, implying a narrow margin of safety of 1.2%. The valuation assessment categorizes the shares as fairly valued with a Hold rating and Low Risk profile. With a market capitalization of $230.58 billion and a forward dividend yield of 3.4%, PepsiCo occupies a familiar role for long-term dividend investors: stable, predictable, and unlikely to deliver outsized short-term upside.

Longer-term growth trends support that stability. Revenue has compounded at 6.0% over the past five years and 5.7% over the past decade, while earnings per share expanded at an annualized 8.5% over five years and 6.2% over ten years. This differential between earnings and revenue growth reflects margin discipline, capital allocation efficiency, and modest share repurchases.

The broader beverage industry is projected to grow at roughly 3% annually over the next decade. PepsiCo’s historical revenue growth exceeding that industry baseline suggests continued share resilience and pricing power. The central question for investors is not durability—it is whether today’s price offers enough compensation for the quality embedded in the business.

2. Earnings Momentum & Profitability Trends

PepsiCo’s most recent quarterly results underscore steady earnings progression. For the quarter ending December 31, 2025, EPS excluding non-recurring items reached $2.26, improving from $1.98 in Q3 2025 and $1.96 in Q4 2024. On a diluted basis, EPS was $1.85, modestly below the prior quarter’s $1.90 but well above the $1.11 recorded in the same quarter a year earlier. Revenue per share climbed to $21.371 from $17.447 in the previous quarter, signaling seasonal strength and sustained pricing support.

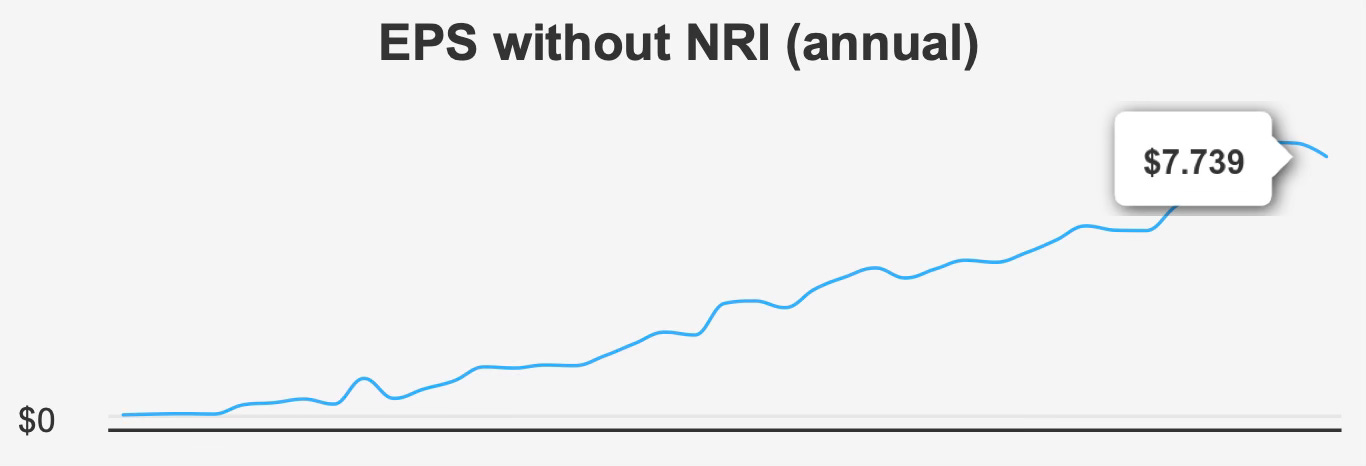

Over a multi-year horizon, earnings expansion has been consistent rather than cyclical. An 8.5% five-year EPS growth rate, compared with 6.0% revenue growth, suggests incremental margin improvement and operational leverage. Gross margin remains steady at 54.2%, aligned with the five-year median, indicating pricing discipline in a cost-sensitive consumer environment.

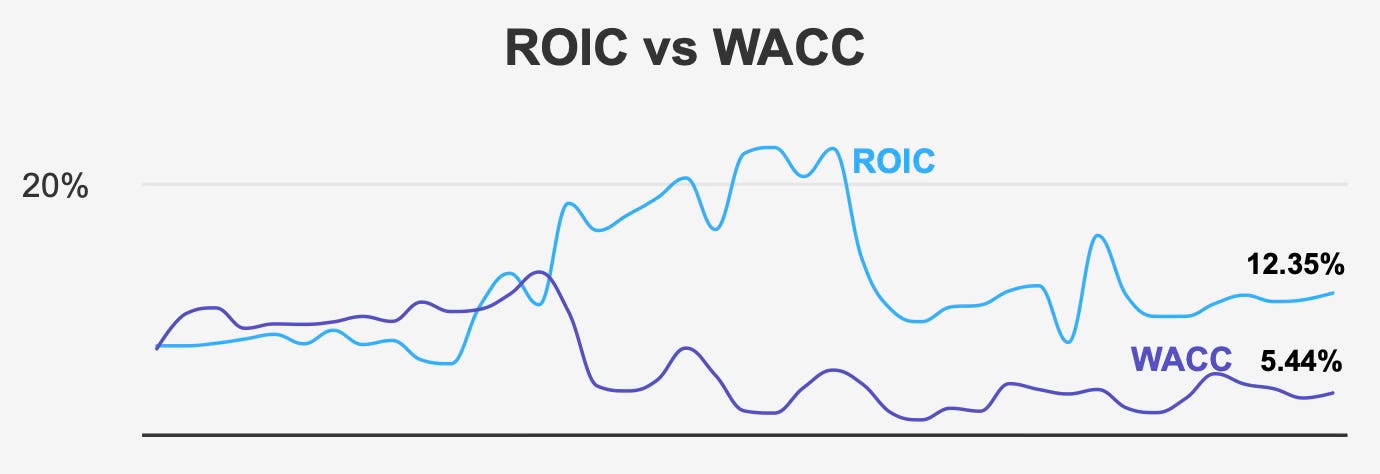

Capital efficiency further distinguishes the business. PepsiCo’s five-year median return on invested capital stands at 11.8%, comfortably above its median weighted average cost of capital of 5.7%. In the most recent measurement, ROIC improved to 12.4% versus a WACC of 5.4%, preserving a wide economic profit spread. This persistent gap between returns and cost of capital supports long-term intrinsic value creation.

Return on equity of 43.5% reinforces the same conclusion. While leverage contributes to this elevated figure, the combination of strong margins, disciplined investment, and scale efficiencies underpins sustained shareholder value creation.

Share repurchases play a supplementary role. Over the past year, the buyback ratio was 0.3%, below the ten-year average of 0.5%. This restrained pace indicates management is prioritizing balance sheet stability and dividend commitments over aggressive capital return acceleration. Repurchases have supported per-share growth at the margin but remain a secondary driver compared with organic expansion.

Looking ahead, analysts project revenue of $98,485.23 million by the end of 2026. EPS is estimated at $8.321 next fiscal year, rising to $8.902 the following year. These projections imply mid-single-digit earnings growth, broadly consistent with historical performance and management’s steady operational execution.

The next earnings announcement is scheduled for April 24, 2026. For long-term investors, the focus will remain on margin resilience and free cash flow generation rather than short-term volume volatility.

3. Dividend Profile & Sustainability

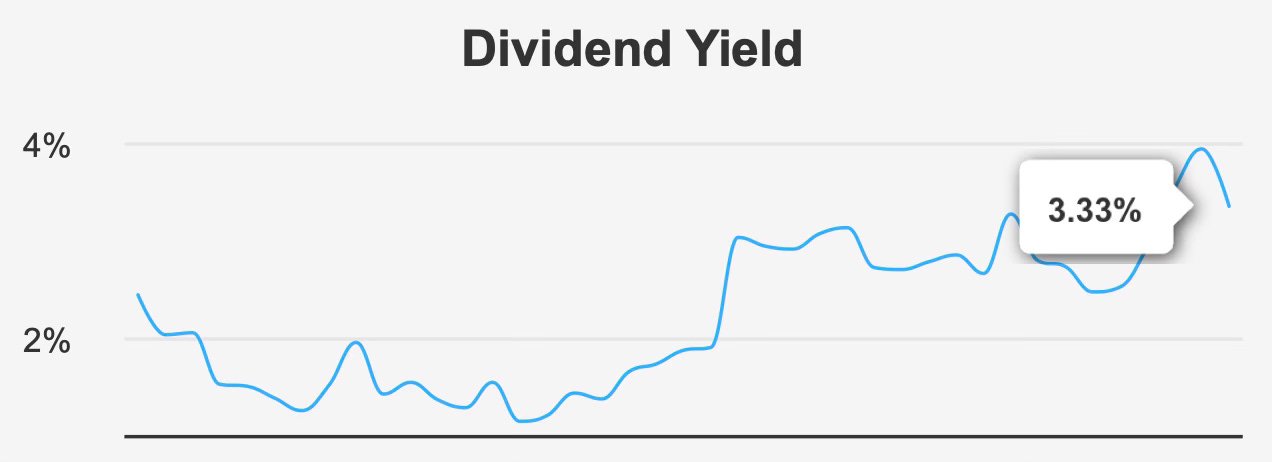

PepsiCo’s dividend remains central to its investment case. The forward yield of 3.3% exceeds the company’s ten-year median yield of 2.8%, reflecting either improved income attractiveness or modest multiple compression. In either case, current yield levels are competitive within the non-alcoholic beverage sector.

Dividend growth has been consistent. Over the past five years, the dividend expanded at a 7.2% annual rate, with the three-year rate slightly higher at 7.5%. Looking forward, growth is expected to moderate to approximately 5.0%, reflecting a more mature earnings base and higher payout ratio.

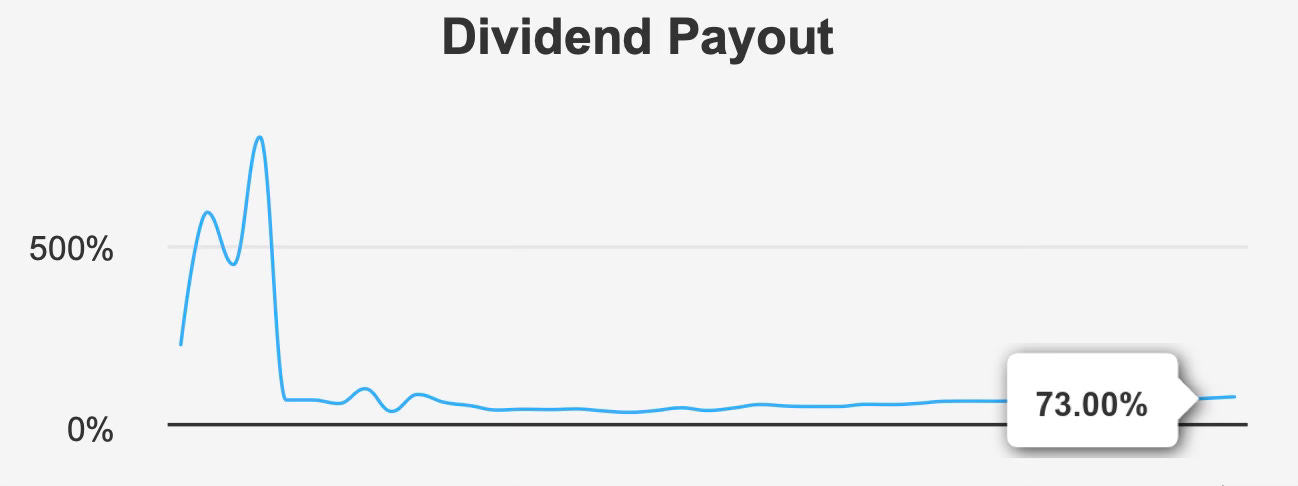

The payout ratio currently stands at 73.0%. While elevated relative to more conservative dividend payers, it remains sustainable given PepsiCo’s recurring cash flows and earnings coverage ratio of 1.07. Importantly, this payout level is below historical periods when the ratio exceeded 100%, suggesting improved earnings alignment with dividend commitments.

Dividend timing remains consistent, with the next ex-dividend date on March 6, 2026, and payment scheduled for March 31, 2026. The regular quarterly cadence reinforces predictability for income-focused investors.

Leverage metrics are manageable. Debt-to-EBITDA stands at 3.21, within a moderate range for a defensive consumer staple. Although debt issuance increased by $9.2 billion over the past three years, overall leverage remains within acceptable bounds. Combined with an Altman Z-score of 3.71, the probability of financial distress appears low.

Operational integrity further supports dividend sustainability. The Beneish M-Score of -2.45 suggests a low likelihood of earnings manipulation, while expanding operating margins point to internal efficiency gains. These factors collectively reinforce the dividend’s durability even if growth moderates toward the projected 5–6% range.

4. Valuation Analysis: Multiples, Intrinsic Value Alignment, and Market Expectations

At $168.72, PepsiCo trades modestly below its assessed intrinsic value of $170.71, yielding a margin of safety of just 1.2%. This narrow discount aligns with the Fairly Valued designation and suggests limited valuation-driven upside.

On earnings metrics, the forward P/E stands at 19.5x, a notable compression from the trailing P/E of 28.1x and below the ten-year median of 26.2x on a trailing basis. The divergence reflects anticipated earnings normalization and growth into the current price.

Enterprise valuation remains stable. The trailing EV/EBITDA multiple of 17.4x sits slightly above the ten-year median of 16.6x but well below the decade high of 25.1x. This positioning suggests the market is pricing PepsiCo at a modest premium to its historical norm, consistent with its defensive characteristics and low-risk profile.

Price-to-book of 11.3x remains elevated relative to asset value, although this metric is less instructive for brand-driven consumer businesses where intangible assets dominate. The price-to-free-cash-flow ratio of 30.1x aligns closely with its ten-year median, reinforcing the conclusion that valuation is balanced rather than stretched.

Analyst price targets average $169.63, indicating expectations clustered near the current trading level. This convergence between intrinsic value, analyst targets, and market price underscores a consensus view: PepsiCo is priced for steady execution, not acceleration.

While valuation is not excessive relative to history, neither does it provide a meaningful buffer against operational disappointment. Investors are effectively paying for predictability.

5. Risk Assessment & Capital Structure Considerations

PepsiCo’s risk profile is defined less by volatility and more by valuation sensitivity and growth moderation. Revenue growth has slowed relative to earlier cycles, and the stock’s trailing P/E near 28.1x approaches a two-year high. With shares trading near peak levels, multiple expansion appears limited.

The dividend payout ratio of 73.0% warrants monitoring, particularly in a slower growth environment. While sustainable today, any material earnings deceleration could constrain dividend growth flexibility.

Liquidity conditions show some softening. Current daily trading volume of 1,834,527 shares represents approximately 21.5% of the two-month average of 8,532,535 shares, indicating a temporary dip in trading activity. The Dark Pool Index of 36.3% suggests over one-third of trading occurs off-exchange, potentially reducing transparency in price discovery.

Insider ownership remains low at 0.49%, with no insider purchases and only two sales over the past year. Institutional ownership stands at 76.31%, reflecting strong professional investor presence. The absence of insider buying may reinforce the perception of fair valuation rather than deep undervaluation.

Government contract revenue has been volatile, peaking at $8,505,360 in 2022 before declining and projected to fall to $754,276 in 2026. While not central to the investment case, this variability highlights non-core revenue instability.

Patent filings increased from 44 in 2021 to 51 in 2023 and are projected at 56 for 2024 and 2025 before a sharp drop to 4 in 2026. This anticipated decline may signal strategic realignment rather than reduced innovation, but it introduces uncertainty around longer-term intellectual property development.

Despite these considerations, the company’s financial resilience remains intact. ROIC materially exceeds WACC, the Altman Z-score is strong, and margins are expanding. Risk appears manageable, though valuation leaves little room for execution missteps.

Final Assessment

PepsiCo represents a textbook example of a high-quality, income-oriented consumer franchise trading at fair value. Revenue growth in the mid-single digits, EPS expansion near 8–9% over five years, and consistent dividend increases around 7% annually underscore operational reliability. Capital efficiency remains strong, with ROIC more than double WACC and ROE exceeding 40%.

The forward dividend yield of 3.4% offers income above the company’s historical median, supported by a sustainable payout ratio and moderate leverage. Dividend growth is likely to moderate toward 5% annually, aligning with projected earnings expansion.

Valuation metrics cluster around historical norms. A forward P/E of 19.5x and EV/EBITDA of 17.4x reflect quality but not distress. With only a 1.2% margin of safety to intrinsic value, upside appears limited absent multiple expansion or earnings acceleration.

For long-term dividend investors prioritizing capital preservation and steady compounding, PepsiCo remains a dependable holding. However, at current levels, it offers stability more than opportunity. The stock fits best within portfolios seeking durable income growth and low operational risk rather than outsized total return potential.