Kimberly-Clark - A Classic Defensive Dividend Holding

Steady cash flows and a near-5% yield underpin long-term income appeal, while modest growth keeps total return expectations restrained.

Investment Thesis: Durable Consumer Staples Franchise Built for Income Stability Rather Than Growth Acceleration

Kimberly-Clark KMB 0.00%↑ occupies a distinctly defensive position within consumer packaged goods, anchored in everyday hygiene categories where demand persists regardless of economic cycles. Its brand portfolio — spanning Huggies, Pull-Ups, Kotex, Depend, Kleenex, and Cottonelle — ties the company to recurring consumer habits rather than discretionary spending patterns. The professional segment further broadens demand exposure by supplying sanitation products to workplaces and institutions, creating a revenue base tied to ongoing consumption rather than replacement cycles.

Geographically, the business remains balanced. North America contributes just over half of total revenue, Europe accounts for more than 10%, and the remainder comes primarily from Asia and Latin America. This mix reduces reliance on any single economy while keeping exposure tilted toward developed markets where hygiene consumption is relatively predictable.

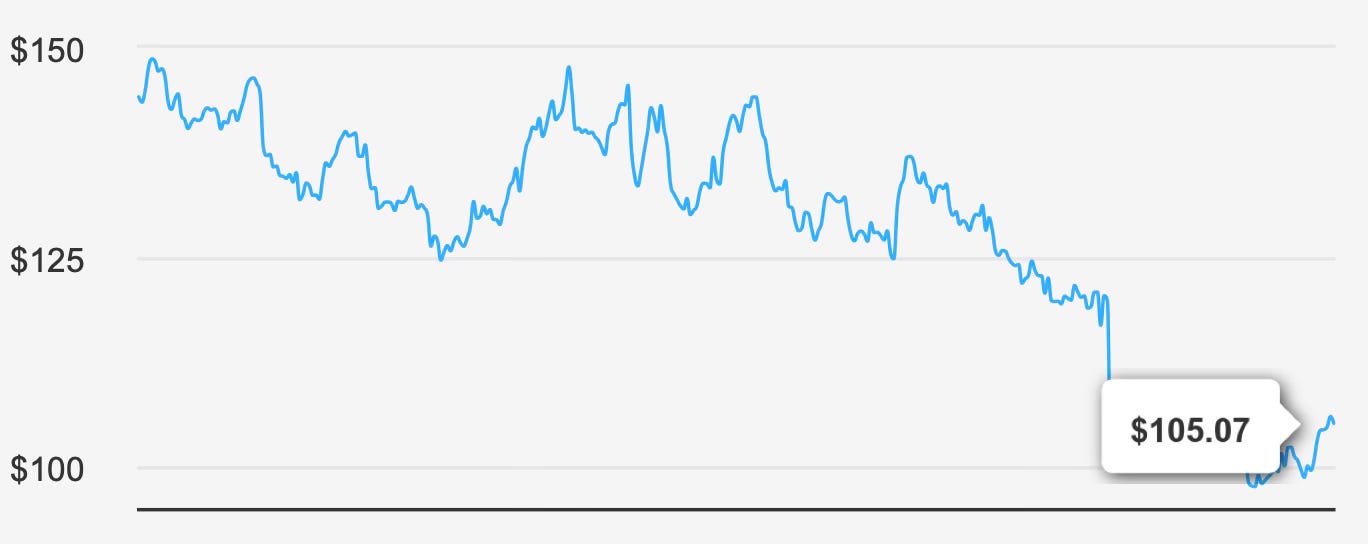

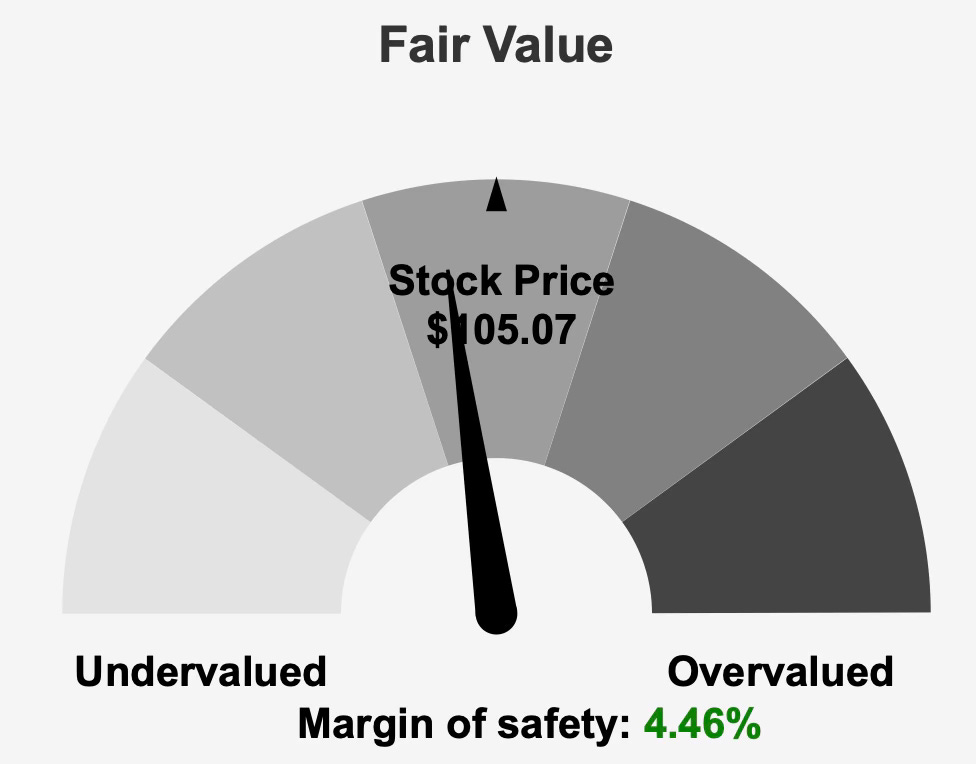

The market currently values the shares near $105, modestly below an intrinsic value estimate of roughly $110, implying a margin of safety slightly above 4%. This discount is narrow and consistent with a company whose investment appeal lies in reliability rather than expansion. Over five years, revenue has declined about 1.4% annually, while the ten-year growth rate is only about 1.2%. These figures confirm the business operates in a mature category where demographic stability replaces organic expansion as the central operating condition.

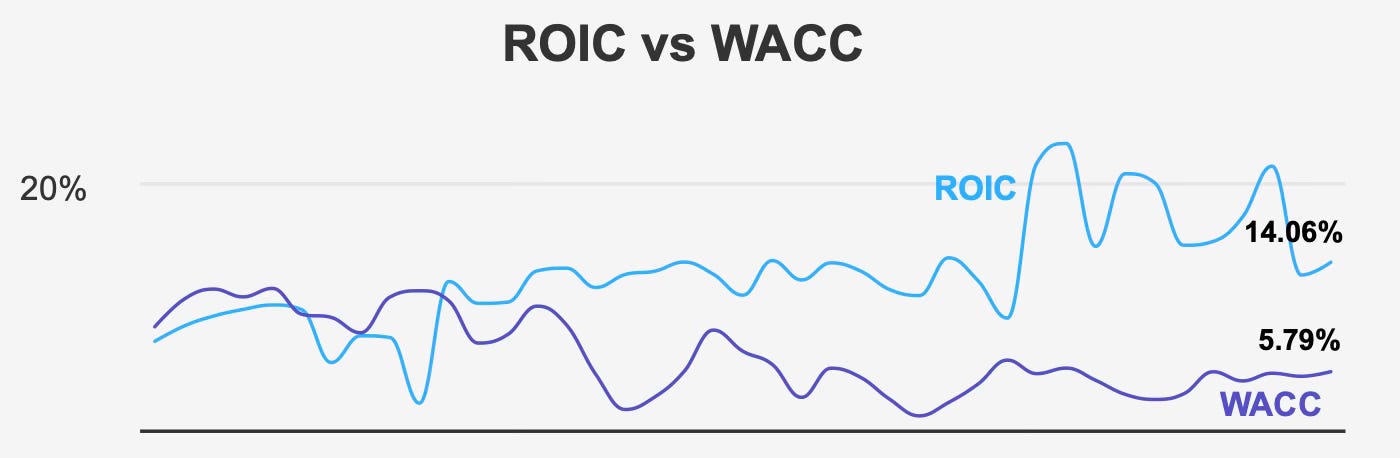

Yet the investment case does not depend on growth. Kimberly-Clark consistently generates economic value: its five-year median return on invested capital stands near 15.6% against a cost of capital around 5.4%, and current returns remain similarly strong at roughly 14.1% versus 5.8%. This persistent spread reflects brand strength, cost discipline, and pricing power rather than volume expansion. Even modest growth can support shareholder returns when capital efficiency remains high.

The thesis therefore centers on dependable income generation. Investors are not purchasing a compounding growth engine; they are acquiring a defensive equity whose return profile comes from dividend yield plus incremental earnings progression. The primary constraint is the same as the primary strength: stability limits upside but protects downside.

2. Earnings Momentum & Profitability Trends

Recent earnings performance reinforces the company’s steady operating pattern. Fourth-quarter diluted EPS reached $1.50, improving from $1.34 in the previous quarter but slightly below $1.53 recorded two quarters earlier. Excluding non-recurring items, EPS measured $1.43, down marginally from $1.45 in the prior quarter and from $1.50 one year earlier.

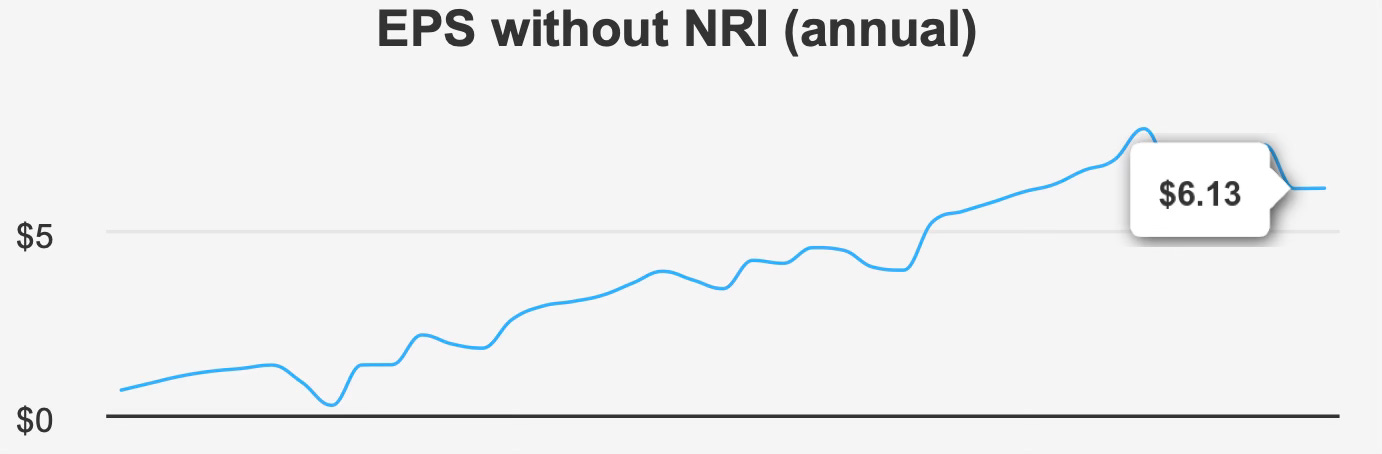

Long-term growth metrics confirm that earnings are essentially flat over time. Annual EPS excluding non-recurring items has declined around 1.5% annually over five years and increased only about 0.7% annually over a decade. Kimberly-Clark is therefore maintaining profitability rather than expanding it — a key distinction for investors evaluating dividend durability versus growth potential.

Margins, however, remain a source of strength. Gross margin currently sits near 35.7%, above the five-year median of about 34.4% and close to a ten-year peak around 36.6%. This indicates that pricing and cost control offset volume pressure, allowing the company to preserve profitability even when revenue growth stagnates.

Capital efficiency amplifies this stability. Return on equity remains extraordinarily high, with a five-year median near 290% and a current figure around 167%. While such levels partly reflect accounting equity structure, they nonetheless demonstrate efficient profit extraction from invested capital. More importantly, returns on invested capital consistently exceed capital costs by a wide margin, confirming the business continues to create economic value despite slow top-line expansion.

Share repurchases have historically played only a minor role. Over the past decade the company retired roughly 0.8% of shares annually, but buybacks were effectively zero in the most recent year and averaged about 0.6% over three years. Earnings growth therefore stems from operations rather than financial engineering, placing dividends at the center of shareholder return.

Forward expectations mirror the past. Revenue is projected to rise gradually from about $16.9 billion in 2026 to $17.5 billion in 2027 and $18.4 billion in 2028. EPS is expected to reach approximately $7.15 and $7.70 in the next two fiscal years. These projections describe a business advancing slowly through price adjustments, product mix improvements, and efficiency initiatives rather than cyclical demand surges.

Overall, Kimberly-Clark’s earnings profile supports dividend stability: modest growth, stable margins, and consistently positive economic returns.

3. Dividend Profile & Sustainability

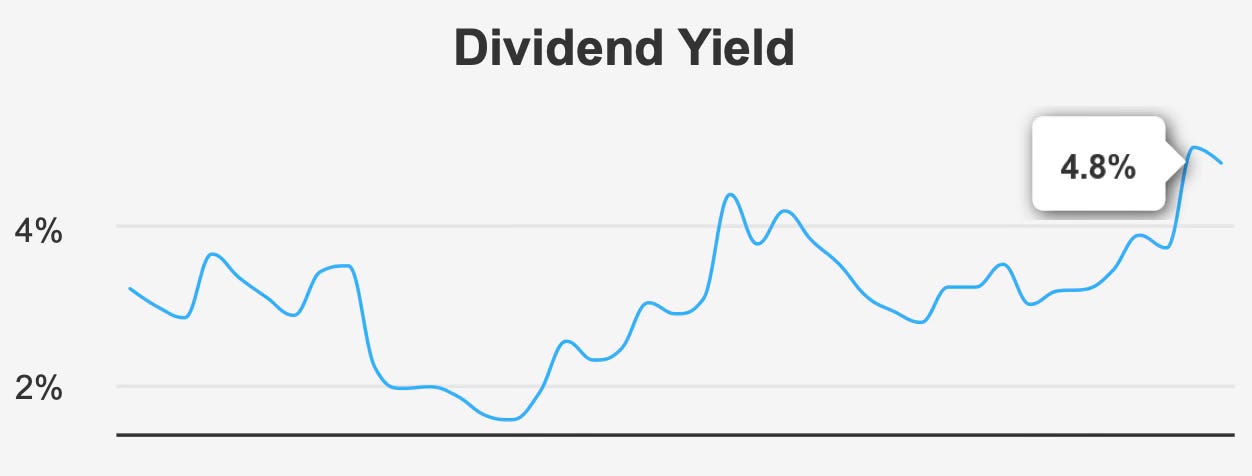

The dividend remains the primary reason investors hold Kimberly-Clark. The forward yield approaches 4.9%, positioning the shares firmly within income-oriented portfolios. The most recent quarterly distribution increased to $1.28 from $1.26, continuing a pattern of gradual annual raises.

Growth in the payout is intentionally conservative. The dividend has expanded about 3.0% annually over five years and roughly 2.8% over three years, with forward expectations around 3.5% annually. This closely tracks long-term earnings growth, indicating management maintains a payout policy aligned with profit expansion rather than attempting to accelerate shareholder distributions beyond operational capacity.

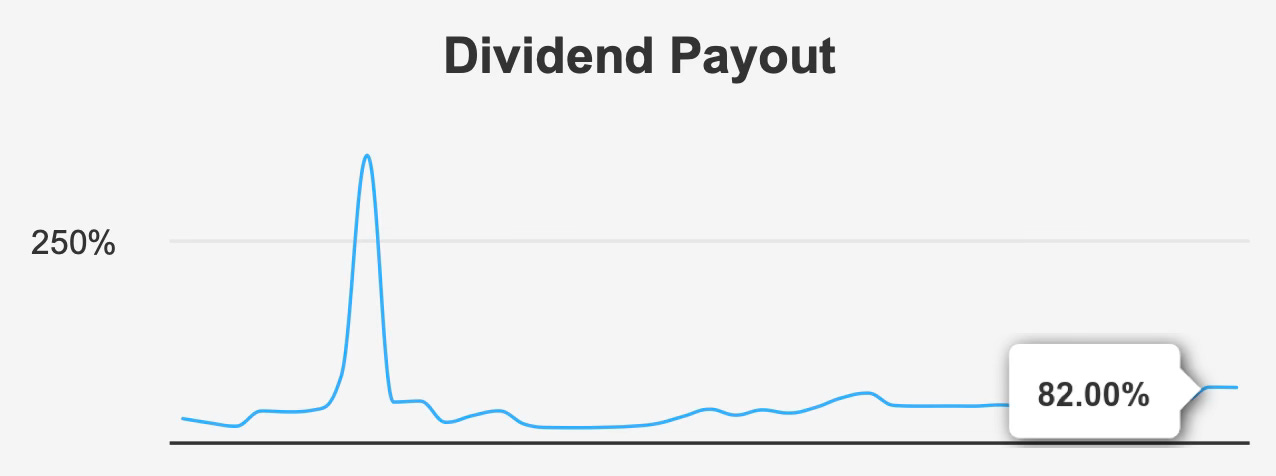

The sustainability discussion therefore revolves around coverage rather than growth. The payout ratio stands near 82%, leaving limited margin for earnings volatility. Dividend coverage of approximately 1.2 suggests the dividend is supported but not heavily cushioned. In a stable consumer staples business this can remain viable, yet it restricts flexibility during periods of cost inflation or pricing pressure.

Leverage reinforces the balance. Debt-to-EBITDA sits around 2.2 — moderate but not insignificant. The company must continue generating steady cash flow to maintain both leverage and dividend commitments simultaneously. In practical terms, dividend increases will likely remain modest because excess cash flow is limited.

Payment timing underscores consistency. The next ex-dividend date is scheduled for early March 2026 with payment in early April, maintaining a predictable quarterly cadence. The reliability of this schedule contributes to the stock’s role as an income anchor rather than a growth vehicle.

The dividend is therefore dependable but mature. Investors should expect steady income and incremental increases rather than rapid growth.

4. Valuation: Relative Pricing Suggests Fair Value With Income-Driven Return Expectations

Kimberly-Clark’s valuation aligns closely with its fundamental profile: stable, modestly undervalued, but not materially mispriced. The shares trade slightly below intrinsic value, leaving only a small margin of safety. Consequently, future returns depend more on dividends and earnings progression than on multiple expansion.

The forward earnings multiple sits around 13.9x, below the trailing level near 17.3x and well below the ten-year median of about 22.4x. This compression reflects investor expectations for slow growth rather than weakening profitability. The market assigns a lower earnings multiple because expansion potential is limited, not because the business is deteriorating.

Enterprise valuation conveys a similar message. EV/EBITDA of roughly 12.8x remains below the long-term median near 14.5x yet above the decade low near 10.9x. The stock therefore trades in a balanced zone between undervaluation and normalization.

Free cash flow valuation appears somewhat tighter. A price-to-free-cash-flow ratio around 21.4x exceeds the long-term median of about 20.0x, suggesting investors pay a small premium for dependable cash generation and dividend reliability. By contrast, price-to-sales near 2.0 remains below the historical median around 2.3, indicating revenue growth expectations remain subdued.

Overall valuation signals neither a bargain nor a warning. The stock behaves like a bond-proxy equity: yield drives total return, while valuation remains anchored within a narrow historical range.

5. Risk Assessment & Capital Structure Considerations

Kimberly-Clark’s risk profile is balanced between defensive stability and financial rigidity. The most visible concern is the high payout ratio combined with slow revenue growth. Dividend sustainability depends heavily on maintaining margins rather than expanding sales.

Financial strength metrics reinforce a middle-ground assessment. The Altman Z-score sits near 2.7, placing the company in a grey area — financially stable but not immune to pressure. Leverage around 2.2x EBITDA remains manageable yet limits flexibility for aggressive buybacks or accelerated dividend increases.

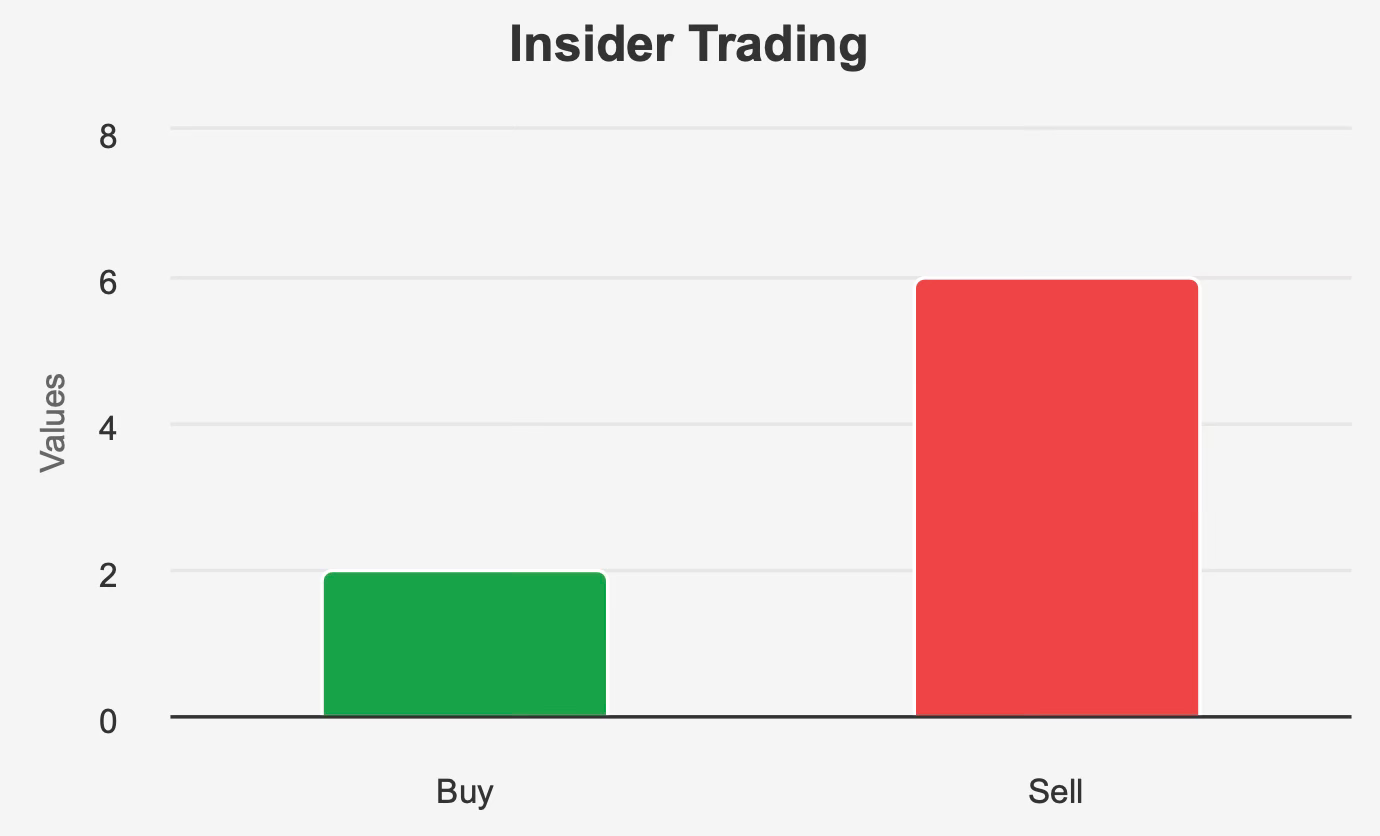

Accounting quality appears sound. The Beneish M-score suggests a low likelihood of earnings manipulation. Institutional ownership exceeds 80%, indicating strong long-term investor participation, though insider ownership remains low, implying limited direct alignment between management and shareholders.

Trading liquidity remains robust, supported by historically high average daily volume, although recent trading activity has temporarily declined. A substantial portion of transactions occurs in private exchanges, suggesting institutional investors dominate price discovery.

Overall, risks relate primarily to stagnation rather than collapse. Margin compression, cost inflation, or sustained volume decline could pressure dividend growth, but the probability of severe financial distress appears limited under current conditions.

Final Assessment

Kimberly-Clark represents a classic mature dividend stock: reliable, predictable, and deliberately slow growing. The company generates economic value through strong brands and disciplined capital allocation rather than expansion. Profitability remains stable, margins are resilient, and capital returns consistently exceed capital costs.

The dividend yield near 5% forms the backbone of expected shareholder returns, with growth likely in the low-single-digit range. The payout ratio limits flexibility but remains sustainable under stable operating conditions. Valuation appears fair — slightly below intrinsic value but not sufficiently discounted to create a strong capital appreciation thesis.

In practical terms, the stock functions best as an income anchor rather than a total-return driver. Investors seeking dependable cash flow and moderate volatility may find it appropriate, while those requiring meaningful earnings growth or multiple expansion will likely find limited upside.

The overall conclusion is balanced: Kimberly-Clark offers stability and income, but its return profile depends on patience and yield rather than acceleration.