Johnson & Johnson: Premium Quality, Premium Price

A textbook income compounder - but not at this entry point

1. Investment Thesis: A High-Quality Defensive Franchise Trading Beyond Its Fundamental Worth

Johnson & Johnson JNJ 0.00%↑ stands among the most durable business models in global healthcare. After the 2023 separation of its consumer division, the company now operates through two focused pillars — innovative medicine and medtech — concentrating on immunology, oncology, and neurology. Slightly more than half of revenue originates in the United States, giving the company both scale and geographic diversification.

The investment case rests on three strengths: predictable demand, high returns on capital, and consistent shareholder distributions. The company generates returns comfortably above its cost of capital, carries moderate leverage, and maintains one of the most reliable dividend growth records in the market.

However, the problem facing long-term investors today is not quality — it is price.

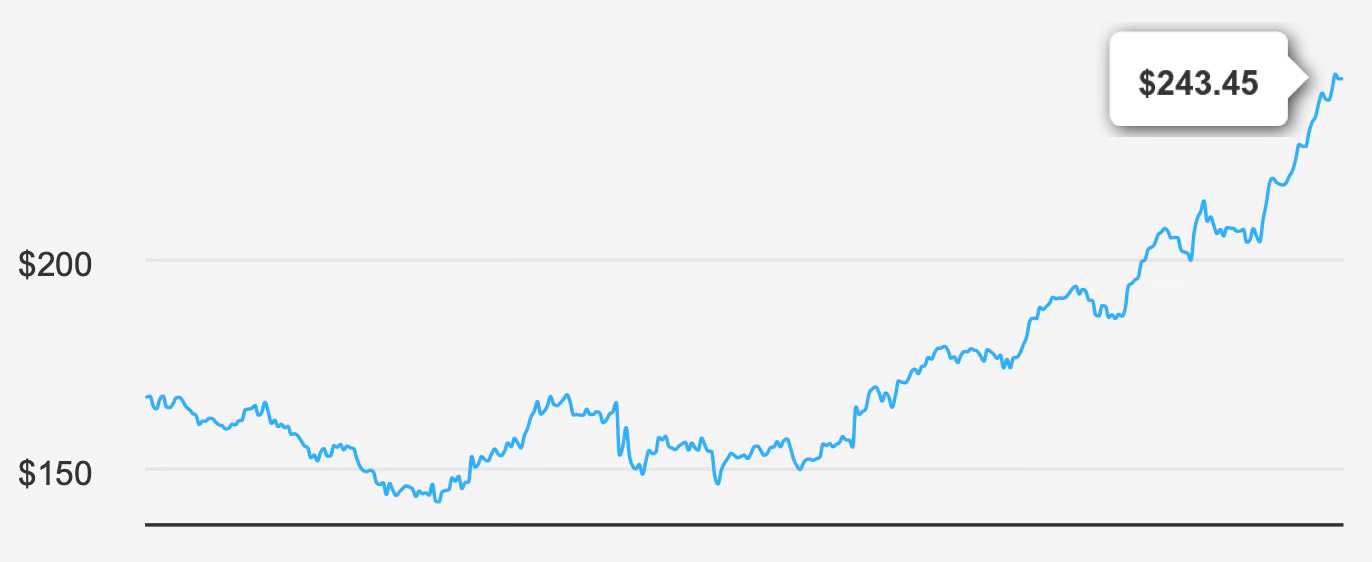

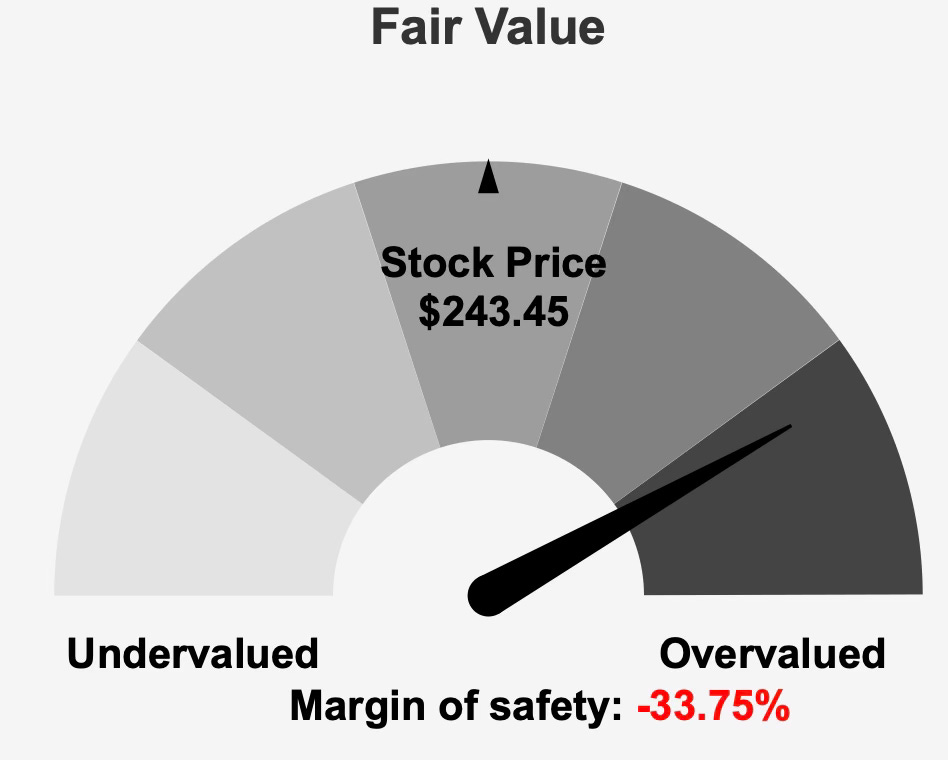

The shares trade around $243 versus an estimated intrinsic value of roughly $182, implying a negative margin of safety of about 33.8%. That disconnect matters because Johnson & Johnson is not a high-growth company. Its five-year earnings growth rate sits near 4.0%, and revenue growth has remained close to the low-single-digit range over long periods.

In other words, the market is paying a premium multiple for a stability profile rather than a growth profile.

For dividend investors, this creates a paradox: the company itself is financially strong and dependable, yet prospective returns are constrained by valuation compression risk. The dividend is secure, but total return potential is limited unless fundamentals accelerate beyond historical norms.

The core thesis therefore separates business strength from shareholder outcome. Johnson & Johnson remains a best-in-class defensive compounder, but at the current price investors are pre-paying for many years of reliability.

2. Earnings Momentum & Profitability Trends: Slow Growth Supported by Exceptional Capital Efficiency

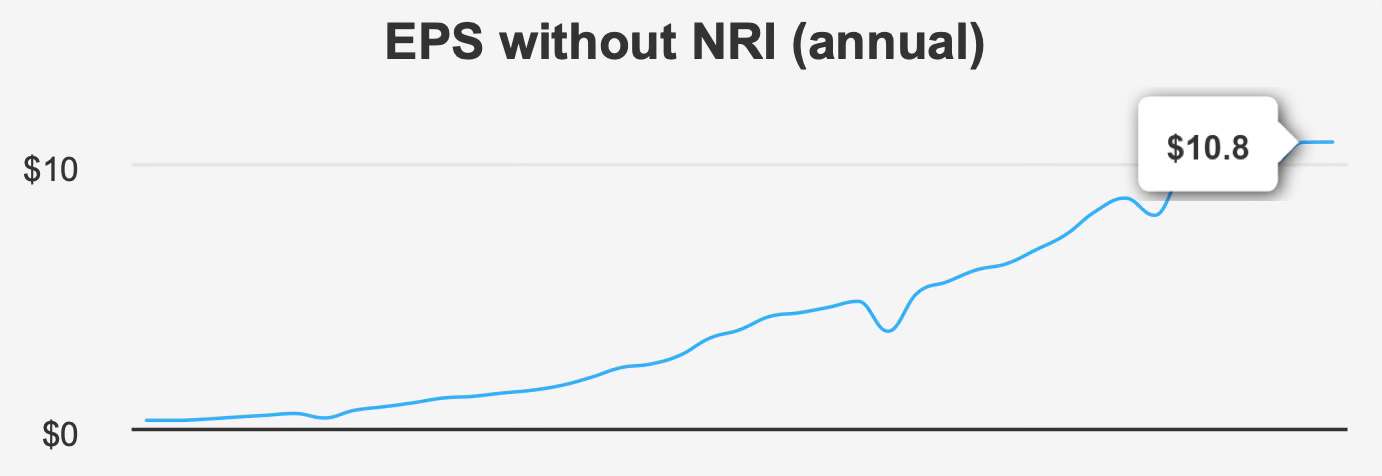

Recent operating results illustrate the company’s steady but unspectacular expansion profile. Fourth-quarter 2025 adjusted EPS came in at $2.46, improving from $2.04 a year earlier though declining sequentially from $2.80 in the prior quarter. Diluted EPS showed a similar pattern, rising meaningfully year over year but only modestly quarter to quarter.

Revenue per share increased to $10.05 from $9.27 the year before, confirming that growth remains incremental rather than cyclical. Over extended periods the pattern is consistent: earnings per share expanded at roughly 4.0% annually over five years and about 5.9% over a decade.

Margins reinforce the same story — stability over acceleration. Gross margin registered 67.9%, slightly below its long-term medians around 69%, suggesting modest pressure but no structural deterioration.

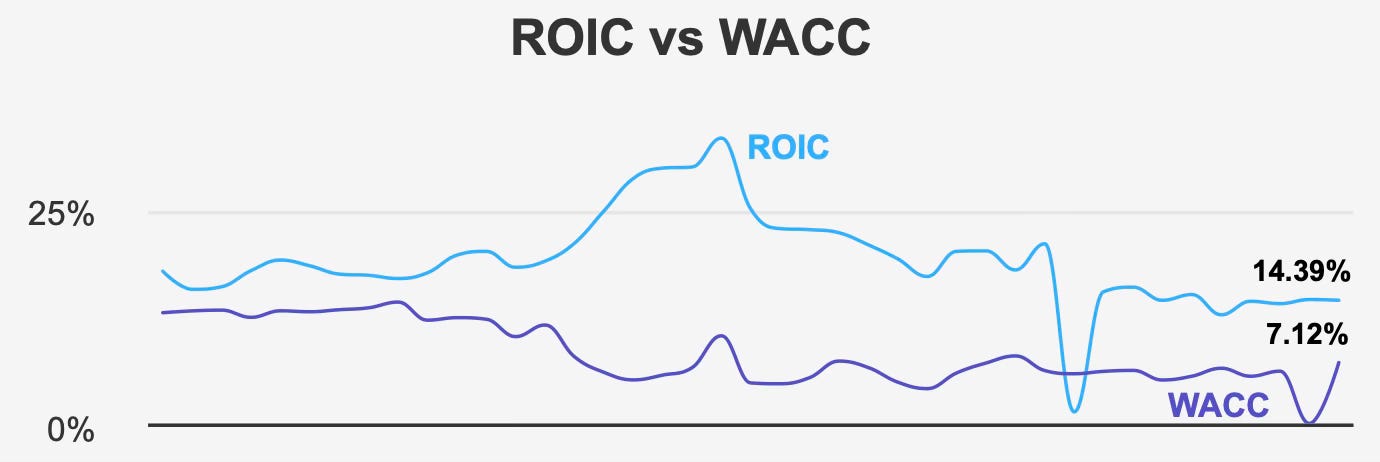

Where Johnson & Johnson truly differentiates itself is capital efficiency.

Return on invested capital currently sits near 14.9% against a cost of capital around 7.1%, producing a spread of approximately 7.8%. Over five years the median ROIC has held around 14.3% while WACC averaged near 5.5%, confirming persistent economic value creation across cycles.

Return on equity reinforces this picture, with a five-year median close to 24.0%. The company is not growing quickly, but it converts investment into profits exceptionally well.

Share repurchases have played a secondary role. Over a decade, buybacks reduced the share count by about 1.3%, and a more active 2.9% reduction occurred across the last three years, though no repurchases took place during the past year. This indicates management prioritizes dividends and reinvestment rather than aggressive financial engineering.

Looking forward, consensus expectations call for revenue to reach roughly $100.5 billion in 2026 and $112.2 billion by 2028, with EPS projected near $9.83 next year and about $10.58 the year after. These projections align closely with the historical mid-single-digit trajectory.

The earnings profile therefore remains clear: Johnson & Johnson is a slow-growing but highly efficient compounder whose value proposition relies on reliability rather than expansion.

3. Dividend Profile & Sustainability: A Reliable Income Stream Backed by Strong Coverage

Johnson & Johnson’s dividend is not merely consistent — it is engineered to be conservative.

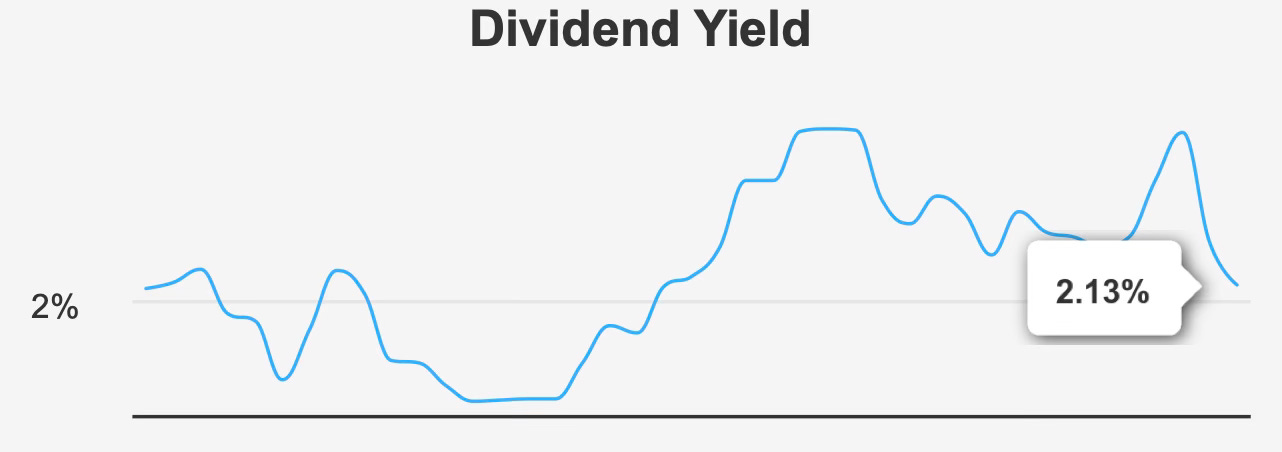

The forward yield stands around 2.13%, slightly above its historical low but still below the long-term median of 2.62%. The modest yield reflects the market’s willingness to accept lower income in exchange for reliability.

Growth remains steady rather than aggressive. Dividends have expanded approximately 5.6% annually over five years and 5.4% over three years, closely matching earnings growth. Management forecasts a similar 5–6% range over the next several years, signaling a deliberate policy of sustainable increases rather than cyclical raises.

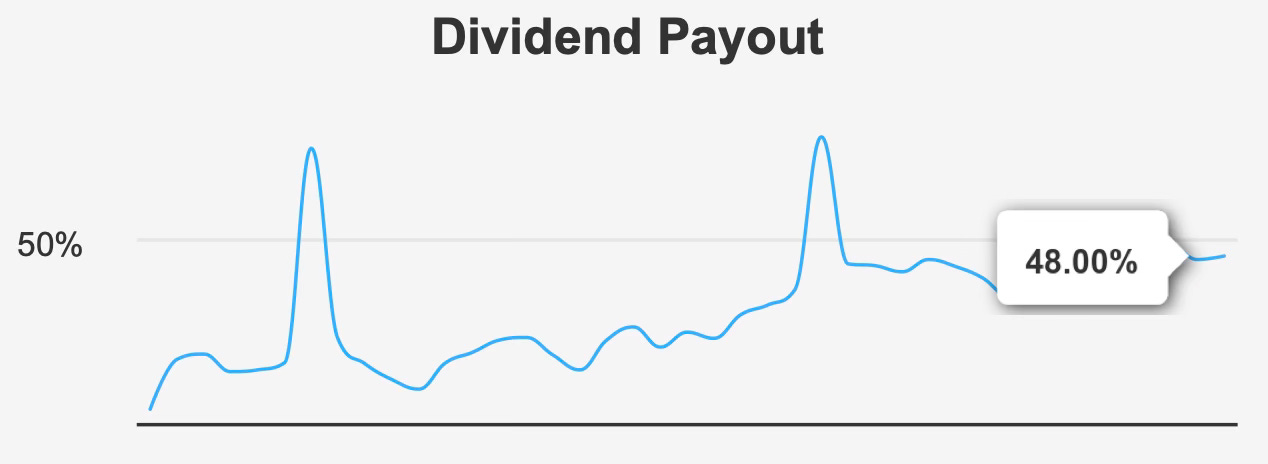

Coverage ratios reinforce confidence. The payout ratio is about 48%, giving the company ample flexibility through economic cycles. Debt metrics are equally supportive — debt to EBITDA stands near 1.79, comfortably below typical caution thresholds.

Dividend coverage around 2.15x indicates earnings more than double the required distribution.

The upcoming ex-dividend date is February 24, 2026, with payment scheduled March 10, maintaining the company’s predictable quarterly cadence.

What makes the dividend particularly durable is the underlying economics: strong returns on capital paired with moderate leverage. Unlike high-yield equities that rely on payout ratios near the limit, Johnson & Johnson funds its dividend from recurring profitability rather than balance-sheet strain.

The trade-off is simple. Investors receive stability instead of high income. The dividend will almost certainly continue growing — but not rapidly enough to offset a significant valuation contraction.

4. Valuation: Premium Multiples Applied to Modest Growth Expectations

Valuation currently represents the central risk to long-term returns.

At roughly $243 per share, the stock trades materially above its calculated worth near $182, leaving a negative margin of safety close to 33.8%.

Earnings multiples are not extreme relative to history but are elevated relative to growth. The trailing P/E is about 22.0x, slightly below the decade median near 23.9x, while forward earnings imply roughly 21.1x. For a company growing earnings around 4–6%, this represents a stability premium.

Cash flow valuation is more stretched. Price-to-free-cash-flow sits around 31.6x, near a decade high, indicating investors are paying aggressively for dependable cash generation.

Sales-based valuation also reflects optimism. A price-to-sales ratio of about 6.3x approaches historical highs, and price-to-book near 7.4x is similarly elevated.

Even enterprise valuation offers limited relief — EV/EBITDA around 15.0x remains only slightly below its long-term average.

Analyst expectations reinforce the same conclusion. A recent average price target near $230 remains below the current market level, suggesting upside is already largely priced in.

The market is effectively capitalizing Johnson & Johnson as a bond-like equity: low volatility, dependable income, and predictable growth. That premium may persist, but it leaves minimal margin for disappointment.

In valuation terms, investors are buying certainty at a price that assumes certainty will never falter.

5. Risk Assessment & Capital Structure Considerations: Financial Strength Offsets Operational Risks but Not Pricing Risk

Financial risk remains low.

The Altman Z-score stands around 4.17, indicating minimal bankruptcy probability, while a Beneish M-score near −2.54 suggests clean accounting practices. These metrics confirm the company’s reputation for conservative financial management.

Leverage has increased modestly, with roughly $22.1 billion in new debt issued over three years, but coverage ratios remain comfortable. Debt-to-EBITDA below 2.0 preserves flexibility during downturns.

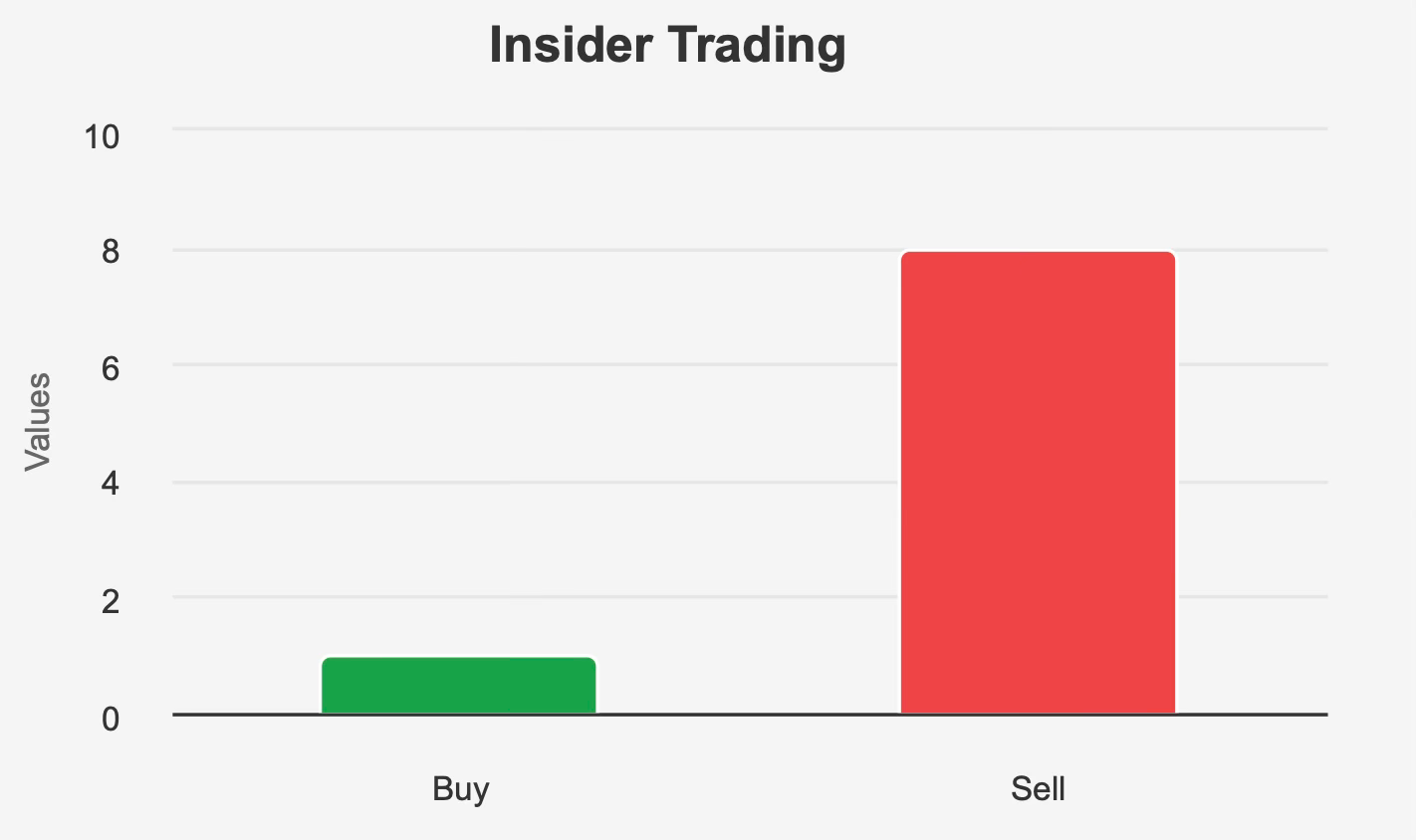

Ownership structure adds stability. Institutional investors hold about 74.2% of shares, supporting governance oversight, while insider ownership remains minimal at 0.19%. Insider transactions have skewed toward selling rather than buying, which may reflect valuation awareness rather than operational concern.

Operational risk is relatively modest because healthcare demand is non-cyclical. However, valuation risk dominates. With the stock trading near decade-high multiples and near its high price levels, the primary downside is multiple compression rather than earnings collapse.

This distinction matters: the business is unlikely to deteriorate quickly, but shareholder returns can still disappoint if expectations normalize.

Final Assessment

Johnson & Johnson exemplifies a high-quality defensive investment. It produces consistent cash flows, earns returns well above its cost of capital, maintains conservative leverage, and grows its dividend at a sustainable mid-single-digit pace.

From a business perspective, very little is wrong.

From an investment perspective, the issue is entry price.

The shares currently reflect a premium valuation relative to intrinsic value and growth prospects. A stable 5–6% earnings trajectory paired with a roughly 2% yield cannot reasonably support a valuation significantly above historical norms indefinitely.

For existing shareholders, the company remains a dependable long-term holding. The dividend appears secure and likely to grow steadily. Selling solely due to business risk would not be justified.

For new investors, however, expected returns are constrained. The absence of a margin of safety shifts the investment from income compounding to valuation speculation.

Johnson & Johnson remains an exceptional company — but at today’s price, it is no longer an exceptional investment opportunity.