General Mills: A High-Yield Consumer Staple Trading at a Discount to Its Economic Value

Assessing income sustainability amid modest growth expectations

Investment Thesis: A Defensive Consumer Franchise Trading Below Its Normalized Economic Worth

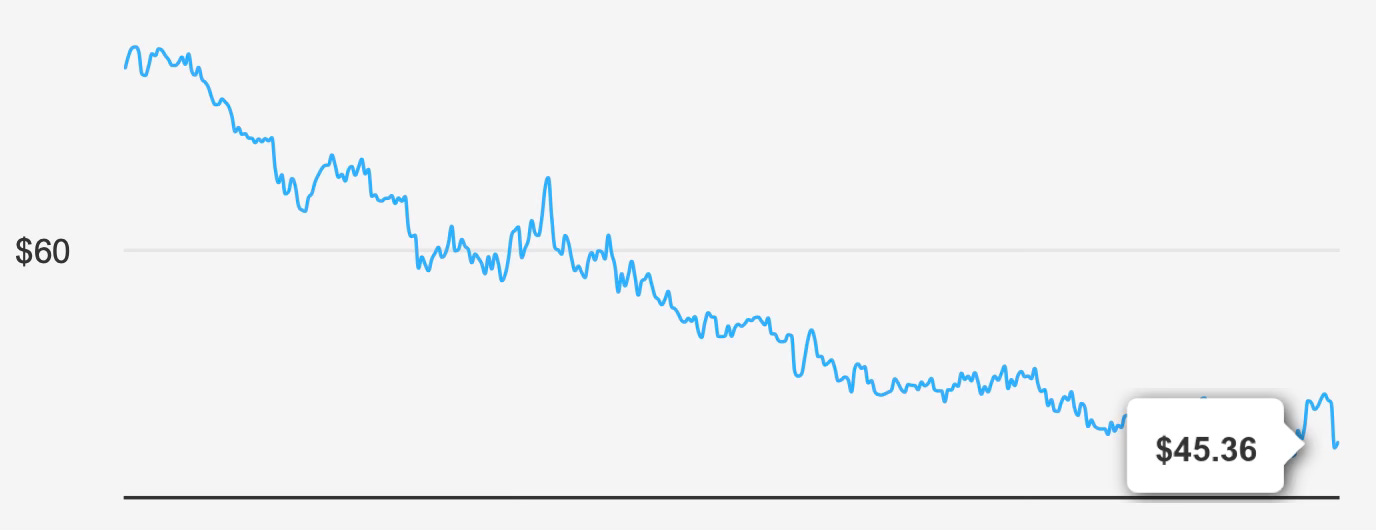

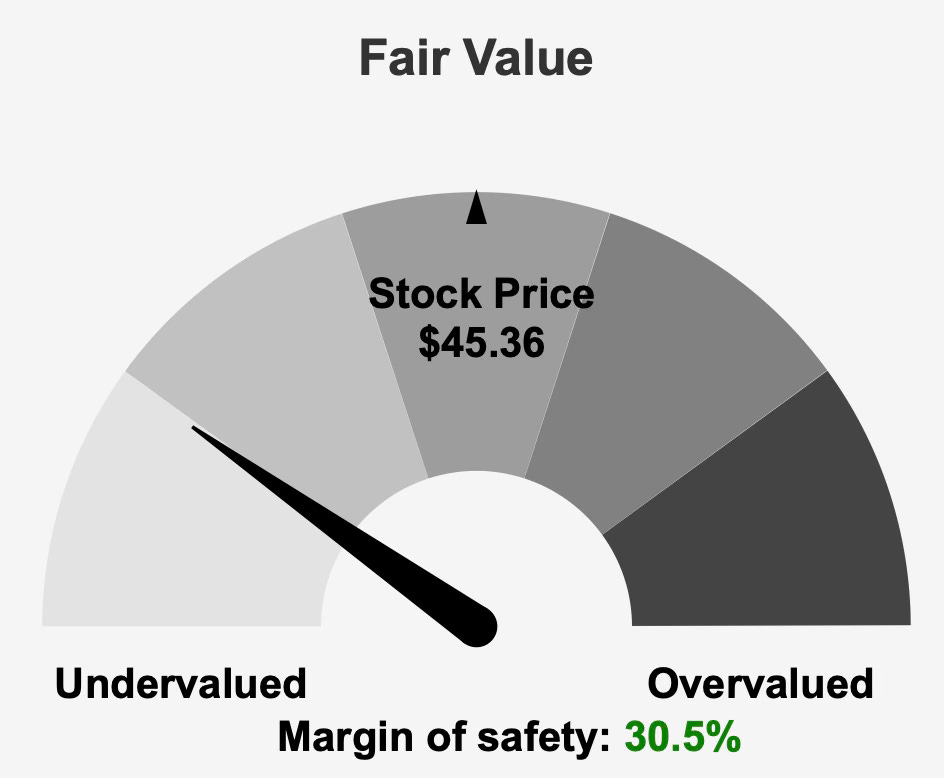

General Mills GIS 0.00%↑ currently represents a rare combination in the consumer staples sector: stable operating economics, a well-covered dividend yield above 5%, and a valuation materially below both intrinsic value and long-term trading norms. At roughly $45 per share against an estimated intrinsic value of $65.27, the equity trades with a margin of safety of about 30.5%, placing it firmly in deep value territory for a defensive branded food company.

The investment case does not depend on rapid expansion. Instead, it rests on resilience — slow but persistent earnings growth, consistent capital returns, and the ability to generate returns above the company’s cost of capital across cycles. Over the past five years, earnings without non-recurring items grew at a compound rate of 2.7% and approximately 5.0% over ten years, reflecting a mature but durable earnings engine rather than a growth narrative.

General Mills operates a portfolio of enduring consumer brands spanning cereals, snacks, baking products, and pet food, with 81% of revenue derived from the United States but supported by international distribution across Europe, Canada, Asia, and Latin America. This geographic and category breadth reduces cyclicality and stabilizes cash generation — a critical factor for dividend investors.

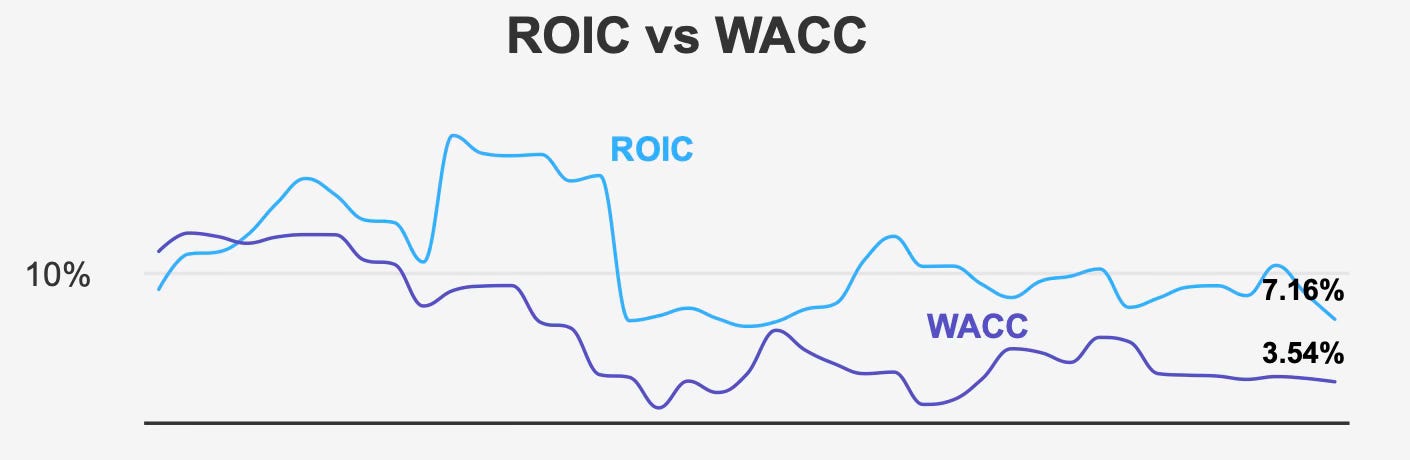

Importantly, economic profitability remains intact. The company’s five-year median return on invested capital of 9.02% comfortably exceeds its weighted average cost of capital of 3.84%. Even the current ROIC of 7.16% remains well above the 3.54% cost of capital. This persistent positive spread confirms that capital deployment continues to create value despite slower growth.

In short, the thesis is not about acceleration but normalization. The stock does not require multiple expansion to deliver acceptable returns — merely stability. Investors are effectively being paid a 5%+ yield while waiting for valuation to revert toward historical ranges.

Earnings Momentum & Profitability Trends

Recent quarterly results illustrate the company’s operating reality: modest growth punctuated by margin pressure but supported by consistent demand. In the quarter ending November 2025, earnings excluding non-recurring items reached $1.10 per share, improving from $0.86 in the prior quarter yet below $1.40 a year earlier. Diluted EPS came in at $0.78, primarily reflecting higher operating costs rather than demand weakness.

Revenue per share rose sequentially to $9.047 from $8.327 but remained slightly under the $9.351 recorded in the comparable prior-year period. The pattern is characteristic of mature consumer staples businesses: stable demand, periodic cost inflation, and gradual pricing adjustments that smooth earnings over time rather than producing sharp growth.

Margin performance reinforces that interpretation. Gross margin of 33.76% came in just below the five-year median of 34.55% and ten-year median of 34.67%, suggesting near-term cost pressures but not structural erosion. The deviation is modest enough to imply cyclical input costs rather than competitive deterioration.

Capital allocation also contributes meaningfully to per-share performance. The company reduced its share count by 3.4% over the past year through buybacks, supporting earnings per share growth even as operating profit remained steady. For a low-growth enterprise, consistent repurchases are a meaningful driver of shareholder return.

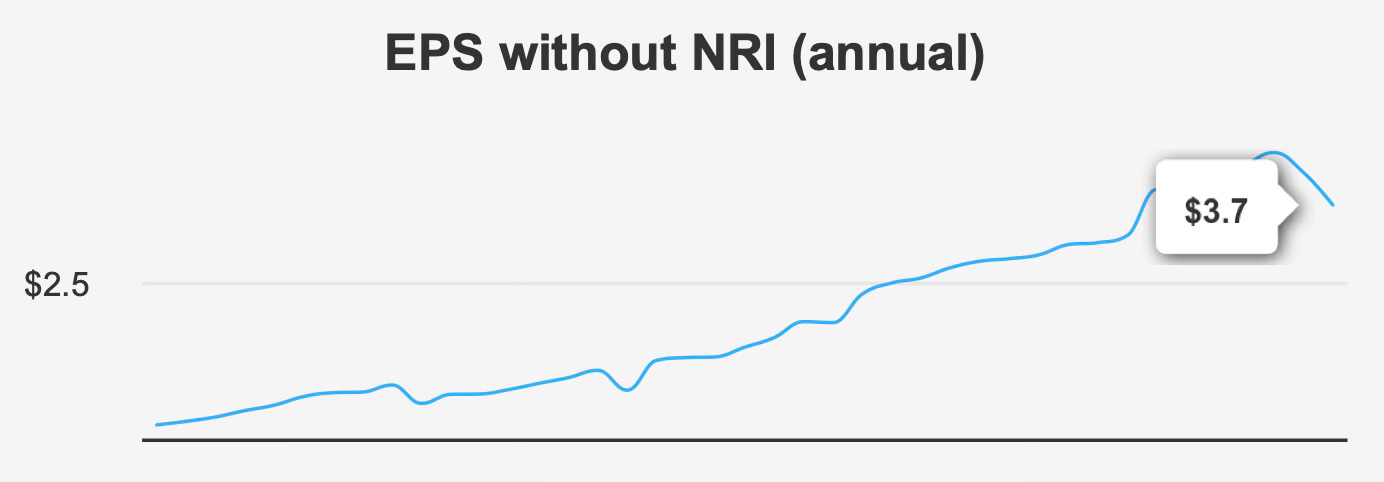

Forward expectations remain conservative. Analysts anticipate revenue of approximately $18.60 billion in 2026, easing to $18.44 billion in 2027 before recovering to $18.81 billion in 2028. Next fiscal-year EPS is projected around 4.783, indicating continued stability rather than acceleration.

Profitability metrics remain strong despite modest growth. A five-year median return on equity of 25.16% and current ROE of 27.29% demonstrate efficient use of shareholder capital. Combined with positive economic profit, this suggests the company’s competitive positioning is intact.

Overall, earnings quality is the defining feature — predictable, resilient, and sufficient to support long-term distributions.

Dividend Profile & Sustainability

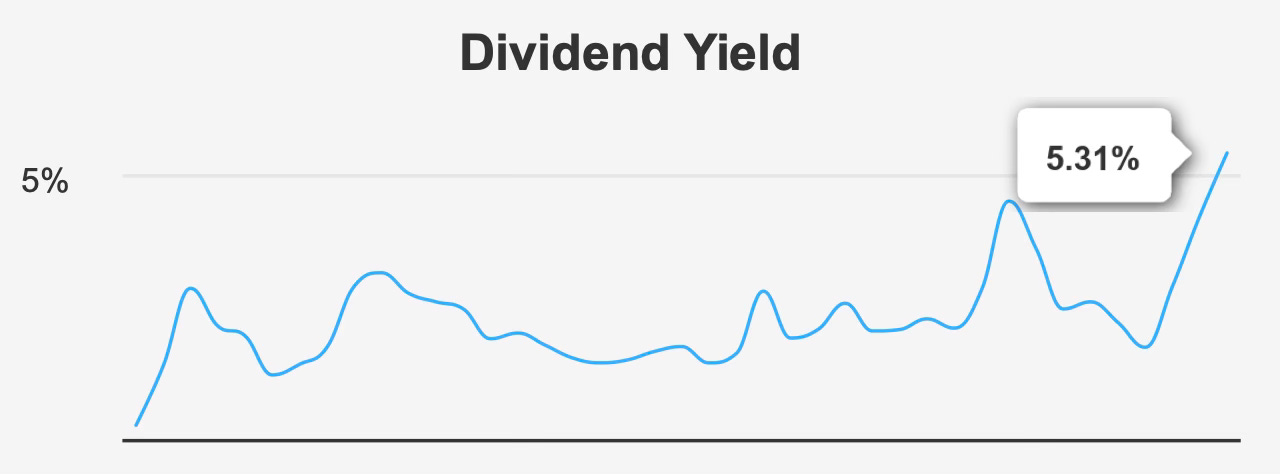

The dividend is the central attraction. The forward yield stands at 5.31%, significantly above the company’s ten-year median of 3.40%, placing the stock among higher-income options within consumer staples.

The most recent quarterly dividend of $0.61 per share reflects stability rather than aggressive growth. Over the past five years, dividend growth averaged 4.5%, accelerating to 5.6% over three years but expected to slow to roughly 2.23% in the coming three to five years.

This projected slowdown is important. It indicates management is prioritizing sustainability over expansion — a rational decision given moderate leverage and slower earnings growth.

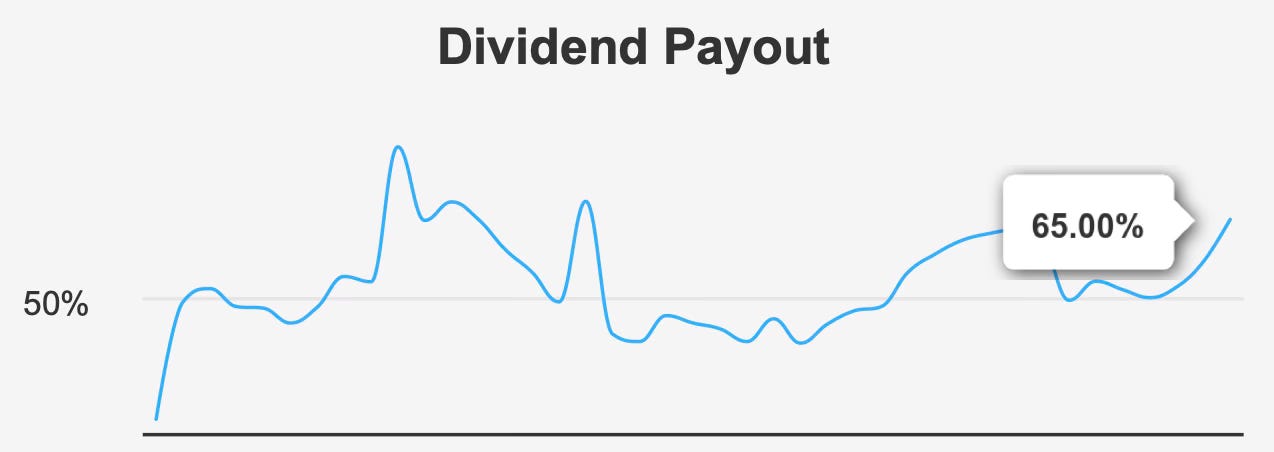

Coverage appears adequate. The payout ratio sits near 65%, lower than historical highs and consistent with a mature consumer staples company maintaining a dependable distribution. Dividend coverage of approximately 1.92 provides a reasonable buffer against earnings volatility.

Debt levels require monitoring but remain manageable. A debt-to-EBITDA ratio of 3.97 places the company in a moderate risk category, suggesting leverage is meaningful but not excessive for a stable cash flow business. The steady free cash generation typical of food manufacturers supports continued distributions despite leverage.

Importantly, the company’s ability to consistently generate returns above its cost of capital strengthens dividend reliability. Firms creating economic profit rarely cut dividends absent severe external shocks.

Taken together, the dividend should be viewed primarily as an income instrument with modest growth rather than a dividend growth story. Investors receive immediate yield while expecting slow annual increases aligned with inflation-like earnings expansion.

Valuation: Discounted Multiples Relative to Historical Trading Norms and Estimated Intrinsic Value

Valuation provides the strongest support for the investment case. At roughly $45 per share versus intrinsic value of $65.27, the equity trades meaningfully below estimated fair value.

Earnings multiples reinforce the discount. The trailing P/E ratio of 9.75x sits well below the ten-year median of 16.39x, while the forward P/E of 12.18x remains materially compressed relative to historical norms.

Enterprise valuation also suggests below-average pricing. EV/EBITDA of 10.69x sits under the decade median of 13.60x. The price-to-book ratio of 2.6x hovers near a ten-year low around 2.53x, and price-to-free-cash-flow near 13.9x remains modest relative to historical levels.

The key insight is consistency: every major valuation metric sits at or near the lower end of its historical range despite unchanged business quality. The market appears to be discounting slower growth rather than deteriorating fundamentals.

Even analyst expectations reflect muted optimism, with a price target near $50.37 — below intrinsic value estimates but still above the current market price.

For a stable consumer staple, valuation compression typically stems from rising rates, short-term margin pressure, or rotation away from defensive sectors. Such conditions rarely persist indefinitely, meaning valuation normalization alone could generate acceptable returns without operational improvement.

Risk Assessment & Capital Structure Considerations

The company’s risk profile is balanced rather than minimal.

Leverage increased by approximately $1.5 billion over the past three years, raising sensitivity to interest costs but remaining manageable given stable cash flows. The Altman Z-score of 2.47 places the firm in a gray zone — not distressed, but not immune to macroeconomic shocks.

Operationally, declining revenue per share and year-over-year earnings softness highlight a challenging cost environment. Additionally, the forward earnings multiple exceeding the trailing multiple suggests the market anticipates near-term earnings pressure rather than expansion.

Insider activity also warrants attention. Over the past year, insiders sold shares four times with no purchases, and insider ownership remains only 1.54% compared with institutional ownership of 83.47%. While not definitive, persistent selling may signal limited near-term upside expectations internally.

On the positive side, accounting integrity appears strong, with a low likelihood of earnings manipulation based on the Beneish M-Score. Liquidity is robust, with average daily trading volume exceeding 8.2 million shares and significant institutional participation indicated by a dark pool index above 60%.

Overall risk centers on stagnation rather than collapse — the primary concern is prolonged low growth, not financial instability.

Final Assessment

General Mills offers a classic income-oriented value proposition: dependable cash flows, moderate growth, and a dividend yield well above historical averages, all purchased at a discounted valuation.

The business is not accelerating. Revenue growth projections remain modest, dividend increases are slowing, and margins face periodic pressure. Yet none of these factors undermine the core investment case — a stable branded food franchise consistently generating returns above its cost of capital.

At approximately a 30% discount to intrinsic value and trading at single-digit trailing earnings multiples, investors are compensated for waiting through a yield exceeding 5%. The return profile therefore relies on three components: dividend income, gradual earnings expansion, and eventual multiple normalization.

This is unlikely to be a high-growth investment. Instead, it fits best within portfolios prioritizing income durability and downside protection. Provided leverage remains stable and earnings do not structurally deteriorate, the valuation gap alone provides a meaningful cushion.

For long-term dividend investors, the stock represents a conservative accumulation candidate — not because growth is strong, but because expectations are already low.