Flagship Communities REIT: Evaluating the Stability and Long-Term Prospects of a Manufactured Housing Income Platform

Flagship Communities REIT: Evaluating the Stability and Long-Term Prospects of a Manufactured Housing Income Platform

Investment Thesis: Evaluating the Long-Term Income Stability and Structural Growth Potential of Flagship Communities REIT

Flagship Communities REIT operates as an open-ended real estate investment trust focused on owning and managing income-producing manufactured housing communities across the United States. The trust’s core objective centers on generating predictable and sustainable cash distributions for unitholders through a portfolio of multifamily residential assets designed to deliver stable occupancy and recurring rental income.

Manufactured housing communities occupy a distinctive niche within the broader real estate market. Demand for affordable housing has remained structurally strong in many U.S. regions, particularly as traditional homeownership costs continue to rise. Within this context, operators of manufactured housing portfolios often benefit from relatively stable tenant demand, modest operating costs, and the potential for gradual rental increases. These characteristics have historically made the sector attractive for income-oriented investors seeking dependable distributions rather than rapid capital appreciation.

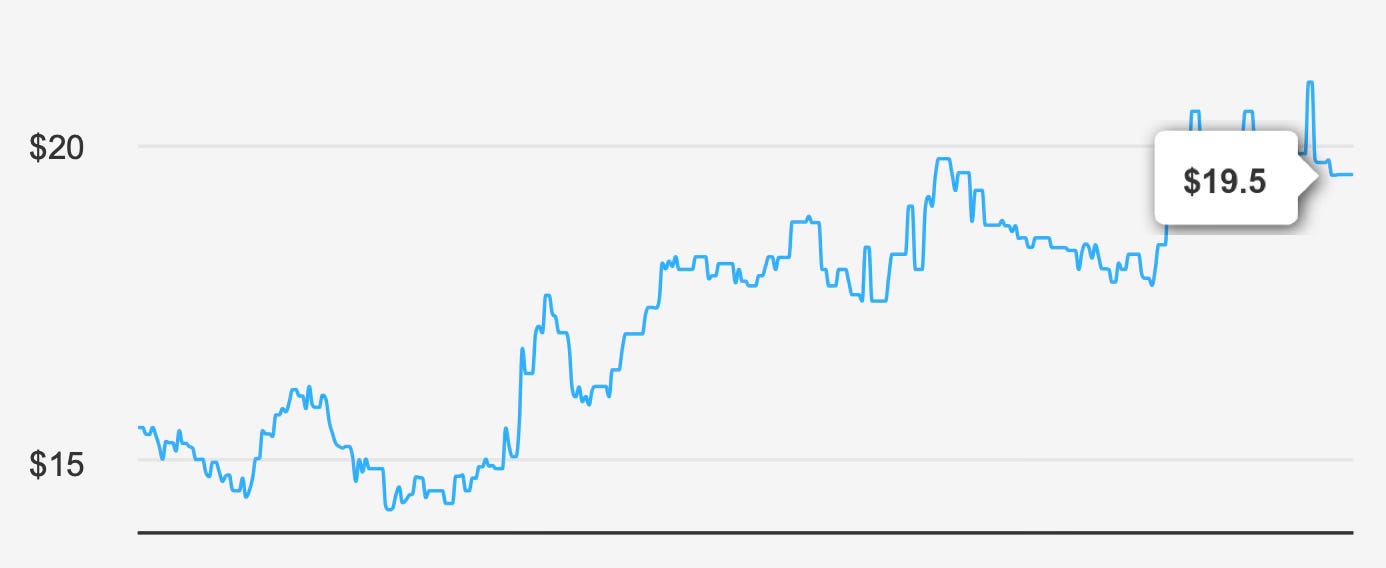

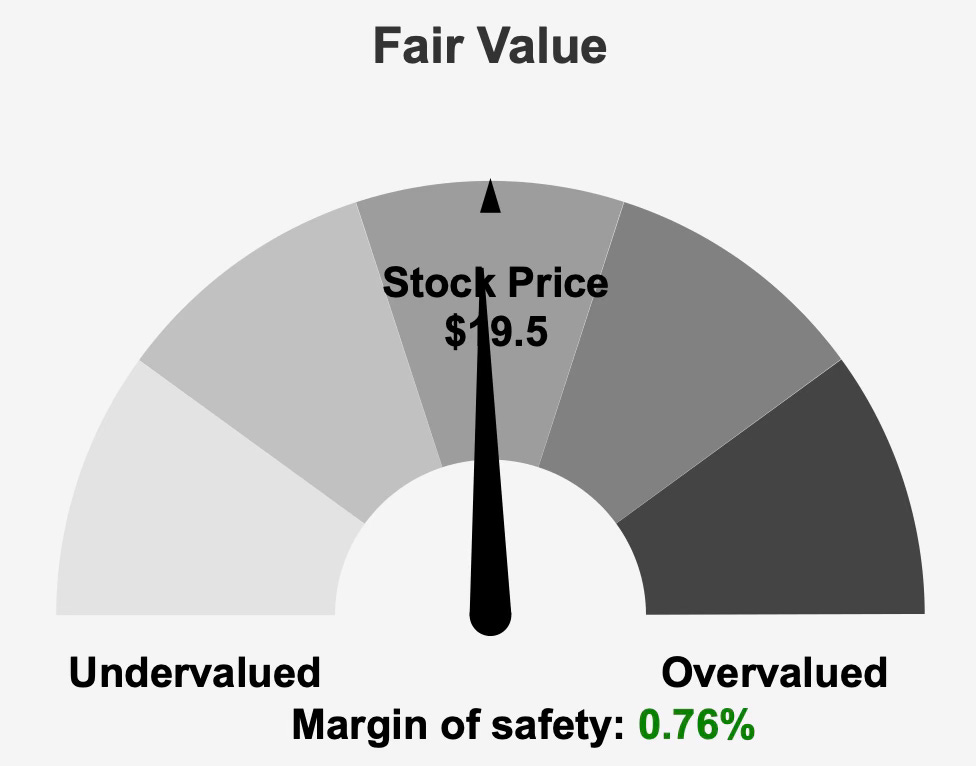

At a market capitalization of approximately $384.2 million and a current share price near $19, Flagship Communities REIT represents a relatively small but specialized platform within the REIT universe. The trust’s estimated intrinsic value of $19.65 implies only a marginal difference between market price and underlying value, leaving a margin of safety of roughly 0.8%. This narrow spread suggests that the market currently views the trust as fairly valued, with limited immediate upside embedded in the share price.

From a growth perspective, the company’s long-term financial trajectory appears relatively stable but not particularly dynamic. Both five-year and ten-year compound annual growth rates for earnings and revenue are reported at 0.0%, indicating that the business has maintained steady operating levels rather than pursuing aggressive expansion strategies. While such stability can be desirable for income investors, it also highlights the importance of disciplined capital allocation and operational efficiency in sustaining shareholder returns.

Forward estimates suggest modest improvement in the company’s top-line performance. Revenue projections point to approximately $103.1 million in 2025, rising to $118.7 million in 2026 and reaching about $125.7 million in 2027. These expectations imply gradual expansion rather than transformative growth, aligning with the broader manufactured housing sector, where industry forecasts anticipate annual growth of around 5% over the coming decade.

For dividend investors, the investment case ultimately hinges on three interconnected pillars: the durability of cash flow generation, the sustainability of the distribution policy, and the valuation at which those income streams can be acquired. Flagship Communities REIT appears to offer reasonable stability in distributions and operating income, but the absence of meaningful growth and the presence of capital efficiency concerns introduce important considerations for long-term shareholders.

Earnings Momentum and Profitability Trends

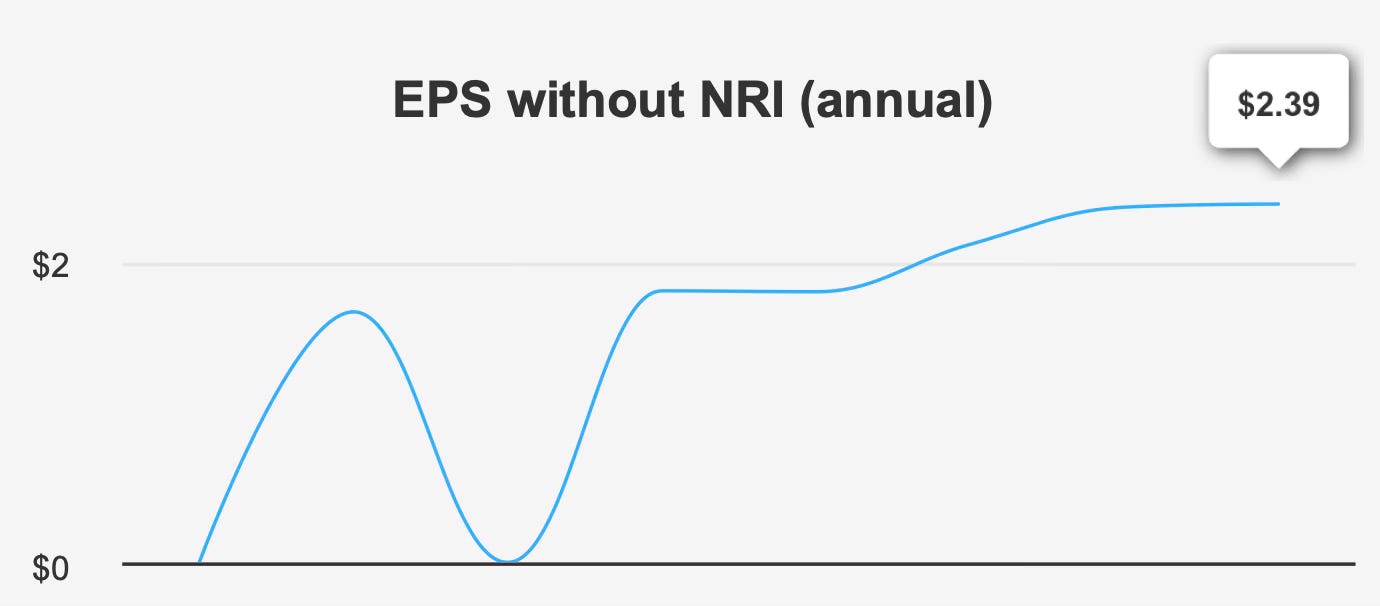

Recent earnings results illustrate a business that remains operationally stable but exhibits moderate quarter-to-quarter volatility. In the most recent reporting period ending September 30, 2025, the company recorded earnings per share excluding non-recurring items of $0.587. This figure represents a decline from $0.723 in the prior quarter, although it improved modestly compared with $0.572 reported during the same quarter of the previous year.

Diluted earnings per share followed a similar pattern, declining to $1.267 from $1.809 in the preceding quarter while still slightly exceeding the $1.226 recorded a year earlier. These movements suggest that quarterly profitability can fluctuate based on operating conditions and potential non-recurring adjustments, yet the broader earnings base remains relatively steady.

Revenue trends provide a clearer indication of incremental operating progress. Revenue per share increased to $1.345 in the most recent quarter, up from $1.292 in the prior period and continuing a steady climb from $1.197 recorded during the same quarter the previous year. The gradual improvement reflects modest growth in rental income and portfolio performance, consistent with the stable demand profile typically associated with manufactured housing communities.

Profitability margins also remain relatively consistent. Gross margin for the latest quarter stood at approximately 65.5%, nearly identical to the five-year median of 65.5%. This level of margin stability indicates that the company has maintained effective cost control within its operating structure despite the broader inflationary pressures that have affected many property operators.

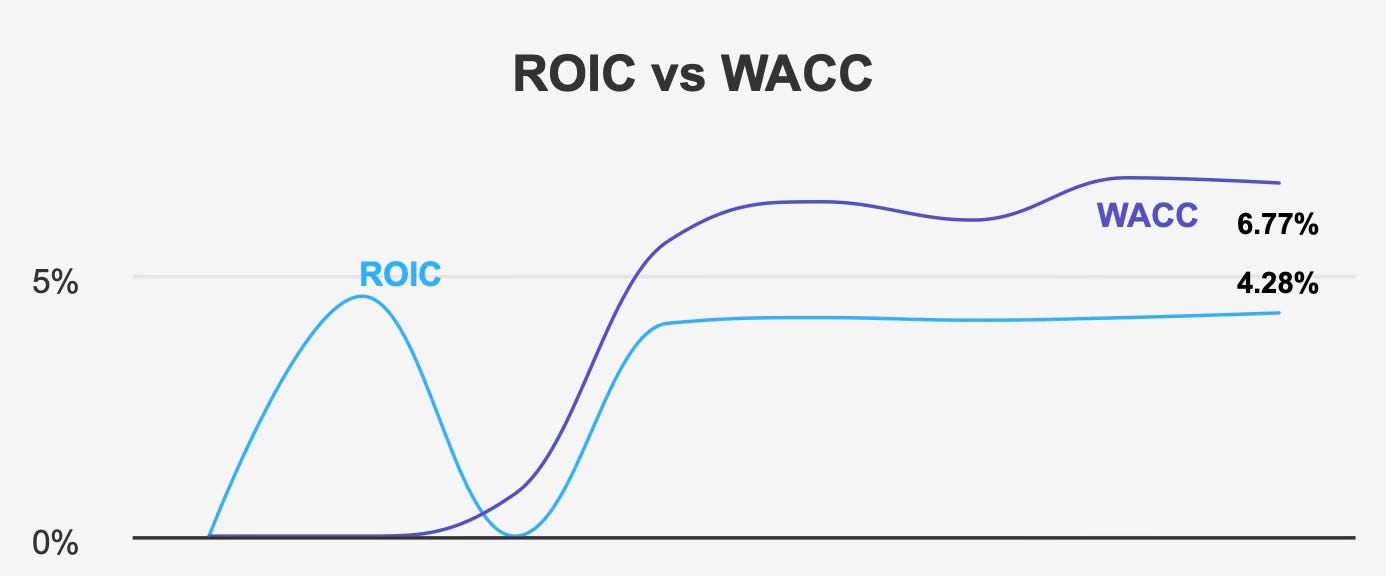

However, a deeper examination of capital efficiency reveals a more nuanced picture. Return on invested capital currently stands at roughly 4.3%, while the company’s weighted average cost of capital is estimated at 6.8%. When the cost of capital exceeds the return generated by invested funds, the result is a structural erosion of economic value.

Over a longer horizon, the pattern remains consistent. The five-year median return on invested capital of about 4.2% remains below the five-year median cost of capital of approximately 6.1%. This persistent gap suggests that the company’s investment decisions or operational efficiency have not yet produced sufficient returns to exceed financing costs.

Interestingly, return on equity tells a somewhat different story. The company currently reports a return on equity of about 15.8%, with a five-year median near 18.3%. Such figures appear relatively strong in isolation but likely reflect the amplifying effect of financial leverage rather than purely operational efficiency.

In practical terms, this dynamic implies that debt financing may be enhancing equity returns while simultaneously reducing overall capital efficiency. For investors, the distinction is important: a high return on equity does not necessarily indicate strong value creation if it is supported by leverage rather than operating productivity.

Overall, Flagship Communities REIT demonstrates consistent operating performance and resilient margins. Yet the long-term challenge lies in improving the relationship between invested capital and economic returns, particularly as the company continues to deploy additional capital into its property portfolio.

Dividend Profile and Sustainability

For many investors, the primary attraction of a real estate investment trust lies in its income distribution policy. Flagship Communities REIT maintains a monthly dividend structure, a feature that provides frequent cash returns and can enhance the appeal of the stock among income-focused shareholders.

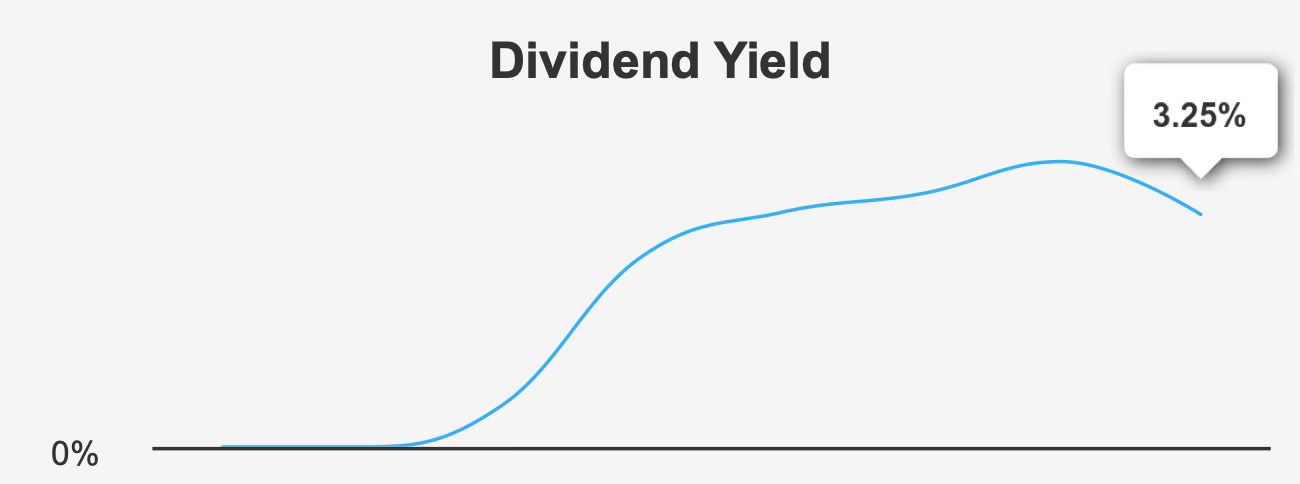

The most recent quarterly dividend per share stands at $0.0545, reflecting a stable distribution level that has been maintained over recent reporting periods. At current market prices, this translates into a forward dividend yield of approximately 3.25%, a figure that sits very close to the company’s ten-year median yield of about 3.39%.

From a historical perspective, dividend growth has been relatively modest. The five-year growth rate remains flat at 0.0%, suggesting that distributions have largely remained unchanged over an extended period. However, the more recent three-year growth rate of about 5.2% indicates that management has begun implementing incremental increases in distributions.

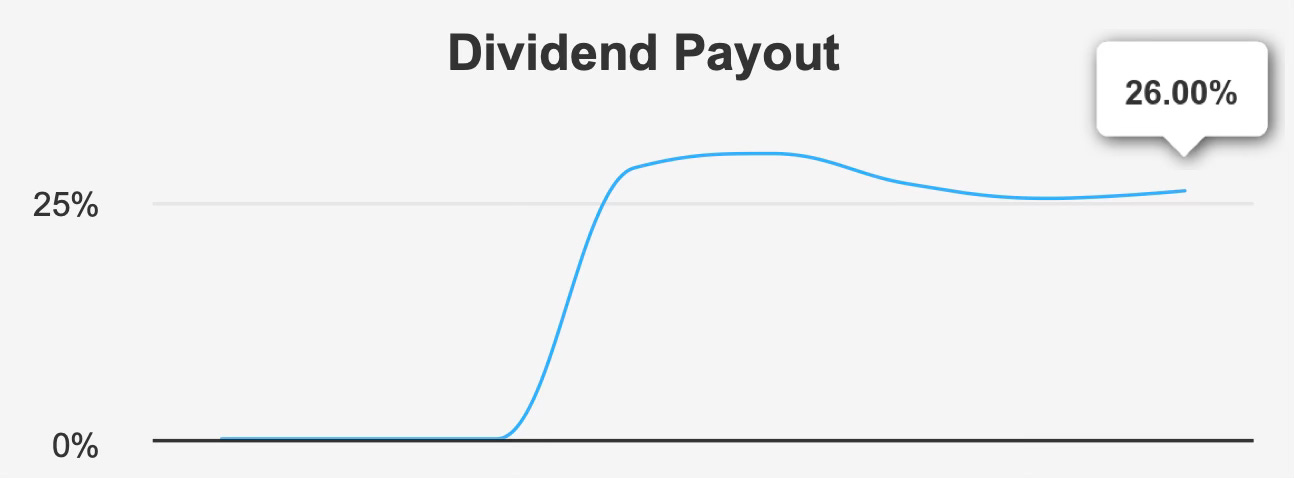

One of the most encouraging aspects of the dividend profile is the company’s relatively conservative payout ratio. Current dividend payments represent approximately 26% of earnings, a level that provides substantial coverage for the distribution. Dividend coverage currently stands at nearly 7.9x earnings, reinforcing the view that the company has significant flexibility to sustain its payments even during periods of earnings volatility.

Looking ahead, projected dividend growth over the next three to five years is estimated at roughly 4.4% annually. While not exceptionally high, such growth would align with the stable, income-oriented strategy typically associated with real estate investment trusts.

The company’s balance sheet metrics also contribute to the assessment of dividend sustainability. Debt-to-EBITDA currently sits at about 3.9x, a level generally considered moderate within the REIT sector. This leverage profile suggests that the company retains adequate financial flexibility while still benefiting from debt financing to support portfolio expansion.

Nevertheless, the broader capital efficiency concerns previously discussed remain relevant when evaluating long-term dividend sustainability. If returns on invested capital continue to trail the company’s cost of capital, future distribution growth could eventually face constraints unless operational improvements materialize.

In the near term, however, the dividend appears secure. Low payout ratios, solid coverage, and consistent operating cash flows collectively support the continuation of the current distribution policy.

Valuation Analysis: Interpreting Market Pricing Relative to Historical Multiples and Asset Value

From a valuation standpoint, Flagship Communities REIT appears to trade close to its estimated fair value. The stock’s intrinsic value is calculated at approximately $19.65, compared with a market price around $19.50. This narrow difference implies that investors are currently paying roughly the fair price for the underlying business.

Examining traditional valuation multiples reinforces this conclusion. The trailing price-to-earnings ratio stands near 4.0x, almost identical to the company’s ten-year median of about 4.0x. Such alignment indicates that the market is valuing the company largely in line with its historical earnings multiple.

Forward expectations suggest higher earnings multiples, with the forward P/E ratio estimated around 14.3x. This increase likely reflects projected changes in earnings dynamics rather than an expansion in market valuation.

Enterprise value metrics provide additional context. The company currently trades at approximately 7.1x EV/EBITDA, slightly below its ten-year median of about 7.6x. This positioning indicates that the stock is valued modestly below historical norms when measured against operating cash flow generation.

Similarly, the price-to-sales ratio sits near 3.8x, closely aligned with its long-term median of 3.8x. Such consistency further supports the notion that the market views the company as a mature, stable operator rather than a high-growth opportunity.

Cash-flow valuation metrics also remain close to historical averages. The price-to-free-cash-flow multiple of approximately 14.6x compares favorably with a ten-year median of roughly 15.1x, suggesting efficient cash flow generation relative to valuation.

One of the more interesting valuation signals appears in the price-to-book ratio, currently around 0.6x. Trading below book value can sometimes indicate that the market is discounting the underlying asset base, particularly in property-focused businesses where tangible assets represent a substantial portion of enterprise value.

However, given the company’s capital efficiency challenges and limited historical growth, the market’s conservative valuation approach may simply reflect realistic expectations for future performance.

Risk Assessment and Capital Structure Considerations

While Flagship Communities REIT demonstrates several characteristics associated with stable income investments, certain financial risks merit careful consideration.

One area of concern relates to the company’s increasing leverage. Over the past three years, the trust has issued approximately $99.3 million in new debt, raising questions about the sustainability of its capital structure over the long term. Although the current leverage ratio remains within a moderate range, continued reliance on debt financing could amplify financial risk if operating conditions deteriorate.

The company’s Altman Z-score of roughly 1.1 places it within the distress zone, a classification that historically indicates an elevated probability of financial stress within the next two years. While such metrics should not be interpreted as deterministic predictions, they nevertheless highlight the importance of prudent balance sheet management.

Capital allocation efficiency represents another critical risk factor. As previously discussed, the persistent gap between return on invested capital and the cost of capital suggests that current investment strategies may not be generating sufficient economic value.

Corporate governance dynamics also warrant attention. Insider ownership currently stands at 0%, meaning company leadership holds no direct equity stake in the business. In some cases, a lack of insider ownership can raise concerns regarding alignment between management incentives and shareholder interests.

Institutional ownership, by contrast, is approximately 23.2%, reflecting moderate participation from professional investors. While this level of institutional involvement can contribute to market stability, it does not necessarily signal strong conviction regarding future growth prospects.

Collectively, these factors suggest that while the company’s operating business remains relatively stable, financial structure and capital allocation decisions will play an important role in determining long-term shareholder outcomes.

Final Assessment

Flagship Communities REIT represents a specialized real estate platform focused on manufactured housing communities, a segment that generally benefits from stable tenant demand and predictable rental income. The company’s operational performance reflects these characteristics, with consistent margins, steady revenue growth, and reliable cash flow generation.

For income investors, the trust offers a reasonably attractive distribution profile. A forward dividend yield of about 3.35%, supported by a conservative payout ratio of roughly 26%, provides a solid foundation for income stability. The monthly dividend schedule further enhances the stock’s appeal for investors seeking regular cash distributions.

However, the broader investment case is balanced by several structural considerations. Long-term growth has remained essentially flat, and capital efficiency metrics indicate that the company has not consistently generated returns above its cost of capital. These factors limit the potential for significant valuation expansion unless operational improvements occur.

Valuation metrics suggest that the stock currently trades close to fair value. With the market price hovering near intrinsic value estimates and most valuation multiples aligned with historical averages, the shares appear neither significantly undervalued nor materially overpriced.

In summary, Flagship Communities REIT offers a stable income profile supported by consistent operating performance and manageable leverage. Yet the combination of modest growth prospects, capital efficiency challenges, and fair valuation suggests that the stock may be best suited for investors prioritizing steady income rather than substantial long-term capital appreciation.