FactSet Research Systems (FDS): A High-Return Data Franchise Trading at a Wide Discount to Intrinsic Value

Strong returns on capital, disciplined payouts, and a wide margin of safety define the opportunity

Investment Thesis: A Capital-Light Analytics Franchise Trading at a Significant Discount to Underlying Value

FactSet Research Systems FDS 0.00%↑ operates at the center of the global investment ecosystem, providing financial data aggregation, portfolio analytics, and workflow solutions to institutional clients. More than 80% of its annual subscription value comes from buy-side clients, including wealth and corporate investors, underscoring the company’s entrenched role in portfolio construction and reporting infrastructure.

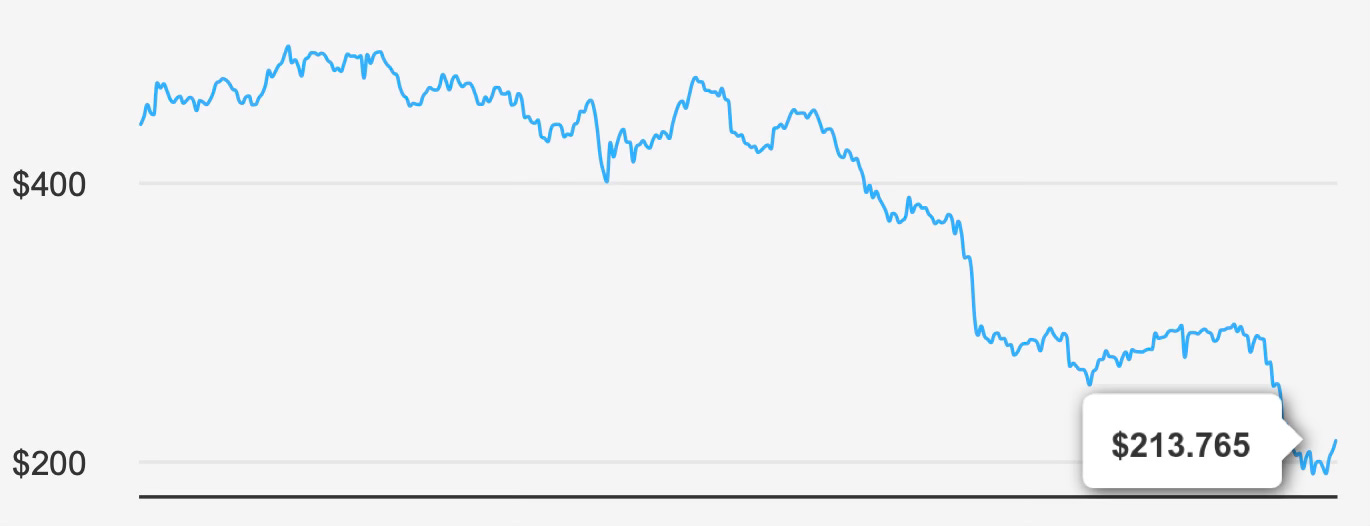

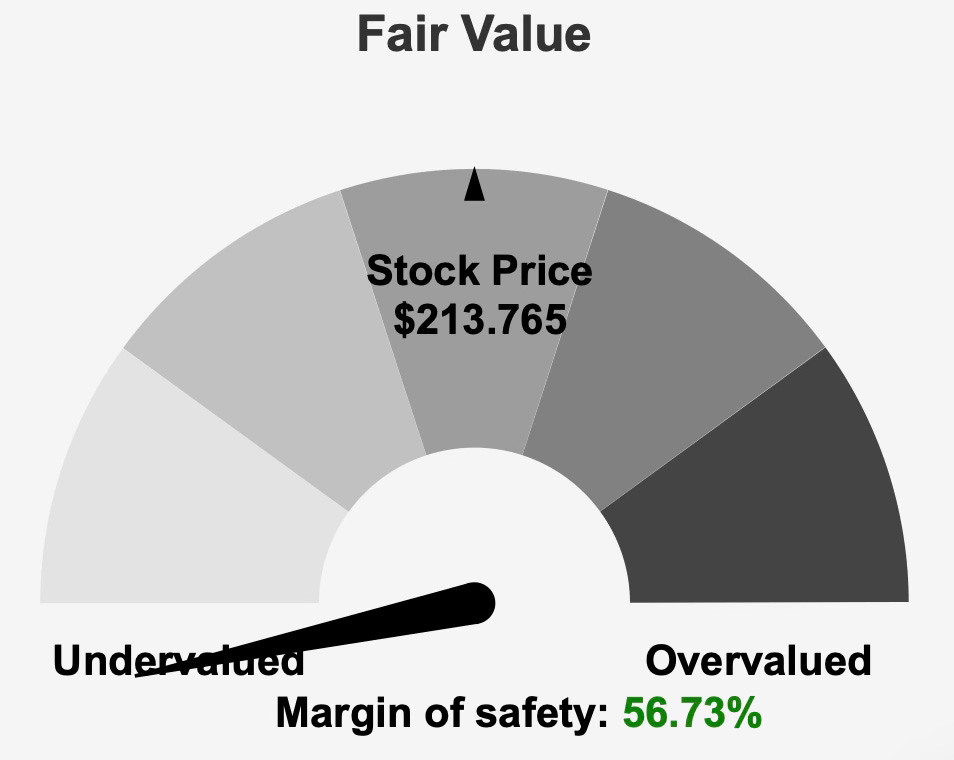

At a current share price of $213 and a market capitalization of $7.93 billion, the stock trades at a substantial discount to its calculated intrinsic value of $494.03. That gap implies a margin of safety of 56.7%, positioning shares in what can reasonably be described as significantly undervalued territory. The valuation dislocation stands out particularly given the company’s consistent revenue growth profile and disciplined capital allocation.

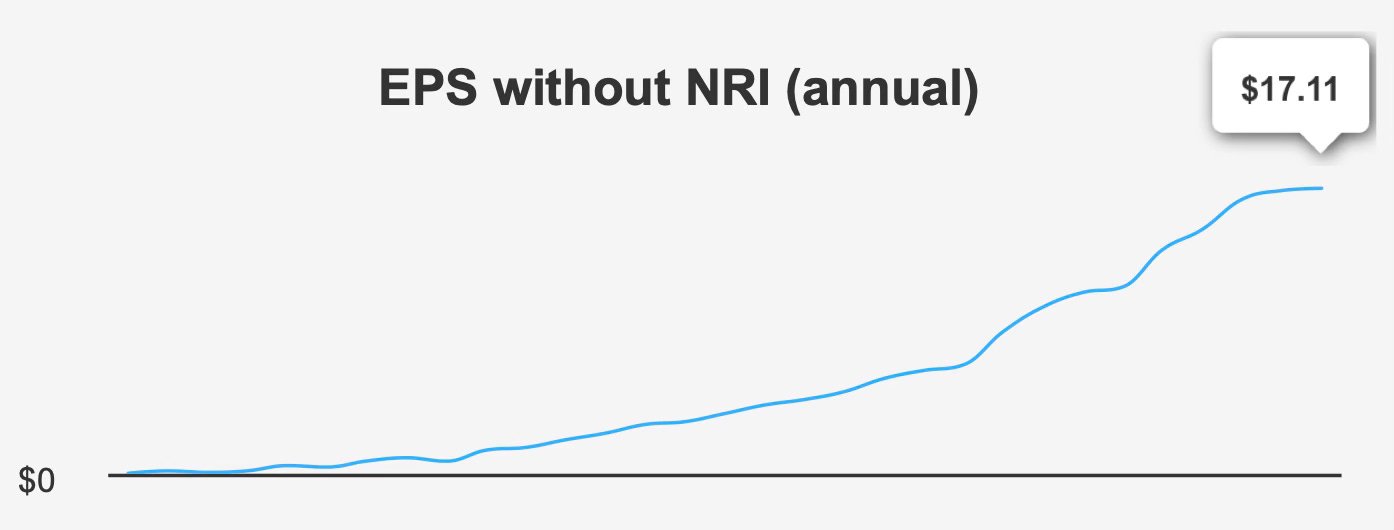

Over the past five years, revenue has compounded at 10.0%, closely aligned with the 10-year growth rate of 9.6%. Earnings have grown even faster, with EPS excluding non-recurring items compounding at 10.4% over five years and 12.3% over a decade. This spread between revenue and earnings growth reflects operating leverage and steady margin management rather than financial engineering.

The business model remains structurally attractive. FactSet aggregates data from exchanges, brokerages, third-party providers, and proprietary sources into a unified platform that is deeply embedded in client workflows. Acquisitions such as Portware in 2015, BISAM in 2017, and CUSIP Global Services in 2022 have expanded execution, risk management, and data capabilities, reinforcing the company’s competitive positioning within capital markets infrastructure.

Against an industry backdrop projected to grow at approximately 8% annually over the next decade, FactSet’s historical 9–10% revenue growth suggests continued share stability or modest share gains. The current valuation appears to discount this durability.

2. Earnings Momentum & Profitability Trends

The most recent quarter, ended November 30, 2025, reflects steady operational progress. EPS excluding non-recurring items reached $4.51, up from $4.05 in the prior quarter and $4.37 in the same quarter last year. The quarter-over-quarter and year-over-year improvement signals continued execution rather than a one-off benefit. Diluted EPS also edged higher to $4.06 from $4.03 sequentially.

Revenue per share rose to $16.154 from $15.638 in the preceding quarter, reinforcing the company’s consistent top-line trajectory. Analysts currently project revenue to reach $2,448.59 million in 2026. Forward EPS expectations stand at $15.367 for fiscal 2026, followed by $17.384 the year after, suggesting continued mid-to-high single-digit earnings expansion.

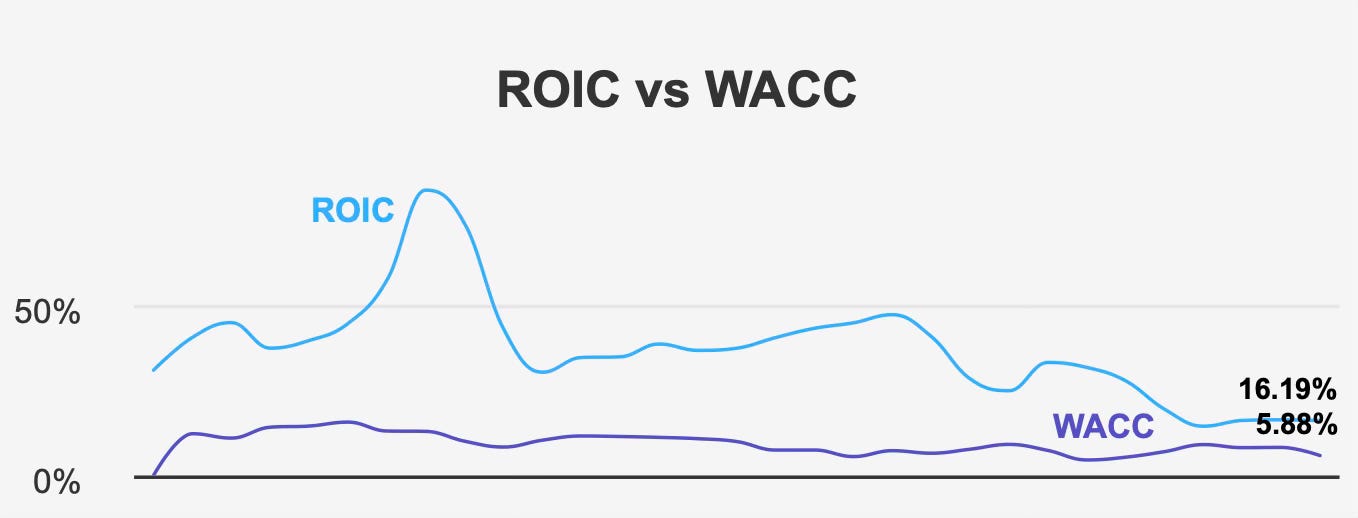

Profitability metrics remain particularly compelling. Over the past five years, median return on invested capital has been 16.5%, comfortably above the median weighted average cost of capital of 8.2%. In the most recent reading, ROIC stands at 16.2% against a WACC of 5.9%. This sustained spread indicates durable economic value creation and disciplined capital deployment.

Gross margin for the latest quarter was 52.3%, only modestly below the five-year median of 52.8%, indicating stability in cost management despite slight fluctuations. Importantly, the company’s Piotroski F-Score of 8 signals strong financial health across profitability, leverage, and operating efficiency metrics, while a Beneish M-Score of -2.52 suggests a low probability of earnings manipulation.

Share repurchases have also contributed incrementally to per-share growth. Over the past year, the company reduced its share count by 2.1%, a notable acceleration compared with 0.4% over three years and 0.1% over five years. While buybacks are not the primary driver of EPS expansion, they enhance per-share compounding when executed at attractive valuations.

Overall, earnings momentum remains steady rather than explosive, but the consistency of execution across cycles supports the investment case.

3. Dividend Profile & Sustainability

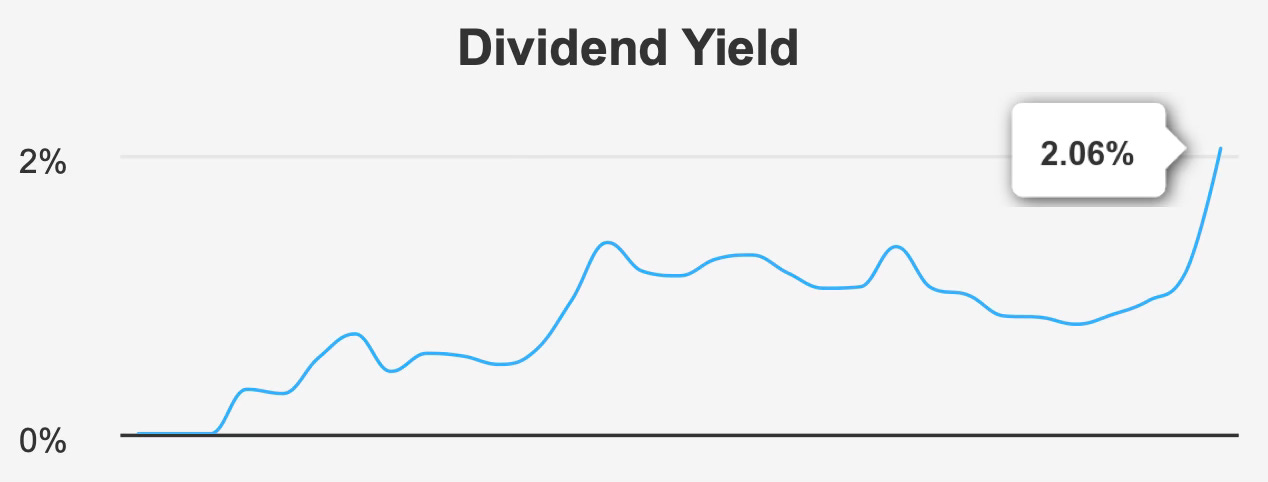

FactSet’s dividend framework reflects both discipline and flexibility. The company currently pays a quarterly dividend of $1.10 per share, translating into a forward yield of 2.1%. While not a high-yield security, the payout is supported by solid coverage and strong capital returns.

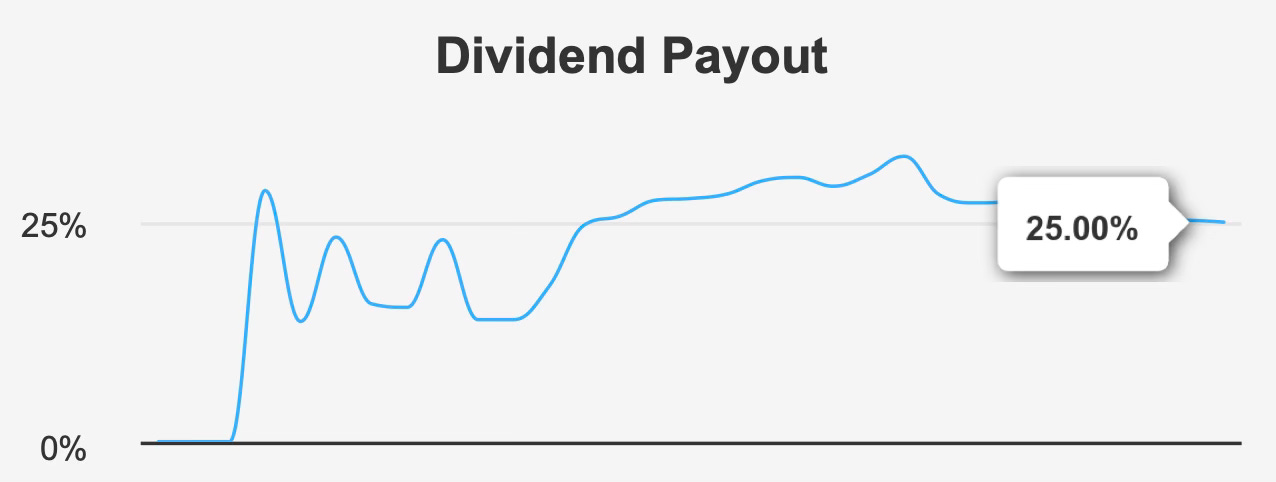

The dividend payout ratio stands at 25.0%, providing substantial room for reinvestment, debt service, and future increases. Dividend coverage is 3.62x, underscoring the sustainability of current distributions. Over both the three- and five-year periods, dividend growth has averaged 7.8%, closely aligned with earnings growth.

Looking forward, estimated dividend growth of 2.3% over the next three to five years implies moderation relative to historical rates. That deceleration may reflect a more balanced capital allocation approach or management’s desire to preserve flexibility amid shifting industry conditions. Even so, the low payout ratio suggests that dividend reductions are unlikely barring a material deterioration in operating performance.

Leverage metrics further reinforce stability. Debt-to-EBITDA stands at 1.59x, comfortably below the 2.0x threshold typically associated with elevated financial risk. The company’s Altman Z-score of 4.29 indicates strong financial stability and low bankruptcy risk.

The next ex-dividend date is February 27, 2026, with payment scheduled for March 19, 2026. For income-focused investors seeking stability rather than aggressive yield, FactSet’s dividend profile aligns with a conservative, growth-oriented strategy.

4. Valuation: Depressed Multiples Relative to History and Intrinsic Value

FactSet’s valuation currently reflects compression across multiple metrics, creating a compelling setup for long-term investors.

The stock trades at 13.6x trailing earnings, near the lower end of its 10-year range. The forward P/E of 12.2x further underscores the discounted forward outlook. On an enterprise basis, EV/EBITDA stands at 9.4x, also close to historical lows.

Revenue-based and asset-based multiples echo this pattern. The trailing price-to-sales ratio of 3.44x sits near its 10-year low of 3.15x. Price-to-book stands at 3.67x, similarly positioned toward the lower end of historical norms. Price-to-free-cash-flow at 12.6x suggests that the market is assigning a modest valuation to the company’s cash generation profile.

This compression is occurring despite continued revenue growth, expanding operating margins, and strong capital returns. The intrinsic value calculation of $494.03 implies more than double the current share price, equating to a 56.7% margin of safety. Even the more conservative analyst price target of $304.91 suggests meaningful upside from current levels, although targets have declined over the past three months.

The stock’s proximity to a five-year low, combined with a dividend yield near a 10-year high, further supports the argument that valuation rather than fundamentals is driving weakness. While multiples alone do not guarantee re-rating, the alignment of discounted valuation with stable performance creates an asymmetrical risk-reward profile.

5. Risk Assessment & Capital Structure Considerations

Despite its strengths, FactSet is not without risk.

Asset growth of 23.9% over five years materially exceeds revenue growth of 10.0% over the same period. That divergence may indicate declining asset efficiency or integration costs associated with acquisitions. Investors should monitor whether incremental assets translate into proportional revenue and earnings gains.

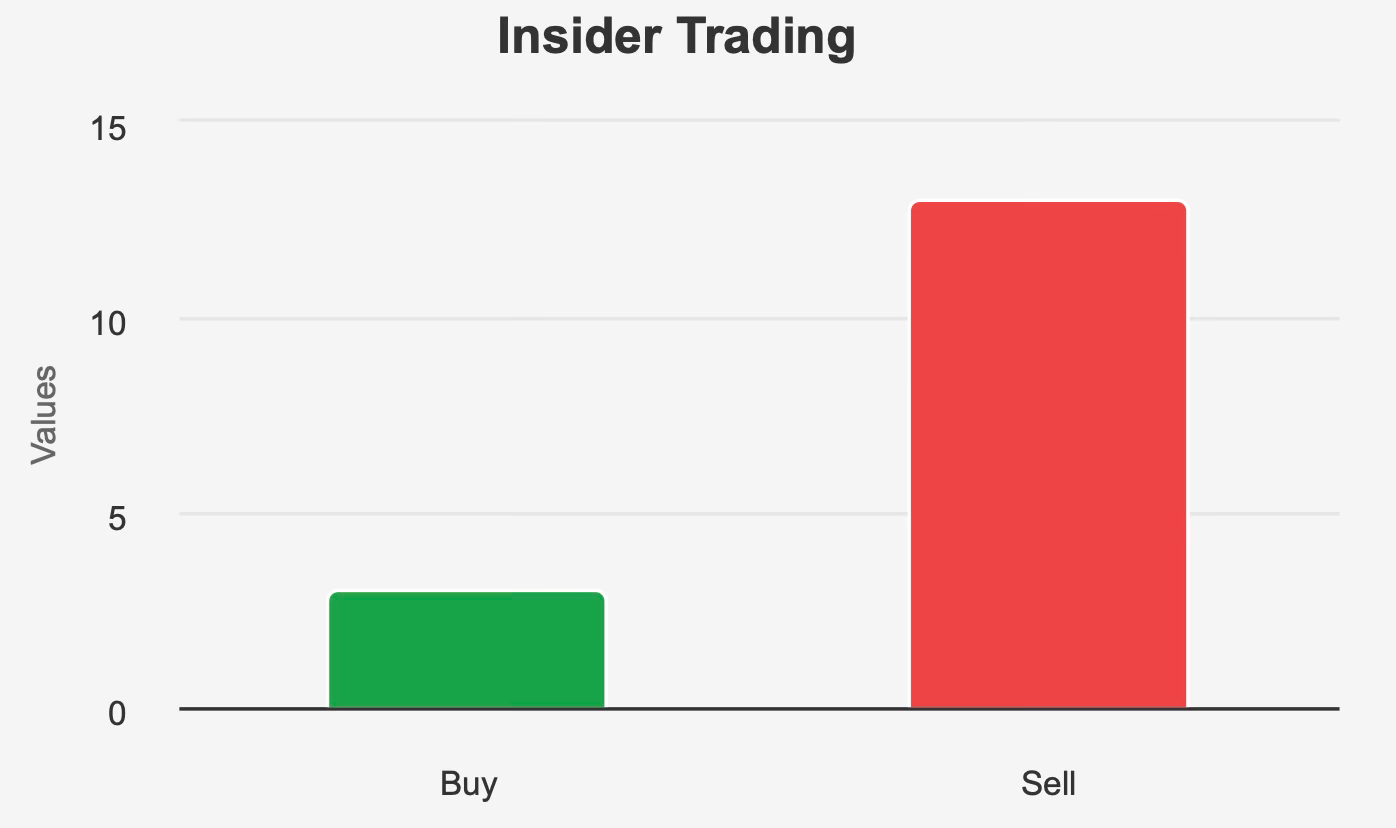

Insider trading patterns warrant attention. Over the past year, insiders executed 13 sales compared with three purchases. In the last three months, no purchases were recorded, with two sales occurring. While insider ownership remains meaningful at 18.2%, the skew toward selling may reflect either valuation considerations or internal caution.

Institutional ownership is exceptionally high at 97.0%, which supports liquidity and reflects broad professional confidence, but also increases the potential for volatility if sentiment shifts.

Trading dynamics also suggest evolving liquidity conditions. Daily trading volume of 242,973 shares is well below the two-month average of 856,420 shares. Meanwhile, a Dark Pool Index of 64.8% indicates that a substantial portion of trading activity occurs off-exchange, potentially affecting price discovery and execution quality.

Government contract revenue grew significantly from 553,970 in 2021 to 1,816,078 in 2025, but a projected decline to 128,742 in 2026 suggests potential expirations or strategic shifts. While government exposure is not the company’s primary revenue driver, such variability underscores the importance of diversified client relationships.

Finally, following a congressional purchase on January 29, 2026, the stock declined 18.3%, underperforming the broader market by a wide margin during that period. This short-term weakness may reflect company-specific concerns or broader capital markets volatility.

Even so, core solvency and profitability indicators remain solid, limiting structural financial risk.

Final Assessment

FactSet Research Systems represents a high-quality, capital-light analytics franchise trading at compressed valuation multiples. Revenue has grown at roughly 10% annually over five years, while earnings have compounded at a slightly faster pace. Returns on invested capital consistently exceed the cost of capital by a wide margin, reflecting disciplined capital allocation.

The dividend profile is conservative, with a 2.1% forward yield supported by a 25.0% payout ratio and manageable leverage of 1.59x debt-to-EBITDA. While dividend growth is projected to moderate, sustainability appears strong.

Valuation is the defining feature of the current opportunity. Trading at 13.6x trailing earnings and 12.2x forward earnings, with EV/EBITDA at 9.4x and price-to-free-cash-flow at 12.6x, the stock sits near historical lows across key metrics. Against an intrinsic value estimate of $494.03 and a margin of safety approaching 57%, the market appears to be discounting stability rather than deterioration.

Risks remain, particularly around asset efficiency, insider selling patterns, and fluctuating government contract exposure. However, balance sheet strength and consistent operating performance mitigate downside concerns.

For long-term dividend-oriented investors seeking a combination of durable growth, capital discipline, and valuation support, FactSet presents a compelling case. The current pricing environment offers an opportunity to acquire a consistently profitable financial data franchise at a multiple that implies limited growth, despite evidence to the contrary.