Extendicare Inc.: Solid Operations but Limited Dividend Appeal at Current Prices

Operational efficiency and demographic tailwinds remain compelling, though investors face a narrow margin of safety.

Investment Thesis: A Demographically Supported Healthcare Operator With Strong Capital Efficiency but Elevated Market Expectations

Extendicare Inc. operates within Canada’s senior care sector, providing long-term care, home healthcare services, and managed services to healthcare providers. The company’s core business is concentrated in long-term care facilities, which generate the majority of revenue, complemented by home healthcare operations under the ParaMed brand and consulting and purchasing services through its managed services division. This diversified service model allows the company to participate across multiple segments of the senior care ecosystem while maintaining a stable base of government-supported demand.

The broader industry backdrop remains supportive. Long-term demographic trends, including population aging and rising demand for assisted living and home healthcare services, create structural growth opportunities. The industry is projected to expand at roughly 6% annually over the coming decade, providing a favorable environment for operators with established infrastructure and regulatory relationships.

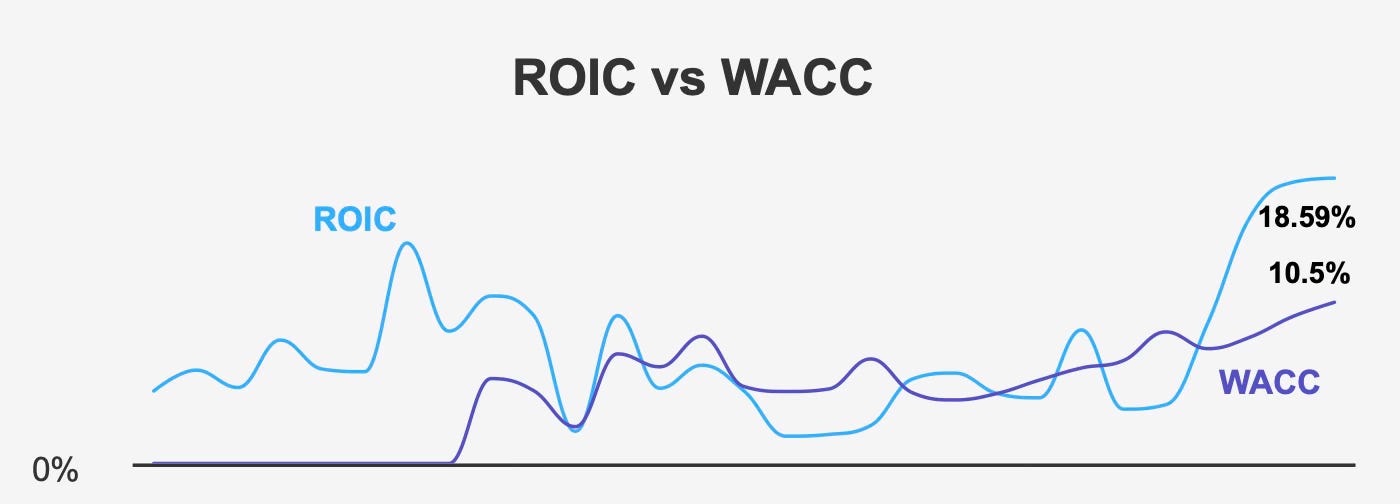

From a capital efficiency perspective, Extendicare’s financial profile appears strong. The company recently generated a return on invested capital of approximately 18.5%, significantly exceeding its weighted average cost of capital of about 10.5%. This spread suggests the company is creating meaningful economic value by deploying capital into operations that produce returns well above its financing costs. Over the past five years, the firm has maintained a median return on invested capital of roughly 9.1%, still comfortably above its historical cost of capital.

Profitability metrics also demonstrate strong equity efficiency. Return on equity currently stands at roughly 51.6%, with a five-year median near 38.8%. Such figures indicate that management has been effective in leveraging shareholder capital to generate earnings growth and operational returns.

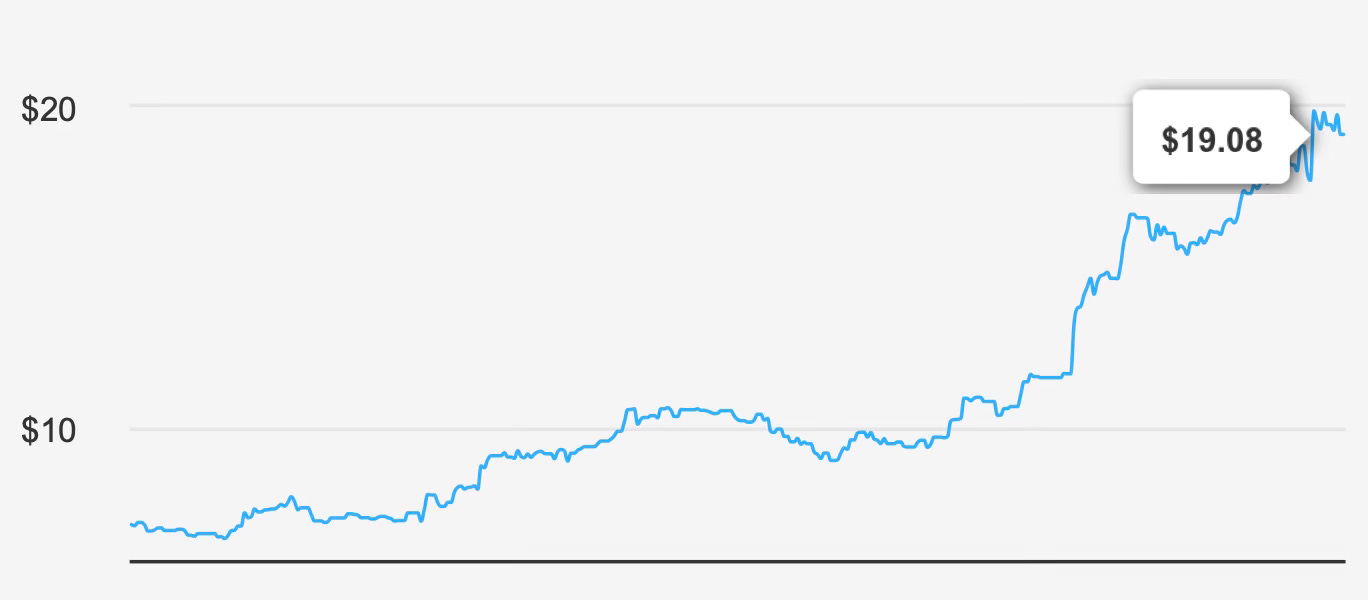

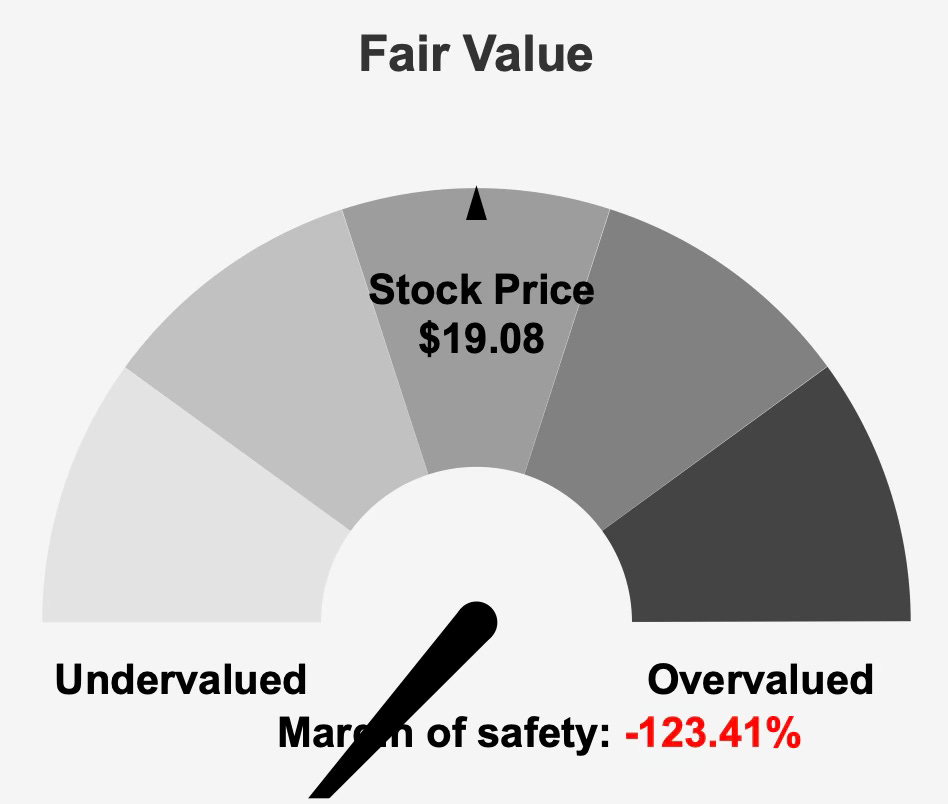

Despite these positive operational indicators, the current market valuation raises concerns. With the stock trading around $19 while intrinsic value estimates suggest approximately $8.54, the implied margin of safety is deeply negative. This disconnect between operational quality and valuation forms the central tension in the investment case. While the company operates in a structurally attractive industry and demonstrates strong capital efficiency, the market price already reflects a substantial premium to fundamental value.

For dividend-focused investors, this dynamic creates a nuanced investment picture. The underlying business appears stable and profitable, but the current valuation may limit both yield attractiveness and long-term capital appreciation.

Earnings Momentum and Profitability Trends Reflect Improving Operational Performance

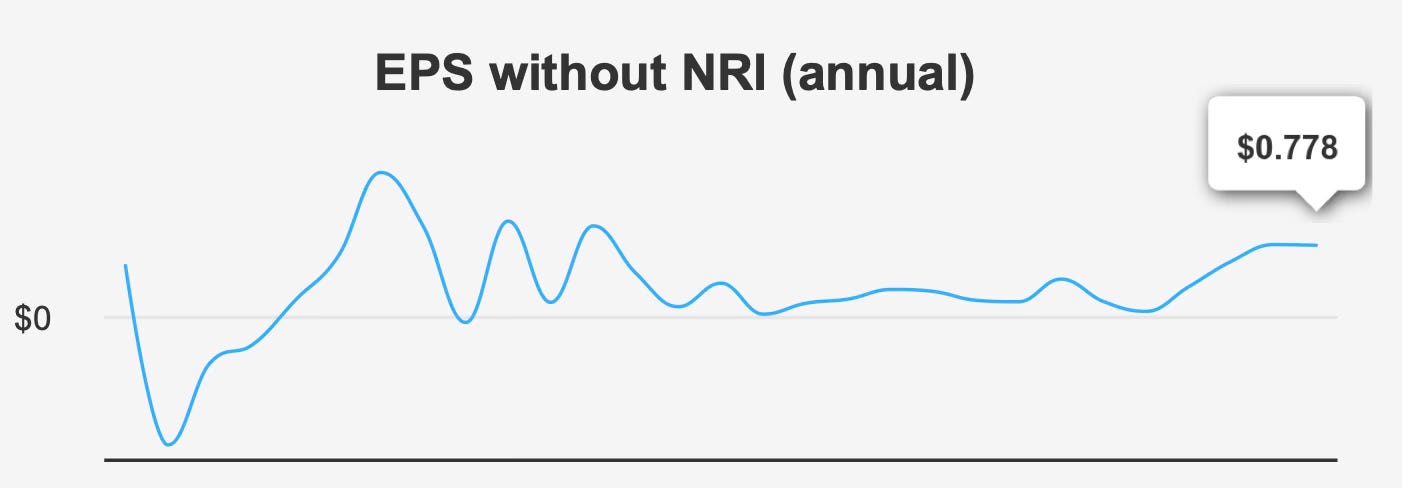

Recent financial results highlight a clear improvement in Extendicare’s earnings trajectory. In the fourth quarter of 2025, the company reported earnings per share excluding non-recurring items of $0.225. This represented a sequential increase of roughly 4.7% compared with the previous quarter and a notable year-over-year gain of approximately 33%.

Diluted earnings per share followed a similar trajectory, rising to $0.206 compared with $0.203 in the prior quarter and $0.161 in the same period the previous year. These improvements suggest that operational execution has strengthened over the past year, supported by stable demand and improving service utilization.

Revenue performance also demonstrated steady progress. Revenue per share increased slightly to $3.715 from $3.708 in the prior quarter, while rising significantly from $2.333 a year earlier. The year-over-year increase indicates that the company is expanding its revenue base while maintaining consistent per-share performance.

Over longer time horizons, earnings growth has been particularly impressive. Earnings per share excluding non-recurring items have compounded at approximately 34.2% annually over the past five years, reflecting strong operational momentum. Over a ten-year period, the compound growth rate moderates to around 8.1%, suggesting that recent performance represents an acceleration compared with the company’s longer-term earnings trajectory.

Looking ahead, analysts expect continued expansion. Revenue projections indicate the potential for total revenue to reach roughly $1.58 billion by 2026. Earnings forecasts estimate approximately $0.811 per share in the next fiscal year, rising further to about $0.988 in the following year.

While these projections suggest continued growth, certain structural limitations remain visible within the operating model. Notably, gross margin has remained effectively flat at around 0% for an extended period. This reflects the highly regulated nature of the long-term care industry, where pricing power is often constrained by government reimbursement frameworks and cost structures remain relatively rigid.

Nevertheless, the company has managed to offset these limitations through operational scale, service diversification, and capital allocation discipline. Even within a constrained pricing environment, Extendicare has demonstrated the ability to generate strong returns on capital and consistent earnings growth.

Taken together, the earnings profile presents a company benefiting from demographic tailwinds and operational efficiency improvements, although long-term margin expansion may remain limited by industry structure.

Dividend Profile and Sustainability: Stable Payments Supported by Conservative Payout Levels

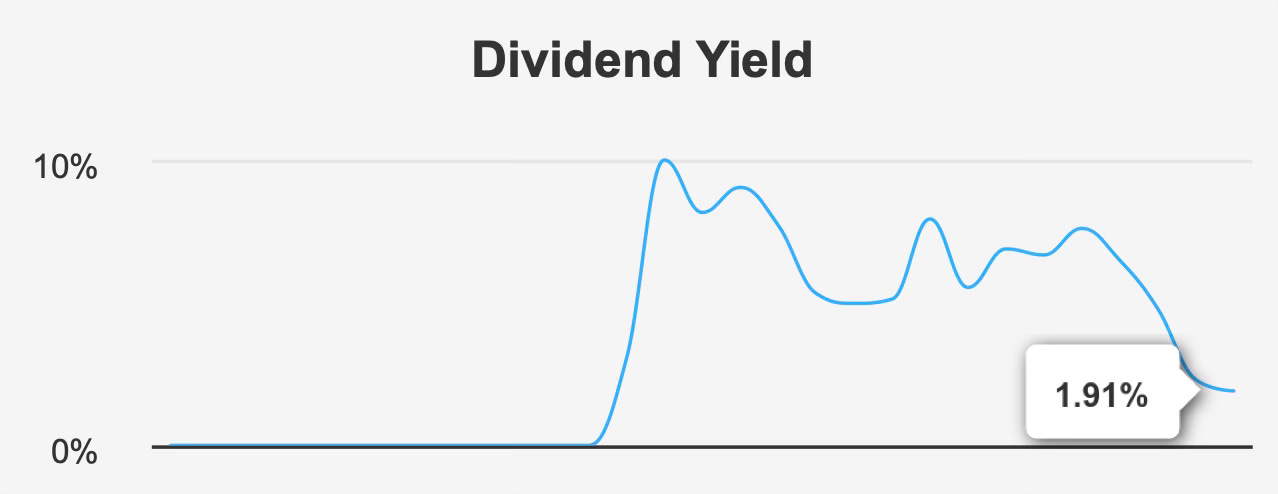

Extendicare maintains a modest but stable dividend program designed to provide consistent income to shareholders. The company currently offers a forward dividend yield of approximately 1.9%, positioning the stock at the lower end of its historical yield range. Over the past decade, the dividend yield has reached a median level of roughly 6.1%, with historical lows near 1.9%.

The relatively subdued yield at present largely reflects the stock’s elevated share price rather than a decline in dividend payments.

Dividend growth itself has been relatively modest in recent years. The three-year dividend growth rate stands at about 1.4%, suggesting that management has prioritized stability over aggressive increases. More broadly, the company’s five-year dividend growth rate remains subdued at approximately 0.6%.

Despite this slow growth, the dividend appears well supported by underlying earnings. The payout ratio currently sits near 46%, leaving a comfortable buffer between dividend payments and earnings generation. Dividend coverage is also strong, with earnings covering the dividend approximately 2.2 times.

Such a coverage profile indicates that the dividend remains sustainable even in periods of earnings volatility. The relatively conservative payout ratio also provides management with flexibility to increase dividends gradually if earnings continue to expand.

Debt levels further reinforce the dividend’s stability. The company’s debt-to-EBITDA ratio stands around 1.77, remaining below the commonly referenced 2.0 threshold associated with moderate financial leverage. This indicates that Extendicare maintains manageable debt obligations relative to operating earnings, reducing the risk that dividend payments would need to be curtailed to service debt.

Dividend payments occur monthly, providing consistent income for investors seeking regular cash flow. The most recent quarterly dividend payment was maintained at CAD 0.042 per share, reflecting management’s preference for predictable distributions rather than frequent adjustments.

Looking forward, dividend growth could accelerate if projected earnings materialize. Forecasts suggest potential dividend growth of roughly 39% over the next three to five years, reflecting expectations for continued earnings expansion.

While the yield itself remains modest, the combination of stable cash flows, conservative payout levels, and manageable leverage suggests that Extendicare’s dividend is secure under current operating conditions.

Valuation Analysis and Market Pricing Relative to Fundamental Value

Valuation currently represents the most significant challenge in the investment case for Extendicare. The company’s estimated intrinsic value sits near $8.54 per share, while the stock trades around $19. This difference implies a negative margin of safety exceeding 120%, indicating that the market price substantially exceeds fundamental value estimates.

Traditional valuation multiples reinforce this conclusion.

The stock currently trades at approximately 23.7x trailing earnings, with a forward price-to-earnings ratio near 22.6x. Both figures sit above the company’s ten-year median multiple of roughly 18.7x. Such a premium suggests that investors are assigning a higher valuation to future earnings than historical norms would typically justify.

Enterprise valuation metrics present a similar picture. The company’s trailing EV/EBITDA multiple stands near 13.7x, modestly above the ten-year median of about 12.3x. While the difference is not extreme, it still indicates that the market currently prices the company at a premium relative to its historical operating earnings.

Revenue-based valuation ratios highlight an even more pronounced shift. The price-to-sales ratio currently stands near 1.35x, roughly double the ten-year median of about 0.68x. This suggests that investors are valuing each dollar of revenue significantly higher than they have historically.

The price-to-book ratio shows a similar pattern. At approximately 6.5x book value, the stock trades above its historical median of around 5.8x, indicating that the market is placing a higher premium on the company’s equity base.

Free cash flow valuation also points toward elevated expectations. The price-to-free-cash-flow ratio currently stands around 21.4x, exceeding the ten-year median of approximately 19.0x.

Taken collectively, these metrics suggest that Extendicare is trading at a consistent premium across multiple valuation frameworks. While the company’s operational performance has improved in recent years, the current valuation already reflects substantial optimism regarding future growth.

For income-focused investors, the valuation premium also compresses the dividend yield, reducing the stock’s attractiveness relative to alternative dividend opportunities.

Unless future earnings growth significantly exceeds expectations, valuation normalization could present a headwind for long-term shareholder returns.

Risk Assessment and Capital Structure Considerations

Several risk factors accompany Extendicare’s current valuation and operating profile.

First, valuation compression remains a primary concern. The stock’s price-to-earnings ratio is currently near a two-year high, while the price-to-sales ratio approaches a ten-year high. With the share price also trading near its long-term peak, the potential for further multiple expansion appears limited.

At the same time, the dividend yield sits close to its ten-year low, reducing the income cushion that might otherwise offset valuation risk for long-term investors.

Liquidity conditions represent another potential consideration. The stock’s recent daily trading volume has been significantly lower than its two-month average, suggesting that market liquidity may fluctuate. For larger investors, limited liquidity could increase the risk of price volatility when executing sizable trades.

Corporate governance factors also warrant attention. Insider ownership currently stands at 0%, and no insider buying or selling activity has been reported over the past year. While the absence of selling could suggest management confidence, the lack of ownership may raise questions about alignment between management and shareholder interests.

Despite these concerns, several indicators highlight financial stability. The company maintains a Piotroski F-Score of 7, suggesting strong operational quality and improving financial metrics. A Beneish M-Score of roughly −2.78 indicates a low probability of earnings manipulation, reinforcing confidence in the integrity of reported financial results.

Balance sheet stability also appears solid. An Altman Z-Score near 3.9 suggests a low probability of financial distress, indicating that the company’s capital structure remains healthy.

Overall, while valuation risks are meaningful, the company’s financial foundation remains stable, supported by manageable leverage and solid operational performance.

Final Assessment

Extendicare represents a stable healthcare operator benefiting from long-term demographic trends and consistent demand for senior care services. The company has demonstrated strong capital efficiency, with returns on invested capital comfortably exceeding its cost of capital and earnings growth accelerating in recent years.

Dividend payments appear sustainable, supported by conservative payout levels, manageable leverage, and consistent operating cash flow. Monthly dividend distributions may also appeal to income-oriented investors seeking regular cash flow.

However, valuation remains the defining challenge. With the stock trading significantly above intrinsic value estimates and at a premium to historical multiples, the current price already reflects considerable optimism regarding future growth.

As a result, while the underlying business appears financially sound and operationally effective, the investment opportunity for new dividend investors may be limited at present price levels.

For long-term investors focused on income and capital preservation, Extendicare may be worth monitoring for potential entry opportunities should valuation levels become more attractive in the future.