EPR Properties: Income Stability Within a Specialized Real Estate Portfolio

Evaluating whether EPR’s specialized property portfolio supports long-term dividend reliability.

Investment Thesis: Income Appeal Supported by Experiential Real Estate Exposure but Limited by Valuation Premium

EPR Properties EPR 0.00%↑ operates as a specialized real estate investment trust focused primarily on experiential real estate assets. The company invests in properties that facilitate entertainment, recreation, and education activities, including theaters, family entertainment centers, ski resorts, and private education facilities. This focus differentiates EPR from traditional REITs that emphasize office, retail, or residential assets. Instead, the portfolio is tied to consumer experiences and destination-based properties that tend to generate stable tenant demand when economic conditions are supportive.

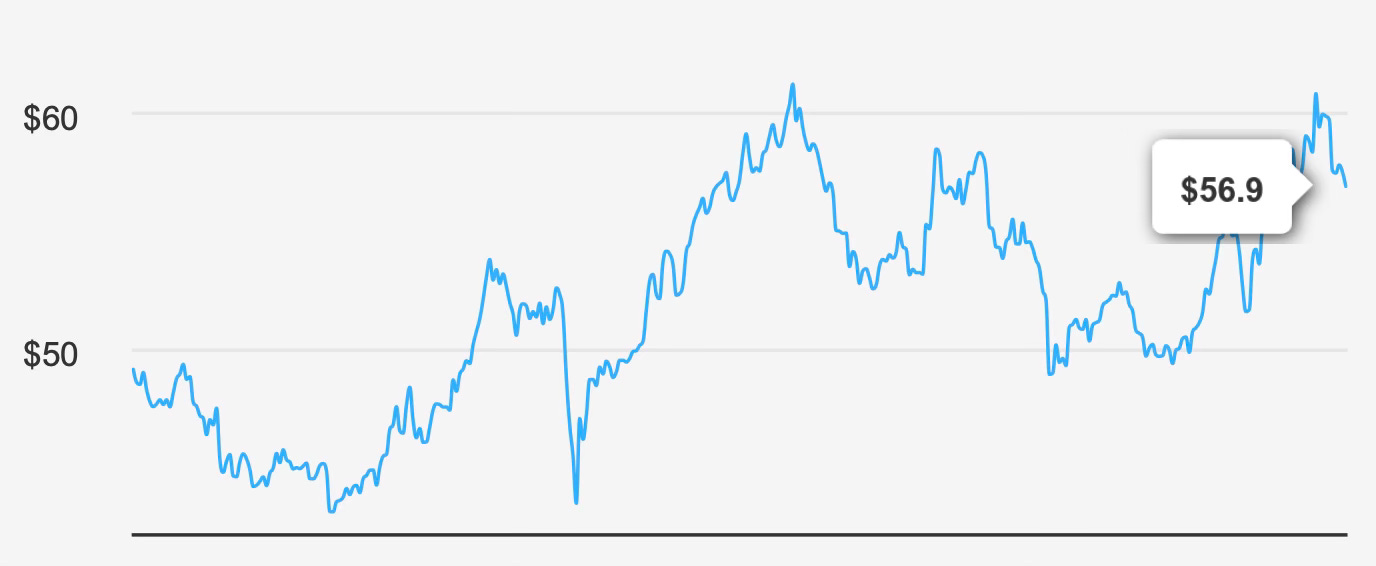

At present, the company commands a market capitalization of approximately $4.35 billion and trades near $56 per share. The stock offers a forward dividend yield of roughly 6.3%, positioning it among the higher-yielding REITs in the public market. For income-focused investors, that level of yield is immediately attractive, particularly when supported by relatively stable real estate cash flows and long-term lease structures.

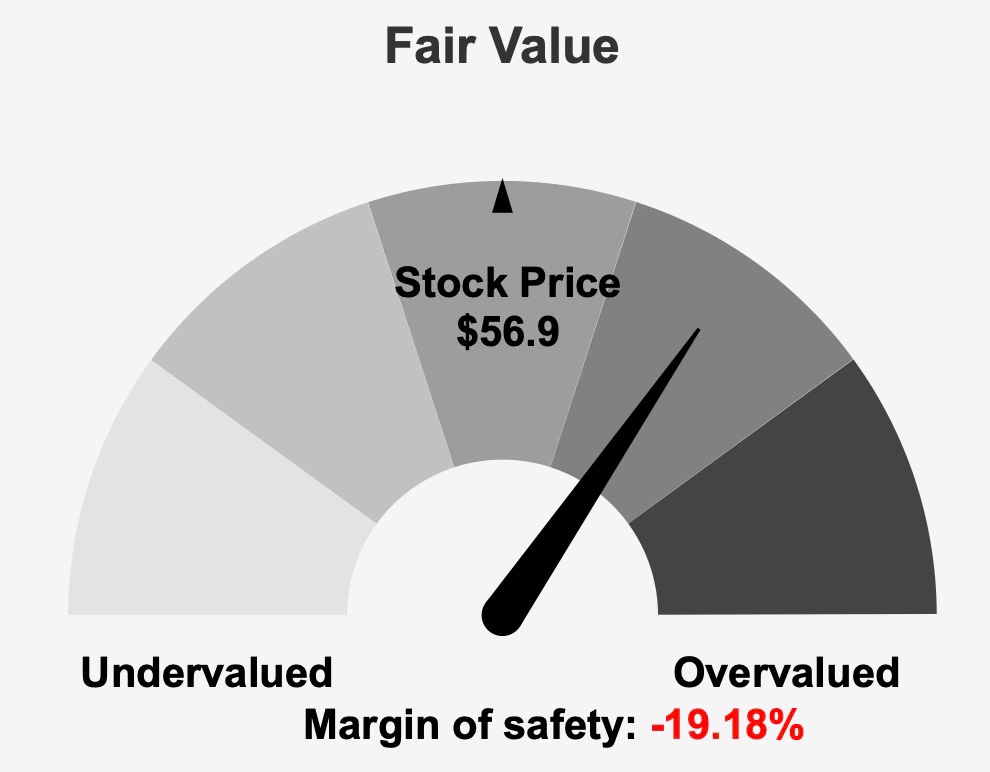

However, valuation currently presents a constraint on the investment case. Internal valuation estimates place intrinsic value near $47.74 per share, implying a negative margin of safety of approximately 19.2% relative to the current market price. In other words, investors purchasing the shares today are paying a premium to estimated fair value.

This does not necessarily negate the investment appeal, but it alters the risk-reward profile. Rather than representing a deeply discounted income opportunity, EPR appears more appropriately classified as a hold-oriented income vehicle. The company’s underlying property portfolio and cash-flow characteristics support continued dividend payments, yet the absence of a valuation discount reduces the margin for error.

Growth trends further reinforce this balanced outlook. Over the past five years, the company achieved dividend growth of 21.1%, reflecting recovery from earlier disruptions and renewed operational momentum. More recent trends, however, suggest that growth is moderating. Dividend increases over the past three years averaged just 2.7%, and forward expectations point to approximately 2.4% annual growth.

Taken together, these factors produce a nuanced investment picture. EPR offers an appealing yield and a specialized property portfolio that generates stable rental income, yet the shares currently trade above intrinsic value while dividend growth has slowed meaningfully. For long-term income investors, the stock may still serve as a portfolio stabilizer, though near-term upside appears limited unless earnings growth accelerates or valuation multiples compress.

Earnings Momentum & Profitability Trends

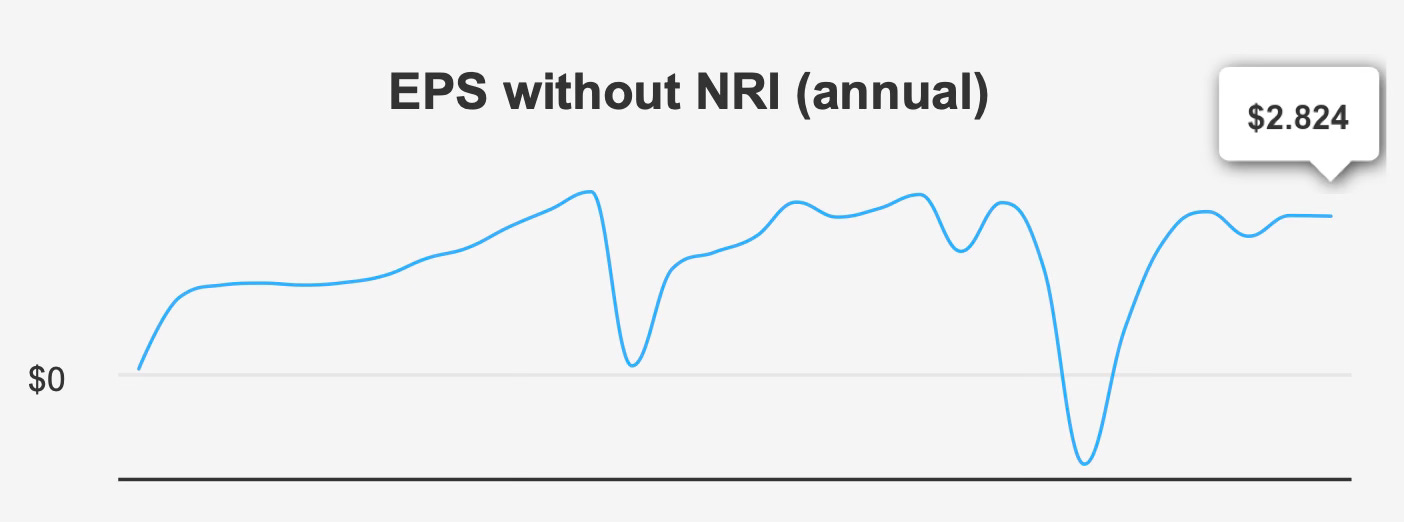

Recent earnings results demonstrate that EPR has made meaningful progress in stabilizing profitability following earlier periods of volatility. The company reported fourth-quarter 2025 earnings excluding non-recurring items of $0.752 per share, representing a clear improvement from $0.706 in the third quarter of 2025 and a substantial increase compared with $0.395 reported in the fourth quarter of 2024.

This progression suggests that operational performance continues to strengthen as experiential properties regain momentum and tenant activity normalizes. The improvement in adjusted earnings highlights the underlying stability of the company’s property portfolio and the recovery trajectory that has taken shape over the past year.

Reported diluted earnings per share also illustrate this trend. Fourth-quarter diluted EPS held steady at $0.79 compared with the previous quarter, while representing a dramatic turnaround from a negative $0.19 recorded in the same period one year earlier. Such a shift underscores how quickly profitability has improved as property utilization and tenant operations stabilize.

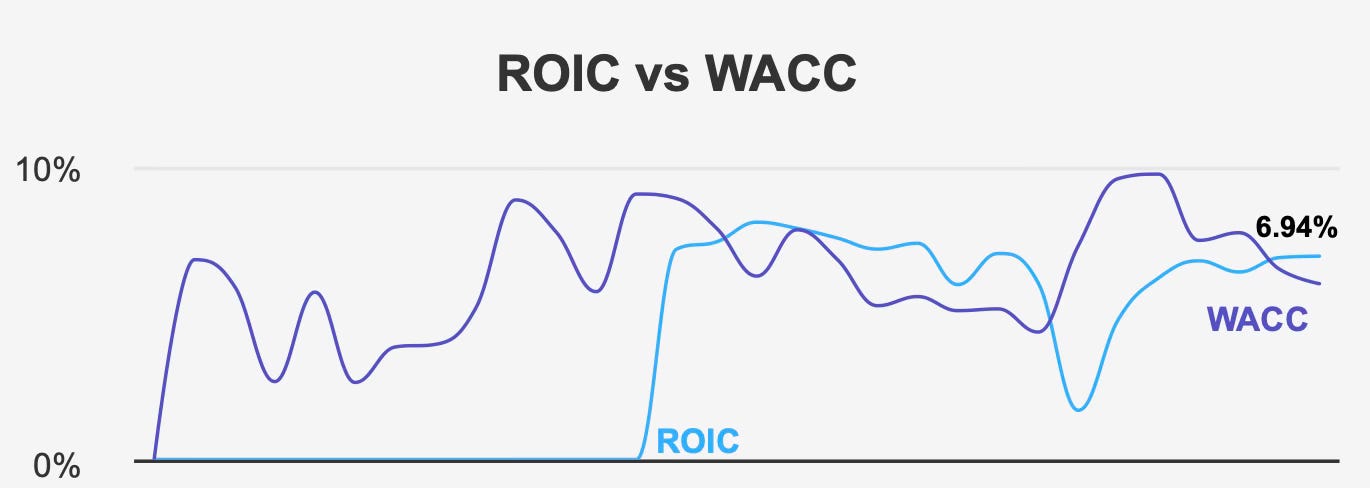

Beyond earnings growth, capital efficiency metrics provide further insight into how effectively management deploys capital. EPR currently generates a return on invested capital of 6.94%, modestly exceeding its weighted average cost of capital of 6.0%. When a company’s ROIC surpasses its cost of capital, it indicates that investments are producing economic value rather than merely covering financing costs.

The spread between these two figures is not especially large, but it remains meaningful. Even a modest margin above the cost of capital suggests that new investments are contributing incremental value to shareholders.

Looking at historical performance provides additional context. Over the past decade, EPR has produced a median ROIC of approximately 6.3%. This level is closely aligned with the company’s long-term median WACC of about 6.9%, suggesting that capital allocation has generally been balanced over time.

Historical extremes further highlight the company’s operating range. The highest ROIC achieved during the past decade reached 7.38%, while the lowest fell to roughly 1.68%. Such variation reflects the cyclical pressures that can influence experiential real estate assets, particularly during periods of economic disruption or reduced consumer spending.

Shareholder return metrics also illustrate a strengthening financial profile. Return on equity currently stands at 11.82%, representing a meaningful improvement from the decade low of negative 4.67%. The recovery in ROE aligns with the broader improvement in earnings and indicates that equity capital is again generating solid returns.

Overall, profitability metrics suggest that EPR has regained operational stability while maintaining capital efficiency near historical norms. Earnings growth in recent quarters reinforces the recovery narrative, though the relatively narrow spread between ROIC and WACC implies that the company is creating value at a steady but measured pace rather than delivering exceptional returns.

Dividend Profile & Sustainability

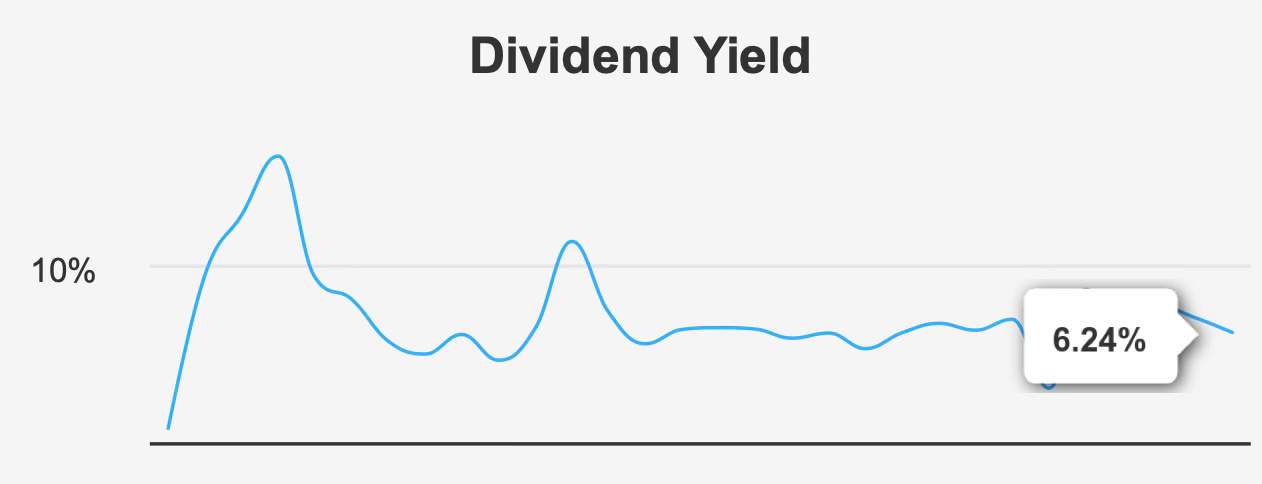

For many investors, the primary attraction of EPR Properties lies in its dividend. With a forward yield of approximately 6.2%, the company offers a level of income that stands well above the broader equity market and compares favorably with many REIT peers.

The strength of this dividend profile is rooted in the company’s underlying real estate model. Experiential properties typically operate under long-term lease structures that generate predictable rental income streams. This type of contractual cash flow can support stable distributions even when broader economic conditions fluctuate.

Historical dividend growth further illustrates the company’s ability to reward shareholders during periods of operational recovery. Over the past five years, the dividend expanded at an impressive annual rate of roughly 21.1%. Such rapid growth largely reflects the normalization of operations following earlier disruptions that temporarily pressured real estate cash flows.

More recent growth trends, however, reveal a clear moderation. Over the past three years, dividend growth has slowed to approximately 2.7% annually. Forward expectations suggest an even more measured pace of around 2.4%.

This shift does not necessarily signal weakness. Rather, it reflects the transition from recovery-driven expansion toward a steadier, mature growth phase. As the company’s property portfolio stabilizes and earnings growth normalizes, dividend increases are likely to track more closely with underlying cash-flow growth.

In practical terms, this means investors should expect the dividend to remain reliable but not rapidly expanding. A 6.2% yield combined with roughly 2–3% annual growth still produces a respectable income profile for long-term investors, particularly those seeking steady distributions rather than aggressive dividend growth.

Upcoming dividend dates further reinforce the company’s commitment to shareholder distributions. The next ex-dividend date is scheduled for March 31, 2026, with a payout date of March 16, 2026.

Ultimately, the sustainability of EPR’s dividend appears closely tied to the stability of its experiential property portfolio. As long as tenant demand remains steady and occupancy levels hold, the company should be able to maintain its current distribution structure. While dividend growth may remain modest in the near term, the overall income stream remains supported by predictable real estate cash flows.

Valuation Perspective: Comparing Intrinsic Value, Market Pricing, and Historical Multiples

Current valuation metrics suggest that EPR Properties trades at a modest premium relative to intrinsic value estimates, even though some market multiples appear reasonable when compared with historical norms.

The company’s intrinsic value is estimated at approximately $47.74 per share, while the market price currently sits near $56. This difference implies a negative margin of safety of roughly 19.2%. In valuation terms, that gap indicates that the market is assigning a premium to the company’s shares relative to modeled fair value.

From a multiples perspective, the picture is somewhat more balanced. The trailing twelve-month price-to-earnings ratio stands at about 17.4x, which is notably below the company’s 10-year median of 22.5x. Although this suggests the shares are not historically expensive on an earnings basis, the current multiple also remains well above the historical trough of 7.8x.

Forward valuation metrics show a slightly higher earnings multiple of roughly 18.6x. This modest increase reflects expectations that earnings growth will continue, albeit gradually, in the coming periods.

Other valuation measures reinforce the impression of moderate pricing rather than deep undervaluation. The trailing price-to-sales ratio currently sits near 6.47x, somewhat below the long-term median of 7.28x. This comparison suggests that revenue is being valued somewhat conservatively relative to historical levels.

Enterprise valuation metrics tell a similar story. The company’s EV/EBITDA ratio stands near 12.9x, compared with a 10-year median of approximately 15.9x. While this indicates that operating earnings are not being priced at extreme levels, the multiple remains above the historical low of roughly 9.2x.

Book value comparisons present a slightly different perspective. The current price-to-book ratio of around 1.86x sits above the historical median of approximately 1.53x. This suggests that the market is assigning a somewhat richer valuation to the company’s net asset base.

Taken together, these metrics paint a nuanced picture. EPR is not trading at the elevated multiples seen during peak valuation periods, yet it also lacks the deep discount that typically attracts value-oriented investors. The premium relative to intrinsic value reinforces this conclusion.

For investors evaluating entry points, the current valuation implies that much of the company’s recovery and stability is already reflected in the share price. Future returns may therefore depend more heavily on dividend income and incremental earnings growth rather than significant multiple expansion.

Risk Assessment & Capital Structure Considerations

Despite the relative stability of its real estate model, EPR faces several structural risks that investors should consider when evaluating the long-term investment case.

One notable factor involves market liquidity. Current daily trading volume averages approximately 271,836 shares, a significant decline from the two-month average of 871,361 shares. This reduction in trading activity suggests that market participation has recently slowed.

Lower liquidity can introduce additional volatility, particularly for mid-capitalization REITs. When trading volumes decline, relatively small shifts in supply or demand can produce more pronounced price movements.

Another interesting market indicator is the company’s Dark Pool Index, which currently sits at approximately 60.63%. A DPI above 50% typically indicates that a large portion of trading activity occurs away from public exchanges through private institutional venues.

High dark pool participation can signal several things. On one hand, it may reflect institutional interest in accumulating or adjusting positions without influencing market prices. On the other hand, it can reduce price transparency and contribute to more abrupt price adjustments when large trades eventually appear in the public market.

Operational risks also stem from the company’s specialized asset base. Experiential properties are closely tied to discretionary consumer spending and entertainment demand. During periods of economic stress, visitation levels at theaters, entertainment centers, and recreational venues can decline, potentially affecting tenant performance and rental stability.

While long-term leases provide a measure of protection, tenant credit quality remains an important variable in the stability of rental income.

Capital efficiency metrics offer some reassurance in this regard. The company’s ability to maintain ROIC above its cost of capital suggests that investments are being evaluated carefully and deployed with reasonable discipline.

Nonetheless, the relatively narrow margin between these figures implies that profitability is sensitive to changes in financing costs or operating performance. Rising interest rates or declining tenant activity could compress this spread and reduce value creation.

Overall, the risk profile appears moderate. EPR benefits from a specialized but relatively stable property portfolio, yet investors must remain mindful of liquidity dynamics, economic sensitivity within experiential real estate, and the company’s limited margin of safety at current valuation levels.

Final Assessment

EPR Properties presents a compelling but balanced investment case for income-focused investors. The company’s specialized real estate portfolio generates stable rental income streams, supporting a forward dividend yield of approximately 6.3%. For investors seeking dependable income, that yield alone represents a meaningful component of potential total return.

Operational performance has improved in recent quarters, with earnings growth reflecting a broader stabilization in experiential property demand. Profitability metrics such as ROIC and ROE confirm that the company is again producing solid returns on invested capital, even if those returns remain modest relative to historical peaks.

The primary constraint on the investment case lies in valuation. With shares trading near $56 compared with an intrinsic value estimate of $47.74, the stock currently carries a negative margin of safety of about 19%. This premium suggests that the market has already priced in much of the company’s recovery and stability.

Dividend growth expectations also point toward a slower expansion phase. After a period of rapid increases driven by operational recovery, the dividend is now expected to grow at a more modest pace of roughly 2–3% annually.

For long-term investors focused on income stability, EPR remains a viable holding. The combination of a strong yield, stable property cash flows, and improving profitability supports continued dividend payments.

However, from a valuation standpoint, the current share price limits near-term upside potential. Investors may prefer to wait for a more attractive entry point before initiating or expanding positions.

In its current state, EPR Properties appears best suited for investors seeking reliable income rather than aggressive capital appreciation. The company’s stable real estate foundation supports long-term dividend sustainability, but valuation discipline remains essential when considering new investments.