Enterprise Products Partners: High Yield, Fully Valued

A high-yield MLP trading above intrinsic value

Investment Thesis: Durable Midstream Cash Flows Supported by Economic Profit but Limited by Overvaluation

Enterprise Products Partners EPD 0.00%↑ operates one of the largest integrated midstream networks in North America, transporting and processing natural gas, natural gas liquids, crude oil, refined products, and petrochemicals across most producing basins in the continental United States. The partnership’s scale and position in the NGL market allow it to operate across nearly the entire hydrocarbon value chain, providing unusually stable fee-based cash flows relative to upstream energy producers.

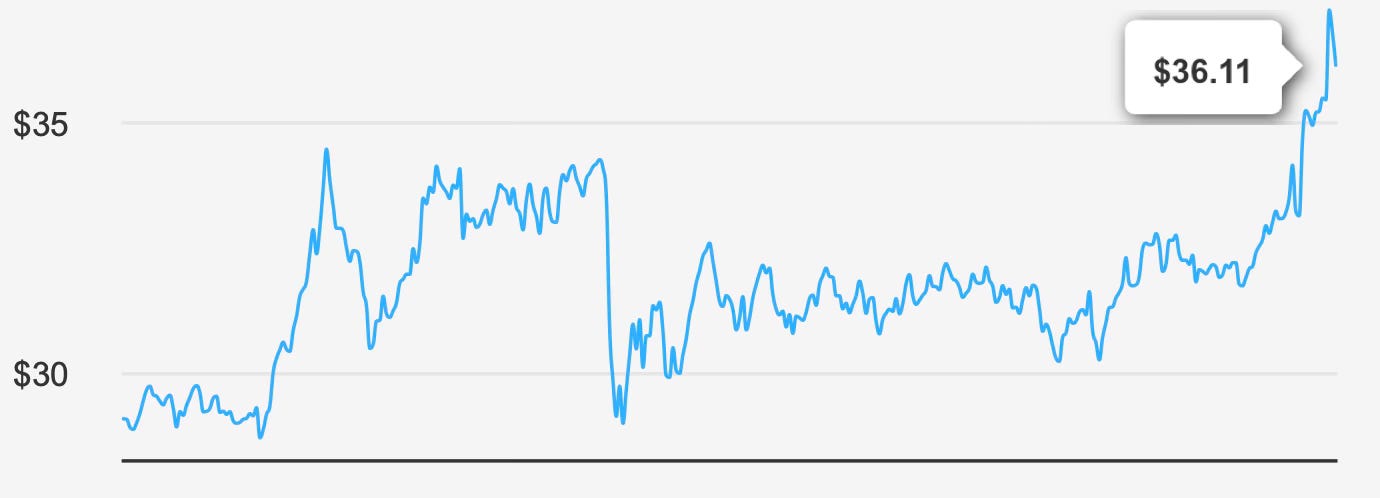

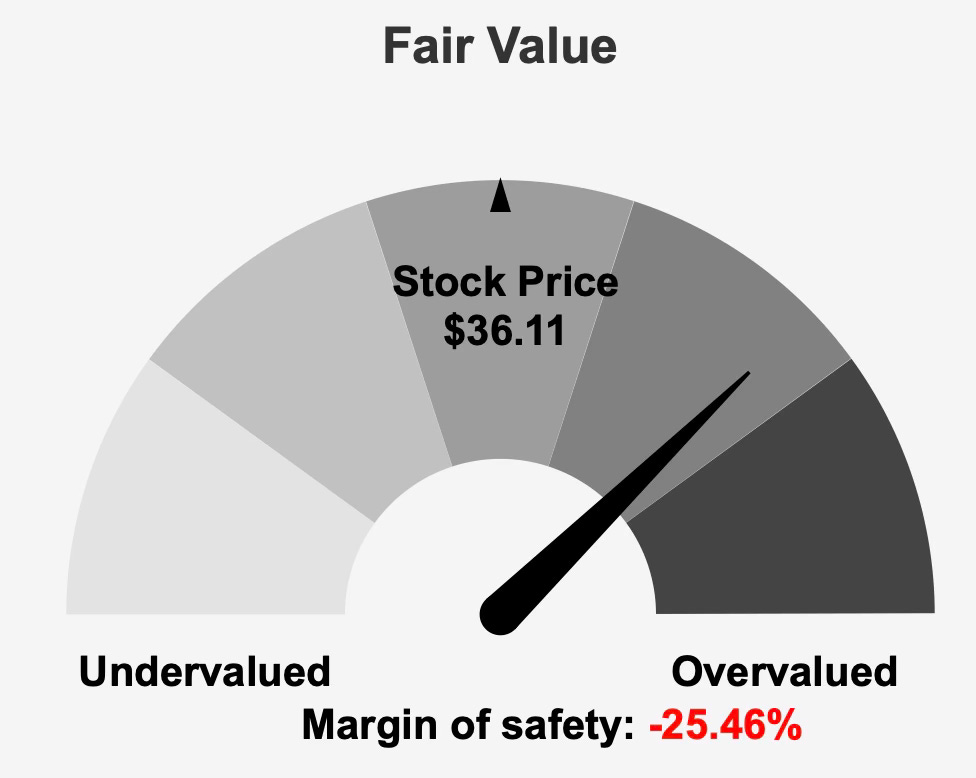

At roughly $36 per unit, the market assigns a valuation above the estimated intrinsic value of $28.78, leaving a negative margin of safety near 25%. Despite a forward distribution yield around 6.0%, investors today are effectively paying a premium for reliability rather than receiving compensation for uncertainty.

The central investment tension lies between operating stability and valuation discipline. The partnership consistently generates returns on invested capital above its cost of capital, indicating economic profitability. Yet the market already prices in that stability. Unlike distressed high-yield securities where yield compensates for risk, Enterprise Products represents the opposite case: a stable asset with income appeal but limited valuation support.

The distribution itself appears durable because of predictable midstream cash flows and steady earnings growth. However, future investor returns depend more on entry price than operational quality. The yield compensates for low growth but not for valuation compression should sentiment shift.

For income investors, the partnership therefore offers dependable cash generation rather than compelling total return potential at current prices. The story is less about safety — which appears solid — and more about paying too much for it.

2. Earnings Momentum & Profitability Trends

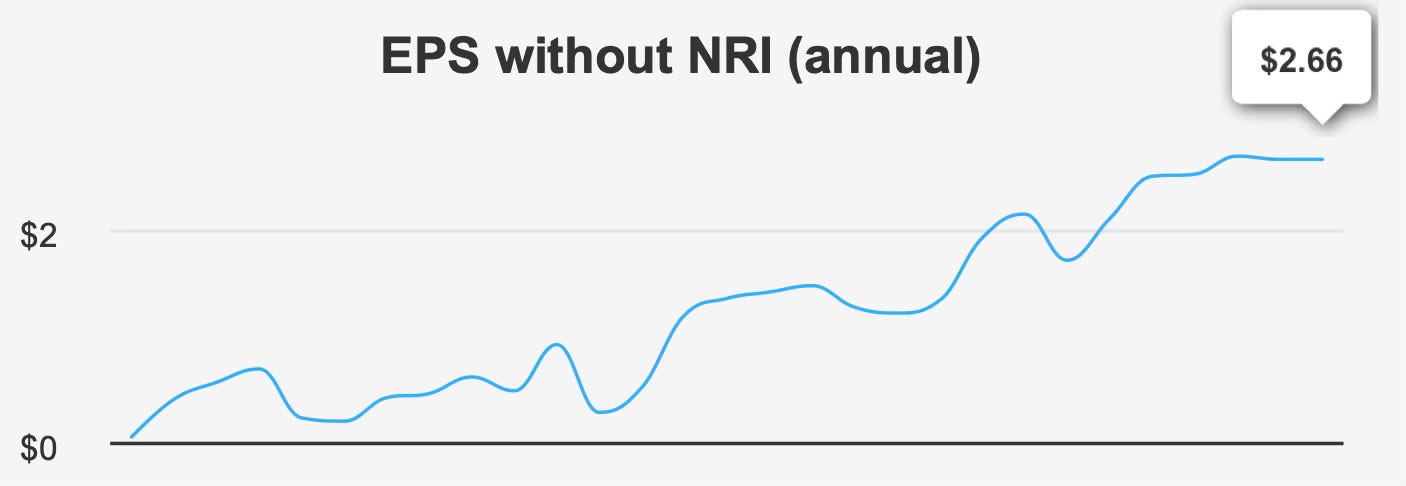

Enterprise Products continues to demonstrate steady operating performance rather than cyclical swings typical of commodity producers. In the quarter ending December 31, 2025, adjusted earnings reached $0.75 per unit, rising from $0.61 in the prior quarter and slightly above $0.74 a year earlier. Revenue per share improved sequentially to $6.31 from $5.50 but remained modestly below $6.49 year over year.

Over longer periods, the partnership’s growth profile remains consistent. Adjusted earnings have compounded at approximately 7.3% annually over five years and 8.3% over ten years. This places Enterprise Products close to the expected long-term industry growth rate near 4–5%, reflecting steady expansion rather than aggressive capacity additions.

Margins support this stability narrative. Gross margin of 13.6% closely matches the five-year median of 13.5%, although it remains below historical highs near 17.8%. This suggests normalization following earlier favorable energy market conditions rather than structural deterioration.

Looking ahead, analysts forecast earnings of roughly $2.77 next year and $3.10 the year after, implying moderate growth supported by incremental infrastructure utilization rather than volume surges. Revenue expectations also point to expansion from approximately $53.1 billion in 2026 to $65.1 billion by 2028, consistent with gradual throughput increases across the system.

Capital allocation further reinforces stability. Share repurchases remain minimal at roughly 0.2% over the past year, aligning with the partnership model that prioritizes distributions and reinvestment over buybacks.

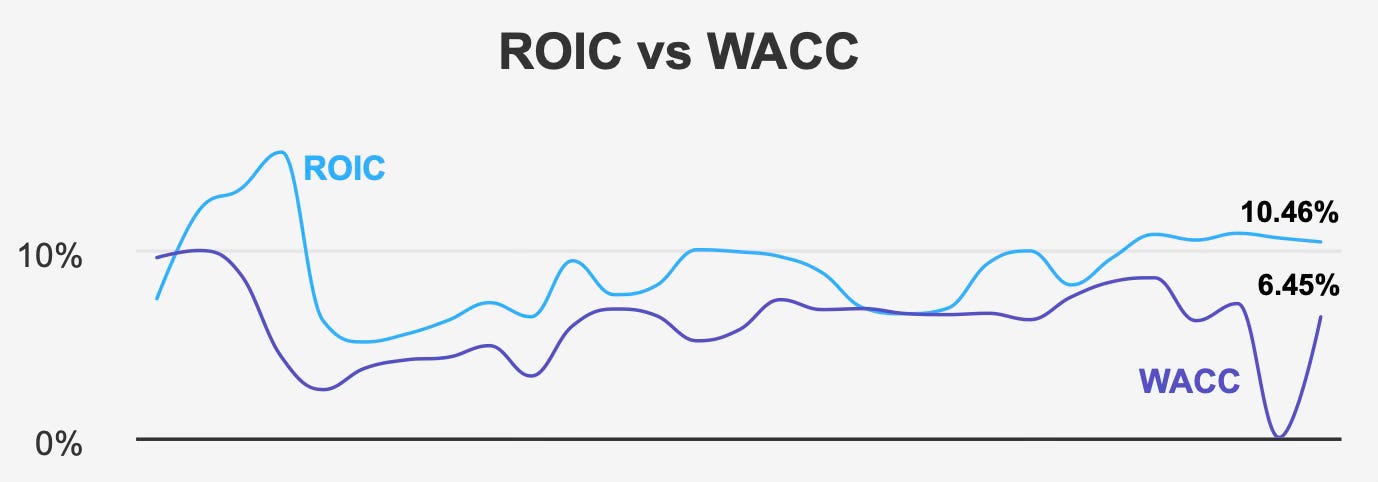

The most important indicator of long-term durability is economic profitability. Enterprise Products produces a return on invested capital near 10.5%, comfortably exceeding its cost of capital around 6.5%. Over five years the spread has persisted, demonstrating that new projects generate value rather than merely sustaining volumes.

Return on equity near 20% reflects efficient capital usage within a capital-intensive industry. Unlike many energy businesses that destroy value during expansion cycles, Enterprise Products has historically expanded while maintaining returns above financing costs.

Taken together, earnings trends indicate a slow-growing but financially consistent infrastructure operator. The partnership is unlikely to deliver rapid growth, but its cash flow base appears structurally stable.

3. Dividend Profile & Sustainability

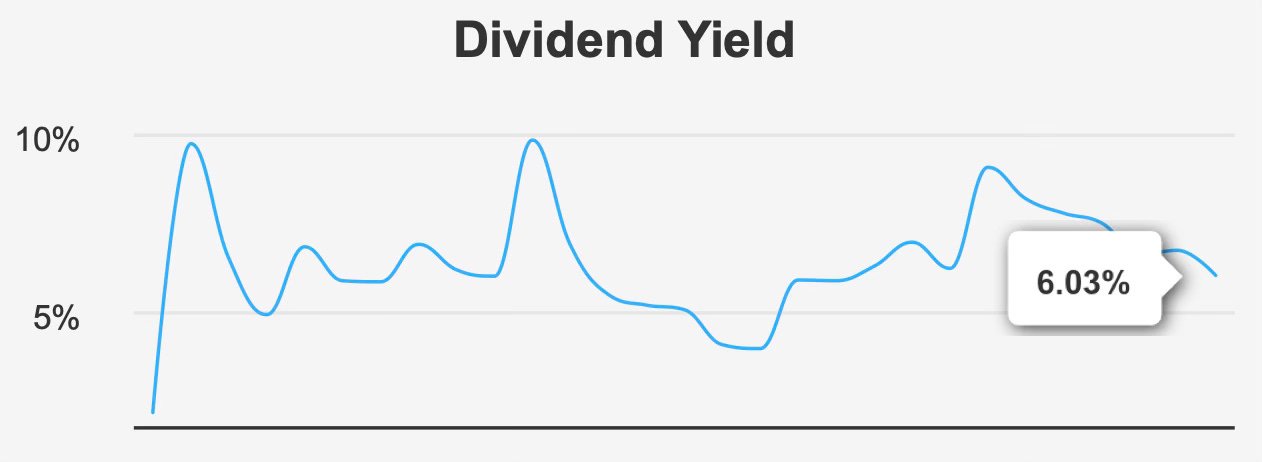

The partnership’s defining feature remains its income stream. The forward distribution yield stands near 6.0%, within its long-term range but below the ten-year median of roughly 6.8%. The recent quarterly distribution of $0.55 per unit continues a long pattern of incremental increases.

Growth has been modest but reliable. Distributions have risen about 3.5% annually over five years and roughly 4.9% over three years. Future increases are expected near 6.2%, suggesting management confidence in expanding distributable cash flow.

The payout ratio near 81% reflects a typical MLP structure where most cash flow is returned to unitholders. Unlike corporate dividends, this higher ratio does not automatically imply danger, but it does reduce flexibility if operating conditions weaken.

Coverage remains adequate at approximately 1.23x, meaning current cash generation exceeds distributions with a reasonable buffer. The next ex-dividend date of January 30, 2026, followed by payment on February 13, 2026, maintains a consistent quarterly cadence that income investors rely upon.

The primary sustainability question is leverage rather than earnings volatility. Debt to EBITDA around 4.6 sits slightly above typical comfort levels for midstream partnerships. While manageable under stable cash flows, it reduces flexibility during downturns and limits aggressive distribution growth.

In practical terms, the distribution appears dependable but not rapidly expanding. Investors should expect low-single-digit annual increases consistent with infrastructure-style assets rather than growth equities.

4. Valuation: Premium Pricing Reflects Stability More Than Growth Prospects

Enterprise Products trades above its intrinsic value estimate of $28.78 at a market price around $36, implying a negative margin of safety near 25%. Investors are effectively paying upfront for perceived reliability.

The forward earnings multiple near 13.1x sits slightly above its long-term median near 12.4x. While not extreme, it indicates the market assigns a modest premium to stable cash flows. Similarly, the price-to-sales ratio of 1.5x aligns closely with historical norms, suggesting revenue valuation remains steady.

Cash flow valuation appears more stretched. EV/EBITDA near 15.5x exceeds the historical median around 11.2x and approaches the upper end of its historical range. Price-to-free-cash-flow around 25.6x also stands well above the long-term median near 18.2x, reinforcing that investors currently accept lower implied returns in exchange for stability.

Price-to-book near 2.7x similarly reflects a premium relative to long-term norms, though not excessive. Analyst price targets around $36.71 indicate limited upside from current levels.

Overall, valuation metrics consistently tell the same story: the partnership is not overpriced relative to peers but expensive relative to its own history and intrinsic value. The yield therefore compensates primarily for low growth, not valuation risk.

5. Risk Assessment & Capital Structure Considerations

Enterprise Products faces relatively low operational risk but meaningful financial sensitivity to leverage and valuation. The partnership has issued roughly $4.4 billion of debt over the past three years, raising concerns about long-term balance sheet flexibility.

The Altman Z-score of 1.96 suggests moderate financial stress rather than distress, reinforcing that the business is stable but capital-intensive. Margin declines of roughly 7% annually in both gross and operating measures indicate cost pressures that could modestly affect future profitability.

Revenue per share has weakened slightly and the distribution payout ratio remains elevated, limiting room for aggressive growth if energy demand softens.

On the positive side, insider buying without selling activity indicates internal confidence, and earnings quality metrics suggest low manipulation risk. Institutional ownership around 25% adds stability to trading dynamics.

Liquidity remains strong, with daily trading volume exceeding five million units and dark-pool activity above 50%, pointing to consistent institutional participation.

Overall risk is not operational survival but return compression. The partnership’s stability reduces the probability of distribution cuts but increases sensitivity to interest rates and valuation shifts.

Final Assessment

Enterprise Products Partners represents a dependable income vehicle rather than a discounted opportunity. The partnership generates economic profit, produces stable earnings, and supports a well-covered distribution. Operationally, it behaves more like infrastructure than energy.

However, the market already recognizes this stability. Units trade above intrinsic value, multiples sit above long-term norms, and upside appears limited relative to downside if valuation normalizes.

Income investors therefore face a trade-off: accept a reliable 6% yield with modest growth, or wait for a more favorable entry point that improves long-term return potential.

The distribution itself appears sustainable. The investment case, however, depends almost entirely on price paid. At current levels, Enterprise Products is best viewed as a high-quality holding worth maintaining but not aggressively accumulating.