Ellington Credit Company: Assessing a 19% Yield Against Structural Profitability Limits

High yield, improving earnings, and the key risks investors must consider

Investment Thesis: Income Appeal Supported by Improving Earnings but Limited Long-Term Value Creation

Ellington Credit Company EARN 0.00%↑ operates within the asset management sector with a focused strategy centered on corporate collateralized loan obligations (CLOs). The firm primarily invests in mezzanine debt and equity tranches across the CLO capital structure, targeting investments that generate strong current income while also supporting risk-adjusted total returns over time.

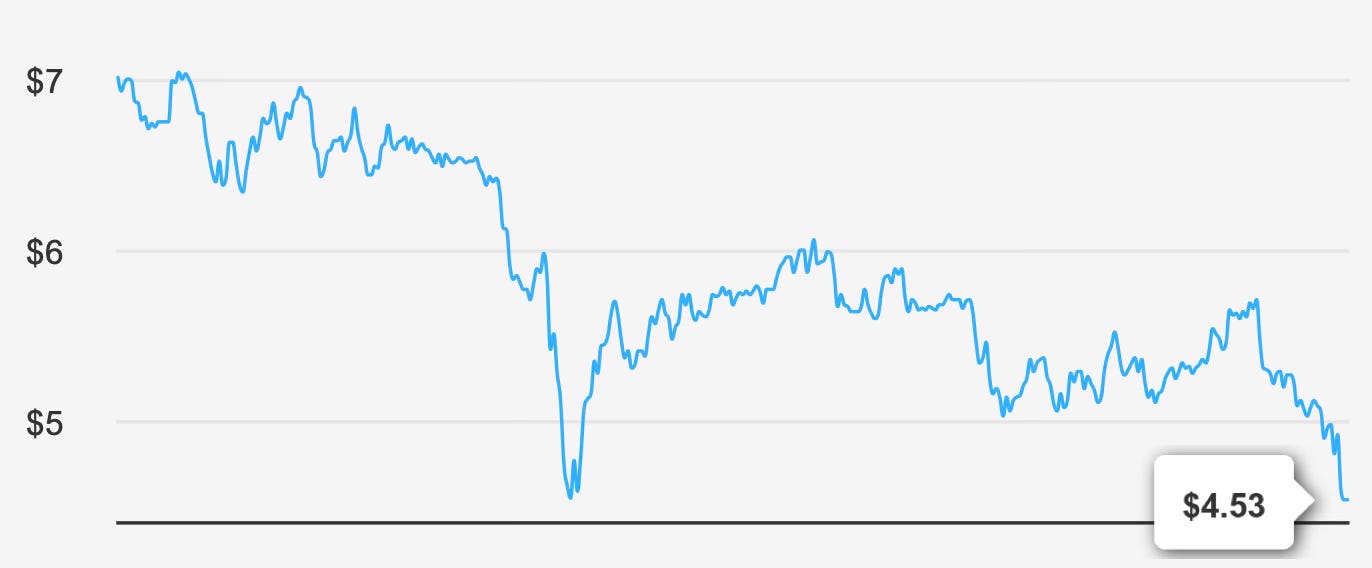

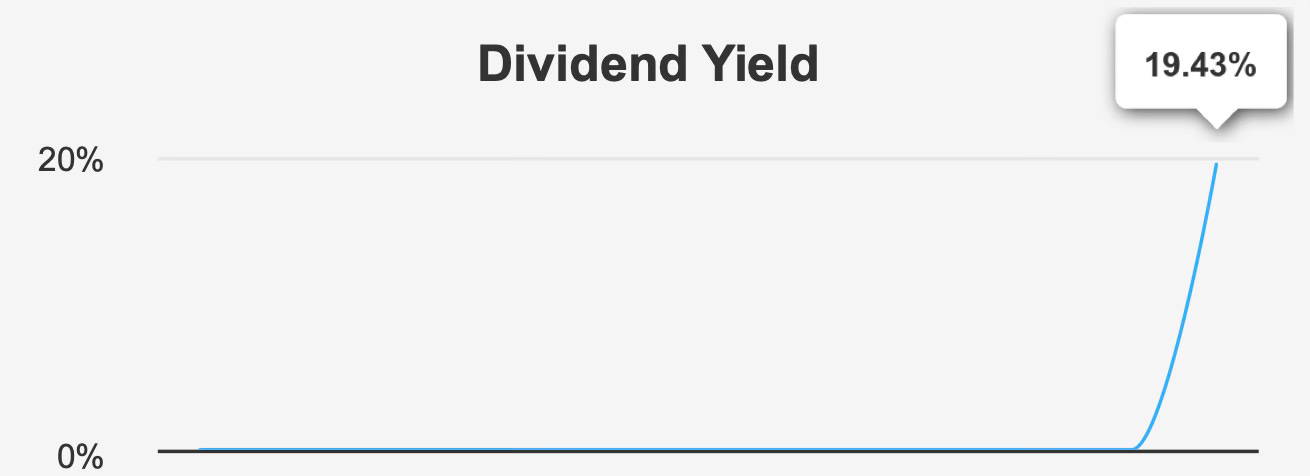

At the current share price of approximately $4, the company carries a market capitalization of about $170.2 million. The core investment appeal is straightforward: Ellington Credit offers a forward dividend yield of roughly 19.4%, a level that dramatically exceeds typical income yields available within the broader asset management and credit-investment universe.

Such a high yield naturally attracts income-oriented investors seeking elevated cash flow. Yet yield alone does not define investment quality. A deeper review of the company’s operating profile reveals a more complex picture where strong income potential is paired with structural profitability challenges.

Recent earnings improvements indicate that the firm’s investment portfolio has begun generating stronger income streams. However, longer-term growth metrics remain stagnant. Over both five-year and ten-year periods, compound annual EPS growth has effectively remained flat. This pattern suggests that while the company may experience periods of improving profitability, sustained long-term earnings expansion has been difficult to achieve.

The broader industry outlook does offer some support. Asset management and credit investment markets are projected to expand at roughly 5% annually over the coming decade. For firms with expertise in structured credit investments such as CLO tranches, this environment could create opportunities to scale income-generating portfolios.

Nevertheless, the investment thesis ultimately hinges on a critical structural issue: the company’s ability to generate economic returns above its cost of capital. Historical performance suggests that this has been a persistent challenge.

As a result, Ellington Credit presents a clear but nuanced investment proposition. The company delivers exceptional income potential and has demonstrated recent earnings improvement, but long-term value creation remains uncertain. Investors considering the stock must therefore balance the appeal of its high yield with the structural limitations embedded in its profitability profile.

Earnings Momentum & Profitability Trends

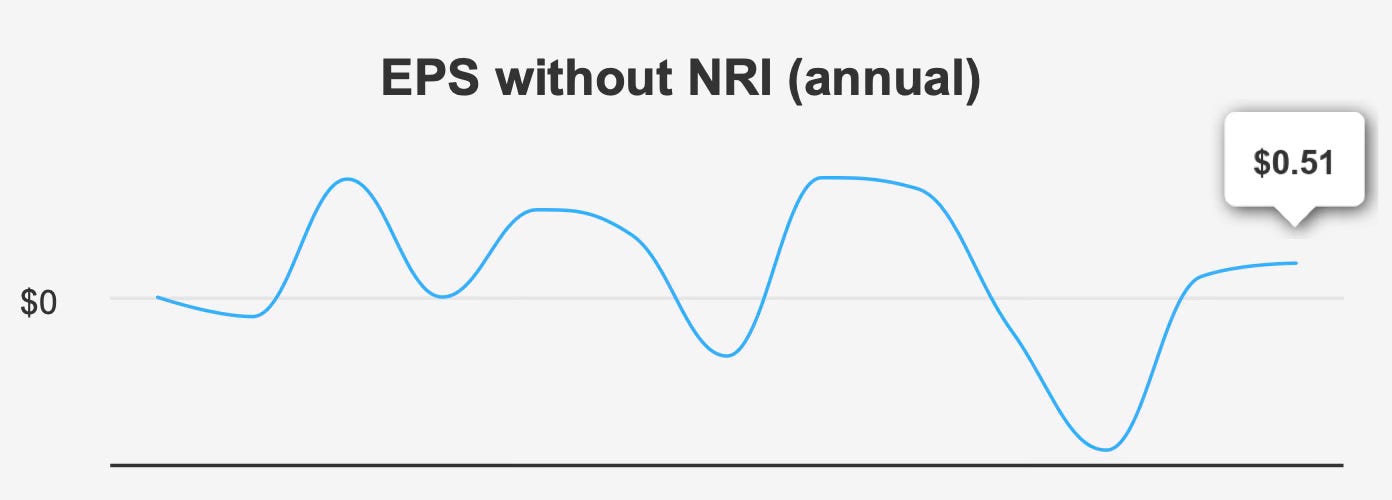

Recent financial results indicate a notable improvement in Ellington Credit’s earnings performance. In the most recent quarter ending September 2025, earnings per share excluding non-recurring items reached $0.39. This represents a significant increase from $0.12 in the previous quarter and $0.16 in the same quarter a year earlier.

The improvement suggests that portfolio performance and operational efficiency have strengthened in the near term. Revenue per share also increased meaningfully, rising to $0.45 from $0.37 in the prior quarter. Together, these results reflect stronger income generation from the firm’s investment portfolio.

Looking ahead, analyst expectations suggest that earnings growth may continue. Consensus projections estimate earnings per share of approximately $0.96 for the next fiscal year, followed by about $1.01 the year after. If achieved, these figures would represent a gradual but steady improvement in profitability.

Revenue growth expectations also appear moderate but positive. Total revenue is projected to reach roughly $52.1 million by 2026, suggesting incremental expansion in the company’s investment portfolio and income-generating assets.

Despite these encouraging short-term trends, several structural concerns remain.

One of the most notable issues is the absence of long-term earnings growth. Over both five-year and ten-year horizons, compound annual EPS growth remains effectively flat. This indicates that earnings improvements have tended to occur in cycles rather than through sustained expansion.

Share dilution has also played a role in shaping shareholder outcomes. The company’s one-year share buyback ratio stands at approximately –77.8, indicating significant share issuance rather than repurchases. Over a three-year period, the buyback ratio remains negative at roughly –14.6.

Persistent share issuance can dilute earnings per share and reduce the effectiveness of dividend distributions. While raising capital can support portfolio expansion, it also spreads earnings across a larger shareholder base.

Overall, Ellington Credit’s earnings outlook appears cautiously improving. Short-term profitability trends are favorable, and industry growth may provide additional support. However, the absence of long-term growth and the effects of share dilution mean that earnings stability will remain an important factor in evaluating the company’s future performance.

Dividend Profile & Sustainability

The dividend policy represents the most compelling element of Ellington Credit’s investment profile. The company distributes a monthly dividend of $0.08 per share, resulting in a forward dividend yield of approximately 19.4%.

Monthly dividends are particularly attractive to income investors because they provide steady and predictable cash flow throughout the year. With twelve payments annually, the structure resembles an income stream more commonly associated with fixed-income securities than with traditional equities.

However, the sustainability of such an elevated yield warrants careful evaluation.

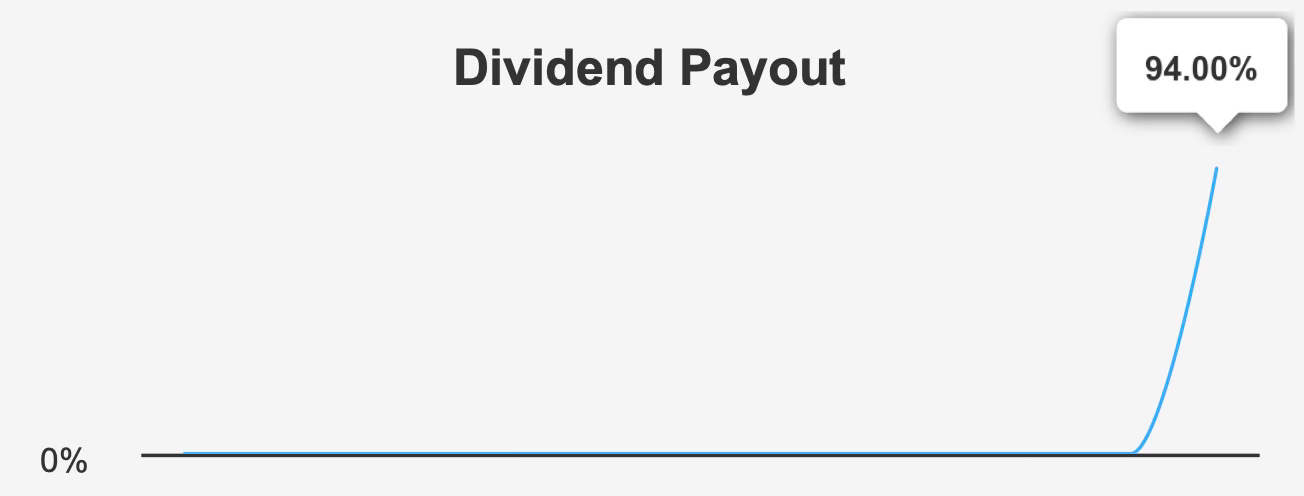

The company’s dividend payout ratio currently stands at roughly 94%. This level indicates that nearly all earnings are being distributed to shareholders rather than retained within the business. While high payout ratios are common among income-oriented investment vehicles, a ratio approaching 100% leaves very little room for operational volatility.

Dividend coverage currently sits at approximately 1.06, suggesting that earnings slightly exceed the amount required to fund dividend payments. Although this technically supports the dividend, it also implies a relatively thin margin of safety.

Another notable feature of the dividend profile is the absence of growth. Over both three-year and five-year periods, dividend growth has remained at 0%. Forecasts also indicate that dividend payments are likely to remain flat over the next three to five years.

This pattern reinforces the idea that Ellington Credit functions primarily as a high-income security rather than a dividend growth investment. Investors receive substantial current income but should not expect regular increases in payout levels.

Dividend timing remains predictable. The most recent ex-dividend date occurred on February 27, 2026, with payment scheduled for March 31, 2026. Such consistency is valuable for investors who rely on dividends as part of their income planning.

Ultimately, the dividend profile offers both appeal and caution. The yield is extraordinarily high, but its sustainability depends heavily on the company’s ability to maintain stable earnings in an environment where profitability margins remain relatively constrained.

Valuation Analysis: Assessing Market Pricing and Income-Based Value

Valuation analysis for Ellington Credit is complicated by limited intrinsic value data, making traditional discounted cash flow approaches difficult to apply. As a result, investors must rely on relative indicators and broader market signals when evaluating the stock’s attractiveness.

One notable indicator is the stock’s current trading level. Shares are currently near a five-year low, reflecting a market environment where investor expectations appear relatively subdued.

Similarly, the company’s price-to-earnings ratio has approached a three-year low, suggesting that the market may be assigning limited long-term growth expectations to the firm.

However, valuation signals are not uniformly supportive. The stock’s price-to-book ratio has recently approached a one-year high. This implies that while earnings-based metrics may suggest relative value, asset-based valuation measures indicate that the shares may not be particularly cheap relative to the company’s underlying asset base.

This divergence highlights the challenges of valuing structured credit investment firms. Market pricing often reflects expectations about income stability rather than conventional growth metrics.

For income-focused investors, valuation ultimately depends on dividend sustainability. If the company maintains its current payout level, the present yield alone may justify the stock’s valuation despite modest growth prospects.

Conversely, if earnings volatility forces a reduction in dividends, the market’s current pricing could prove difficult to sustain.

Risk Assessment & Capital Structure Considerations

Ellington Credit’s risk profile reflects a combination of financial strengths and structural challenges.

One of the company’s most notable advantages is its balance sheet structure. The firm currently operates without debt, eliminating interest-expense obligations and reducing financial leverage risk. A debt-free structure provides flexibility during periods of market volatility and allows the company to manage its portfolio without the pressure of refinancing obligations.

However, the absence of debt does not necessarily translate into strong economic returns.

Return on invested capital has consistently been reported at 0%, indicating that the company has struggled to generate meaningful returns from its asset base. In contrast, the weighted average cost of capital currently stands around 2.5% and has reached as high as 9.9% over the past decade.

When returns on invested capital remain below the cost of capital, economic value creation becomes difficult. In practical terms, this dynamic suggests that the company has historically eroded rather than created shareholder value.

Return on equity provides a slightly more favorable perspective, reaching roughly 8.6%. While this level indicates some profitability, it remains modest relative to the risks associated with structured credit investments.

Operational risks also deserve attention. Revenue per share has declined over the past three years, indicating that portfolio income has not consistently expanded.

Ownership dynamics offer limited additional reassurance. Insider ownership stands at approximately 1.0%, while institutional investors hold about 10.3% of the company’s shares. Although insiders have made several purchases over the past year and no sales have been reported, overall insider ownership remains relatively modest.

From a trading perspective, liquidity appears strong. Daily trading volume averages around 735,796 shares, significantly higher than the two-month average of roughly 369,131 shares. This level of liquidity supports efficient market participation and allows investors to enter or exit positions without significant price disruption.

Overall, the company’s primary risk lies not in financial leverage but in its structural profitability profile. The ability to consistently generate returns from its investment portfolio will remain the central determinant of long-term shareholder outcomes.

Final Assessment

Ellington Credit Company represents a distinctive income investment opportunity defined by exceptionally high dividend yield and modest near-term earnings improvement.

The company’s forward dividend yield of roughly 19.4% is among the highest available in publicly traded equities, and its monthly distribution structure provides a steady income stream that may appeal strongly to income-focused investors.

Recent earnings momentum is encouraging. Profitability has improved in recent quarters, and analyst projections suggest that earnings could continue to rise modestly over the next two years.

Yet the broader structural picture remains mixed. Long-term earnings growth has been essentially flat, and the company has historically struggled to generate returns above its cost of capital. Combined with a dividend payout ratio near 94%, these factors create a relatively narrow margin for operational setbacks.

Market pricing reflects this balance of opportunity and caution. While the stock trades near multi-year lows and offers extraordinary income potential, concerns surrounding long-term value creation continue to influence investor sentiment.

For investors prioritizing immediate income, Ellington Credit may represent a compelling high-yield opportunity. The company’s current earnings trajectory appears sufficient to support its dividend in the near term.

However, sustaining such a high payout will require continued earnings stability and disciplined portfolio management. Without meaningful improvements in capital efficiency, the company may remain primarily an income vehicle rather than a long-term compounding investment.

In that context, Ellington Credit can best be viewed as a specialized income security: attractive for yield-focused portfolios, but one that requires ongoing monitoring of the economic fundamentals that ultimately support its dividends.