Dynex Capital: When a 15% Dividend Masks Structural Weakness

A Deep Dive Into Earnings Quality, Dividend Sustainability, and Valuation Risk

Investment Thesis: A High-Yield Mortgage REIT With Limited Economic Value Creation

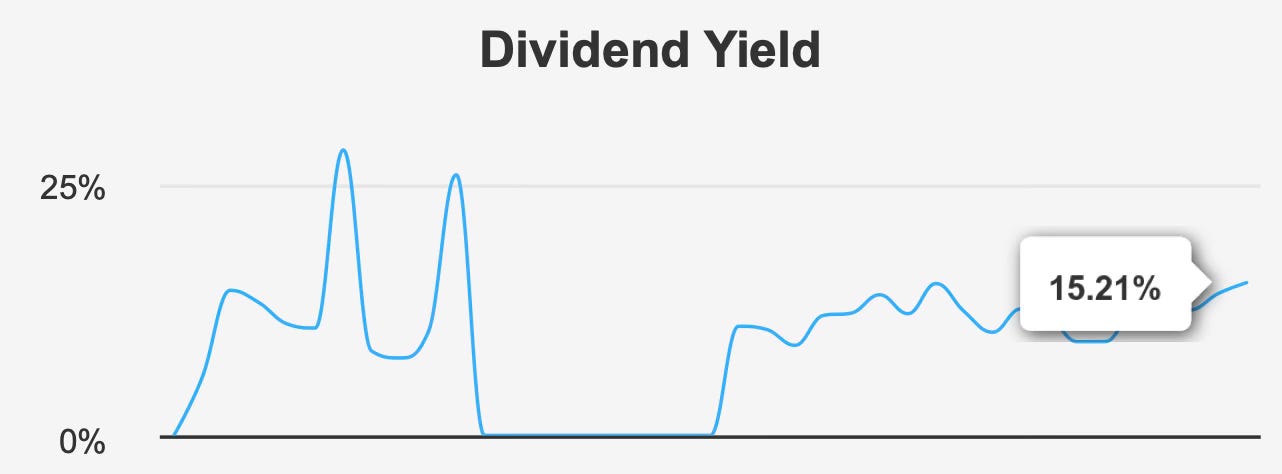

Dynex Capital DX 0.00%↑ operates in a segment of the real estate investment trust market focused on mortgage-backed securities, primarily agency residential and commercial mortgage-backed securities guaranteed by government-sponsored enterprises. This structure allows the company to generate income through spread investing while distributing the majority of its earnings as dividends to shareholders. The investment appeal of Dynex Capital largely centers on its income profile, highlighted by a forward dividend yield of 15.2%, significantly above its historical 10-year median yield of 12.1%.

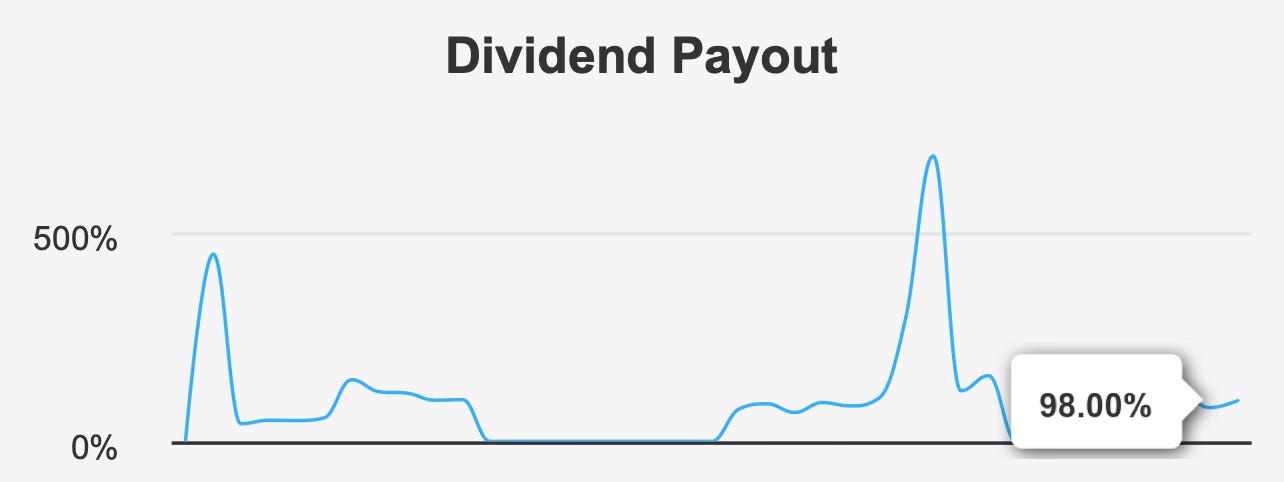

At first glance, such a yield can appear compelling for income-focused investors, particularly within the REIT sector where high distributions are common. However, a deeper examination reveals that the current dividend yield may reflect elevated risk rather than a durable income opportunity. The company’s payout ratio sits at approximately 98%, leaving minimal margin for reinvestment or earnings volatility. With such a narrow buffer, even modest earnings pressure could threaten dividend stability.

The broader growth profile also raises questions about long-term income sustainability. Dynex Capital’s five-year revenue growth stands at negative 23.4%, while the long-term revenue trend over ten years has been effectively flat. This stagnation suggests that the company’s earnings base has struggled to expand meaningfully over time, limiting its ability to support consistent dividend growth.

Capital efficiency further complicates the investment case. The firm’s return on invested capital has remained at 0.0% over both five-year and ten-year periods, while the weighted average cost of capital stands near 10.8%. When returns fail to exceed the cost of capital, the business effectively destroys shareholder value rather than creating it.

While recent earnings improvements and aggressive share repurchase activity have temporarily boosted per-share metrics, these factors appear more reflective of financial engineering than structural growth. As a result, Dynex Capital currently represents a classic high-yield scenario where income appears attractive, but the underlying economics of the business remain fragile.

Earnings Momentum and Profitability Trends: Recent Improvement Amid Structural Growth Constraints

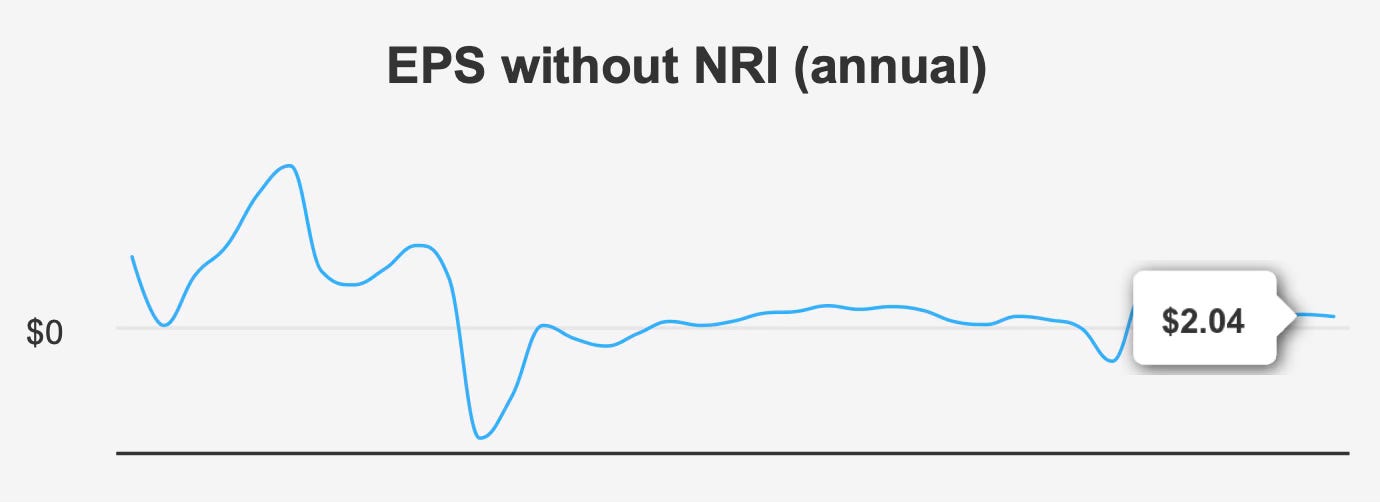

Dynex Capital has shown a notable improvement in earnings over the past several quarters, particularly following earlier volatility in 2025. In the most recent quarter ending December 2025, the company reported earnings per share excluding non-recurring items of $1.16, an increase from $1.08 in the prior quarter and nearly double the $0.60 reported in the same quarter the previous year.

This rebound suggests that portfolio positioning and interest rate dynamics have recently moved in the company’s favor. Mortgage REIT earnings are highly sensitive to changes in interest rate spreads, funding costs, and mortgage prepayment behavior. Improvements in these areas can quickly translate into higher earnings due to the leveraged nature of the business model.

However, the sustainability of this earnings momentum remains uncertain. Historical operating data indicates that Dynex Capital’s gross margin has remained largely stagnant over the past five years. This suggests that despite fluctuations in earnings, the underlying profitability of the investment portfolio has not structurally improved.

Share repurchase activity has also played a role in recent earnings growth. The company reported a one-year buyback ratio of negative 106.9%, indicating substantial share activity that has affected the share count. While buybacks can enhance per-share earnings, the unusual magnitude of this ratio suggests that new share issuance may have offset repurchases. In practical terms, this dynamic can artificially inflate earnings per share without reflecting meaningful growth in the underlying business.

Looking ahead, analyst estimates project modest continued earnings expansion. Forecasts suggest earnings per share could rise to approximately $1.41 in the next fiscal year and $1.47 the following year. Revenue projections indicate a similarly uneven trajectory. Expectations point to revenue of roughly $243.7 million in 2026, followed by a temporary decline to $216.7 million before a significant increase to $437.2 million by 2028.

These projections highlight the inherent volatility in mortgage REIT earnings. Revenue and earnings often fluctuate with changes in interest rates, asset yields, and leverage dynamics rather than consistent operational expansion.

While industry growth for mortgage-backed securities is expected to average roughly 3% annually over the coming decade, this modest sector growth rate underscores the limited organic expansion opportunities available to firms like Dynex Capital. In such an environment, the company’s ability to improve profitability will likely depend more on portfolio management and macroeconomic conditions than on traditional business growth.

Dividend Profile and Sustainability: Attractive Yield but Limited Growth Capacity

For most investors considering Dynex Capital, the central attraction is its exceptionally high dividend yield. With a forward yield of 15.2%, the stock ranks among the highest-yielding securities in the REIT universe. This level of income can be particularly appealing in a market environment where reliable yield remains scarce.

The company currently distributes a dividend of $0.17 per share on a monthly basis, maintaining a steady payout structure in recent quarters. Monthly distributions are relatively uncommon among equities and can enhance the appeal of income investments for investors seeking regular cash flow.

However, the sustainability of this dividend deserves close scrutiny. The payout ratio of approximately 98% indicates that nearly all available earnings are being returned to shareholders. While REITs are required to distribute the majority of taxable income, such a high payout leaves almost no buffer for adverse changes in earnings.

Dividend growth expectations are also modest. Over the past three years, dividend growth averaged roughly 8.6%, but projections for the next three to five years suggest growth of only about 0.6%. This dramatic slowdown indicates that management is likely prioritizing dividend stability rather than expansion.

Dividend coverage metrics reinforce this cautious outlook. The company’s dividend coverage ratio stands at approximately 1.02, meaning earnings only marginally exceed the dividend obligation. Even small declines in earnings could therefore force the company to reduce distributions.

For income-focused investors, the key question is whether the current yield compensates for this risk. High-yield securities often reflect market skepticism regarding dividend durability. In Dynex Capital’s case, the combination of slow growth, thin coverage, and volatile earnings suggests that the elevated yield may represent a risk premium rather than a stable long-term income stream.

Valuation Analysis: High Yield Does Not Necessarily Indicate Undervaluation

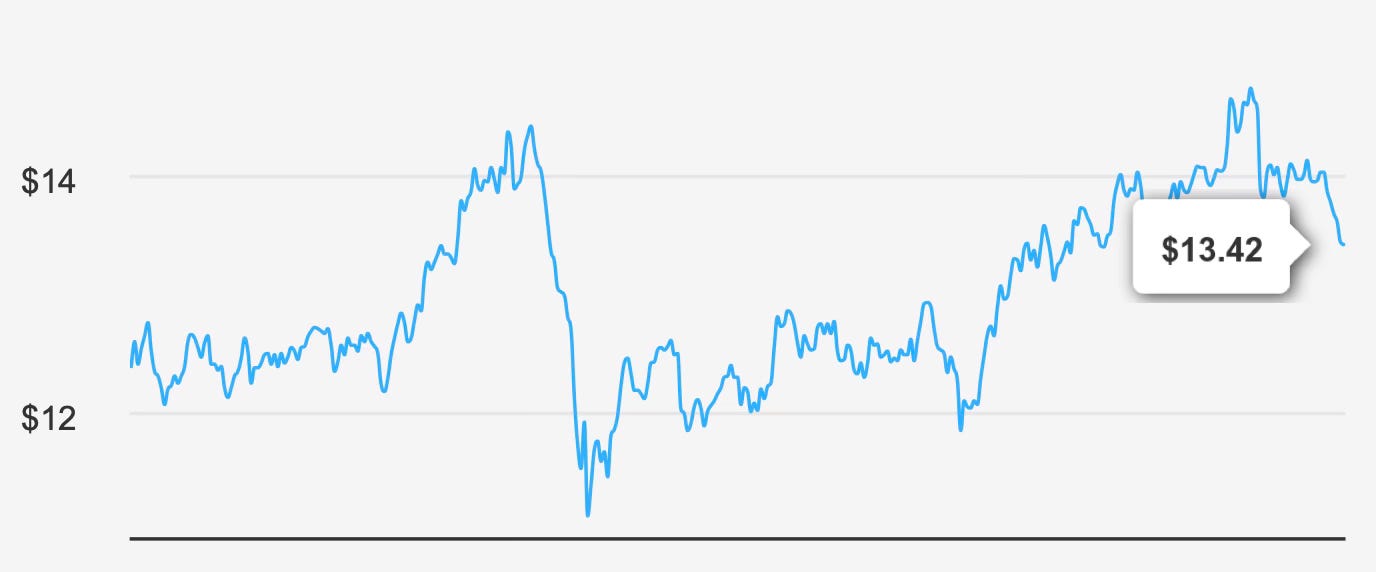

Dynex Capital currently trades around $13 per share, implying a market capitalization of approximately $2.7 billion. Based on intrinsic value estimates of roughly $9.0 per share, the stock appears to trade significantly above its calculated fair value, implying a negative margin of safety approaching 49%.

This discrepancy suggests that the market price may be supported primarily by the stock’s income characteristics rather than by underlying business fundamentals.

Traditional valuation metrics also paint a mixed picture. Current price-to-earnings and price-to-sales ratios are reportedly near two-year lows, which could suggest relative cheapness compared with recent trading history. However, historical comparison alone does not necessarily imply fundamental undervaluation.

In fact, forward valuation dynamics introduce additional concerns. The company’s forward P/E ratio exceeds its trailing P/E ratio, a pattern that typically indicates expectations of declining earnings or reduced profitability. When investors anticipate weaker future earnings, valuation multiples often compress accordingly.

Another important factor influencing valuation is earnings quality. Dynex Capital’s Sloan ratio stands at approximately -47.7%, indicating that a meaningful portion of reported earnings may be derived from accounting accruals rather than cash generation. Lower-quality earnings can make dividend sustainability more uncertain and reduce investor confidence in reported profitability.

At the same time, the company’s dividend yield is currently near a five-year high. In many cases, unusually high dividend yields occur when the market discounts future dividend cuts or deteriorating fundamentals.

Taken together, these valuation signals suggest that Dynex Capital’s apparent income attractiveness may obscure underlying financial fragility. The stock’s valuation appears less like a classic deep-value opportunity and more like a potential value trap where high yield masks weak economic returns.

Risk Assessment and Capital Structure Considerations

Dynex Capital presents a complex risk profile shaped by both structural industry dynamics and company-specific financial characteristics.

One of the most notable concerns is the company’s inability to generate returns above its cost of capital. With a return on invested capital of 0.0% compared with a weighted average cost of capital of approximately 10.8%, Dynex Capital has not demonstrated the ability to create economic value over extended periods. Persistent value destruction at the capital allocation level can limit long-term shareholder returns even when dividends appear attractive.

Revenue trends also signal potential vulnerability. The decline in revenue per share over the past five years indicates that the company’s income-generating capacity has weakened over time. For a high-payout REIT, sustained revenue pressure can quickly translate into dividend stress.

Earnings quality concerns further amplify this risk. The negative Sloan ratio suggests that accounting adjustments may contribute meaningfully to reported profitability, raising questions about the durability of earnings available for distribution.

Despite these challenges, Dynex Capital does possess some financial strengths. Notably, the company operates with no debt on its balance sheet, which reduces financial leverage risk and provides greater flexibility during periods of market stress. A debt-free balance sheet can help offset volatility in mortgage spreads and funding costs.

Ownership structure also offers insight into market perception. Institutional investors hold approximately 40.5% of shares outstanding, indicating meaningful participation from professional asset managers. Insider ownership, however, remains relatively low at around 1.7%, suggesting limited alignment between management and shareholders.

Insider trading activity has also been relatively quiet. Over the past year, insiders executed two purchases and no sales, while no transactions occurred during the most recent three-month period. Although the absence of selling can be interpreted as a neutral signal, the limited scale of insider buying does not strongly reinforce confidence in future growth prospects.

Market liquidity for the stock remains strong. Daily trading volume recently exceeded 9.7 million shares, significantly higher than the two-month average of roughly 6.3 million shares. Elevated liquidity can benefit institutional investors by enabling large trades with minimal market impact.

However, a dark pool index approaching 80% indicates that a substantial share of trading occurs in alternative trading systems rather than public exchanges. While this can signal institutional participation, it may also introduce additional complexity to price discovery.

Final Assessment

Dynex Capital represents a classic example of a high-yield equity whose income appeal must be weighed carefully against underlying economic fundamentals.

The company currently offers one of the most attractive dividend yields in the REIT sector, supported by consistent monthly distributions and a historically high payout level. For investors seeking immediate income, this feature alone may justify interest in the stock.

Yet the broader financial picture reveals significant structural limitations. Revenue growth has been weak, returns on invested capital have failed to exceed the cost of capital, and dividend coverage remains extremely thin. These factors collectively suggest that the company’s ability to sustain and grow its dividend over the long term is uncertain.

Recent improvements in earnings provide some short-term optimism, but these gains appear influenced by share count dynamics and favorable market conditions rather than a fundamental transformation of the business model.

Valuation metrics reinforce this cautious outlook. With shares trading well above estimated intrinsic value and the dividend yield already near historical highs, the risk-reward balance appears unfavorable for long-term investors.

Ultimately, Dynex Capital may continue to attract income-focused investors willing to accept elevated risk in exchange for high yield. However, for investors prioritizing durable dividend growth and consistent value creation, the company’s current financial profile raises significant concerns.