Durable Income at a Discount: Evaluating T. Rowe Price as a Long-Term Dividend Compounder

A financially resilient asset manager offering an above-historical yield with conservative payout coverage

1. Investment Thesis: High-Quality Cash-Generative Asset Manager Temporarily Priced for Low Expectations

T. Rowe Price TROW 0.00%↑ operates one of the most structurally attractive business models in financial services: a fee-based asset manager with limited balance-sheet risk and high incremental margins. The firm manages approximately $1.767 trillion in assets across equities, balanced funds, fixed income, money market products, and alternatives, with roughly two-thirds held in retirement-oriented accounts — a client base that tends to be notably sticky through market cycles.

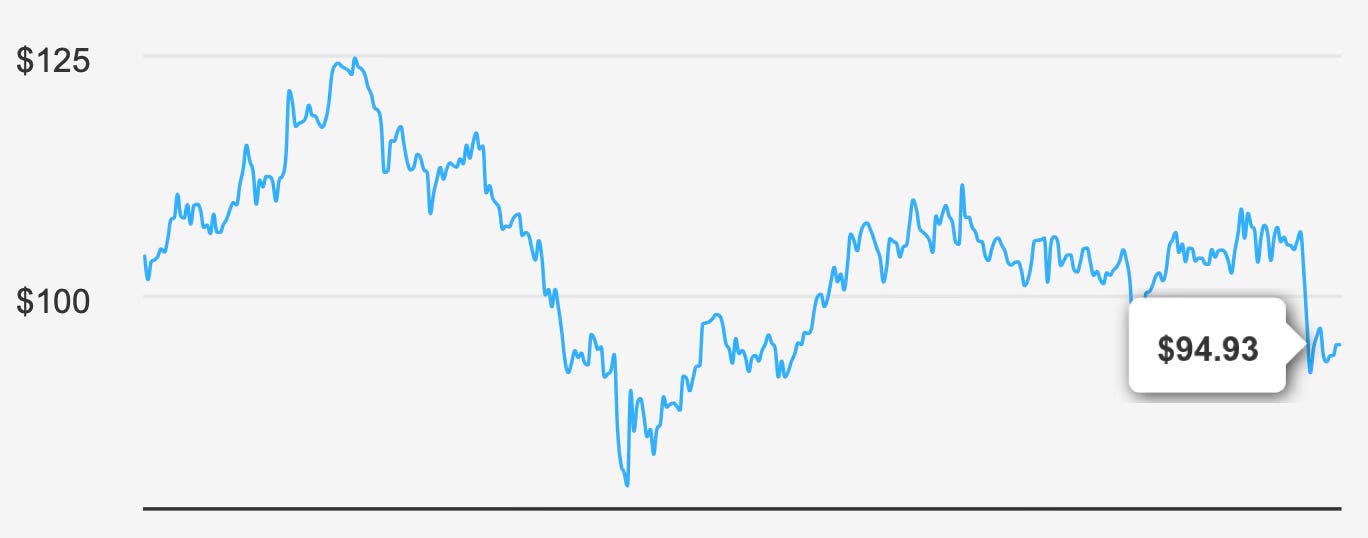

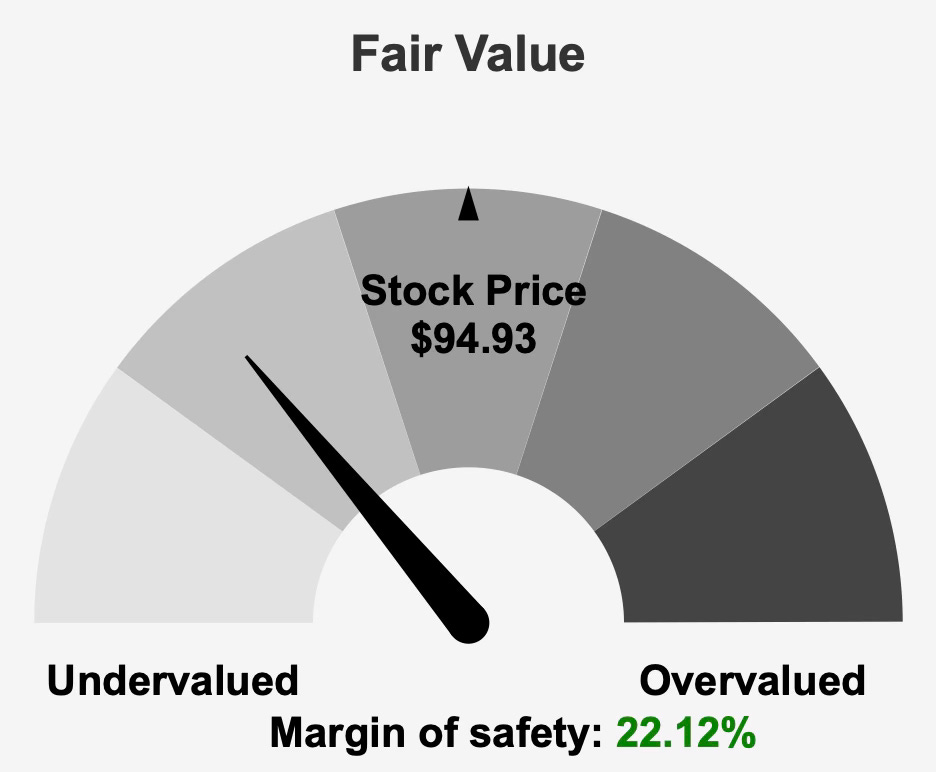

Despite this structural strength, the market currently values the company as if long-term growth is permanently impaired. Shares trade around $94 against an intrinsic value of $121.89, implying a margin of safety near 22.1%. The valuation disconnect largely stems from short-term earnings pressure and slowing flows across active asset management, rather than deterioration in the economics of the business itself.

The core investment case rests on three pillars:

First, the firm consistently generates economic profit. Returns on invested capital remain materially above its cost of capital, confirming the presence of durable competitive advantages. Second, the balance sheet is exceptionally conservative, allowing large portions of earnings to be distributed to shareholders without threatening financial stability. Third, the dividend yield has expanded significantly due to price compression rather than payout expansion, making the income stream more attractive than at almost any point in the past decade.

The market is currently discounting cyclical headwinds — margin compression, slower industry growth, and moderate earnings volatility — as if they are permanent structural damage. Yet long-term industry forecasts still imply roughly 6% annual growth over the coming decade, consistent with demographic retirement savings trends and ongoing demand for professional asset allocation.

In short, investors today are paid a historically elevated yield while waiting for normalization in flows and valuation multiples.

2. Earnings Momentum & Profitability Trends: Cyclical Pressure but Enduring Value Creation

Recent earnings results illustrate the cyclical nature of the business rather than structural decline. Quarterly EPS excluding non-recurring items came in at $2.44, lower than the prior quarter’s $2.81 but meaningfully higher than $2.12 in the same quarter a year earlier. Diluted EPS showed a similar pattern at $1.99 compared with $1.92 year-over-year.

Revenue per share rose modestly to $8.852 from $8.619, signaling operational stabilization following earlier market-driven pressure.

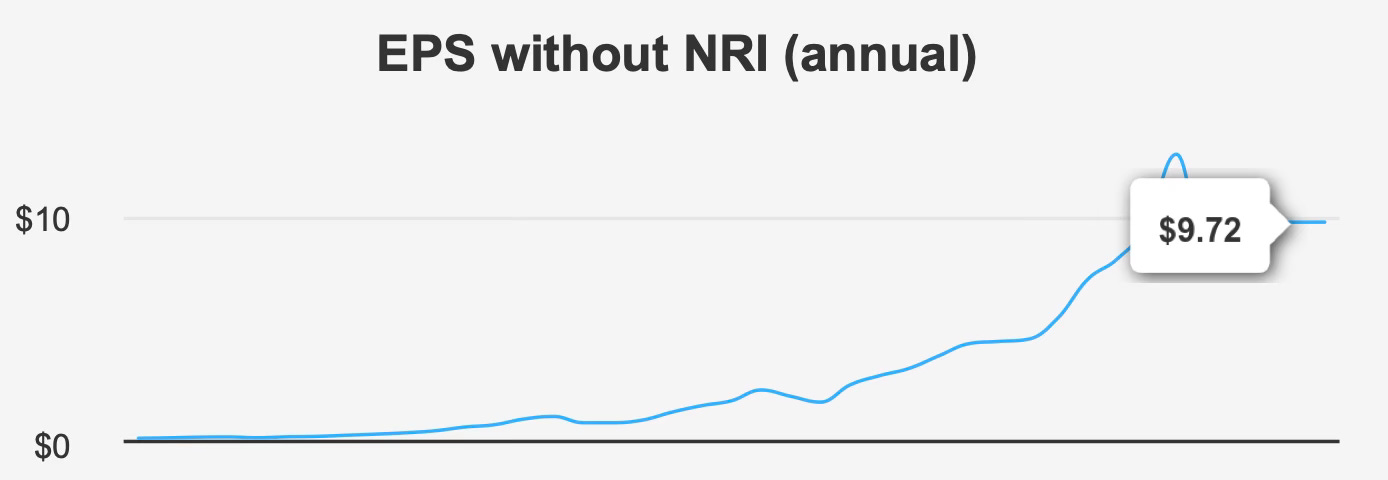

Long-term growth trends further clarify the situation. Over five years, EPS without non-recurring items declined at a 2.6% annual rate, but the 10-year growth rate remains a healthy 8.1%. The divergence highlights the timing of measurement: the past five years captured a challenging market environment for active managers, while the longer period reflects the business’s normal earnings power.

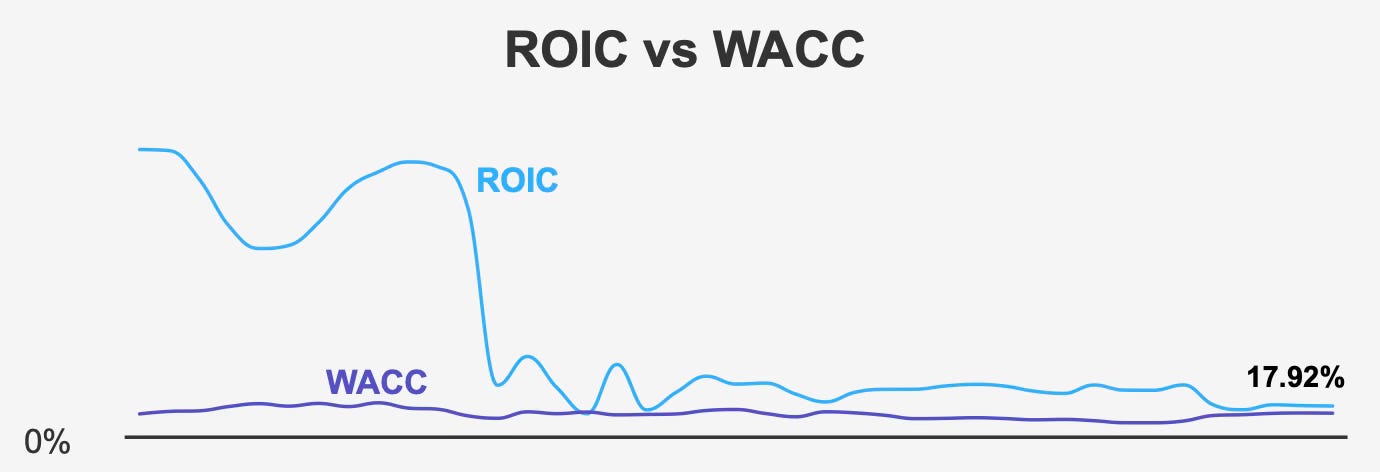

Profitability metrics reinforce this interpretation. The company’s current ROIC of 17.9% exceeds its 13.6% cost of capital, while the 5-year median ROIC of 18.7% similarly exceeds the 12.7% WACC. Over a decade, ROIC has ranged from 15.7% to 30.8%, consistently above the firm’s 9.7% median WACC.

This persistent spread between returns and cost of capital demonstrates that the firm continues to create shareholder value even in weaker operating periods.

Return on equity remains stable near 19.7%, reflecting disciplined capital allocation and limited leverage.

Margins have softened — gross margin recently measured 51.3% versus a 5-year median of 51.9% and well below the prior peak of 61.0%. Operating efficiency also declined, with average annual contraction in gross and operating margins of roughly 3.3% and 6.9%, respectively. However, even after compression, profitability remains strong for a financial services company with minimal capital intensity.

Looking ahead, analysts forecast EPS of $9.687 next fiscal year rising to $9.908 the following year, alongside revenue growth from $7.68 billion in 2026 to $8.01 billion by 2028. These projections imply stabilization rather than rapid expansion — a mature but still productive business.

Share repurchases contribute incremental per-share growth. The company reduced shares outstanding by about 2% over the past year and 1.3% annually over a decade. While not aggressive, buybacks complement dividends without straining liquidity.

Overall, earnings momentum is muted but value creation remains intact — a classic setup for income investors prioritizing durability over acceleration.

3. Dividend Profile & Sustainability: High Yield Supported by Conservative Balance Sheet

The most compelling element of the investment case is the dividend.

The company recently raised its quarterly dividend to $1.30 from $1.27, continuing a multi-decade pattern of annual increases. Over five years, dividends grew at 6.3% annually, though the three-year growth rate slowed to 1.9% amid industry headwinds.

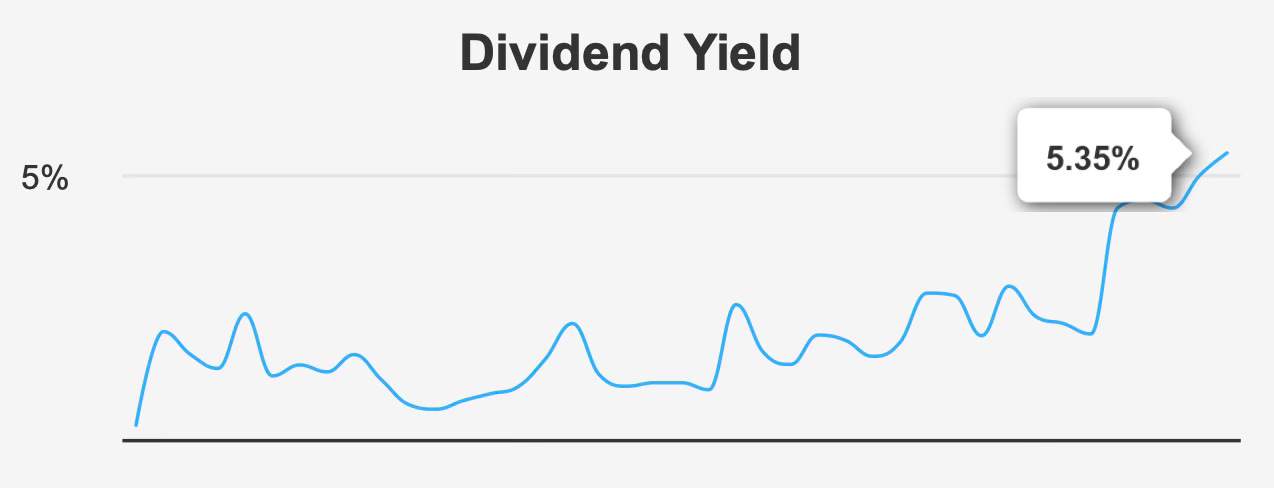

The current forward yield stands at 5.35%, far above the 10-year median yield of 2.95%. Importantly, this expansion occurred primarily due to share price compression rather than payout expansion — a key distinction for sustainability.

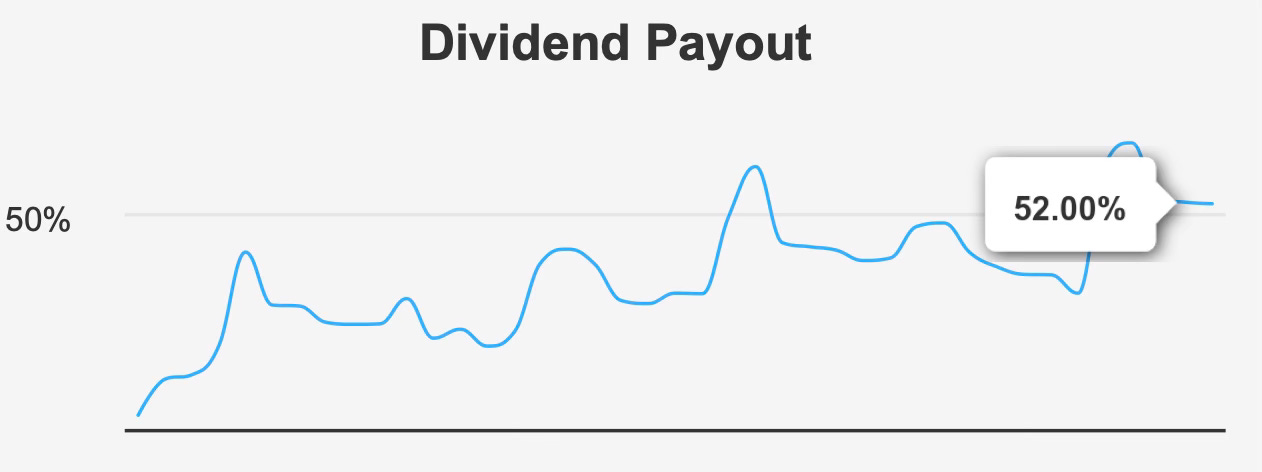

Coverage remains comfortable. The payout ratio sits near 52%, leaving significant earnings retained for reinvestment and stability during weaker markets. Dividend coverage of 1.82 reinforces that distributions are supported by ongoing profitability rather than balance-sheet drawdown.

Leverage is extremely low. Debt-to-EBITDA measures just 0.14, far below common caution thresholds around 2.0. The firm effectively operates with a net-cash-like profile, reducing refinancing risk and enabling dividend continuity during downturns.

The next ex-dividend date is March 16, 2026, with payment scheduled for March 30, 2026.

Future dividend growth is expected to moderate, with a projected 3–5 year growth estimate near 1.44%. However, for income investors, slower growth is acceptable when accompanied by a starting yield above 5% and strong coverage.

The key takeaway: the dividend is not rapidly growing, but it appears exceptionally secure.

4. Valuation: Discounted Multiples Reflect Cyclical Pessimism Rather Than Structural Weakness

Valuation currently embeds a cautious outlook across every major metric.

The forward P/E ratio sits near 9.4x compared with a 10-year median of 14.5x. The EV/EBITDA ratio around 6.0x is near the lower bound of its historical 5.6x–13.9x range and below the 9.1x median.

Sales and book valuation tell the same story. The price-to-sales ratio of 2.87 is close to its 10-year low of 2.59, while price-to-book of 1.91 sits near its historical floor of 1.76 compared with a long-term median of 3.62.

Collectively, these metrics imply the market expects structurally weaker profitability and slower growth indefinitely. Yet returns on capital remain firmly above cost of capital — the defining feature of a durable franchise.

The implied valuation discount appears tied more to industry sentiment toward active managers than to company-specific deterioration. Even analyst targets near $100 only modestly exceed the current price, reflecting near-term caution, but intrinsic value estimates near $121.89 suggest longer-term normalization potential.

For dividend investors, the key observation is this: the yield expansion is a function of valuation compression, not deteriorating payout capacity. When yield increases because fundamentals weaken, risk rises; when yield rises because price falls, expected returns improve.

This situation resembles the latter.

5. Risk Assessment & Capital Structure Considerations

The primary risks are operational rather than financial.

Asset growth has outpaced revenue growth, suggesting capital allocation into lower-fee or less productive segments. Continued fee compression across the asset management industry could further pressure margins. Additionally, insider selling without offsetting purchases may indicate cautious internal sentiment.

Another risk is market sensitivity. As a fee-based manager, revenue depends on market levels and net flows, making earnings cyclical even though the balance sheet remains stable.

However, financial risk is minimal. The company holds sufficient cash to cover debt obligations and maintains strong interest coverage, with high distress-resilience indicators suggesting low bankruptcy probability.

Ownership structure also offers stability. Institutional investors hold roughly 79.8% of shares, while insiders own about 8.4%. Large institutional participation often dampens volatility during downturns.

Liquidity remains adequate with daily trading volume around 1.68 million shares.

In essence, the business faces earnings volatility but not solvency risk — a crucial distinction for dividend sustainability.

Final Assessment

T. Rowe Price represents a classic income opportunity created by cyclical pessimism.

The company’s economics remain strong: returns on capital comfortably exceed the cost of capital, leverage is negligible, and cash generation supports distributions. Earnings growth has slowed, but not disappeared. The dividend grows modestly, yet coverage remains robust.

The market has compressed valuation multiples across P/E, EV/EBITDA, sales, and book value to near historical lows, expanding the yield to above 5%. At the same time, intrinsic value estimates still sit materially above the current share price.

This combination — high yield, conservative payout ratio, strong balance sheet, and discounted valuation — is uncommon among established financial firms.

The investment does not depend on rapid growth. Instead, it relies on stability: stable assets, stable profitability, and stable capital returns. If industry conditions merely normalize rather than improve dramatically, total returns could be driven by dividends plus modest multiple re-rating.

For long-term dividend investors prioritizing reliability over excitement, the stock offers an attractive balance: moderate growth, high income, and low financial risk.

The thesis ultimately hinges on patience. The market is pricing a permanent decline; the fundamentals suggest a cyclical slowdown. When that gap exists, income investors are typically compensated for waiting — and in this case, they are compensated at more than 5% annually.