Dream Office REIT: A High-Yield Office REIT Facing Structural and Financial Headwinds

Persistent profitability challenges and negative economic returns raise concerns about long-term dividend sustainability.

Investment Thesis: Assessing Whether the Current Dividend Yield Adequately Compensates Investors for Structural Earnings Weakness

Dream Office Real Estate Investment Trust operates as a Canadian office-focused REIT specializing in acquiring, managing, and leasing commercial office properties located primarily in major urban markets across Canada. The portfolio is concentrated in central business district and suburban office properties, with the majority of revenue generated from assets located in Ontario, while Alberta contributes a smaller but still meaningful share of rental income. The business model relies heavily on long-term tenant leases to generate rental revenue.

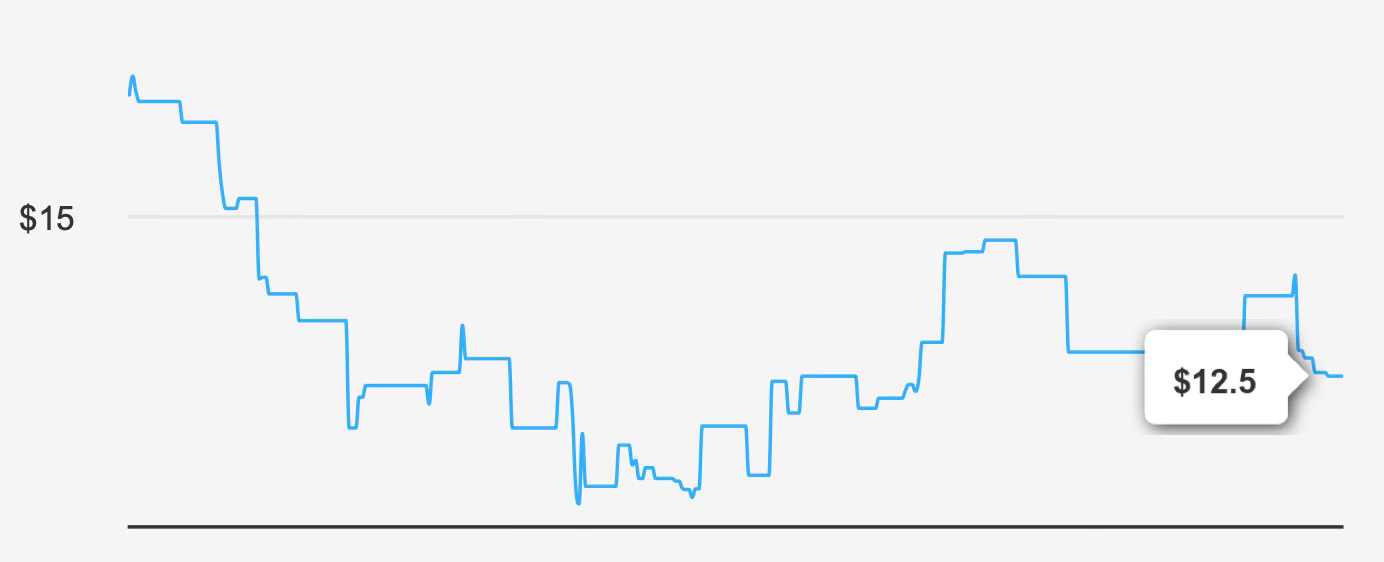

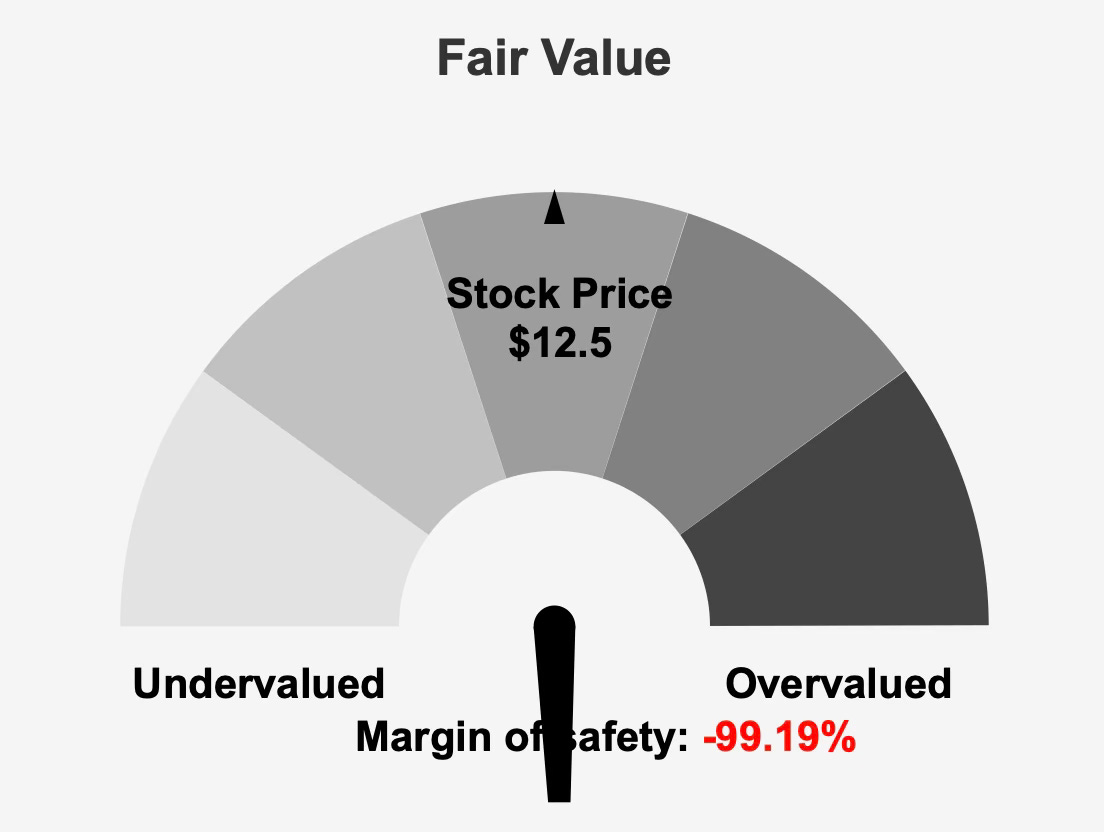

Despite the apparent stability of lease-driven income, the trust’s financial profile reveals persistent operational challenges that undermine the reliability of its dividend proposition. The current share price sits near $12 while the estimated intrinsic value is roughly $6.3, implying a deeply negative margin of safety of about -99.2%. This discrepancy indicates that market pricing remains disconnected from underlying fundamentals, particularly given the company’s weakening earnings trajectory.

Revenue growth has been modest but inconsistent over longer horizons. The company recorded roughly 6.9% annual revenue growth over the past five years, yet the longer ten-year growth rate stands at -3.4%. This contrast highlights how cyclical pressures within the office real estate sector have limited sustained expansion.

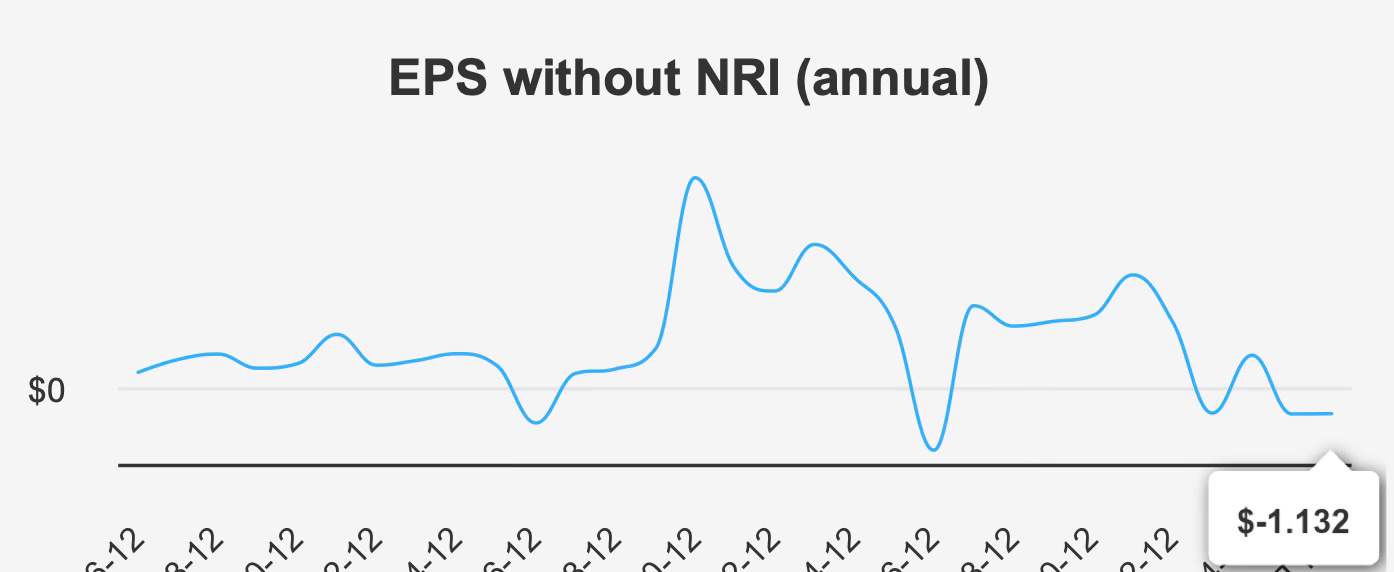

Earnings volatility has further complicated the investment case. In the most recent quarter ending December 31, 2025, earnings per share excluding non-recurring items declined sharply to -$1.05. This represents a significant deterioration from -$0.15 in the previous quarter and a dramatic reversal from the $0.29 reported during the same quarter the prior year. Such swings illustrate the unstable nature of profitability and suggest operating conditions have become increasingly challenging.

Forward projections offer only modest optimism. Analysts expect earnings to recover to roughly $0.96 per share next fiscal year and potentially reach around $1.10 in the following year. Revenue is projected to grow gradually to approximately $132.1 million by 2026 and roughly $139.1 million by 2027. While these forecasts suggest stabilization rather than continued deterioration, the scale of improvement remains relatively modest given the broader structural issues facing office property markets.

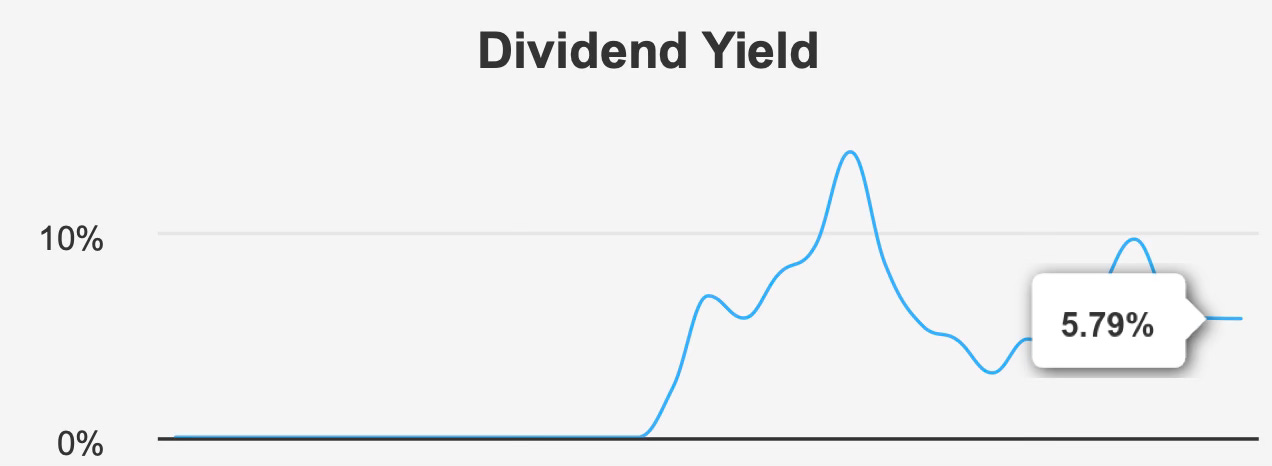

At present, the trust offers a forward dividend yield of approximately 5.8%. For income-oriented investors, this yield may initially appear attractive relative to broader equity markets. However, the sustainability of that income stream ultimately depends on improvements in profitability and capital efficiency. Without meaningful operational recovery, the current dividend yield alone may not adequately compensate for the elevated financial risks embedded in the business model.

Dream Office REIT therefore represents a situation where income potential must be carefully weighed against persistent financial and operational challenges.

Earnings Momentum & Profitability Trends

Recent operating results illustrate a company struggling to generate consistent earnings despite relatively stable operating margins. During the most recent quarter, revenue per share declined slightly to $1.65 compared with $1.69 in the prior quarter. This modest decline suggests that revenue generation remains under pressure.

Profitability metrics reinforce this narrative. Although diluted earnings improved sequentially from -$2.26 in the third quarter of 2025 to -$0.90 in the fourth quarter, the result still represents a deterioration compared with the -$0.69 recorded in the same quarter the previous year. The uneven trajectory reflects ongoing volatility in operating performance.

From a margin perspective, cost management has remained relatively steady. Gross margins currently sit near 54.9%, slightly above the five-year median of roughly 54.1% and close to the ten-year median of 54.7%. This stability suggests that operational cost control has remained relatively disciplined despite the pressures on revenue and earnings.

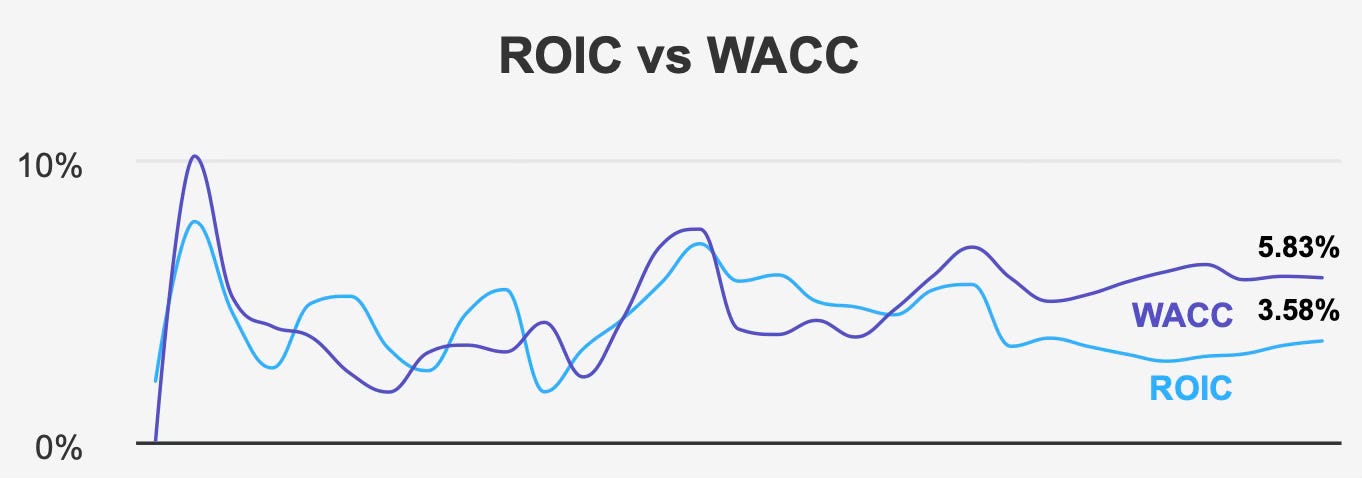

However, stable margins have not translated into meaningful economic profitability. Over the past five years, the company’s median return on invested capital has been approximately 3.1%, which remains well below its weighted average cost of capital of about 5.9%. The current spread continues to reflect this pattern, with ROIC around 3.6% compared with a WACC near 5.8%. This persistent gap indicates that the company has not generated sufficient returns on invested capital to cover its cost of financing.

Return on equity further highlights the company’s profitability challenges. Current ROE stands near -16.2%, reflecting continued losses and inefficient use of shareholder capital. Historical performance has been volatile, with ROE ranging from a high near 11.9% to a low of approximately -30.1%. Such wide fluctuations make it difficult to establish a reliable baseline for future profitability.

Share repurchases have historically provided some support for shareholder value. Over the past decade, the trust reduced its share count by roughly 11.7%. However, recent activity suggests that buybacks have largely paused, with the one-year buyback ratio slightly negative at -0.2%.

Taken together, the data suggests a company capable of maintaining operational stability in certain areas but struggling to convert that stability into consistent profitability.

Dividend Profile & Sustainability

For dividend investors, the central question surrounding Dream Office REIT is whether its distribution remains sustainable given the company’s earnings profile.

The trust currently offers a forward dividend yield of approximately 5.8%, slightly above its long-term median yield of roughly 5.7%. On the surface, this yield appears competitive within the REIT sector.

However, the long-term dividend trend tells a more concerning story. Over the past five years, dividend payments have declined at an annual rate of approximately -14.1%, while the three-year growth rate shows an even steeper decline of about -20.6%. These reductions indicate that management has repeatedly adjusted the payout downward in response to financial pressures.

Historically, the company maintained a payout ratio near 100%, meaning most earnings were distributed to shareholders. Currently, the payout ratio sits at 0%, reflecting the absence of distributable earnings due to ongoing profitability challenges.

Dividend coverage metrics further emphasize the fragility of the current distribution. Coverage currently stands near -8.3, highlighting that earnings do not support the existing payout structure. While the trust continues to distribute dividends on a monthly schedule, the lack of earnings support introduces meaningful uncertainty regarding long-term sustainability.

Forward expectations provide limited reassurance. Dividend growth is projected to remain flat over the next three to five years, suggesting management does not anticipate meaningful increases in distributions.

For income-focused investors, this dynamic presents a clear trade-off: a relatively attractive yield today paired with limited confidence in future dividend growth.

Valuation Analysis: Examining the Disconnect Between Market Pricing and Underlying Economic Fundamentals

Valuation metrics present a mixed picture, with some indicators suggesting asset value while others highlight substantial earnings risk.

Based on current estimates, the trust’s intrinsic value stands near $6.3 per share compared with a market price around $12.5. This gap produces a margin of safety of roughly -99.0%, suggesting the stock trades significantly above its estimated fair value.

Earnings-based valuation multiples also point toward elevated pricing. The forward price-to-earnings ratio currently sits near 13.6x, exceeding the company’s ten-year median multiple of approximately 10.2x. Given the volatility in earnings and uncertain recovery trajectory, this premium multiple appears difficult to justify.

Enterprise value metrics highlight similar concerns. The trailing EV/EBITDA multiple is currently negative at roughly -15.6x, reflecting operational losses rather than positive cash flow generation. Historically, the company’s ten-year median EV/EBITDA multiple has been closer to 10.0x.

In contrast, asset-based valuation measures present a somewhat different perspective. The price-to-book ratio currently sits near 0.3x, well below the long-term median of about 0.7x. Likewise, the price-to-sales ratio stands around 1.8x compared with a historical median of roughly 4.2x.

This divergence between asset-based and earnings-based valuation metrics reflects the central tension in the investment case. While the company’s real estate portfolio may retain considerable asset value, weak earnings generation limits the market’s willingness to assign a higher valuation.

Until the company demonstrates improved profitability and capital efficiency, the apparent asset discount may represent a value trap rather than a compelling opportunity.

Risk Assessment & Capital Structure Considerations

Several financial indicators point to elevated risk within the company’s operating and financial structure.

The company currently reports a Piotroski F-Score of 3, a level typically associated with weak financial quality and limited operational momentum.

Interest coverage remains thin as well. The trust reports an interest coverage ratio of approximately 1.4, well below the commonly cited safety threshold of around 5. This narrow coverage suggests limited financial flexibility in servicing debt obligations during periods of operational weakness.

Credit risk indicators further reinforce these concerns. The company’s Altman Z-Score stands near -0.62, placing it within the financial distress zone and indicating an elevated probability of financial difficulty within the next two years.

Ownership structure also presents some unusual characteristics. Insider ownership currently stands at 0%, meaning directors and management hold no direct equity stake in the trust. Institutional ownership sits near 6.9%, indicating limited but notable participation from institutional investors.

Liquidity conditions appear relatively stable in the near term. Daily trading volume has increased to roughly 7,354 shares compared with a two-month average of about 4,078 shares, suggesting heightened investor interest. Additionally, a dark pool index near 45% indicates that a significant portion of trading occurs through private exchanges, potentially reflecting institutional positioning or hedging activity.

Although the Beneish M-Score suggests a low probability of earnings manipulation, the broader set of financial indicators continues to highlight structural vulnerabilities.

Final Assessment

Dream Office REIT represents a complex investment case combining an attractive headline dividend yield with meaningful operational and financial challenges.

On the positive side, the trust maintains a portfolio of office assets concentrated in major Canadian urban markets and continues to generate stable gross margins near 55%. Revenue forecasts also suggest modest expansion through 2027, indicating that the business may stabilize over the medium term.

However, these strengths are overshadowed by persistent profitability concerns. Negative economic returns, volatile earnings, declining dividends, and weak balance-sheet metrics collectively raise questions about the long-term sustainability of the company’s current strategy.

Valuation further complicates the picture. Although asset-based measures suggest the stock trades below the historical value of its real estate portfolio, earnings-based indicators and intrinsic value estimates imply the shares remain significantly overvalued relative to the company’s current financial performance.

For dividend investors, the central risk lies in the disconnect between the current yield and the company’s underlying earnings capacity. Without a meaningful recovery in profitability and capital efficiency, maintaining the existing dividend could prove difficult.

In its current form, Dream Office REIT appears better suited for speculative investors anticipating a turnaround in office real estate fundamentals rather than conservative income investors seeking stable and growing dividend income.