Dream Industrial REIT: A High-Yield Industrial Property Portfolio Trading at a Modest Discount

Evaluating the Stability, Valuation Support, and Dividend Sustainability of a Global Industrial Real Estate Platform

Investment Thesis: A Globally Diversified Industrial REIT Offering Income Stability With Moderate Valuation Upside

Dream Industrial Real Estate Investment Trust operates a geographically diversified portfolio of industrial properties across Canada, Europe, and the United States. The trust’s core objective is to expand its logistics and industrial real estate footprint while delivering stable and sustainable cash distributions to unitholders.

The portfolio is diversified across several key operating regions including Ontario, Quebec, Western Canada, Europe, and the United States, along with joint venture platforms focused on development and strategic investments. This geographic mix provides exposure to multiple industrial markets and tenant bases, helping reduce concentration risk within any single region.

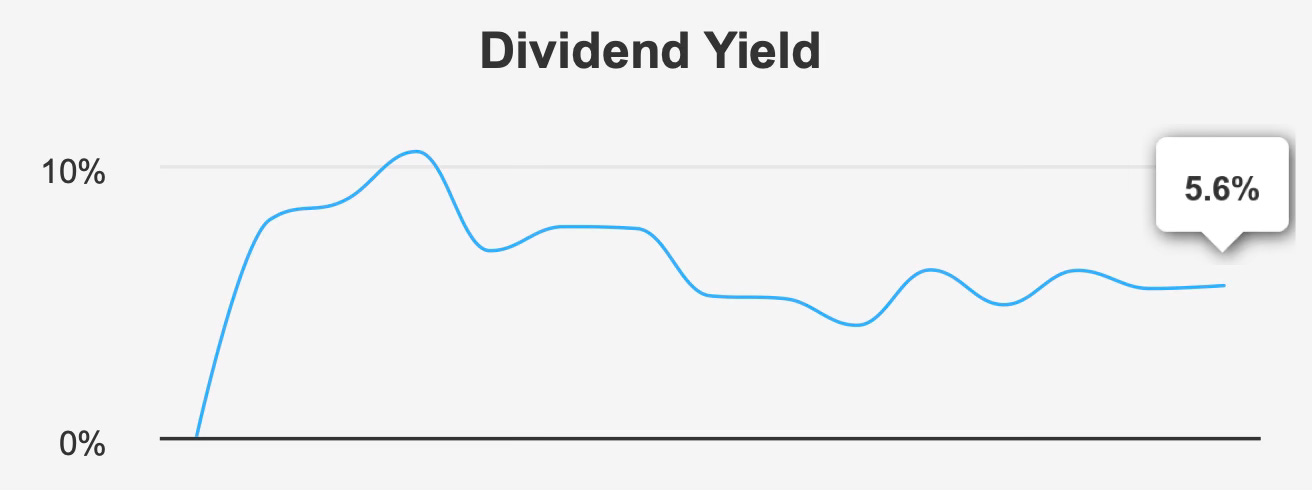

From an income-investor perspective, the trust’s primary appeal lies in its dividend yield, currently around 5.6%. Within the REIT sector, this places the company comfortably in the upper range of income-generating securities while still maintaining a reasonable balance between yield and financial stability. The company distributes dividends monthly, which adds an additional layer of appeal for investors seeking predictable and frequent income streams.

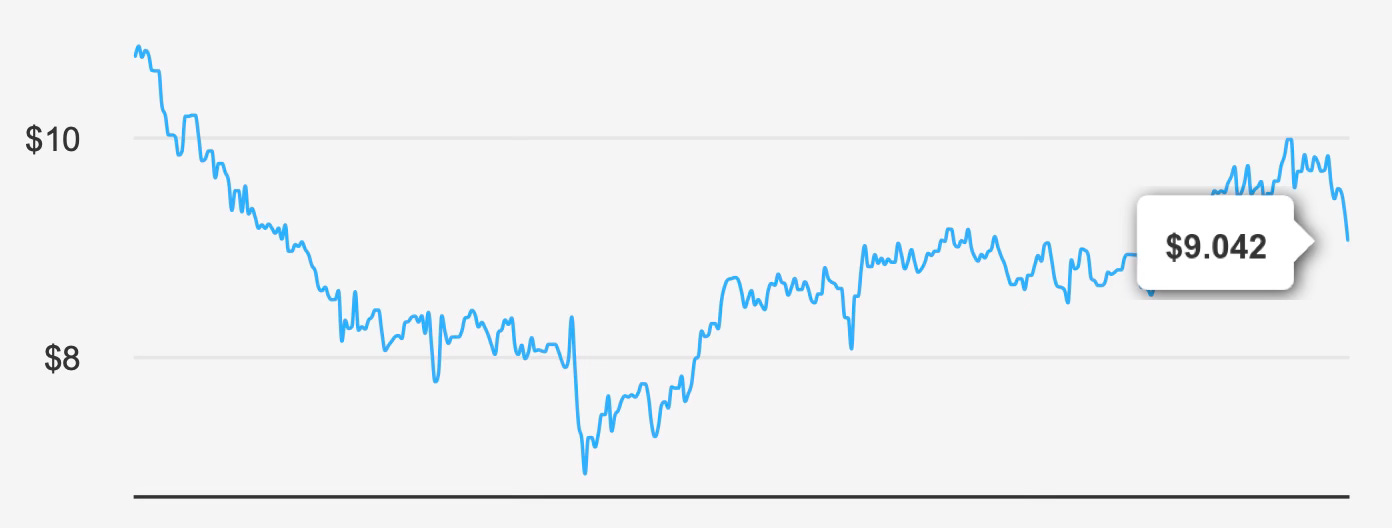

At a share price close to $9, the stock trades modestly below its estimated intrinsic value of approximately $10.14. This represents a margin of safety of roughly 10.8%. While this discount is not especially large, it does provide some valuation support for investors entering the position at current levels.

Operationally, the trust has demonstrated moderate long-term earnings expansion. Over the past five and ten years, earnings per share have grown at approximately 6.0% and 5.6% annually, respectively. These figures reflect the relatively steady, asset-driven growth profile typical of industrial REITs, where income expansion is generally driven by rent increases, portfolio acquisitions, and development projects.

However, the investment case is not without challenges. Capital efficiency remains a concern, as the company’s returns on invested capital have consistently trailed its cost of capital. In addition, dividend growth has remained stagnant in recent years, suggesting that management has focused on maintaining distributions rather than expanding them.

Overall, Dream Industrial REIT offers a balanced but somewhat cautious investment profile. Investors are presented with a diversified industrial property portfolio, a stable income stream, and modest valuation support. At the same time, elevated leverage and limited dividend growth mean that the investment thesis relies more on income stability than on strong long-term growth.

For long-term dividend investors, the central question is whether the trust can sustain its current payout while gradually improving operational performance and capital efficiency.

Earnings Momentum & Profitability Trends

Dream Industrial REIT’s recent financial performance reflects both the stability typical of industrial property portfolios and the financial pressures that often accompany leveraged real estate structures.

In the fourth quarter of 2025, earnings excluding non-recurring items reached $0.181 per share. This represented an improvement from $0.167 in the previous quarter but remained below the $0.199 reported during the same period the year before. The sequential improvement suggests some stabilization in operating conditions, though the year-over-year decline highlights ongoing pressure on profitability.

Diluted earnings per share showed greater volatility, declining to $0.073 compared with $0.113 in the prior quarter and $0.266 in the same quarter of the previous year. While accounting adjustments and non-recurring factors often influence REIT earnings metrics, the magnitude of the decline illustrates how sensitive reported earnings can be to valuation changes and financing costs.

Revenue performance has been more encouraging. Revenue per share increased to $0.324 during the quarter, rising from $0.312 in the previous quarter and $0.288 in the same quarter last year. This gradual upward trajectory indicates that the underlying property portfolio continues to generate steady rental income growth.

Margins remain one of the company’s stronger operational characteristics. Gross margin reached approximately 76.4% during the quarter, closely aligned with its five-year median of about 76.2% and approaching the company’s historical high near 76.4%. Such consistency highlights the efficiency of the company’s property operations and the relatively predictable cost structure associated with industrial real estate assets.

Capital allocation has also played a role in supporting per-share performance. Over the past year, the company repurchased roughly 1.1% of its outstanding shares. Over a five-year period, share buybacks have reduced the share count by approximately 10.3%. Although share repurchases are not typically the primary capital allocation tool for REITs, this gradual reduction in outstanding shares has helped support earnings per share.

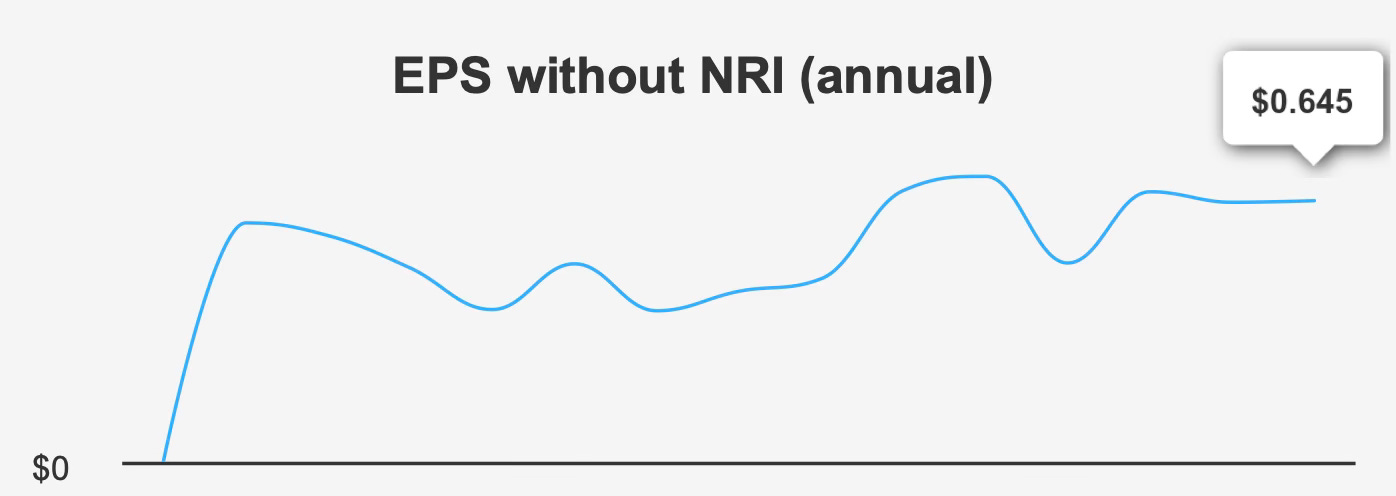

Looking ahead, revenue growth expectations remain positive. Forecasts suggest revenue of approximately $396.1 million in 2026, increasing to about $422.8 million in 2027. Earnings estimates follow a similar trend, with projected EPS of $0.784 and $0.821 over the same period.

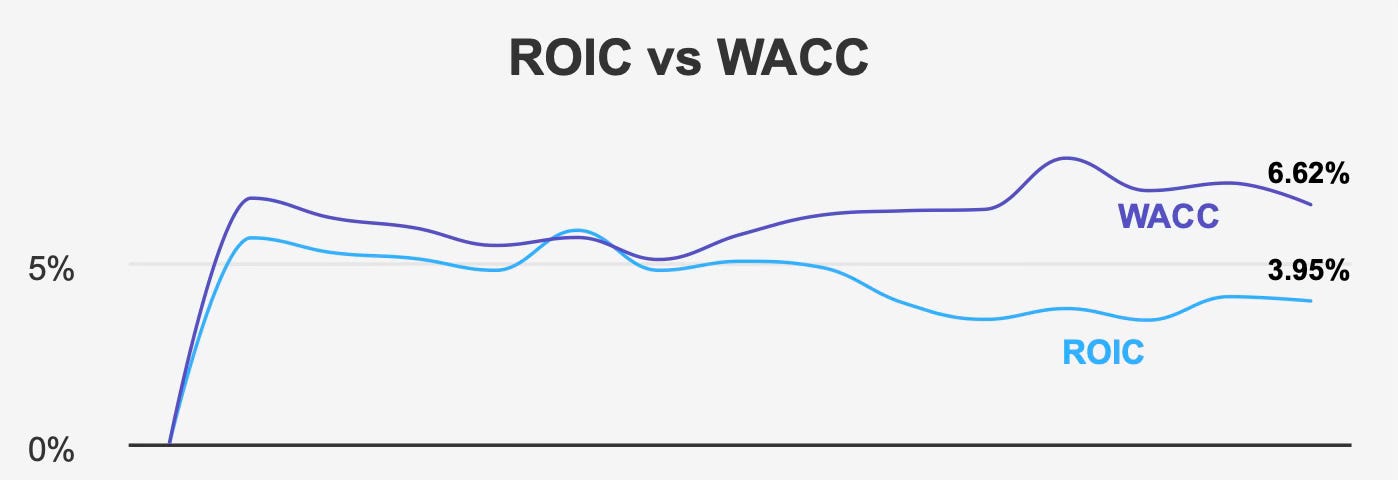

Despite these projections, the company’s broader profitability metrics highlight structural inefficiencies. Return on invested capital currently stands near 3.9%, while the company’s weighted average cost of capital is roughly 6.6%. This means that the business is not generating returns sufficient to fully cover its capital costs.

Historically, this gap has persisted. The company’s five-year median ROIC of roughly 3.7% also falls well below the five-year median WACC of about 7.0%. Even the company’s ten-year peak ROIC of 5.8% has remained below its cost of capital.

This persistent gap suggests that while the company’s assets generate reliable rental income, the broader investment structure has struggled to produce economic value above financing costs.

Dividend Profile & Sustainability

For most investors evaluating Dream Industrial REIT, the dividend represents the core element of the investment case.

The trust currently offers a forward dividend yield of approximately 5.6%, making it an attractive option for income-oriented investors within the REIT sector. Although the yield is slightly below its ten-year median of about 5.8%, it remains broadly consistent with the company’s historical income profile.

However, the company’s dividend growth record is notably stagnant. Over both three-year and five-year periods, dividend growth has remained at 0%. This indicates that management has prioritized maintaining a stable distribution rather than increasing payouts.

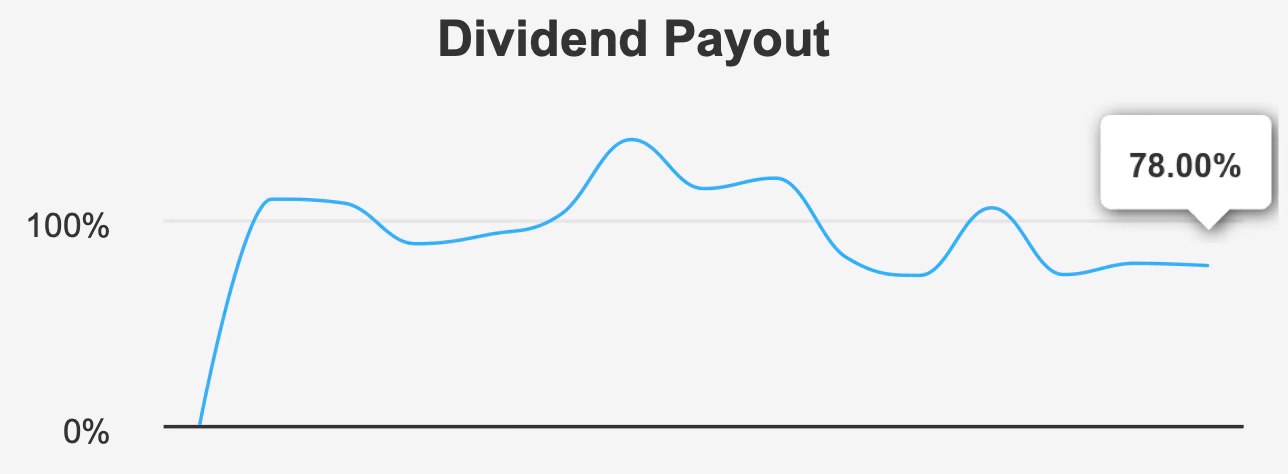

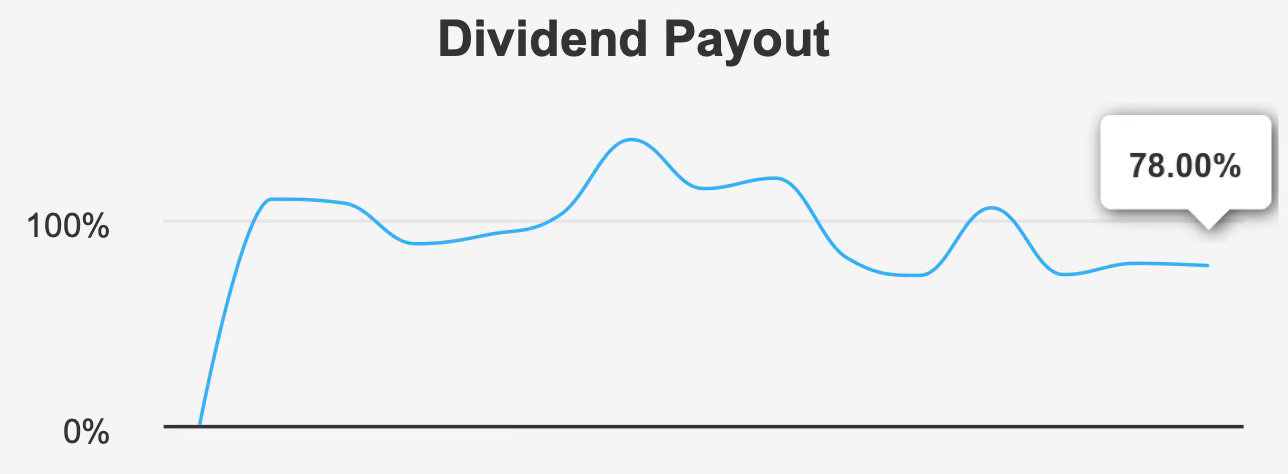

Dividend sustainability can be evaluated through payout metrics. The current dividend payout ratio stands near 78%. While this is below the company’s historical peak of roughly 101%, it still represents a significant portion of earnings being distributed to shareholders.

Dividend coverage currently sits around 0.82, indicating that earnings still support the dividend but leave limited margin for error if operating performance weakens. For REITs, elevated payout ratios are common due to regulatory requirements, but high payout levels inevitably reduce flexibility for future dividend increases.

Looking forward, expectations for dividend growth remain minimal. Current projections indicate a future dividend growth rate of 0%, suggesting that investors should not expect meaningful distribution increases in the near term.

Despite this stagnation, several factors help support dividend stability. Industrial real estate demand has historically remained resilient due to ongoing logistics and supply chain needs. Additionally, the company’s geographically diversified property portfolio reduces reliance on any single market.

However, leverage remains an important consideration. With significant debt obligations, maintaining stable operating income is essential to sustaining both dividend payments and financial obligations.

Overall, the dividend appears relatively secure in the near term but offers limited prospects for growth.

Valuation Analysis: Measuring Whether the Current Discount Provides Adequate Compensation for Structural Risks

Dream Industrial REIT’s valuation presents a somewhat balanced picture. Several metrics suggest modest undervaluation, while others indicate that certain elements of the company’s risk profile are already reflected in the share price.

The trust’s estimated intrinsic value stands at approximately $10.14 per share, compared with a current market price near $9.04. This difference represents a margin of safety of roughly 10.8%, suggesting the stock may be modestly undervalued.

From an earnings perspective, the stock trades at approximately 21.8x trailing earnings. Although this multiple appears elevated compared with many traditional industries, REIT valuation analysis typically places greater emphasis on forward earnings expectations.

On that basis, the forward P/E ratio of roughly 11.5x appears far more attractive and sits close to the company’s ten-year median of approximately 12.3x. This alignment suggests the market expects earnings growth to gradually normalize the valuation.

Revenue-based valuation also appears reasonable. The price-to-sales ratio stands near 7.1x, slightly below the company’s historical median of roughly 7.9x. This modest discount suggests the market is assigning a somewhat lower valuation relative to revenue than in previous years.

Asset-based valuation metrics provide further support. The price-to-book ratio sits around 0.8x, below the company’s long-term median of approximately 0.9x. This indicates that the stock is trading at a discount relative to the book value of its underlying assets.

Cash-flow valuation also appears favorable. The price-to-free-cash-flow ratio stands near 15.9x, below the ten-year median of approximately 18.1x. This suggests that investors are paying a somewhat lower price for each dollar of free cash flow than they historically have.

However, not all valuation indicators point toward undervaluation. The enterprise value to EBITDA ratio currently sits around 26.3x, which is significantly higher than the company’s ten-year median of roughly 18.0x. This elevated multiple may reflect the influence of leverage and capital structure rather than purely operational performance.

Taken together, the valuation landscape appears moderately supportive but not deeply discounted. Investors receive a modest margin of safety and reasonable pricing relative to assets and cash flow, though leverage and capital efficiency concerns temper the attractiveness of the opportunity.

Risk Assessment & Capital Structure Considerations

Dream Industrial REIT carries a moderate risk profile, largely driven by leverage and capital efficiency challenges.

The most prominent concern is the company’s debt burden. The debt-to-EBITDA ratio currently stands at approximately 12.1x, well above the commonly cited threshold of about 4.0x that many analysts consider conservative for real estate companies. Such elevated leverage increases the company’s sensitivity to interest rate changes and economic cycles.

Over the past three years, the company has increased long-term debt by roughly CAD 651.7 million. While debt financing is standard within the REIT sector, sustained increases in leverage require corresponding improvements in earnings to maintain financial stability.

Capital efficiency remains another area of concern. As previously discussed, the company’s return on invested capital continues to fall below its cost of capital, indicating that investments have not consistently produced returns sufficient to justify their financing costs.

Operational trends also highlight potential inefficiencies. The company’s assets have grown at an annual rate of approximately 17.8%, significantly faster than revenue growth of around 5%. While asset expansion may support future income generation, this imbalance suggests that newly deployed capital has not yet translated into proportional revenue growth.

Financial stability metrics also raise caution. The company’s Altman Z-score sits near 1.0, which indicates a relatively elevated level of financial risk compared with stronger balance sheets.

Ownership dynamics provide additional context. Insider ownership currently stands at essentially 0%, while institutional ownership is relatively low at around 4%. The limited presence of both insiders and institutional investors may reflect restrained confidence in the company’s long-term performance.

Liquidity conditions also appear somewhat constrained. Recent trading volume of roughly 1,958 shares is significantly below the two-month average daily volume of approximately 37,185 shares. Lower liquidity can result in wider bid-ask spreads and increased price volatility.

Taken together, these factors suggest that while the company’s operations remain stable, the financial structure introduces a higher level of risk than many investors might expect from a traditional income-focused REIT.

Final Assessment

Dream Industrial Real Estate Investment Trust represents a classic income-oriented REIT investment built around a diversified portfolio of industrial properties and a stable dividend distribution.

The company offers a dividend yield of approximately 5.6%, supported by relatively consistent operating margins and gradual revenue growth. The stock also trades modestly below its estimated intrinsic value, providing some degree of valuation support.

However, the investment profile is shaped by several structural challenges. Capital returns remain below the cost of capital, leverage levels are elevated, and dividend growth has effectively stalled. These factors suggest that the company’s appeal lies primarily in income stability rather than long-term growth.

For investors focused on dependable yield, Dream Industrial REIT may represent a reasonable addition to an income-oriented portfolio. The combination of a stable industrial real estate portfolio and a competitive dividend yield provides a reliable income stream.

At the same time, long-term performance will likely depend on management’s ability to improve capital efficiency, moderate leverage, and translate asset growth into stronger earnings expansion.

In its current form, Dream Industrial REIT appears best suited for investors seeking stable income with moderate valuation support rather than those pursuing aggressive growth or rapidly expanding dividends.