Cyclical Strength, Structural Discipline: Evaluating Nucor as a Dividend Holding

Strong balance sheet and conservative payout offset by cyclical profitability pressures

Nucor Corporation (NUE) Dividend Stock Analysis

1. Investment Thesis: A Financially Strong Steel Producer Offering Income Stability but Limited Growth Upside at Current Valuation

Nucor NUE 0.00%↑ occupies a distinctive position within the steel industry. Unlike traditional integrated producers, it relies primarily on electric arc furnaces using scrap steel, a structure that historically provides cost flexibility and balance sheet resilience during downturns. The company’s operations span steel mills, finished steel products, and raw materials, supplying manufacturers and fabricators across North America.

This operating model has allowed Nucor to build a reputation not for peak profitability, but for survivability across cycles. That distinction matters for dividend investors. Steel is structurally cyclical, yet Nucor has historically mitigated volatility through conservative leverage, disciplined capital allocation, and consistent shareholder returns.

At present, however, the investment case splits into two different time horizons.

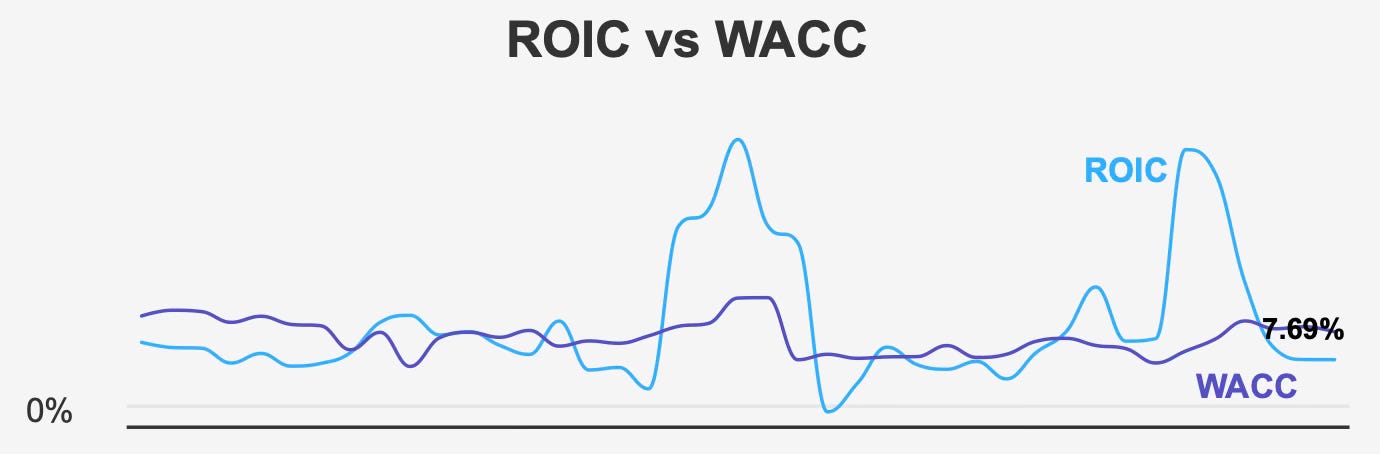

Over the long term, the company has demonstrated strong capital efficiency. Its five-year median return on invested capital of 20.7% materially exceeded its 12.9% cost of capital, confirming a business capable of creating value during favorable cycles. Recently, though, the economic picture has shifted. Current ROIC has declined to 7.7%, now below the 12.3% cost of capital. The company remains profitable, but it is no longer generating excess economic returns.

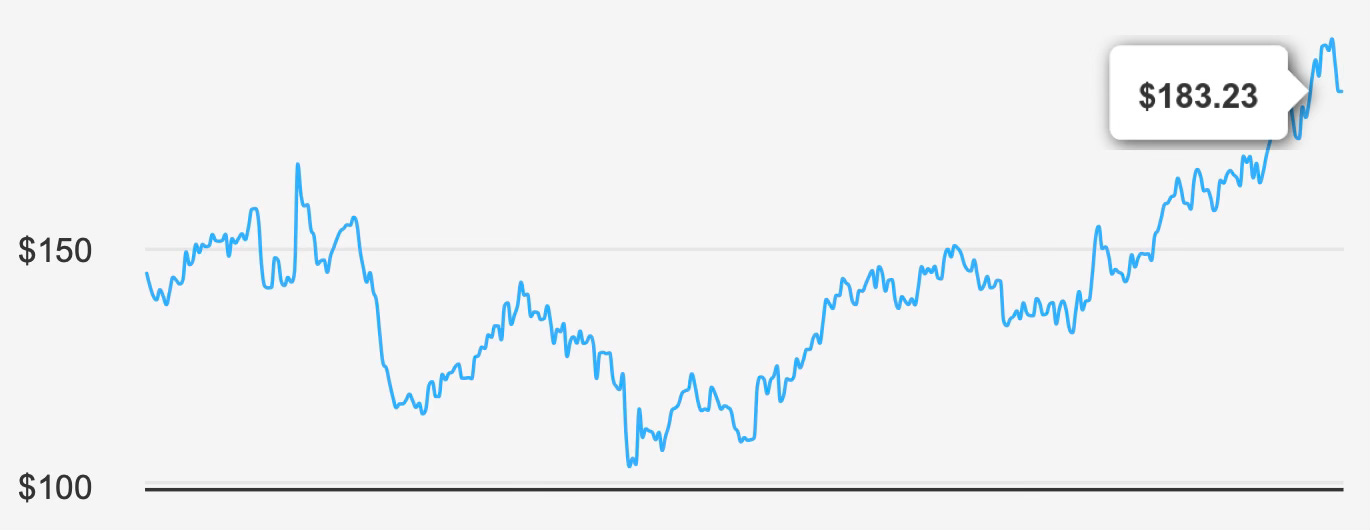

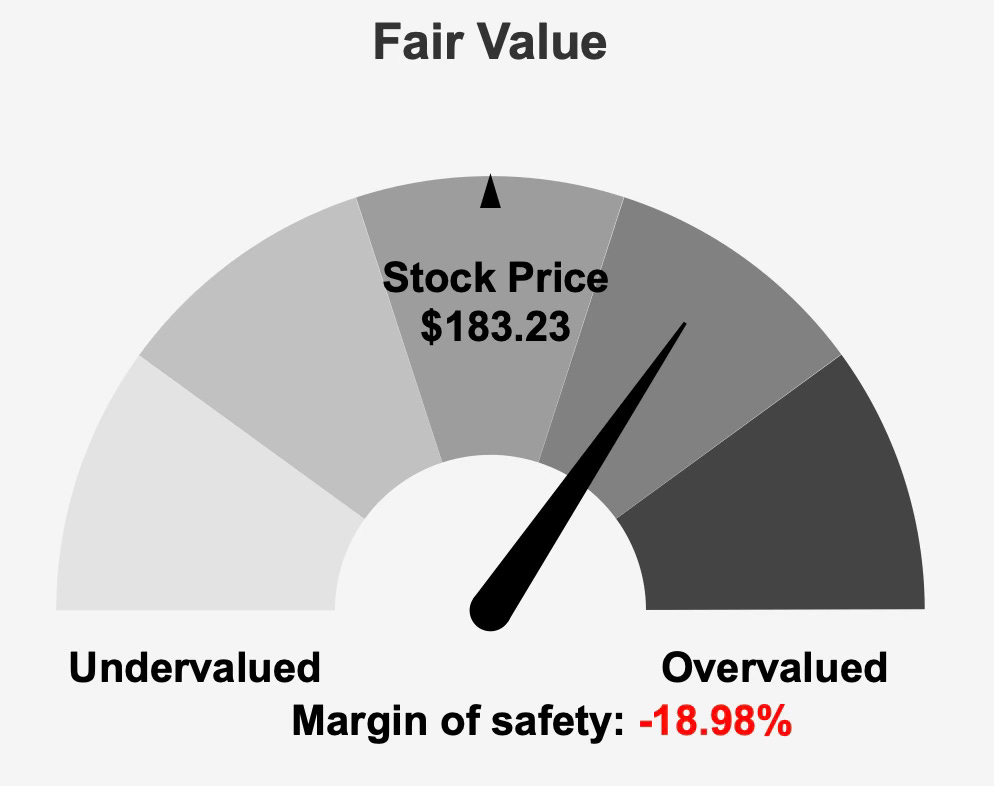

That change does not threaten solvency or dividend payments. It does, however, alter expected shareholder returns. Cyclical businesses typically command lower valuations when returns compress, yet the stock currently trades around $183 compared with an intrinsic value estimate of $154, leaving nearly a 19% negative margin of safety.

The investment implication is clear: Nucor remains a dependable dividend payer, but the stock price already assumes stronger profitability than current operating conditions justify. Investors are buying stability rather than growth — and paying a premium for it.

2. Earnings Momentum & Profitability Trends

Recent quarterly results show mixed operating performance. Earnings per share reached $1.73 in the latest quarter, rising 16.1% sequentially and 41.8% year-over-year. At first glance, the growth appears strong.

However, the improvement reflects recovery within a cyclical trough rather than sustained expansion. Revenue per share actually declined to $33.48 from $37.02 the prior quarter, suggesting price or volume pressure despite improving efficiency.

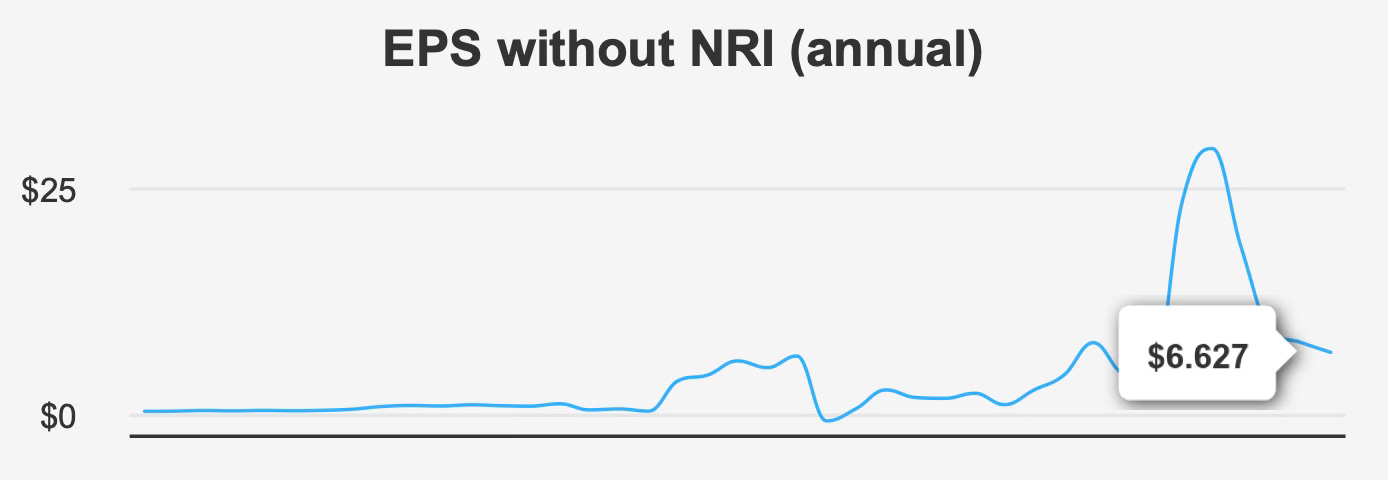

The longer-term earnings record confirms the cyclical nature of the business. Over five years, annual EPS growth has been essentially flat at 0.4% annually, while the ten-year rate stands at 25.4%. The difference illustrates how steel profitability clusters in favorable economic environments and fades during weaker demand periods.

Margin behavior reinforces this interpretation. Gross margin recently measured 11.9%, well below its five-year median of 22.5% and far from the historical high above 30%. Nucor is still profitable, but the economics of the cycle have clearly softened.

Capital returns reflect the same pattern. Return on equity has fallen to 8.5% compared with historical peaks above 55%. When ROIC simultaneously drops below the cost of capital, the company transitions from value creation to value preservation. This is typical late-cycle behavior for commodity producers.

Management continues to offset cyclicality through share repurchases. Over the past year, the company retired roughly 1.7% of shares outstanding, while the decade-long average reduction reaches about 3.7% annually. Buybacks in this context are less about financial engineering and more about stabilizing per-share results during weaker pricing periods.

Forward expectations remain constructive but modest. Analysts forecast earnings of $12.00 next year and $13.25 the following year, alongside revenue projections approaching $38.1 billion by 2028. These estimates imply gradual normalization rather than a new supercycle.

Overall, operating performance does not indicate structural deterioration. Instead, it reflects a business moving through the down portion of a familiar commodity cycle — a key consideration when evaluating dividend durability versus growth potential.

3. Dividend Profile & Sustainability

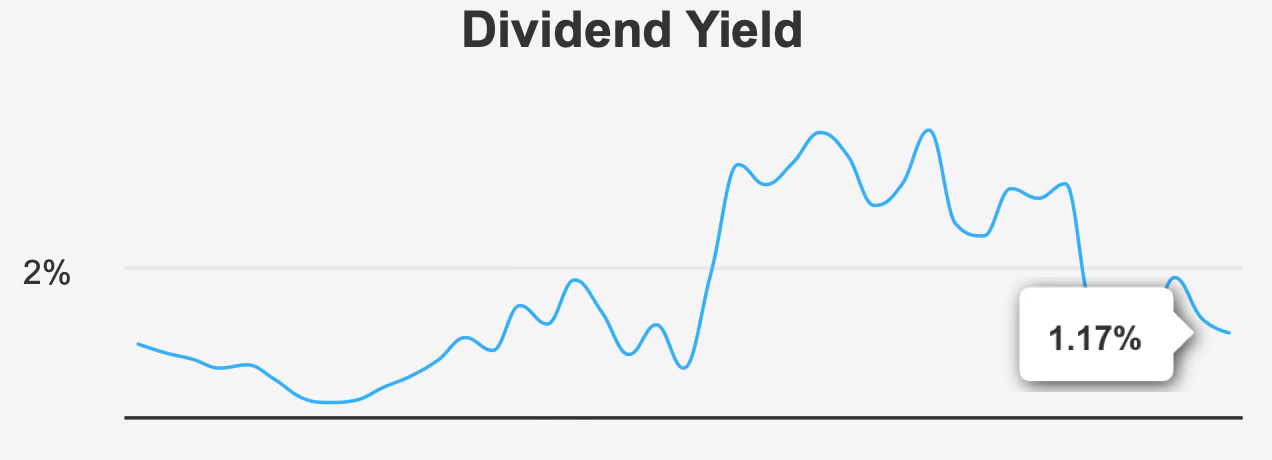

Nucor’s dividend policy emphasizes reliability rather than rapid expansion. The forward yield currently sits near 1.17%, toward the low end of its historical range of roughly 1.0% to 5.2%. The yield appears modest, but its stability carries more importance than its size.

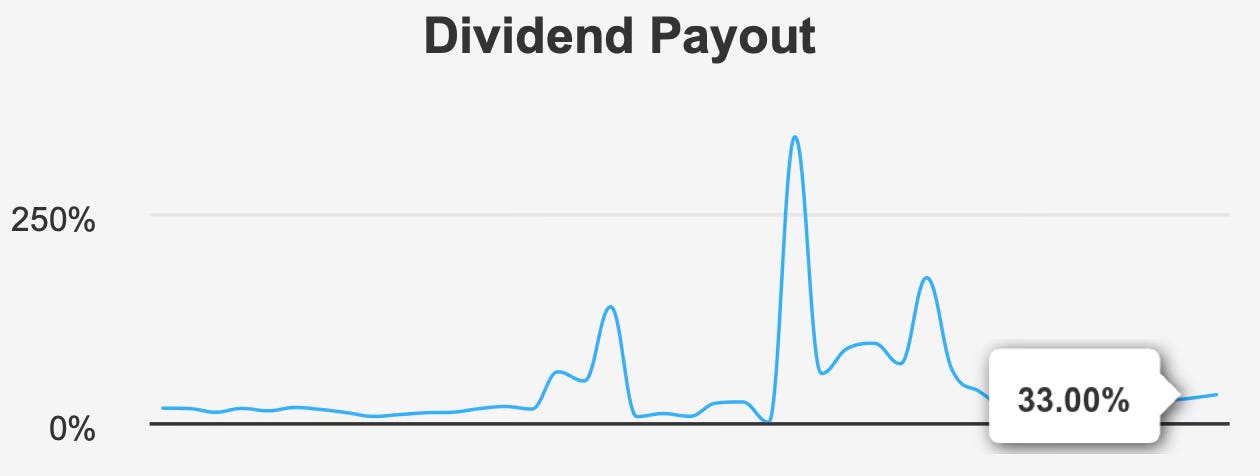

The payout ratio of 33% provides substantial coverage. Earnings exceed dividends by more than three times, resulting in a coverage ratio of 3.41x. Even under materially weaker profitability, the company would likely maintain the distribution.

Recent increases demonstrate cautious consistency. The quarterly dividend rose from $0.55 to $0.56 per share, extending a pattern of gradual adjustments rather than aggressive hikes. Over five years, dividend growth averaged 6.8%, while the three-year rate slowed to 3.2%, indicating moderation aligned with current profitability conditions.

Looking forward, projected dividend growth falls further to roughly 1.24% annually over the next three to five years. Management appears focused on preserving flexibility until returns on capital improve.

Balance sheet strength supports this approach. Debt-to-EBITDA of 1.72 remains comfortably below levels typically associated with cyclical distress. The company retains borrowing capacity while maintaining conservative leverage — an important safeguard in a commodity industry.

The most recent ex-dividend date was December 31, 2025, with payment on February 11, 2026. The next is expected around March 31, 2026, continuing the regular quarterly schedule.

Taken together, the dividend is not designed to deliver high income today nor rapid income growth tomorrow. Instead, it functions as a durable baseline return, supported by conservative financial management across economic cycles.

4. Valuation: Market Pricing Reflects Mid-Cycle Optimism Despite Weaker Current Capital Returns

Valuation currently represents the central challenge in the investment case.

The stock trades near $183 compared with an intrinsic value estimate of $154, implying investors are paying almost one-fifth above estimated fair value. For cyclical companies, the margin of safety typically compensates for earnings variability. Here, that buffer is absent.

Earnings multiples reinforce the concern. The trailing P/E of 24.3x stands well above the ten-year median of 12.9x. Even the forward multiple of 15.2x remains elevated relative to historical norms, suggesting the market anticipates improved profitability.

Enterprise valuation tells a similar story. EV/EBITDA of 11.5x exceeds the decade median of 7.3x, implying expectations of stronger operating conditions ahead.

The price-to-book ratio near 2x appears more reasonable, aligning with long-term averages, but book value in commodity industries often understates cyclical earnings power, making earnings-based multiples more informative.

Analyst price targets around $176 sit slightly below the current share price, reinforcing the notion that optimism is already reflected in the market.

In short, investors are paying for recovery before it fully materializes. That does not make the stock unsuitable for ownership — but it does compress future return potential, particularly for income-focused buyers relying on reinvested dividends.

5. Risk Assessment & Capital Structure Considerations

Financial risk remains low. The Altman Z-score of 4.7 indicates minimal bankruptcy risk, and accounting quality metrics suggest a low probability of earnings manipulation.

Operational risks, however, are cyclical rather than financial. Both gross and operating margins have been declining annually by roughly 6.5% and 8.6%, respectively. Simultaneously, returns on capital have slipped below the cost of capital, indicating weaker economic profitability.

Insider behavior also warrants attention. Over the past year, insiders executed 17 sales without purchases, while ownership remains modest at 2.2%. Institutional ownership of 77.6% suggests the shareholder base is dominated by professional investors whose expectations may shift quickly with steel pricing.

Liquidity remains strong, with daily trading volume around 2.4 million shares, exceeding the two-month average of 1.8 million. A dark pool index above 60% indicates significant institutional participation, which can stabilize pricing but also amplify moves when sentiment changes.

Government contract revenue has declined materially since 2020 with only partial recovery expected, while patent activity shows modest fluctuations rather than sustained expansion. These factors suggest stable operations rather than accelerating innovation — consistent with a mature industrial company.

Overall risk is therefore not solvency-related. It is valuation-cycle risk: the possibility that profitability weakens while the market still prices mid-cycle earnings.

Final Assessment

Nucor represents a disciplined operator in a volatile industry. Its conservative leverage, strong dividend coverage, and history of surviving steel downturns make the distribution dependable even when profitability compresses.

However, the investment appeal depends heavily on entry price. Current valuation implies normalized profitability despite declining margins and returns on capital below the cost of capital. That disconnect limits expected total returns.

The dividend itself appears secure. Growth, however, is likely to remain slow until economic returns recover meaningfully.

For existing shareholders, the stock offers stable income backed by financial strength. For new investors, the absence of a margin of safety reduces attractiveness despite the company’s quality.

Nucor today is best viewed not as a growth dividend stock but as a defensive industrial income holding — reliable, disciplined, and presently priced for better conditions than currently exist.