CT Real Estate Investment Trust: Reliable Yield With Limited Upside

A deep dive into earnings durability, dividend sustainability, and valuation dynamics

Investment Thesis: Stable Income From a Retail-Anchored Property Portfolio With Limited Long-Term Growth Potential

CT Real Estate Investment Trust operates as a Canadian retail-focused REIT with a portfolio primarily anchored by Canadian Tire retail locations. The structure provides unusually stable occupancy and rental income, as a large share of its properties are leased to Canadian Tire Corporation. This relationship creates a dependable base of cash flows that supports the trust’s consistent dividend distribution and income-oriented investor appeal.

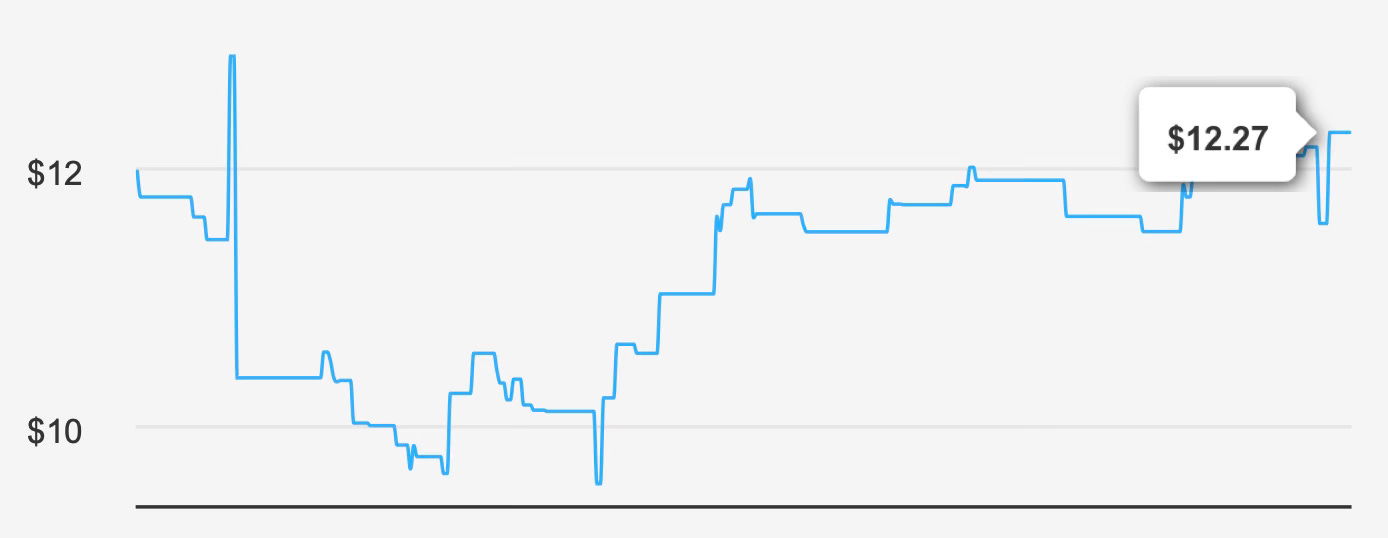

At a market price of roughly $12 with a market capitalization of approximately $3.02B, the trust currently offers a forward dividend yield of about 5.7%. For investors seeking dependable income from real estate assets, this yield sits comfortably above many traditional equity income alternatives. However, the income story is balanced by relatively modest growth prospects. Over the past five years, overall company growth has been measured, with revenue expanding at roughly 3.0% annually and broader growth averaging around 3.4%.

The trust’s underlying business model is intentionally conservative. By focusing on retail properties tied to a strong anchor tenant, the company reduces vacancy risk and creates predictable leasing income. This strategy has historically supported steady earnings and dividend payments, though it also constrains expansion potential compared with more diversified or development-focused REITs.

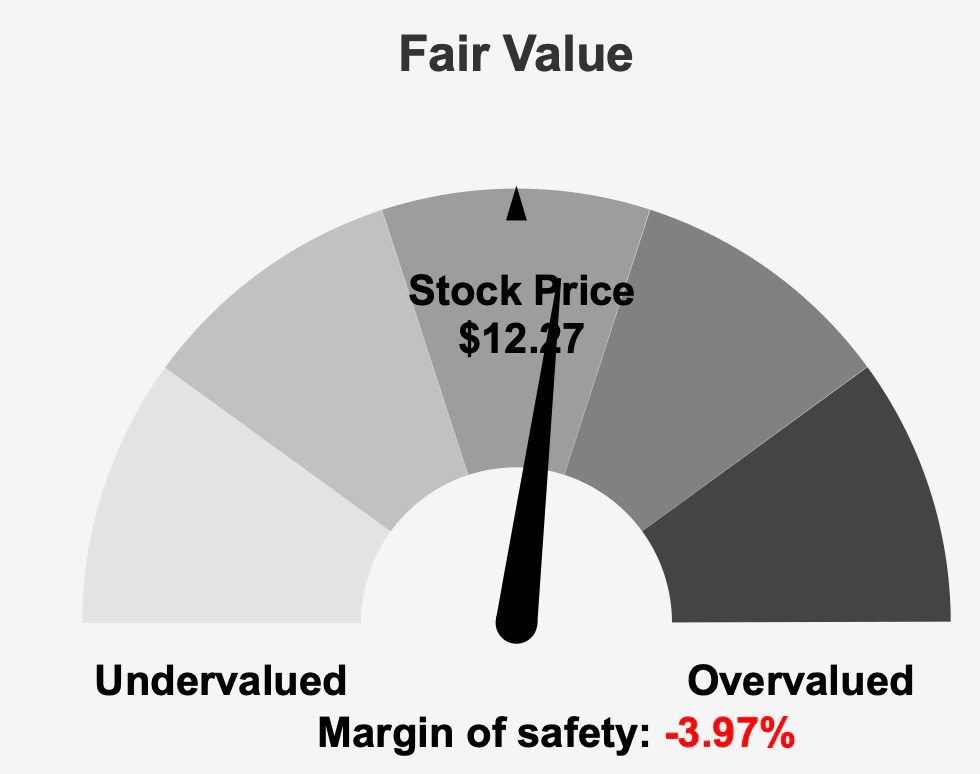

From a valuation standpoint, the stock appears roughly aligned with its estimated intrinsic value of about $11.8, leaving only a slight negative margin of safety near 4%. In other words, the market currently prices the shares close to fair value, suggesting limited room for valuation expansion unless earnings growth accelerates.

For long-term dividend investors, the investment case therefore centers on income reliability rather than capital appreciation. CT REIT offers a stable yield backed by long-term leases and a predictable tenant base, but moderate growth, capital efficiency concerns, and a high payout ratio may limit future dividend expansion.

The result is a profile that appeals primarily to investors seeking steady income rather than those pursuing aggressive dividend growth or strong valuation upside.

Earnings Momentum and Profitability Trends

Recent financial results illustrate the trust’s pattern of gradual earnings expansion combined with steady operating performance. In the quarter ending December 31, 2025, earnings per share excluding non-recurring items reached $0.256, improving from $0.23 in the prior quarter and $0.222 in the same quarter a year earlier. This sequential and year-over-year improvement suggests modest operational momentum.

Diluted earnings per share rose even more sharply to $0.461 from $0.299 in the previous quarter. Although part of this increase reflects accounting adjustments or non-recurring elements, it still indicates that the underlying property portfolio continues to generate healthy cash flow.

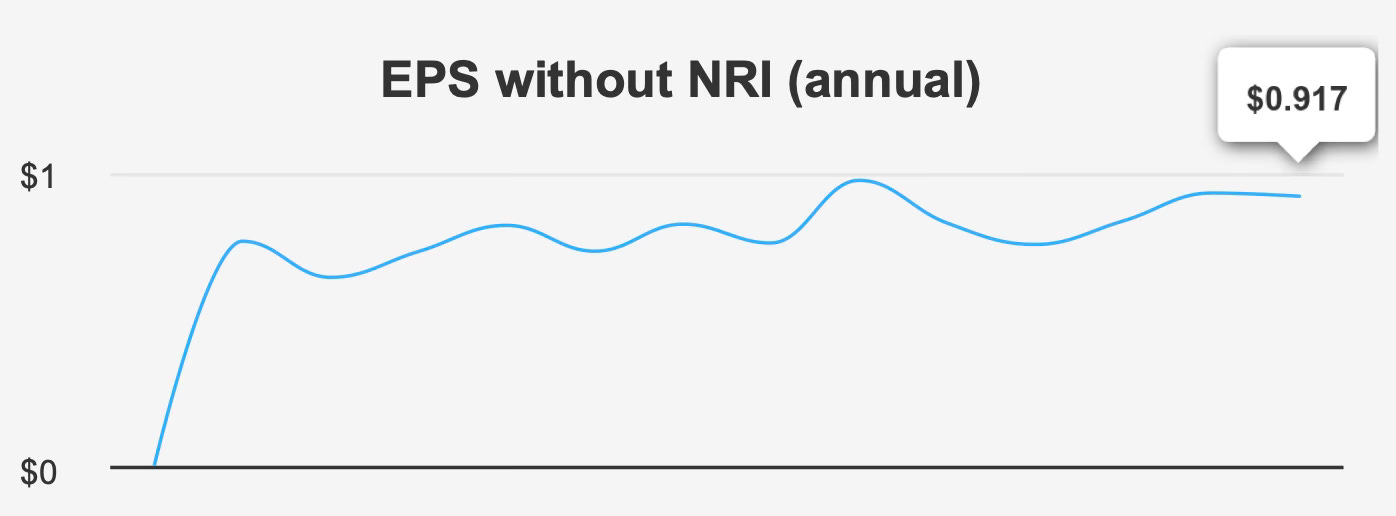

Over longer periods, however, earnings growth has remained modest. The trust’s annual EPS excluding non-recurring items has grown at a compound annual rate of roughly 3.3% over the past five years and about 2.8% over the past decade. Such growth is consistent with mature REIT portfolios where rent escalations and incremental acquisitions provide incremental gains rather than rapid expansion.

Operating margins remain exceptionally strong, reflecting the inherent economics of real estate leasing. The trust reports a gross margin of approximately 78.1%, only slightly below its five-year median of 79.1%. These margins highlight the stability of the property portfolio and the predictable cost structure associated with long-term leases.

Share repurchases have also contributed marginally to shareholder returns. Over the past year the trust reduced outstanding shares by about 0.5%, and roughly 2.0% over the past decade. While modest in scale, these buybacks gradually enhance per-share metrics by lowering the share count.

Looking ahead, analyst estimates suggest incremental earnings improvement. Forecasts point to EPS of approximately 0.929 in the next fiscal year and around 0.959 in the following year. Revenue projections similarly indicate moderate growth, with expected sales reaching about 458.2 by 2026 and increasing to roughly 473.8 by 2027.

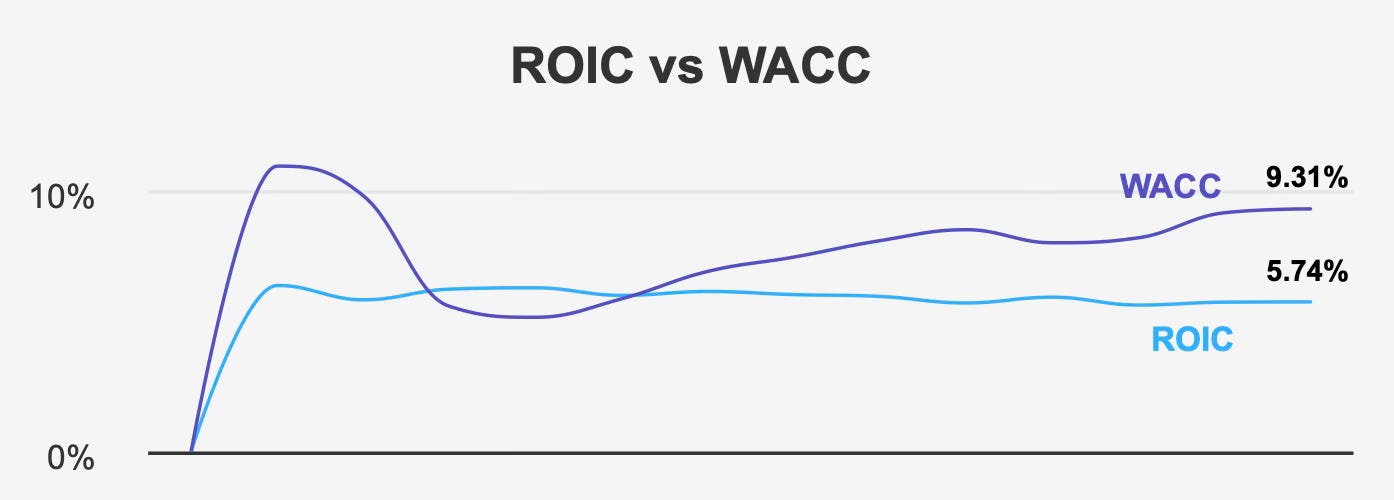

Despite these projections, capital efficiency metrics raise some questions about the quality of earnings growth. The trust’s return on invested capital has historically remained below its cost of capital. The five-year median ROIC stands near 5.9%, compared with a weighted average cost of capital around 8.2%. More recently, ROIC sits near 5.7% while the current cost of capital is approximately 9.3%.

When a company consistently earns returns below its cost of capital, it suggests that incremental investments may not generate economic value over time. In practical terms, this dynamic can limit long-term shareholder wealth creation unless operational improvements or capital allocation adjustments occur.

By contrast, return on equity appears far stronger. The trust reports a five-year median ROE of roughly 24.6%, with current levels near 27.3%. While impressive at first glance, this figure is partially influenced by leverage, which amplifies returns to equity holders.

Taken together, the earnings picture is one of stability rather than acceleration. The business generates consistent income from real estate assets and continues to grow gradually, but underlying capital efficiency metrics suggest limited economic expansion beyond incremental gains.

Dividend Profile and Sustainability

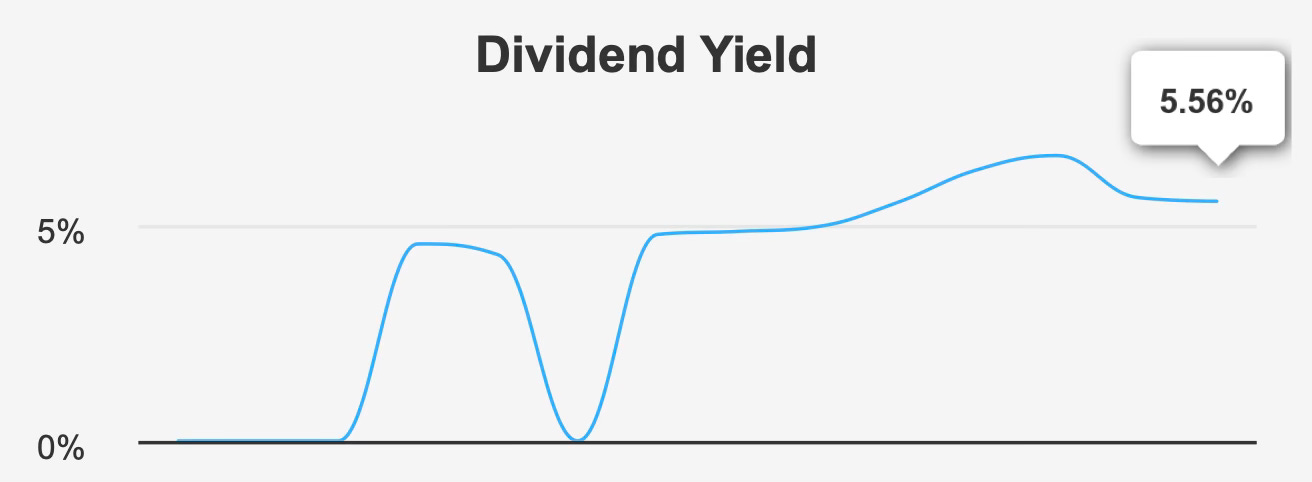

For income investors, the trust’s dividend remains the central component of the investment story. CT REIT currently offers a forward dividend yield of about 5.6%, which is broadly consistent with its historical median yield near 5.3%.

This yield reflects the REIT’s focus on delivering regular income through monthly distributions, a structure that appeals particularly to income-oriented investors seeking predictable cash flow.

Historically, dividend growth has been modest but steady. Over the past five years, the dividend has increased at an annual rate of roughly 3.4%, while the three-year growth rate sits near 3.1%. These figures align closely with the company’s broader earnings growth trajectory.

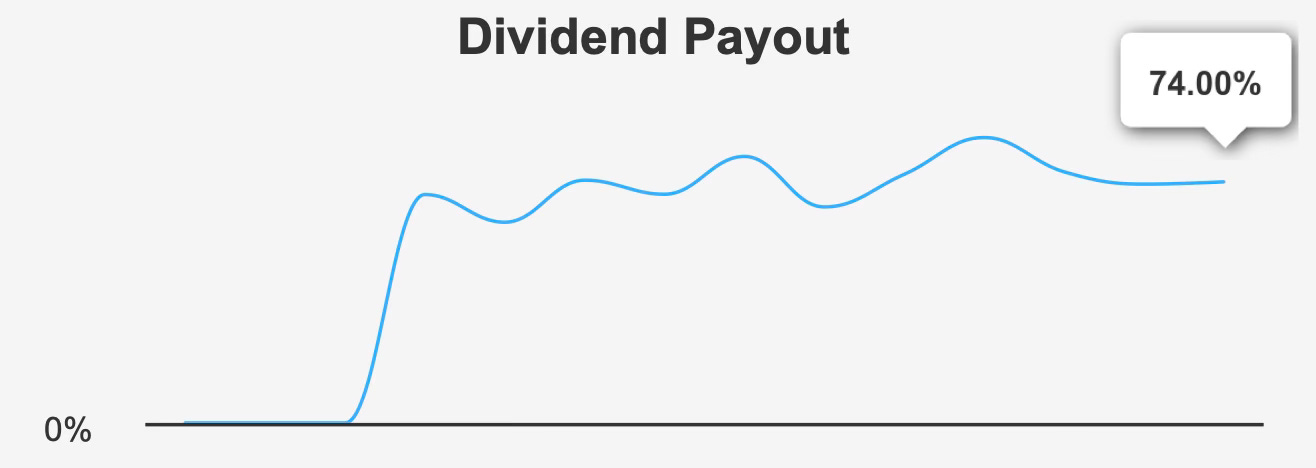

However, forward expectations indicate that dividend growth may stall in the near term. Current projections suggest essentially flat dividend growth going forward. This stagnation reflects the trust’s relatively high payout ratio and limited internal reinvestment capacity.

At present, approximately 74% of earnings are distributed to shareholders through dividends. While this level remains typical for REITs, it leaves relatively little room for reinvestment or rapid distribution increases.

Dividend coverage remains adequate but not excessive. The company’s dividend coverage ratio stands around 1.9, indicating that earnings still comfortably exceed the dividend requirement. This margin provides a buffer against moderate earnings volatility, supporting the stability of current distributions.

The trust’s leverage profile also appears manageable. Debt-to-EBITDA stands near 2.7x, a level generally considered moderate for real estate investment trusts. This suggests the company maintains a reasonable balance between financial leverage and balance-sheet stability.

The next dividend payment cycle also illustrates the consistency of the distribution policy. The upcoming ex-dividend date occurs on February 27, 2026, with the payment scheduled for March 16, continuing the REIT’s monthly payout pattern.

Overall, the dividend appears sustainable under current conditions. Stable rental income and predictable property cash flows support ongoing distributions. The primary limitation lies not in sustainability but in growth. With earnings expanding slowly and the payout ratio already elevated, investors should expect steady income rather than accelerating dividend increases.

Valuation Analysis: Interpreting Market Pricing Relative to Earnings Power, Cash Flow Generation, and Intrinsic Value

CT REIT currently trades near fair value based on multiple valuation approaches. The stock price of approximately $12.27 compares with an estimated intrinsic value of about $11.8, implying a modest negative margin of safety of roughly 4%.

From a traditional earnings perspective, the stock appears somewhat inexpensive relative to historical norms. The trailing price-to-earnings ratio stands around 9.6x, well below the company’s ten-year median multiple of roughly 13.0x. On this basis, the shares could appear attractively priced compared with historical valuation ranges.

However, forward expectations paint a more balanced picture. The forward P/E ratio is approximately 13.3x, nearly identical to the long-term median. This alignment suggests that the market already incorporates expected earnings growth into the share price.

Operational cash-flow metrics also provide useful context. The trailing enterprise-value-to-EBITDA ratio stands near 12.7x, which represents a ten-year low for the company. In isolation, this could indicate a relatively inexpensive valuation compared with historical levels.

At the same time, the price-to-free-cash-flow multiple of roughly 13.1x sits close to its long-term median, reinforcing the view that the stock is neither particularly cheap nor significantly overvalued.

Revenue-based valuation tells a similar story. The price-to-sales ratio of about 9.3x remains slightly below historical norms, reflecting cautious investor sentiment toward retail real estate assets.

Taken together, these valuation indicators create a mixed but generally balanced picture. Earnings multiples suggest some relative attractiveness, while intrinsic value estimates and forward metrics imply that the current market price already reflects the company’s moderate growth outlook.

For dividend investors, this means the investment case rests primarily on income generation rather than valuation expansion. Unless earnings growth meaningfully accelerates or interest-rate dynamics shift in favor of REITs, the stock’s upside may remain limited.

Risk Assessment and Capital Structure Considerations

Although CT REIT benefits from stable rental income and a dependable tenant base, several financial risks warrant consideration.

One of the most notable concerns is the company’s reliance on debt financing. Over the past three years, the trust has issued approximately CAD 286.6M in additional debt, contributing to a relatively weak financial strength profile.

The company’s Altman Z-score currently sits around 1.16, a level typically associated with elevated financial risk. While REIT balance sheets differ from those of industrial companies, such a score still signals the importance of careful leverage management.

Interest coverage also remains relatively modest. The trust reports an interest coverage ratio of approximately 3.4x, below the commonly preferred threshold of 5.0x. This suggests that while the company can meet its interest obligations, the margin of safety is narrower than many conservative investors might prefer.

Operational efficiency metrics further highlight structural limitations. Asset growth has outpaced revenue expansion, indicating that additional investments have not fully translated into proportional income growth.

The previously noted gap between return on invested capital and the cost of capital reinforces this concern. When investments fail to generate returns above the cost of financing, long-term value creation becomes more difficult.

Another risk factor involves corporate governance and ownership alignment. Insider ownership currently stands at 0%, meaning company executives and directors do not hold meaningful equity stakes. Institutional ownership is also relatively low at about 6.9%, suggesting limited participation from large professional investors.

Finally, liquidity considerations may influence investor behavior. Average daily trading volume over the past two months has been roughly 32,759 shares, indicating moderate liquidity. However, occasional trading inactivity can create wider bid-ask spreads and increase price volatility for smaller investors entering or exiting positions.

Collectively, these factors do not necessarily threaten the company’s immediate stability, but they reinforce the need for disciplined capital management and cautious investor expectations.

Final Assessment

CT Real Estate Investment Trust represents a classic income-focused REIT built around predictable property cash flows and a stable tenant relationship with Canadian Tire. The company’s high-quality retail portfolio and long-term lease structure provide a dependable foundation for dividend payments.

At a yield of roughly 5.7%, the stock offers an attractive income stream compared with many traditional equities. Dividend coverage remains adequate, and moderate leverage supports the continuation of distributions.

However, growth prospects appear limited. Earnings have expanded slowly over the past decade, and forward projections suggest only incremental improvement. The relatively high payout ratio also restricts the company’s ability to increase dividends meaningfully in the near future.

Valuation metrics indicate that the stock is trading close to fair value, leaving little margin of safety. Combined with capital efficiency challenges and moderate financial risk indicators, this limits the potential for significant long-term outperformance.

For investors focused on stable income rather than aggressive growth, CT REIT remains a reasonable holding. The trust offers dependable yield supported by a resilient property portfolio.

Yet for those seeking rising dividends or meaningful valuation upside, the investment case appears less compelling.

In short, CT Real Estate Investment Trust stands as a steady but unexciting income vehicle—suitable for maintaining portfolio yield, but unlikely to deliver substantial long-term growth without structural improvements in capital efficiency and expansion strategy.