Cross Timbers Royalty Trust: High Yield, Limited Growth, and a Narrow Margin for Error

A detailed dividend analysis of profitability, valuation, and income sustainability

Investment Thesis: A High-Yield Royalty Trust Offering Income but Limited Fundamental Momentum

Cross Timbers Royalty Trust CRT 0.00%↑ operates as a royalty trust with net profit interests tied to producing oil and gas properties located in Texas, Oklahoma, and New Mexico. The trust structure means that investors primarily receive income generated from underlying energy assets rather than from reinvestment-driven business expansion. As a result, the investment case for the trust is largely defined by income generation and commodity-linked cash flows rather than operational growth.

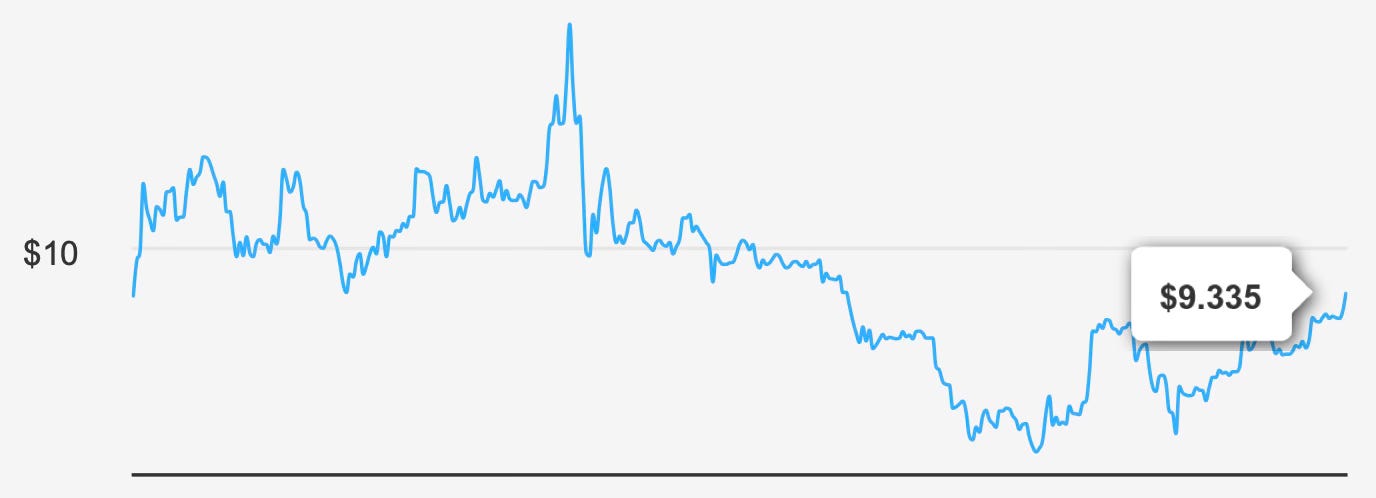

At the current market price of roughly $9 per share, the trust carries a market capitalization of approximately $56.0 million and offers a forward dividend yield of 7.4%. For income-focused investors, this yield remains appealing relative to many traditional equities, particularly within the energy royalty segment. The trust distributes most of its income to shareholders, reflected in a dividend payout ratio of 100%, which is typical for royalty trusts designed primarily as pass-through vehicles.

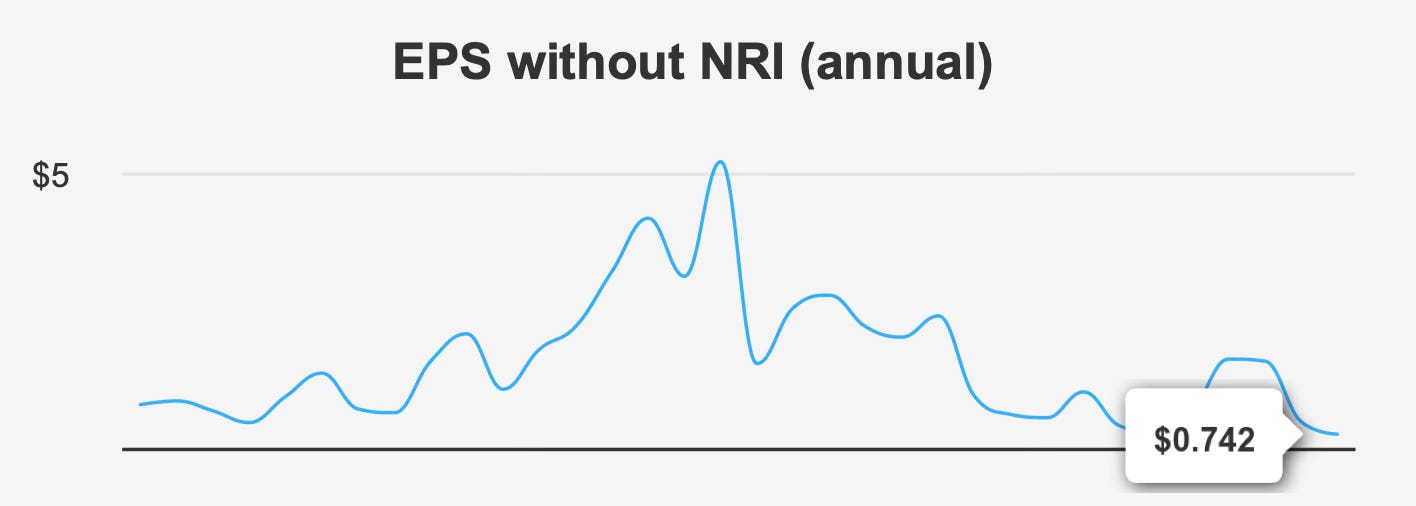

However, the high yield must be considered alongside declining near-term earnings and modest long-term growth prospects. Recent financial results reveal a noticeable deterioration in profitability. Earnings per share excluding non-recurring items declined to $0.076 in the third quarter of 2025, a significant drop from $0.149 in the prior quarter and far below the $0.254 recorded during the same period in 2024. This downward trajectory suggests that the trust is experiencing pressure from either commodity price fluctuations, production dynamics, or operational factors tied to its underlying assets.

Longer-term growth metrics reinforce this mixed picture. Over the past five years, earnings have expanded at a compound annual rate of about 11%. Yet the longer ten-year growth rate tells a different story, with earnings declining slightly at an annualized pace of roughly –2.1%. Revenue trends show similar inconsistency, with five-year revenue growth averaging 10.7% but declining by about 1.9% over the past decade.

Such variability is typical for royalty trusts, where earnings depend heavily on production levels and energy price cycles rather than on operational expansion or reinvestment. Investors should therefore view CRT primarily as an income vehicle rather than a compounding growth asset.

Industry conditions may provide some support over the long term. The broader sector is expected to expand at approximately 5% annually over the next decade, which could provide a modest tailwind if commodity demand remains stable. Still, without direct control over capital allocation or aggressive reinvestment opportunities, the trust’s ability to capitalize on industry growth remains constrained.

Taken together, Cross Timbers Royalty Trust offers investors a high current yield backed by historically strong capital efficiency. Yet declining earnings momentum and limited growth prospects temper the attractiveness of the income stream. For investors seeking stable long-term dividend growth, the trust presents a more complicated profile than its headline yield might initially suggest.

Earnings Momentum & Profitability Trends

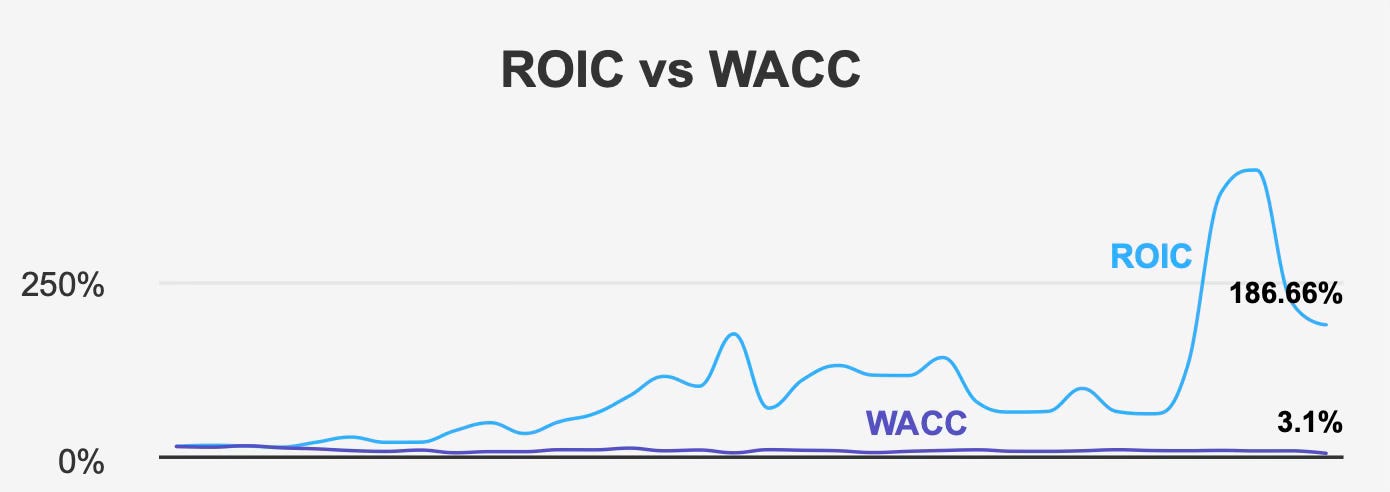

Despite recent earnings declines, Cross Timbers Royalty Trust demonstrates unusually strong capital efficiency metrics. The trust consistently generates returns on invested capital that dramatically exceed its cost of capital, reflecting the high-margin nature of royalty-based revenue streams.

Over the past five years, the trust’s median return on invested capital has reached an extraordinary 220.1%, compared with a weighted average cost of capital of 6.8%. This wide spread indicates that the underlying assets generate returns far above the capital required to maintain them. Even at present levels, the trust’s ROIC stands at 186.7%, while its current WACC is only 3.1%. Such a large differential underscores a business model that produces significant economic value relative to invested capital.

The same pattern appears in shareholder return metrics. Cross Timbers has produced a five-year median return on equity of approximately 222.5%, while its current ROE remains elevated at 188.8%. These figures highlight the structural advantages of royalty trusts, where relatively low capital requirements can produce very high accounting returns.

However, these impressive efficiency ratios should not be interpreted as signs of accelerating growth. Because the trust distributes nearly all available income to investors, high returns on capital do not translate into reinvestment-driven expansion. Instead, they primarily reflect the accounting structure of royalty interests rather than operational scalability.

Recent operating data shows signs of weakening underlying performance. Revenue per share declined to $0.127 in the third quarter of 2025, down from $0.216 in the previous quarter and $0.283 in the same quarter a year earlier. This contraction suggests either lower commodity realizations, declining production volumes, or both.

Another notable characteristic of the trust is its lack of share repurchases. Over the past decade, the buyback ratio has remained at 0%, meaning the trust has not repurchased any outstanding shares. While buybacks are uncommon for royalty trusts due to their distribution-focused structure, the absence of repurchases means earnings per share have not benefited from share count reductions.

Profitability metrics also highlight the limitations of the trust structure. Gross margins have remained unchanged at 0% over the past five years, reflecting the accounting framework of royalty income rather than a traditional operating margin profile. As a result, the usual indicators of operational efficiency offer limited insight into the trust’s long-term earnings trajectory.

In short, Cross Timbers Royalty Trust exhibits extraordinary capital efficiency but weakening near-term earnings momentum. The trust’s financial performance reflects the inherent characteristics of royalty-based income streams: highly profitable in structure, but dependent on external factors such as commodity prices and production levels rather than internal growth initiatives.

Dividend Profile & Sustainability

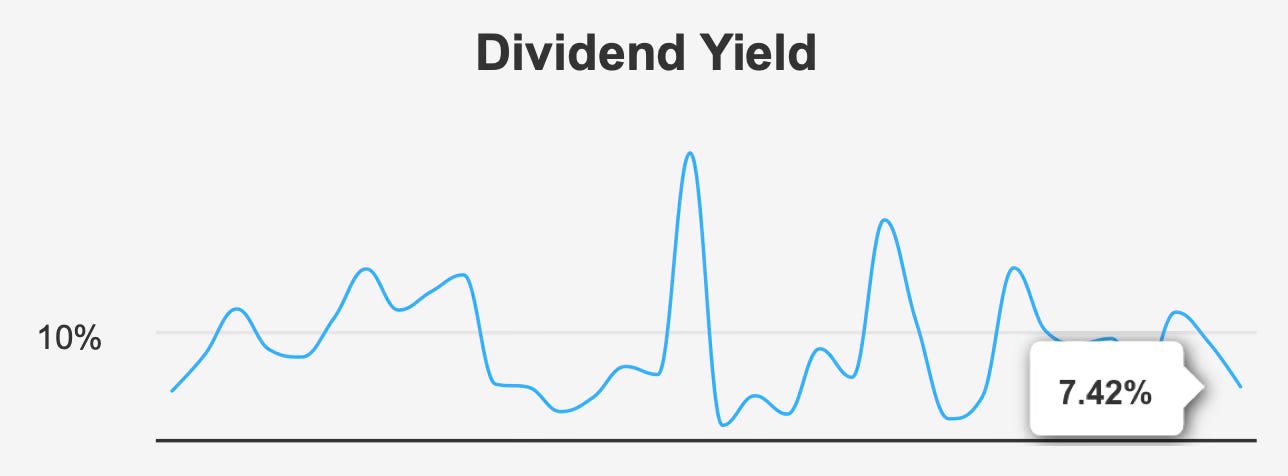

For most investors, the primary attraction of Cross Timbers Royalty Trust is its income generation. The trust currently offers a forward dividend yield of 7.4%, placing it among the higher-yielding securities within the energy income segment.

The dividend schedule is structured on a monthly distribution cycle. The most recent ex-dividend date occurred on February 27, 2026, with the corresponding payment scheduled for March 13, 2026. Monthly dividends are a defining feature of many royalty trusts, providing investors with a steady stream of income rather than the quarterly payments typical of traditional equities.

Dividend growth, however, has become increasingly inconsistent. Over the past five years, dividends per share have grown at an annualized rate of roughly 11%. Yet the shorter three-year growth rate has turned negative at –5.2%, reflecting the recent decline in earnings and the trust’s dependence on fluctuating royalty income.

The trust maintains a payout ratio of 100%, which means virtually all distributable income is passed directly to investors. While this approach aligns with the trust’s structure, it also leaves little room for dividend expansion during periods of weaker earnings. Dividend coverage currently stands at approximately 1.0, indicating that distributions are essentially equal to earnings.

One positive factor supporting the dividend is the trust’s exceptionally conservative balance sheet. Cross Timbers carries no debt, resulting in a debt-to-EBITDA ratio of 0.0. This lack of leverage eliminates interest obligations and reduces financial risk during periods of earnings volatility.

The absence of debt provides an important buffer for dividend sustainability. Even if earnings fluctuate with commodity prices, the trust does not face the additional burden of servicing debt. This financial flexibility helps support ongoing distributions, although it does not guarantee dividend growth.

Looking ahead, dividend expectations appear relatively muted. Forecasts suggest dividend growth will remain essentially flat over the next three to five years. This outlook reflects both the trust’s full payout structure and the uncertain trajectory of underlying earnings.

For income-oriented investors, CRT therefore offers an appealing current yield but limited prospects for dividend expansion. The income stream may remain stable, but it is unlikely to deliver the type of consistent growth often sought by long-term dividend investors.

Valuation Analysis: Examining Market Pricing Relative to Intrinsic Value and Historical Multiples

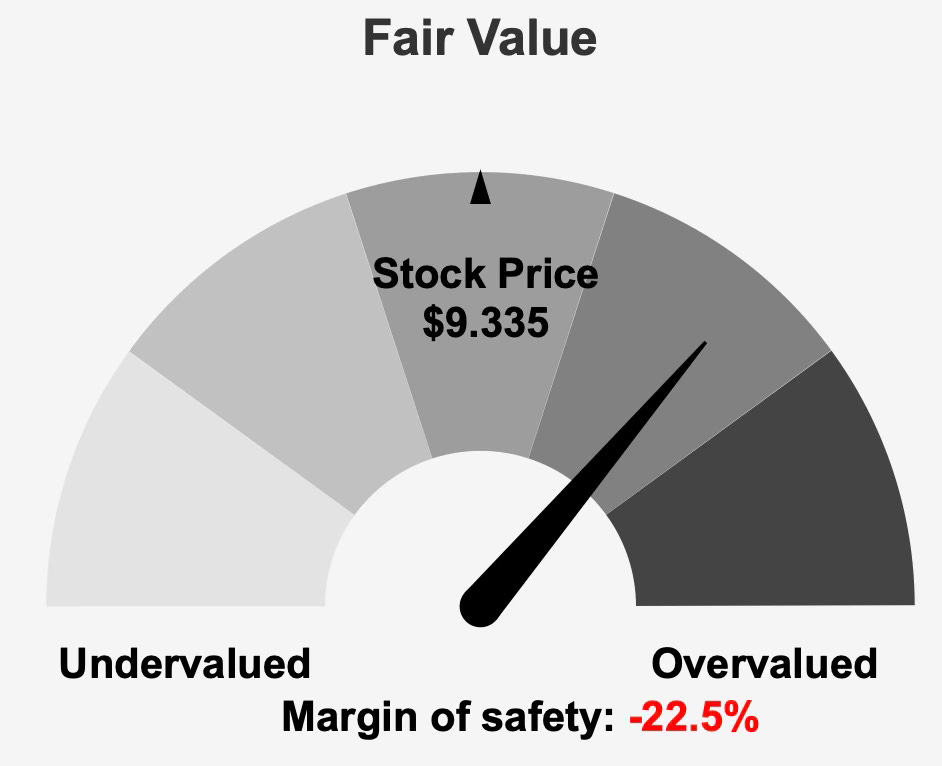

At present levels, Cross Timbers Royalty Trust appears modestly overvalued relative to its estimated intrinsic value. The trust’s intrinsic value is calculated at approximately $7.62 per share, while the market price stands near $9.34. This difference implies a negative margin of safety of roughly –22.5%, indicating that the stock trades above its fundamental valuation estimate.

Earnings-based valuation metrics reinforce this conclusion. The trust currently trades at a trailing price-to-earnings ratio of 12.6x, which is noticeably above its historical median multiple of 10.9x. This suggests investors are paying a premium relative to the trust’s long-term earnings valuation.

A similar pattern appears in enterprise valuation measures. The trailing EV/EBITDA multiple is approximately 12.4x, exceeding the ten-year median level of 10.7x. While the premium is not extreme, it does indicate that the market currently values the trust more highly than it has historically.

Sales-based valuation metrics appear more balanced. The price-to-sales ratio stands at 10.1x, which sits close to the trust’s ten-year median. This suggests the market’s valuation relative to revenue is broadly consistent with historical norms.

However, the most striking valuation metric is the price-to-book ratio. At 25.2x, the stock trades dramatically above its historical median, reflecting a very high premium to its accounting book value. Such elevated levels are not uncommon for royalty trusts, but they do indicate that the market places significant value on the income generated by the underlying assets rather than on their balance sheet representation.

Another complicating factor is the absence of forward earnings estimates. The forward P/E ratio currently registers at 0.0, suggesting that analysts have not published earnings forecasts for upcoming fiscal periods. Without forward estimates, it becomes more difficult for investors to assess whether current valuation levels are justified by expected future performance.

Overall, the valuation profile suggests investors are paying a premium for CRT’s income stream despite declining earnings momentum. While the premium is not excessive by historical standards, the negative margin of safety indicates limited upside at current prices.

Risk Assessment & Capital Structure Considerations

Cross Timbers Royalty Trust presents a mixed risk profile, combining strong financial stability with several areas of concern related to earnings volatility and governance indicators.

One of the most significant red flags is the trust’s Beneish M-Score of 4.53, which sits far above the –1.78 threshold typically associated with potential financial statement manipulation. While this indicator does not confirm wrongdoing, it signals that investors should exercise caution when interpreting reported financial data.

Another concern stems from the trust’s declining revenue per share over the past three years. This downward trend indicates weakening revenue generation and may reflect structural challenges in the underlying energy assets.

At the same time, the trust’s financial health appears exceptionally strong. The absence of debt eliminates leverage risk, while the Altman Z-score of 27.76 indicates an extremely low probability of financial distress. These metrics confirm that the trust’s balance sheet remains highly resilient.

Ownership structure also reflects limited insider and institutional participation. Insider ownership stands at only 0.58%, while institutional ownership is approximately 1.75%. Such low ownership levels suggest that the trust has not attracted significant institutional investment, which may contribute to relatively modest market liquidity.

Trading activity provides additional context. Average daily trading volume recently reached about 35,958 shares, exceeding the two-month average of 23,893. This increase suggests rising investor interest or heightened volatility in recent sessions.

Despite these risks, the trust’s fundamental financial stability remains a key strength. The absence of leverage and strong capital efficiency metrics provide a solid foundation, even if revenue volatility continues.

Final Assessment

Cross Timbers Royalty Trust represents a classic income-oriented royalty trust investment: a high-yield security supported by energy royalties and minimal leverage, but constrained by limited growth opportunities and earnings volatility.

The trust’s capital efficiency metrics are exceptionally strong, with returns on invested capital far exceeding its cost of capital. Combined with a debt-free balance sheet and stable monthly distributions, these factors provide a degree of financial resilience.

However, declining earnings momentum, inconsistent dividend growth, and valuation levels above intrinsic value complicate the investment case. The current share price already reflects a premium relative to historical earnings multiples and estimated intrinsic value, leaving limited margin for error.

For investors seeking reliable income, CRT’s 7.4% yield may still hold appeal. Yet those prioritizing dividend growth or long-term capital appreciation may find the trust’s structural limitations less attractive.

Ultimately, Cross Timbers Royalty Trust appears best suited for income-focused investors willing to accept earnings volatility in exchange for a high current yield. At current valuations, however, the stock seems appropriately categorized as a hold rather than a compelling entry opportunity.