Choice Properties REIT Investment Outlook: Defensive Assets, Constrained Returns

Assessing whether the trust’s stable property portfolio can justify its current market valuation.

Investment Thesis: Reliable Real Estate Cash Flows Offset by Weak Value Creation and Valuation Pressure

Choice Properties Real Estate Investment Trust operates a diversified portfolio of retail, industrial, mixed-use, and residential properties across Canada. Its assets are primarily concentrated in major provinces including Ontario and Quebec, with additional exposure to Alberta, Manitoba, British Columbia, and Saskatchewan. The portfolio is heavily oriented toward grocery-anchored shopping centers and stand-alone supermarket locations, providing defensive tenant demand tied to essential retail activity.

A defining feature of the trust’s operating model is its relationship with Loblaw Companies, which serves as the principal tenant and contributes a substantial portion of total rental income. This structure provides relatively stable cash flows because grocery retail tends to remain resilient across economic cycles. For income-oriented investors, this tenant profile has historically supported predictable rental streams and consistent dividend payments.

However, while the underlying real estate portfolio offers stability, the broader financial picture reveals several structural limitations. Long-term growth has been modest, capital efficiency remains weak, and leverage levels are elevated relative to typical real estate investment trust benchmarks. These factors significantly influence the investment outlook.

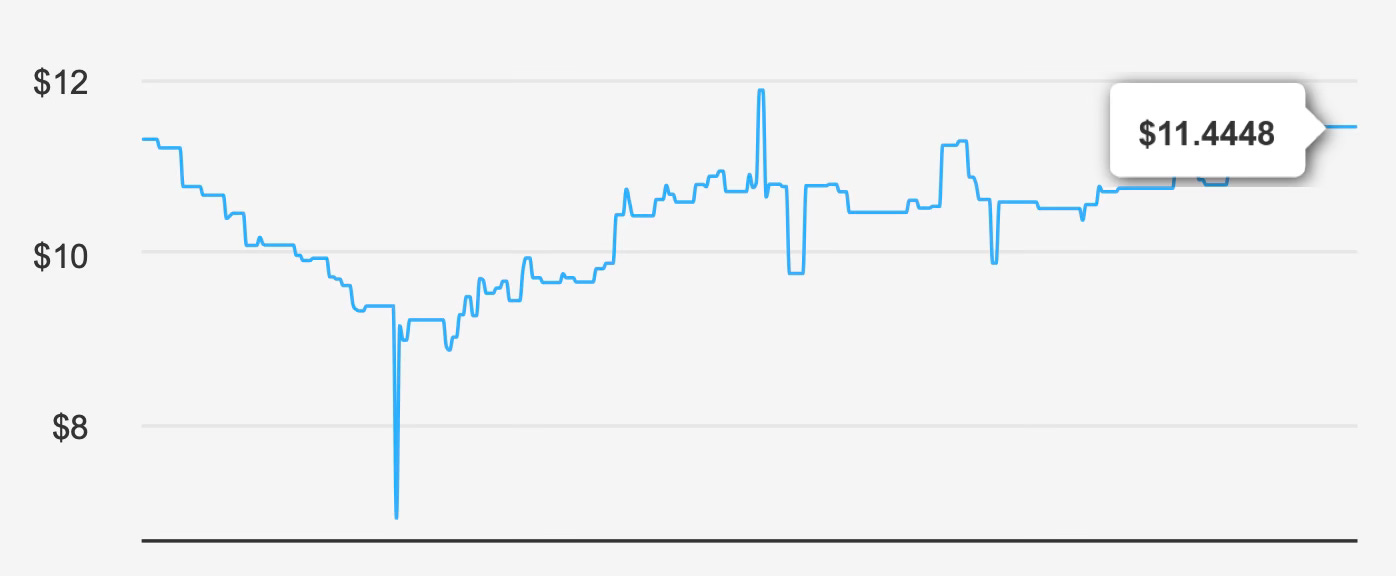

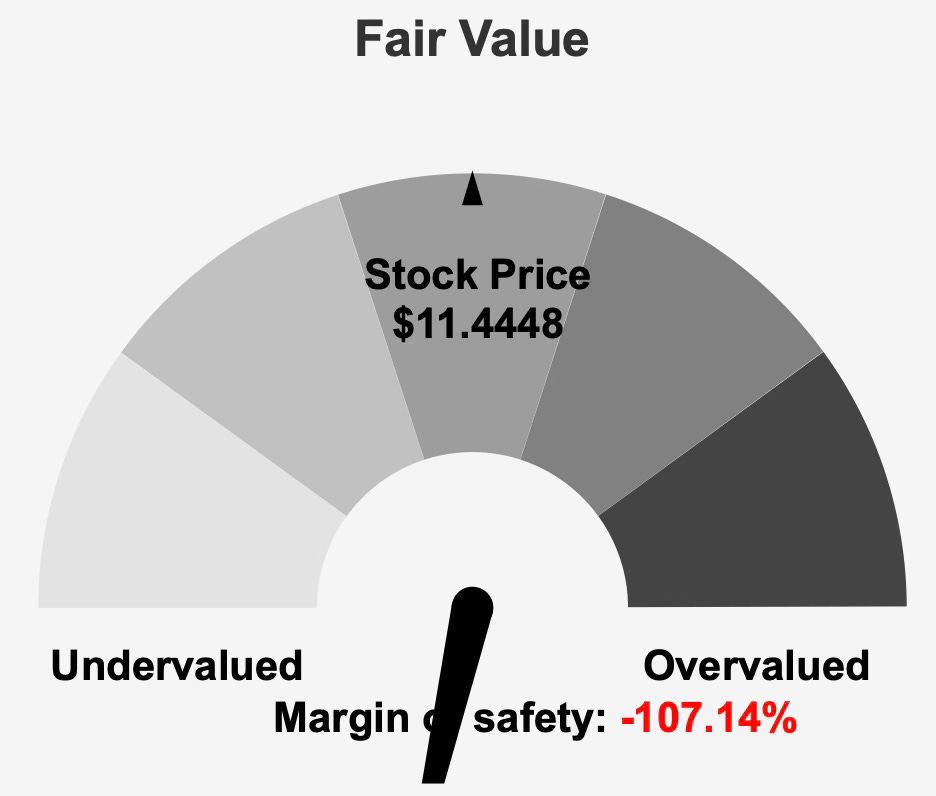

At the current market price near $11, the trust carries a market capitalization of approximately $8.39 billion. Yet fundamental valuation models estimate intrinsic value closer to $5.53, implying the shares trade well above underlying economic value. The resulting negative margin of safety of roughly 107% highlights a disconnect between market pricing and fundamental valuation metrics.

For dividend investors, the forward yield of approximately 4.9% provides moderate income generation, particularly given the REIT’s monthly dividend structure. Nonetheless, the modest growth trajectory, combined with weak capital returns and high leverage, suggests that the trust’s income profile may come with elevated financial risk.

Ultimately, Choice Properties represents a relatively stable real estate platform supported by essential retail tenants, but the trust’s ability to generate long-term value for shareholders remains constrained by slow growth, capital inefficiencies, and a stretched valuation.

Earnings Momentum & Profitability Trends

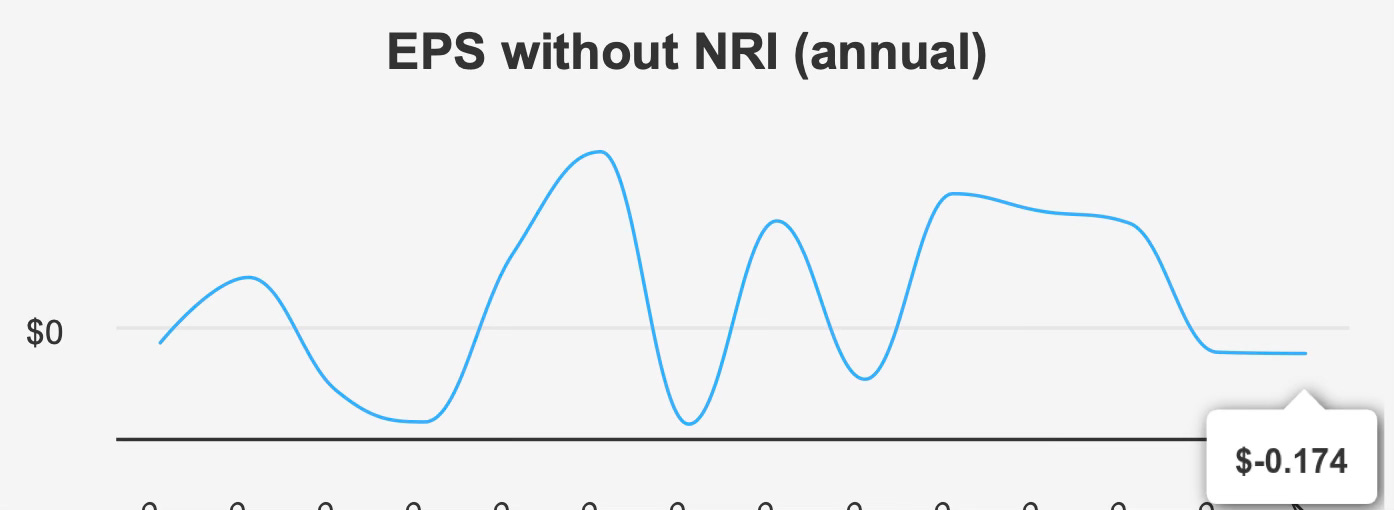

Recent earnings performance highlights the uneven trajectory of the trust’s profitability. In the most recent quarter ending December 31, 2025, earnings per share excluding non-recurring items declined sharply to $0.015. This represents a substantial deterioration from $0.175 in the prior quarter and a significant drop from $0.807 in the same quarter the previous year.

Such volatility reflects a challenging earnings environment relative to earlier periods, particularly following the stronger performance seen during the third quarter of 2025. While quarterly results can fluctuate due to property revaluations, financing costs, and other real estate-specific accounting adjustments, the magnitude of this decline suggests pressure on the trust’s underlying profitability.

Revenue performance has been more stable than earnings. Revenue per share remained at $0.355 in the most recent quarter, essentially unchanged from the prior quarter and slightly higher than the $0.334 reported in the same period of the previous year. This indicates that the trust’s rental income base remains relatively steady even as profitability fluctuates.

Long-term growth metrics further reinforce the picture of limited expansion. Over the past five years, earnings per share excluding non-recurring items have recorded a compound annual growth rate of 0.0%. The ten-year growth rate for earnings is similarly flat. Revenue growth has also been modest, with five-year revenue growth of approximately 1.9% and a ten-year rate slightly negative at around –0.3%.

These figures suggest that while the trust maintains stable operations, it has struggled to generate meaningful growth in earnings or revenue over extended periods.

Profitability margins remain strong at the property level, which is typical for large REITs. The trust reported a gross margin of roughly 71.8%, slightly above its five-year median margin of 71.2%. However, this figure remains below the historical peak of approximately 74.8%, indicating some compression relative to prior periods.

Capital allocation trends also warrant attention. Over the past decade, the trust’s share buyback ratio stands at –7.8%, indicating that share repurchases have not been used as a meaningful capital allocation tool. Instead, the data suggests that the number of shares outstanding has likely increased over time through equity issuance. This can dilute existing shareholders and limit earnings-per-share growth.

Looking ahead, analysts expect moderate improvement in profitability. Earnings per share are projected to reach approximately $0.777 in the next fiscal year, with further growth to roughly $0.806 in the following year. Revenue is expected to rise to about $1.14 billion in 2026 and approximately $1.19 billion in 2027.

While these projections indicate a potential return to gradual growth, the overall trajectory remains relatively modest. Without stronger earnings expansion or significant improvements in capital efficiency, long-term value creation may remain limited.

Dividend Profile & Sustainability

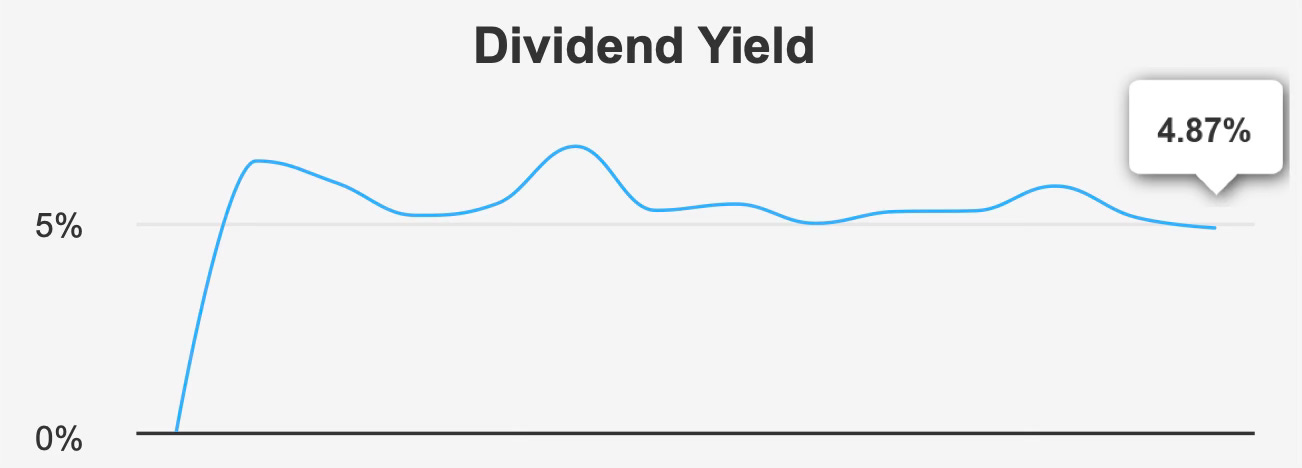

Choice Properties REIT maintains a consistent monthly dividend structure, which is attractive for income-focused investors seeking regular cash distributions. The trust currently pays a dividend of CAD 0.064167 per share each month, providing a forward dividend yield of approximately 4.9%.

Although the yield is competitive within the REIT sector, dividend growth has been minimal. Over the past three years, dividend growth has averaged about 1.2% annually, while the five-year growth rate is slightly lower at around 0.8%. These figures reflect a largely stagnant dividend trajectory, suggesting that management prioritizes maintaining the payout rather than expanding it meaningfully.

The trust’s forward dividend yield also sits slightly below its historical median yield of approximately 5.3%, implying that investors currently receive somewhat less income relative to historical valuation levels.

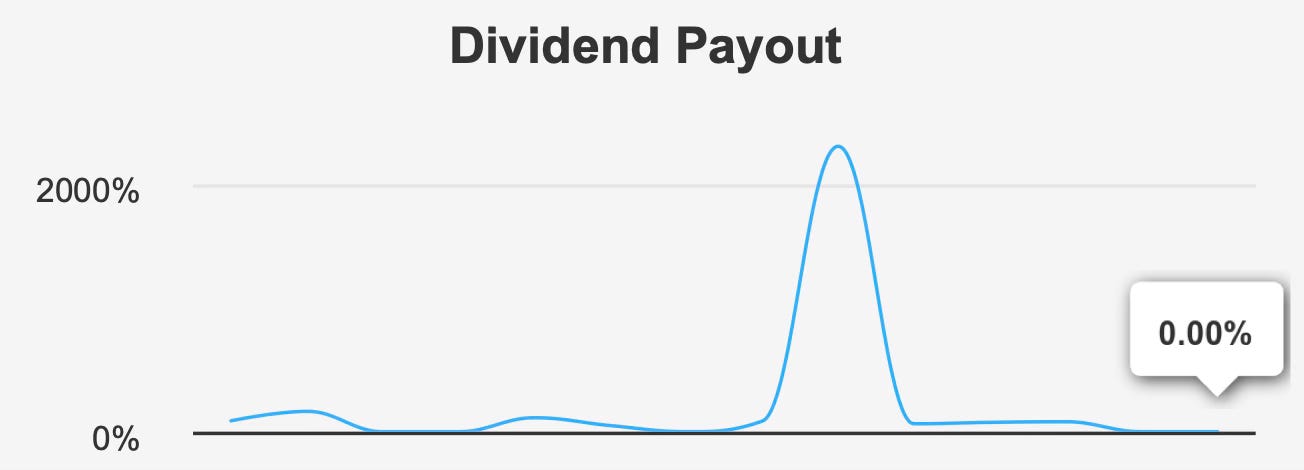

One unusual data point is the reported dividend payout ratio of 0.0%. While this figure likely reflects accounting adjustments or changes in reporting methodology, it complicates the interpretation of dividend coverage. In addition, the dividend coverage ratio currently appears negative, suggesting that earnings alone may not fully support the payout under current conditions.

Despite these concerns, the trust continues to distribute dividends consistently, with the next ex-dividend date scheduled for February 27, 2026, followed by a payout date of March 16, 2026. The monthly payment structure remains a defining feature of the trust’s shareholder return profile.

Future dividend growth expectations are muted. Forecasts suggest a 3–5 year dividend growth rate of 0.0%, implying that investors should not anticipate significant increases in distributions over the near term.

While the yield remains attractive relative to many income investments, the lack of growth limits the dividend’s ability to offset inflation or deliver rising income streams over time.

Valuation Analysis: Market Price Appears Disconnected from Underlying Fundamental Value

Valuation metrics suggest that Choice Properties currently trades at a level that may not be supported by its underlying fundamentals.

Intrinsic value estimates place fair value at approximately $5.53 per share, significantly below the current market price of roughly $11.44. This implies the shares trade at more than double their estimated intrinsic value, resulting in a negative margin of safety of about 107%.

From a multiples perspective, the forward price-to-earnings ratio stands near 14.7x, which is broadly in line with the trust’s ten-year median multiple of around 14.0x. On the surface, this might suggest a reasonable valuation relative to historical earnings expectations.

However, other valuation measures paint a less favorable picture.

The trailing EV/EBITDA multiple sits around 33.8x, substantially higher than the historical median of approximately 13.7x. This sharp divergence suggests that the enterprise value of the trust has risen far faster than its operating earnings.

Similarly, the price-to-free-cash-flow ratio currently stands near 16.8x, compared with a historical median of about 14.7x. While this premium is less dramatic than the EV/EBITDA discrepancy, it still indicates that investors are paying a higher price for each dollar of available cash flow.

The price-to-book ratio remains relatively stable at approximately 1.1x, almost identical to the ten-year median of 1.1x. This suggests the trust trades near book value, which is typical for many real estate investment trusts.

Meanwhile, the price-to-sales ratio stands near 8.1x, slightly above its long-term median of roughly 7.3x. Although this difference may appear modest, it still reflects a premium relative to historical norms.

Taken together, these valuation metrics indicate that the market price currently reflects optimistic expectations relative to the trust’s underlying growth profile and capital efficiency.

Without stronger earnings expansion or improved capital returns, it may be difficult for the trust to justify its current valuation over the long term.

Risk Assessment & Capital Structure Considerations

Several financial indicators highlight elevated risk levels within the trust’s capital structure.

One of the most notable concerns is leverage. The trust currently reports a debt-to-EBITDA ratio of approximately 12.7, significantly higher than the commonly cited industry caution threshold of around 4.0. Such elevated leverage increases sensitivity to interest rate movements and may reduce financial flexibility during periods of economic stress.

Over the past three years, the trust has issued roughly CAD 194.2 million in additional debt, further increasing leverage levels. While debt financing is common in the REIT sector due to the capital-intensive nature of real estate ownership, excessive leverage can magnify financial risk.

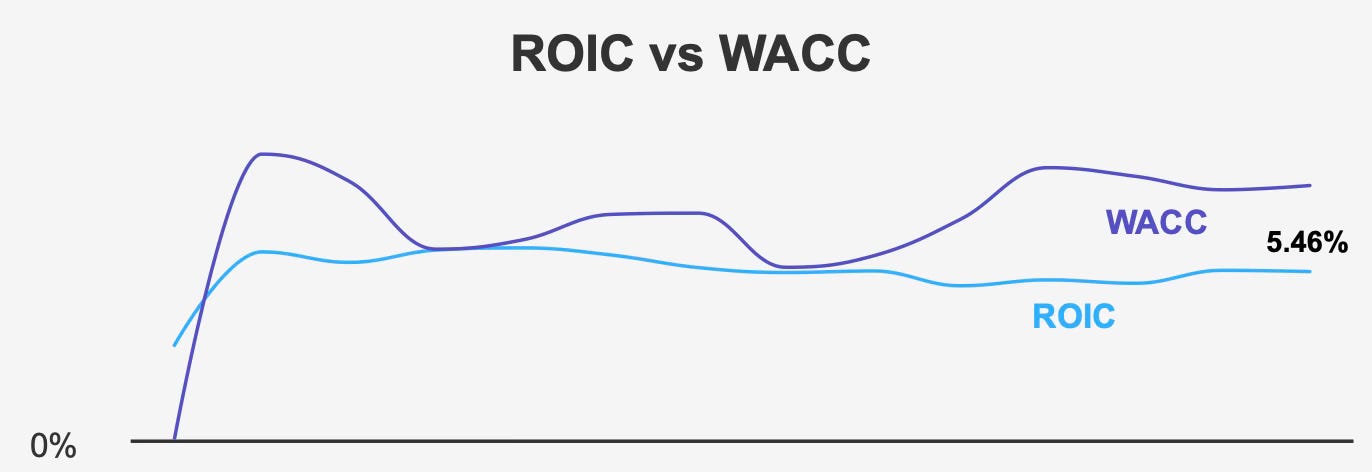

Another important metric is capital efficiency. The trust’s current return on invested capital stands near 5.4%, slightly above its five-year median of about 5.2%. However, this return remains well below the weighted average cost of capital, which currently sits around 8.3% and has averaged roughly 8.1% over the past five years.

When a company consistently earns returns below its cost of capital, it effectively destroys shareholder value rather than creating it. This gap between ROIC and WACC has persisted over time, indicating structural inefficiencies in capital deployment.

Credit risk indicators also warrant attention. The trust’s Altman Z-score is approximately 1.31, placing it within the financial distress zone. This metric suggests an elevated probability of financial strain within the next two years if conditions were to deteriorate.

On the positive side, the Beneish M-Score stands at approximately –2.61, which suggests a low likelihood of earnings manipulation or accounting irregularities.

Ownership structure provides additional context. Insider ownership currently stands at 0%, and there have been no insider purchases or sales over the past year. While this may simply reflect the trust’s governance structure, the absence of insider ownership can sometimes raise questions about alignment between management and shareholders.

Institutional investors hold roughly 28.5% of the trust’s shares, indicating a moderate level of professional investor participation.

Liquidity conditions are another potential concern. Average trading volume over the past two months has been around 24,729 shares, indicating relatively thin trading activity. Additionally, approximately 40% of trades occur through dark pools, which can reduce price transparency and contribute to volatility.

Final Assessment

Choice Properties REIT offers investors exposure to a stable portfolio of grocery-anchored retail and mixed-use properties supported by long-term tenant relationships. The trust’s predictable rental income and consistent monthly dividend payments make it appealing for income-focused investors seeking steady cash distributions.

However, several structural challenges limit the long-term investment case.

Earnings growth has been stagnant for years, revenue expansion remains modest, and capital efficiency metrics show that returns on invested capital consistently fall below the cost of capital. Elevated leverage further increases financial risk, while valuation metrics indicate that the shares currently trade well above estimated intrinsic value.

The trust’s dividend yield near 5% may appear attractive at first glance, but the lack of meaningful dividend growth and the underlying financial pressures reduce its appeal for long-term dividend growth investors.

In its current form, Choice Properties REIT represents a stable but slow-growing real estate platform whose valuation may already reflect much of its income potential. For investors prioritizing income stability, the trust may still warrant consideration, but those seeking strong total returns or dividend growth may find more compelling opportunities elsewhere in the REIT sector.