Chevron: Yield Without Margin of Safety

Stable Dividend, Cyclical Earnings, and Premium Valuation

1. Investment Thesis: A High-Quality Energy Franchise Trading at a Premium to Its Economic Returns

Chevron CVX 0.00%↑ is one of the world’s largest integrated energy companies, operating across upstream exploration, production, and downstream refining activities on nearly every continent. The company produces roughly 3.0 million barrels of oil equivalent per day and holds proven reserves of approximately 9.8 billion barrels of oil equivalent, supported by global refining capacity near 1.8 million barrels per day. Its scale, geographic diversification, and vertically integrated structure provide resilience across commodity cycles and have historically supported consistent shareholder distributions.

For dividend investors, Chevron’s investment case traditionally rests on reliability rather than growth. The company offers a durable cash flow profile, moderate long-term expansion, and a track record of regular dividend increases. However, the current investment environment shifts the focus from business quality to valuation discipline.

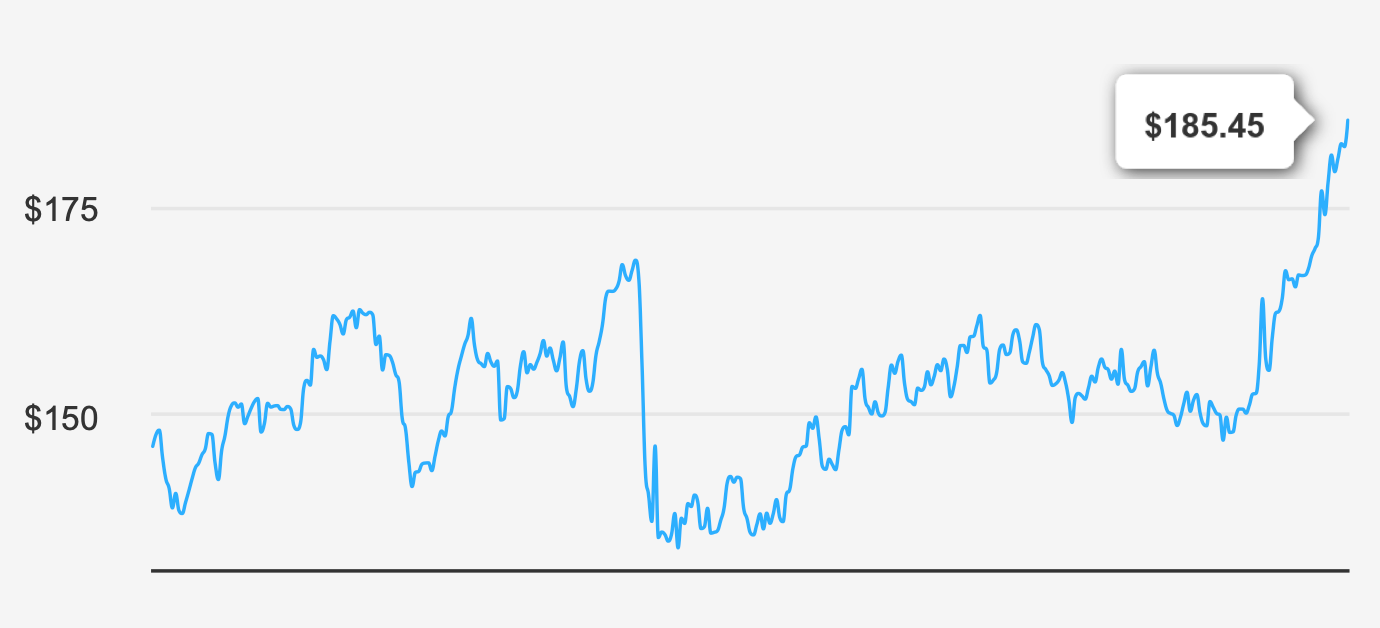

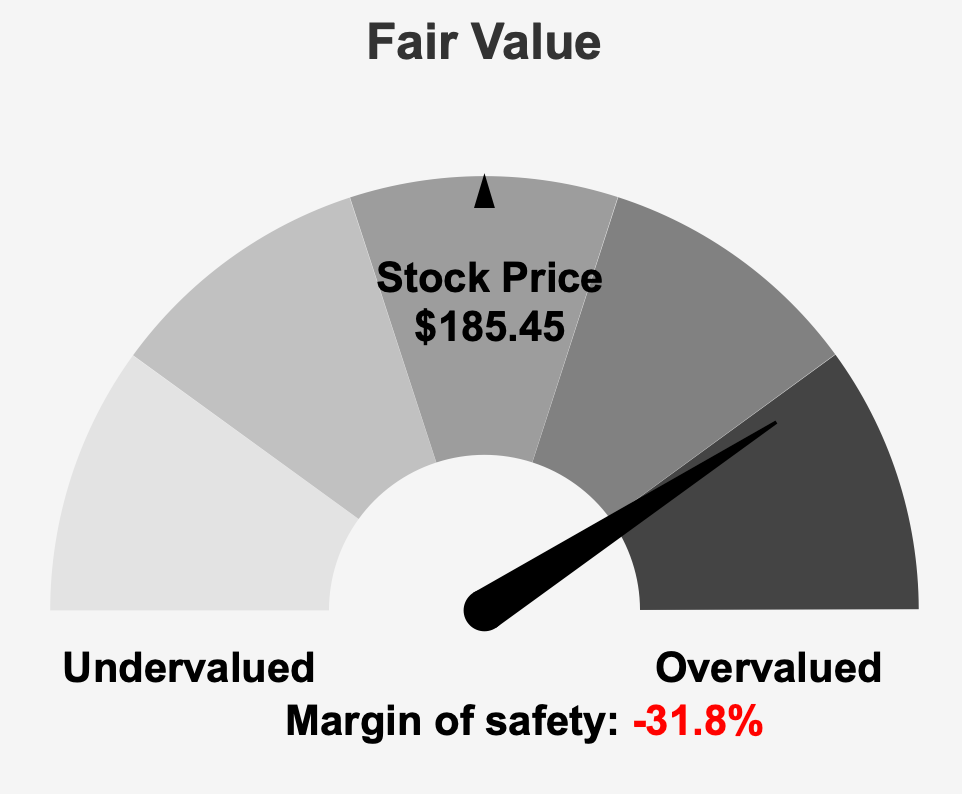

Shares trade around $185 while intrinsic value estimates sit near $140.7, leaving a negative margin of safety of roughly 31.8%. That gap is central to the investment debate. Investors are not evaluating whether Chevron is a good business — it is — but whether the present price already discounts favorable industry conditions.

Long-term growth expectations reinforce the concern. The company’s five-year growth rate is about 6.1%, yet broader industry expansion is projected closer to 2–3% annually over the coming decade. The market therefore appears to be pricing Chevron closer to a steady compounder than a cyclical commodity producer.

The core thesis emerges clearly: Chevron remains a financially strong and operationally reliable dividend franchise, but the current share price reflects optimistic assumptions about future commodity conditions and capital returns. At present levels, investors are paying for stability and yield without receiving a valuation cushion.

2. Earnings Momentum & Profitability Trends

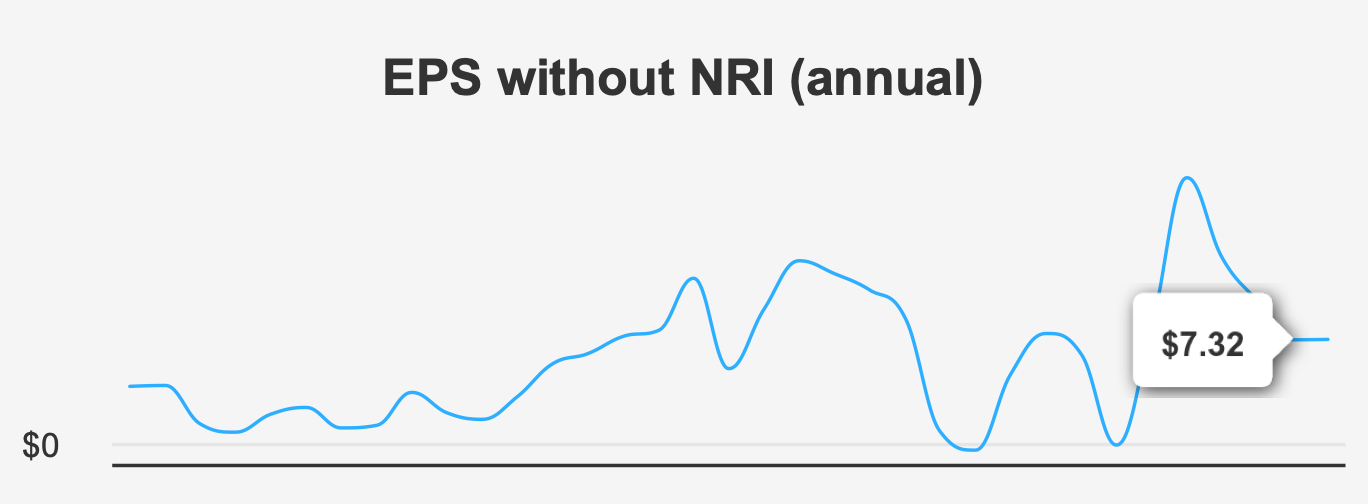

Recent operating results illustrate Chevron’s cyclical earnings profile. Fourth-quarter 2025 earnings per share excluding non-recurring items came in at $1.52, down from $1.85 in the prior quarter and $2.06 in the year-earlier period. Diluted earnings showed a similar pattern, declining to $1.39 from $1.82 sequentially and $1.84 year over year. Revenue per share followed the same trajectory, falling to $22.93 from $24.75 in the previous quarter and $27.17 a year earlier.

While quarterly fluctuations are normal in the energy sector, the longer-term trend is more revealing. Over both five-year and ten-year periods, Chevron’s annual earnings have effectively shown no compound growth. The company generates strong profits during favorable pricing environments but does not consistently compound earnings over time. Instead, results rise and fall with commodity cycles.

Margins support this interpretation. The most recent gross margin measured roughly 30.4%, broadly consistent with the company’s five-year median but slightly below peak historical levels near 31.4%. This stability indicates disciplined operations, yet also confirms the absence of structural margin expansion typically associated with secular growth businesses.

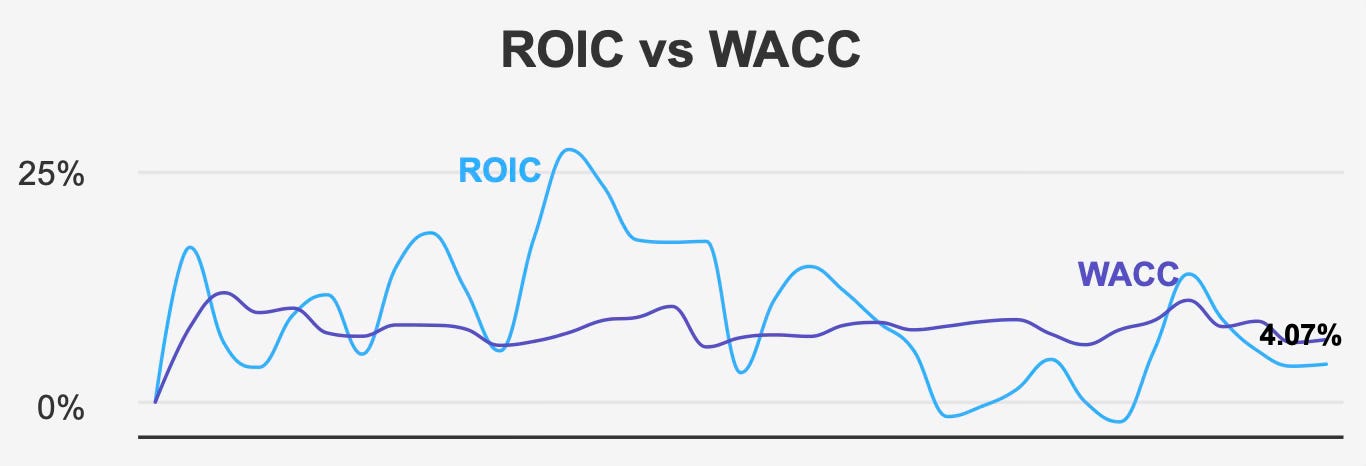

More concerning is capital efficiency. Over the past five years, Chevron’s median return on invested capital has been about 5.6%, below its roughly 8.7% cost of capital. Currently, returns remain subdued at about 4.1% against a cost near 6.7%. In simple terms, the company has not consistently generated returns sufficient to economically justify the capital deployed.

Commodity producers frequently oscillate around their cost of capital, but sustained negative spreads matter for valuation. Businesses that cannot regularly earn more than their cost of capital rarely justify persistent premium multiples without unusually strong pricing conditions.

Near-term projections do indicate recovery. Analyst expectations suggest earnings could reach about $6.44 next fiscal year and approximately $8.43 the following year. Revenue is forecast to increase gradually, moving from roughly $188.5 billion to $202.5 billion and eventually near $205.1 billion over the next several years.

These forecasts imply moderate expansion rather than transformative growth. Chevron’s earnings power remains durable but cyclical — dependable over long horizons, yet highly sensitive to commodity prices and global energy demand.

3. Dividend Profile & Sustainability

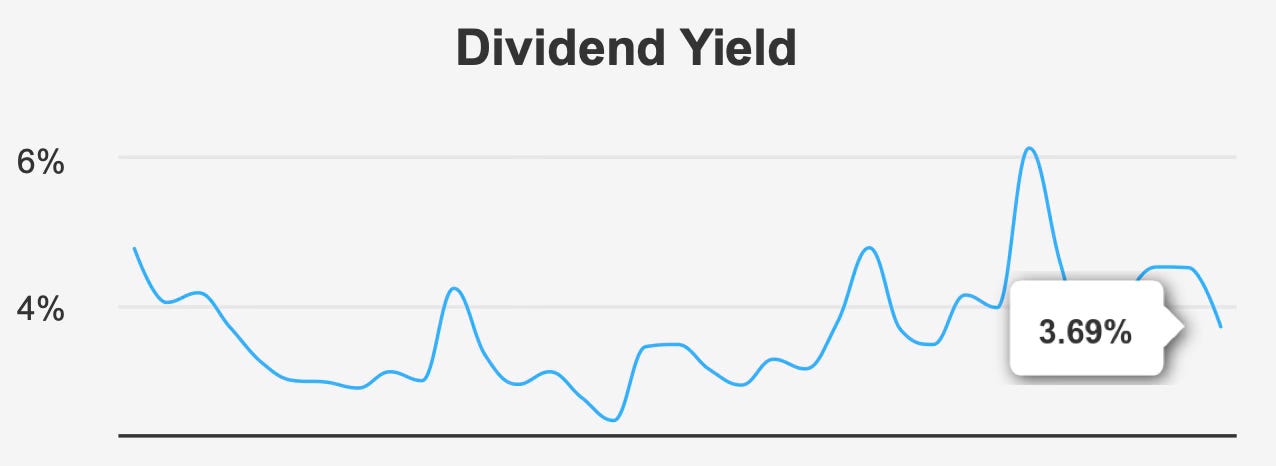

The dividend remains Chevron’s primary attraction. The forward yield stands around 3.8%, close to the company’s decade-long norm near 4%. This consistency reinforces Chevron’s identity as an income-focused equity rather than a capital appreciation vehicle.

Management continues to increase the payout regularly. The latest quarterly dividend rose to $1.78 per share from $1.71, extending a long record of incremental growth. Over the past five years, dividends have grown roughly 6.1% annually, while the three-year rate sits near 6.4%. Looking ahead, expectations moderate toward approximately 4–5% annual growth — slower but still positive.

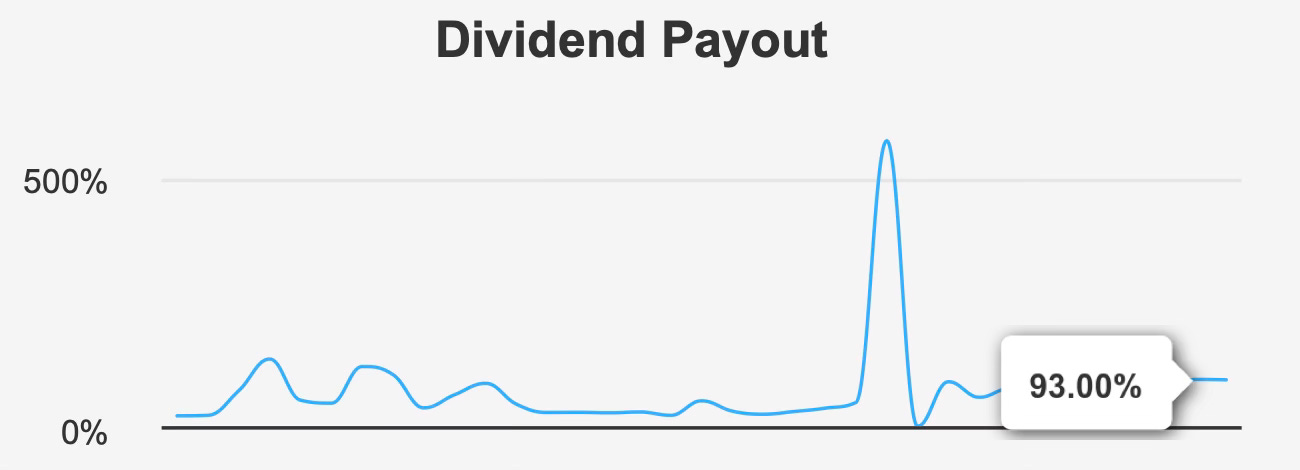

The sustainability question centers on coverage rather than commitment. The payout ratio stands close to 93%, leaving limited buffer during weaker earnings periods. Dividend coverage therefore depends heavily on maintaining stable commodity pricing and operating cash flows.

Fortunately, Chevron’s balance sheet provides flexibility. Debt-to-EBITDA is about 1.0, comfortably below levels typically associated with financial strain. The company retains capacity to support dividends during cyclical downturns through balance-sheet strength and capital allocation adjustments.

This creates a typical supermajor profile: the dividend is unlikely to be cut easily, but growth may slow during weak cycles. Investors should expect stability, not rapid expansion. The distribution appears secure in the medium term, yet the high payout ratio reduces resilience if prolonged commodity weakness emerges.

In practical terms, Chevron offers a dependable income stream rather than a rapidly compounding one. The dividend is stable, growing modestly, and supported by financial strength — but not heavily covered by earnings.

4. Valuation: Premium Multiples Despite Cyclical Earnings and Sub-Cost-of-Capital Returns

Valuation currently represents the dominant risk factor in Chevron’s investment profile. The shares trade meaningfully above intrinsic value estimates, reflecting investor willingness to pay a premium for stability and income in an uncertain macroeconomic environment.

Forward earnings multiples sit around 28.3x, while trailing earnings trade near 27.9x. Both are significantly higher than the company’s historical norm near 16.7x. The market is therefore valuing Chevron closer to a defensive growth equity than a cyclical commodity producer.

Cash flow valuation tells a similar story. Price-to-free-cash-flow is roughly 20.8x compared with a long-term median near 15.6x. Enterprise value to EBITDA stands near 9.9x versus a historical level around 7.7x. Price-to-sales and price-to-book ratios also exceed decade averages, reinforcing the conclusion that investors are paying above-normal multiples across nearly every valuation framework.

These premiums would be easier to justify if returns on capital were improving structurally. Instead, the company continues to earn below its cost of capital. The market is effectively discounting a favorable commodity environment and sustained earnings recovery.

Consensus price targets cluster slightly below the current share price, reinforcing a cautious outlook. The valuation appears to reflect optimism rather than conservatism. Any disappointment in commodity pricing or earnings growth could compress multiples toward historical levels.

Put differently, Chevron’s current valuation embeds the upside scenario while leaving limited protection against normal cyclical volatility.

5. Risk Assessment & Capital Structure Considerations

Chevron’s financial position remains strong but not risk-free. The company has issued roughly $5.4 billion in long-term debt over the past three years, though overall leverage remains manageable due to stable cash generation and moderate debt ratios.

The larger concern lies in economic performance rather than solvency. Persistent returns below the cost of capital indicate that capital deployment efficiency remains a challenge. This is not unusual in the oil industry but becomes more relevant when the stock trades at premium valuation levels.

The company’s Altman Z-score of about 1.47 places it in a theoretical distress zone, though this metric can be less predictive for large integrated energy companies with substantial asset bases and stable cash flows. Nevertheless, it highlights sensitivity to commodity downturns rather than imminent financial danger.

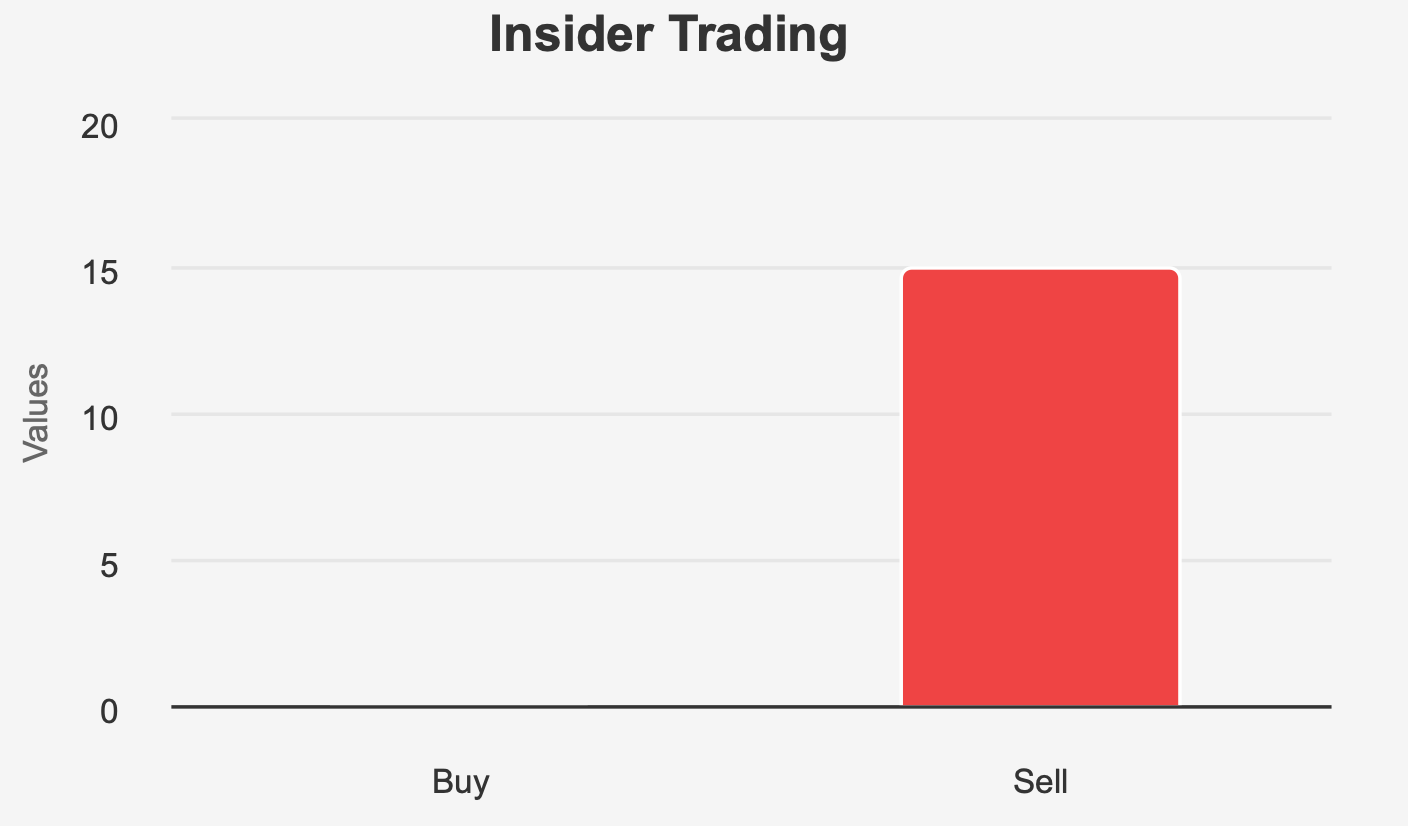

Insider activity presents a softer signal. Over the past year, insiders have consistently sold shares without notable purchases. While insider ownership remains small and institutional ownership exceeds 70%, the selling pattern may indicate limited perceived upside at current prices.

Operationally, Chevron benefits from global diversification, strong liquidity, and substantial trading volume, supporting share stability and capital market access. Financial integrity indicators suggest no evidence of earnings manipulation, providing reassurance regarding reporting quality.

Overall risk therefore centers on valuation and cycle exposure rather than balance-sheet fragility. The company is financially solid but economically cyclical.

Final Assessment

Chevron remains a high-quality energy major with durable operations, global scale, and a reliable dividend. The balance sheet is strong, the payout is stable, and long-term demand for energy supports ongoing relevance.

However, investment returns depend not only on business quality but on entry price. Today, valuation appears to assume favorable commodity conditions, steady earnings recovery, and continued investor demand for defensive yield. Meanwhile, long-term earnings growth has been flat, returns on capital remain below the cost of capital, and the dividend consumes most of current profits.

The stock therefore presents an asymmetrical profile. Downside risk comes from valuation normalization rather than operational deterioration, while upside requires sustained supportive energy markets.

For long-term dividend investors, Chevron remains suitable as a stable income holding when purchased at reasonable valuations. At present levels, however, the shares offer yield without margin of safety.

The company is dependable — but the price demands optimism.