Chemtrade Logistics Income Fund: Operational Momentum Versus Valuation Reality

Operational progress strengthens the investment narrative, though valuation discipline remains essential.

Investment Thesis: Evaluating the Sustainability of Chemtrade’s Income Potential Amid Operational Recovery

Chemtrade Logistics Income Fund operates as a North American supplier of industrial chemicals and services, with activities organized across two primary business segments: Sulphur and Water Chemicals and Electrochemicals. The company generates the majority of its revenue in the United States, while also maintaining operations in Canada and South America.

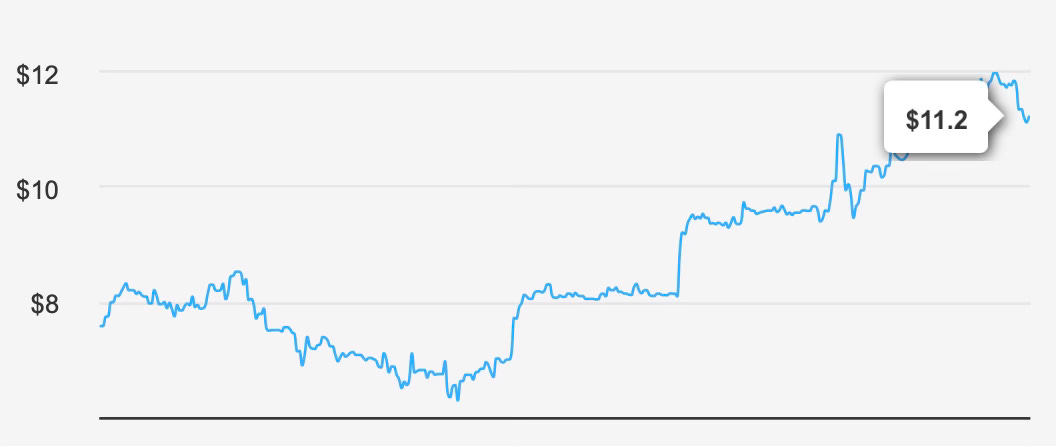

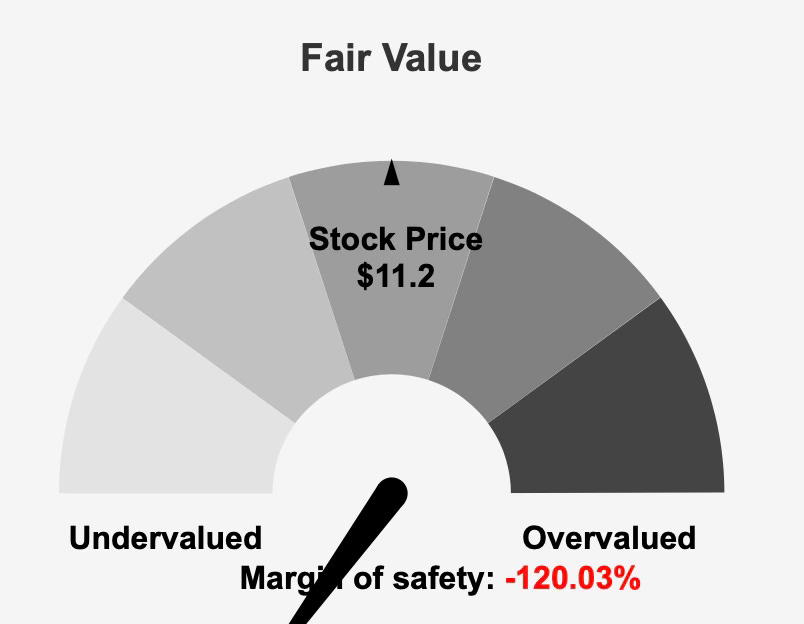

From an investment perspective, the company presents a complex profile that blends improving operating performance with lingering structural concerns. The current share price sits around $11, implying a market capitalization of roughly $1.30 billion. At the same time, intrinsic value estimates stand significantly lower at $5.09, suggesting the market may already be pricing in a substantial portion of the firm’s operational recovery.

Chemtrade’s investment narrative is shaped by three key dynamics. First, the company has recently demonstrated meaningful improvement in profitability and operational efficiency. Margins have expanded, and returns on invested capital have risen above the firm’s cost of capital. These developments suggest that management initiatives aimed at improving cost discipline and capital allocation are beginning to produce measurable results.

Second, the company continues to provide an income-oriented shareholder return profile. With a forward dividend yield near 4.7%, the stock remains relevant for investors focused on income generation. The dividend payout ratio remains below 50%, indicating that distributions are currently supported by earnings rather than financed through balance sheet expansion.

However, the third element of the investment thesis introduces an important counterweight. Despite operational improvement, the company’s longer-term growth profile remains modest. Revenue trends over both five- and ten-year horizons have been negative, and dividend growth over the past five years has declined as well. These structural headwinds raise questions about the sustainability of long-term growth beyond the current operational rebound.

The result is an investment case that depends heavily on execution. If Chemtrade continues improving margins and capital efficiency, the company may be able to sustain and gradually grow its dividend profile. Yet the current valuation suggests the market may already be anticipating much of that progress.

For long-term dividend investors, this creates a nuanced tradeoff: stable income potential supported by improving profitability, balanced against limited valuation upside and lingering structural risks within the underlying business.

Earnings Momentum & Profitability Trends

Chemtrade’s recent financial performance indicates that operational momentum has improved meaningfully, particularly when examining profitability metrics and capital efficiency.

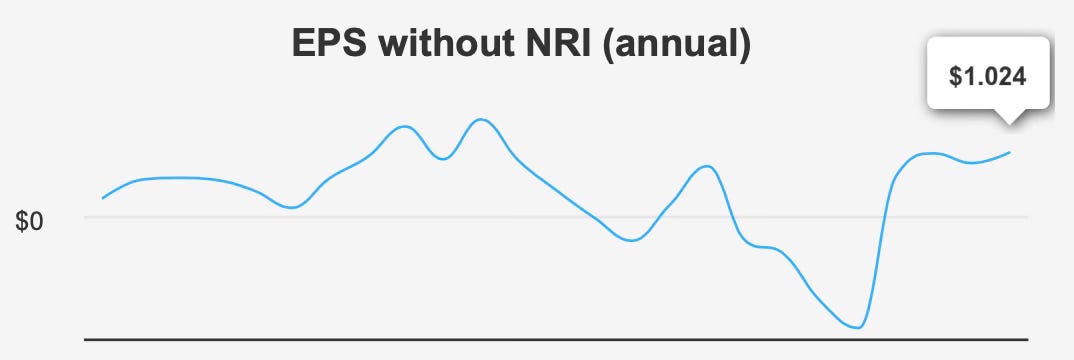

In the third quarter ending September 30, 2025, the company reported earnings per share excluding non-recurring items of $0.493. This represents a substantial improvement from $0.216 in the previous quarter and $0.291 in the same period the prior year. Such growth suggests that the company has benefited from stronger operational execution and improved pricing dynamics across its business segments.

Diluted earnings per share tell a slightly more complex story. At $0.275, diluted EPS declined modestly compared with $0.295 recorded a year earlier, though it improved significantly from $0.066 in the preceding quarter. This divergence between adjusted and diluted results indicates that non-operational factors have influenced reported earnings, though the underlying operating trend remains positive.

Revenue performance has also shown encouraging signs. Revenue per share increased to $3.419, up from $3.196 in the previous quarter. This progression reflects modest but meaningful top-line improvement following several years of broader revenue stagnation.

Perhaps the most striking development lies in Chemtrade’s margin expansion. Gross margin has reached 24.3%, representing a ten-year high and far exceeding the company’s ten-year median margin of approximately 7.0%. This improvement signals that recent operational initiatives—particularly cost controls and pricing strategies—have materially strengthened the firm’s profitability profile.

Capital allocation has also contributed to earnings momentum. Over the past year, the company repurchased roughly 7.8% of its outstanding shares, reducing the share count and amplifying per-share earnings growth. Share buybacks at this scale can significantly enhance shareholder returns when executed alongside improving operating performance.

Looking ahead, consensus expectations imply moderate growth. Revenue is projected to rise from approximately $1.43 billion in 2025 to $1.56 billion in 2026. Earnings forecasts anticipate EPS reaching roughly $0.72 in the coming fiscal year and potentially $1.02 the year after. These projections suggest that analysts expect operational improvements to continue, albeit at a measured pace.

Industry conditions also provide some support for this outlook. The chemicals sector is expected to grow at roughly 5% annually over the coming decade, offering a steady demand backdrop for companies operating in essential industrial supply chains.

Taken together, Chemtrade’s profitability trends indicate that management has successfully stabilized and improved the business following periods of weaker performance. However, the durability of these gains remains an important consideration, particularly given the company’s historically uneven earnings trajectory.

Dividend Profile & Sustainability

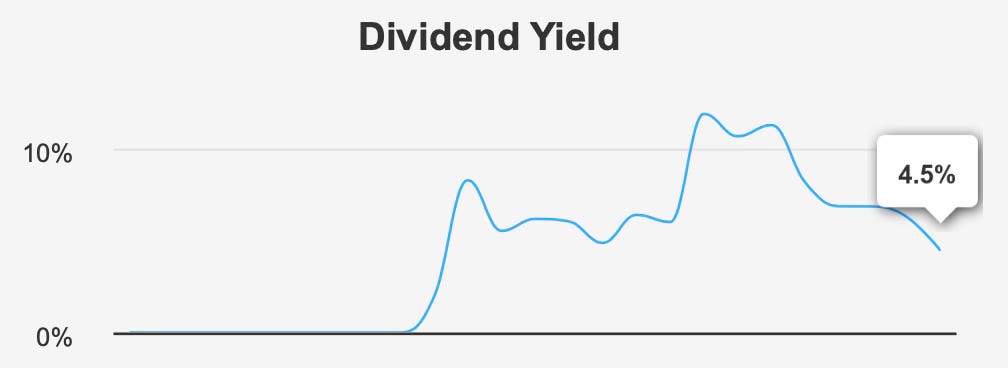

Chemtrade’s dividend profile is one of the most important components of its investment appeal. With a forward yield of approximately 4.5%, the stock offers an attractive income stream relative to many industrial companies.

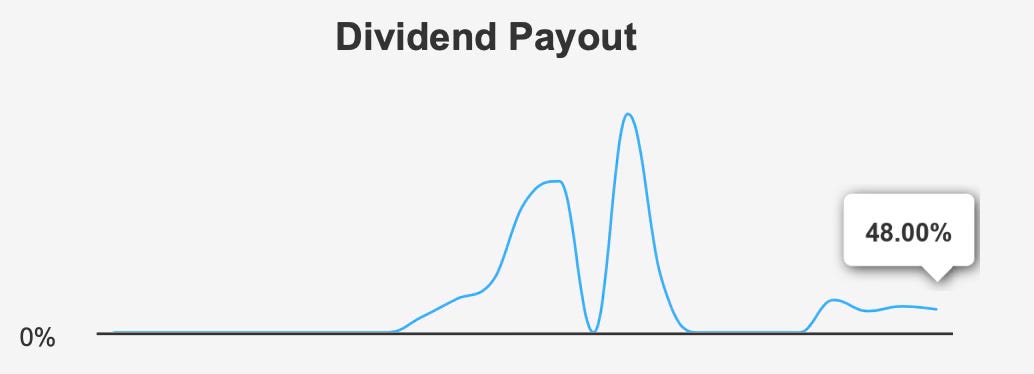

The sustainability of this yield appears reasonable based on current financial metrics. The dividend payout ratio sits near 48%, suggesting that roughly half of earnings are distributed to shareholders while the remaining portion can be reinvested in the business or used to reduce leverage. This level of payout generally provides a buffer against short-term earnings fluctuations.

Dividend coverage also remains adequate. With coverage around 1.24x, the company generates sufficient earnings to support its dividend commitments without relying on external financing.

Nevertheless, Chemtrade’s dividend growth history has been inconsistent. Over the past five years, dividend growth has actually declined by approximately 9.4%, reflecting earlier periods of operational weakness and financial restructuring. More recently, however, the trend has improved. Over the last three years, dividend growth has averaged about 3.2%, indicating a gradual return to expansion.

Forward expectations appear more optimistic. Forecasts suggest dividend growth could accelerate to roughly 15.6% over the next three to five years if earnings expansion continues. Such projections are largely tied to improving profitability and stronger capital efficiency.

The dividend calendar also remains predictable. The next ex-dividend date occurred on February 27, 2026, with payment scheduled for March 31, 2026. Chemtrade follows a consistent distribution schedule, reinforcing its role as an income-oriented security.

While the dividend yield remains appealing, investors should recognize that the current yield is near a ten-year low relative to the company’s own historical range. This dynamic largely reflects the recent appreciation in the stock price rather than a reduction in the dividend itself.

Ultimately, Chemtrade’s dividend profile appears stable under current conditions. Earnings coverage remains adequate, and operational improvements support the potential for moderate dividend growth. However, the company’s inconsistent long-term dividend track record suggests that investors should remain attentive to cyclical shifts in the underlying chemicals market.

Valuation Analysis: Assessing Market Pricing Relative to Intrinsic Value and Historical Multiples

Despite the company’s operational improvements, valuation metrics suggest that the current share price may already reflect a significant portion of the recovery narrative.

Intrinsic value estimates place fair value near $5.09 per share, well below the current market price of roughly $11. This gap implies a negative margin of safety exceeding 120%, indicating that the stock trades at a substantial premium to its modeled intrinsic value.

Traditional valuation multiples provide a somewhat mixed picture. On a forward basis, the stock trades around 11.5x expected earnings, slightly below the company’s ten-year median multiple of approximately 12.5x. Viewed in isolation, this could suggest modest valuation support if projected earnings growth materializes.

However, trailing metrics tell a different story. The trailing price-to-earnings ratio sits near 18.5x, above historical norms and reflecting the lag between improving earnings expectations and reported results.

Enterprise value metrics appear more favorable. The EV/EBITDA ratio of roughly 6.9x stands well below the ten-year median of about 11.7x, implying that the company may be relatively inexpensive when evaluated against operating cash flow.

Other valuation indicators are less supportive. The price-to-sales ratio of roughly 1.0 sits slightly above the long-term median of 0.71, while the price-to-book ratio near 2.3 exceeds the historical median of 1.44. These figures suggest that investors are currently assigning a premium to the company’s asset base.

Free cash flow valuation also appears somewhat stretched. The price-to-free-cash-flow ratio of roughly 12.3 stands above historical averages, indicating that the market may be valuing the company’s cash generation more aggressively than in the past.

Taken together, these metrics present a nuanced valuation picture. Certain operating metrics suggest relative affordability, particularly when viewed through enterprise value ratios. Yet the significant gap between intrinsic value estimates and the current market price raises concerns that the stock may already reflect optimistic expectations.

For dividend investors, valuation discipline remains important. While the income profile may appear attractive, purchasing the stock at elevated valuations could limit long-term total return potential.

Risk Assessment & Capital Structure Considerations

Chemtrade’s risk profile reflects a combination of financial stability improvements and lingering structural concerns.

From a capital structure standpoint, leverage appears manageable. The company’s debt-to-EBITDA ratio stands near 2.5x, placing it within a moderate leverage range for an industrial company. This level of debt does not appear excessive but does warrant monitoring, particularly given the cyclical nature of the chemicals sector.

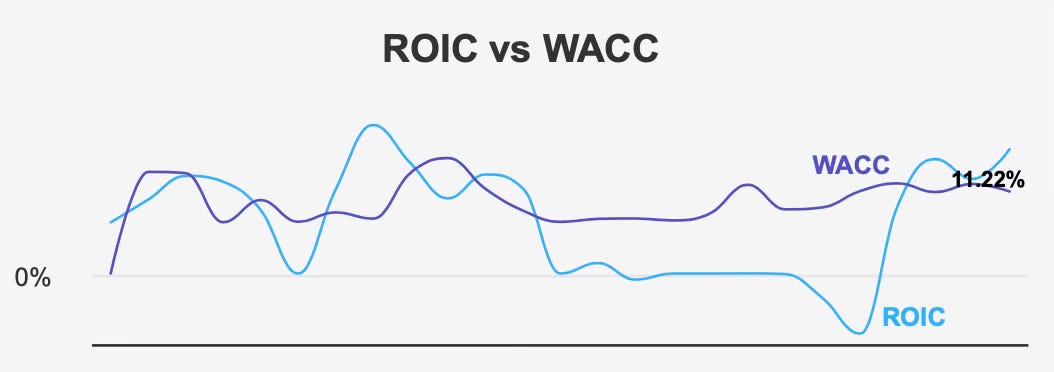

Return metrics indicate improving financial efficiency. The company currently generates a return on invested capital of approximately 11.3%, comfortably above its weighted average cost of capital of about 7.4%. This spread suggests that Chemtrade is now creating economic value rather than destroying it.

This represents a meaningful shift from historical trends. Over the past five years, the company’s median ROIC of roughly 6.3% fell short of the median WACC of about 7.4%, indicating that earlier capital allocation decisions were less efficient.

Other financial indicators provide mixed signals. Return on equity currently stands near 14.3%, reflecting improved profitability but also highlighting the company’s historically volatile earnings patterns.

More concerning is the company’s Altman Z-score of 1.0, which signals potential financial distress risk within the next two years. While this does not necessarily imply imminent solvency issues, it underscores the importance of continued operational stability.

Governance factors also merit attention. Insider ownership stands at 0%, meaning company executives and directors currently hold no equity stake in the business. This absence of insider ownership may raise questions about alignment between management and shareholder interests.

Institutional ownership remains relatively modest at approximately 11.2%, suggesting that large professional investors maintain a limited presence in the shareholder base.

Finally, liquidity considerations are worth noting. The stock trades an average of roughly 14,771 shares per day, indicating moderate but not high liquidity. Additionally, about 38% of trading occurs through dark pools, suggesting a notable level of off-exchange activity.

Overall, Chemtrade’s risk profile reflects improving operational performance but continued structural uncertainty. Investors must weigh these dynamics carefully when evaluating the stock as a long-term dividend holding.

Final Assessment

Chemtrade Logistics Income Fund presents a compelling but complex dividend investment case.

On one hand, the company has demonstrated clear operational improvement. Margins have expanded, capital efficiency has improved, and earnings momentum has strengthened. These developments support the sustainability of the company’s dividend and provide a foundation for moderate growth in shareholder distributions.

The current dividend yield of approximately 4.7% remains attractive, particularly given the manageable payout ratio and improving earnings outlook.

However, several factors temper this positive narrative. Long-term revenue growth remains weak, historical dividend growth has been inconsistent, and intrinsic value estimates suggest the current share price may already reflect optimistic expectations.

Valuation therefore becomes a central consideration. While certain operating multiples appear reasonable, the large premium to intrinsic value raises concerns about the margin of safety available to new investors.

For income-focused investors seeking stable yield, Chemtrade may remain a viable candidate, particularly if operational improvements continue. However, from a total return perspective, the current valuation suggests that future gains may be limited unless earnings growth materially exceeds expectations.

In short, Chemtrade represents a company in the midst of a genuine operational recovery—but one where the market may already be pricing in much of the turnaround.