Cheap for a Reason? A Dividend Investor’s Review of HP Inc.

Understanding whether HP’s shareholder payouts are supported by durable earnings

Investment Thesis: A High-Yield Distribution Supported by Cash Flow but Undermined by Structural Business Pressure

HP Inc. HPQ 0.00%↑ operates as one of the most established global vendors in personal computing and printing hardware, having focused exclusively on these segments since separating from its enterprise infrastructure business in 2015. Its revenue base is geographically diversified, with only about one-third generated in the United States, and its business model relies heavily on outsourced manufacturing and channel distribution partners.

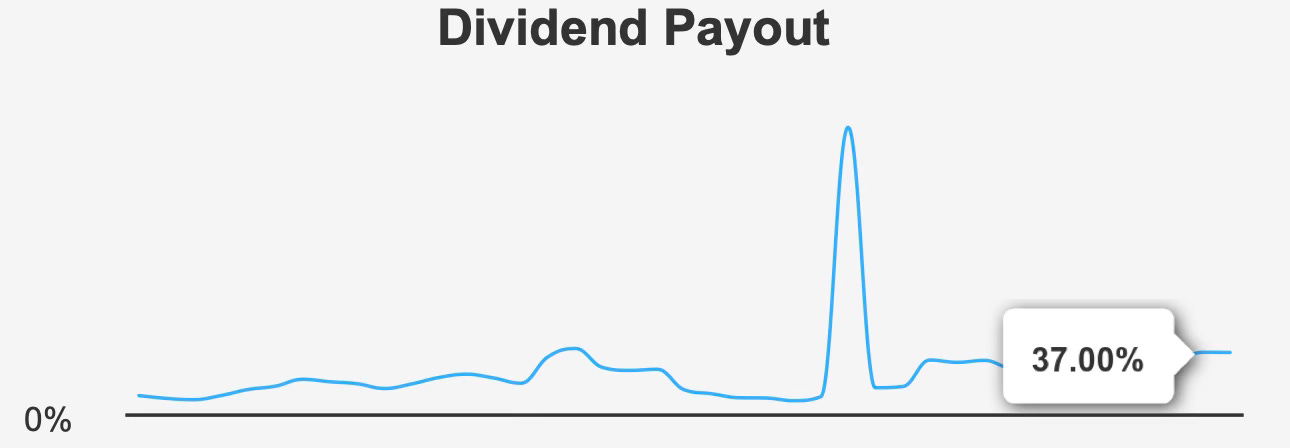

At first glance, the investment case appears straightforward. The stock offers a forward dividend yield of 6.5%, a payout ratio of 37.0%, and valuation multiples well below historical norms. These characteristics normally attract income investors searching for stable distributions supported by strong free cash flow.

However, the core issue is not the presence of cash generation — it is the durability of that cash generation.

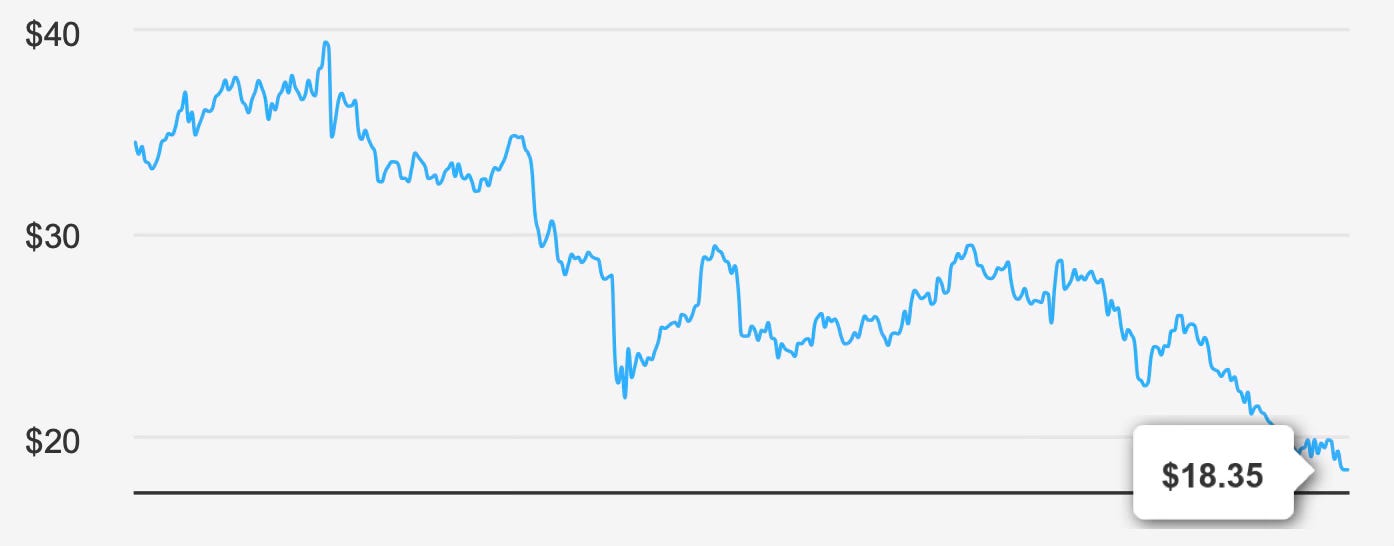

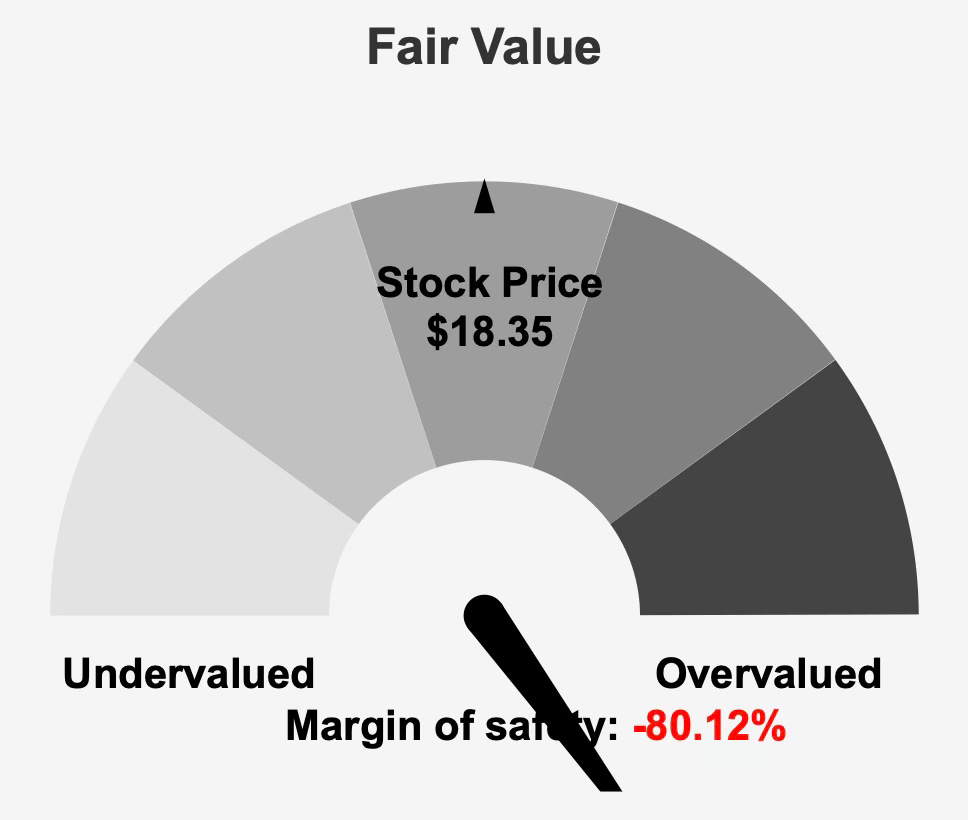

The company’s intrinsic value is estimated near $10.19 compared with a share price around $18, implying a deeply negative margin of safety near 80%. This discrepancy reflects a business whose accounting earnings and shareholder payouts appear healthier than its long-term economic outlook.

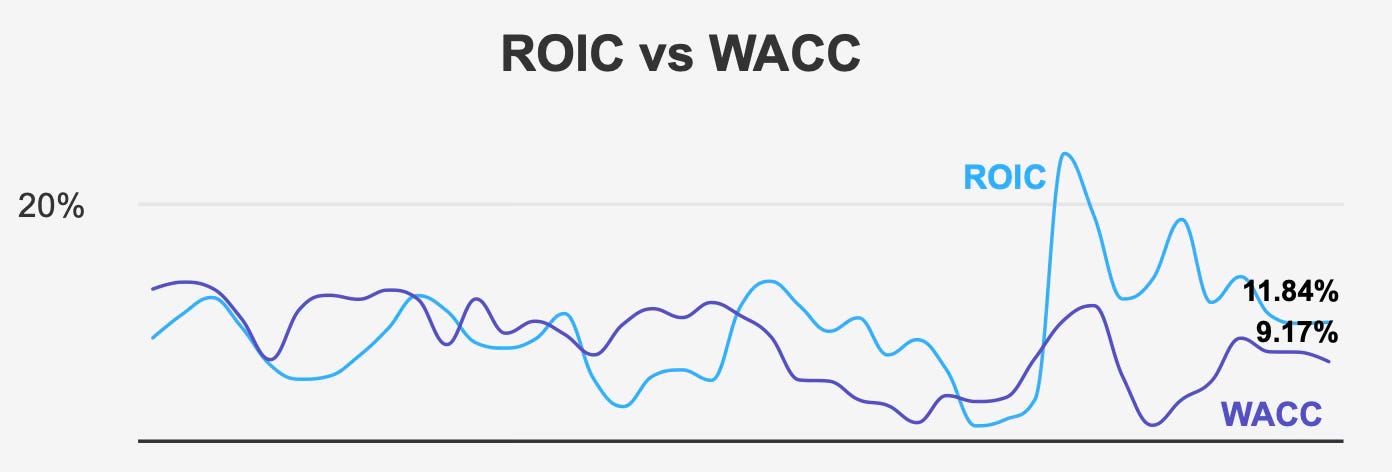

HP continues to produce returns on invested capital above its cost of capital, but the spread is narrowing. Meanwhile, operating margins have been declining approximately 2% annually over five years, revenue per share has weakened over a three-year period, and industry growth expectations remain modest.

The resulting investment profile is unusual: a company capable of paying a dividend comfortably today but whose underlying business trajectory raises doubts about its reliability over a full cycle.

For dividend investors, the key question is therefore not whether the current payout is covered — it clearly is — but whether the business supporting it is structurally stable enough to protect purchasing power over time.

Earnings Momentum & Profitability Trends

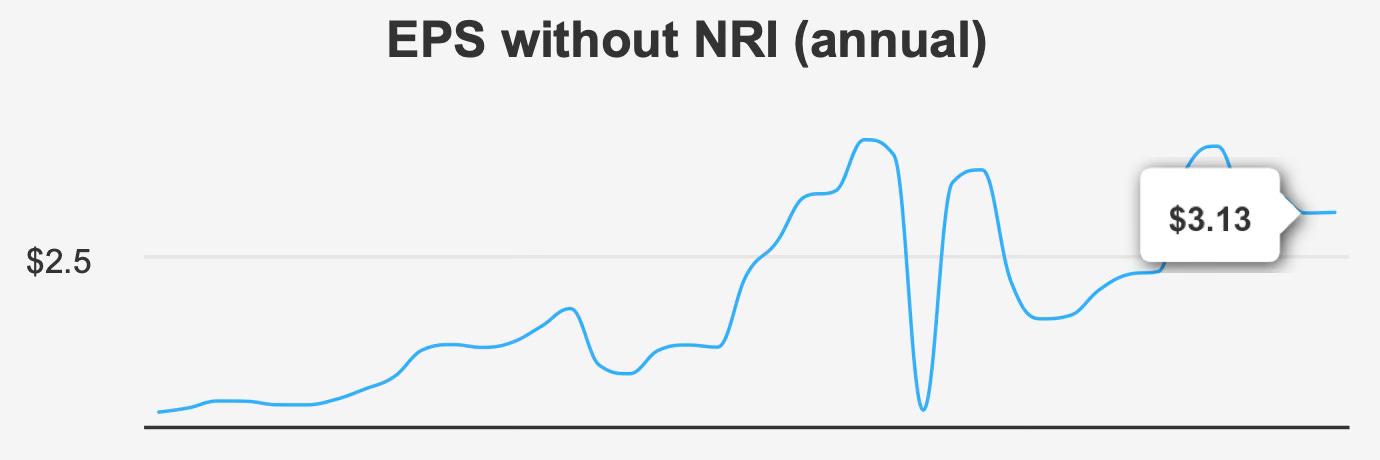

The latest reported quarter showed earnings per share excluding non-recurring items of $0.93, matching the same period a year earlier and improving from $0.75 in the prior quarter. Diluted EPS reached $0.84, slightly higher sequentially but still below last year’s comparable quarter.

This pattern characterizes HP’s earnings profile: stable rather than expanding. The company demonstrates recovery after short-term fluctuations, yet struggles to establish sustained growth momentum.

Revenue per share rose sequentially to $15.46 from $14.60, suggesting operational normalization rather than structural expansion. Looking forward, analyst expectations reinforce this view. Revenue is projected to reach $55.83 billion in 2026 and $57.30 billion by 2028, while earnings are expected to move from $2.76 to $2.99 over the same period.

These figures imply low-single-digit growth — effectively in line with inflation and replacement demand in mature hardware markets.

Profitability metrics are stronger than growth metrics. The company’s current return on invested capital stands at 11.8% compared with a weighted average cost of capital of 9.2%. This positive spread indicates economic value creation, although it has compressed from the five-year median ROIC of 13.2%.

Gross margin of 20.6% sits slightly below the five-year median but remains within long-term historical ranges, confirming that competitive pressures exist but have not yet structurally damaged profitability.

Shareholder returns have been supported by consistent buybacks. Over the past year, the company repurchased 1.9% of outstanding shares, while the ten-year reduction totals 7.5%. These repurchases enhance per-share metrics but do not represent organic growth.

Overall, HP’s earnings quality can be described as financially engineered stability rather than operational expansion — profits remain steady primarily due to disciplined capital allocation and cost control rather than improving market demand.

Dividend Profile & Sustainability

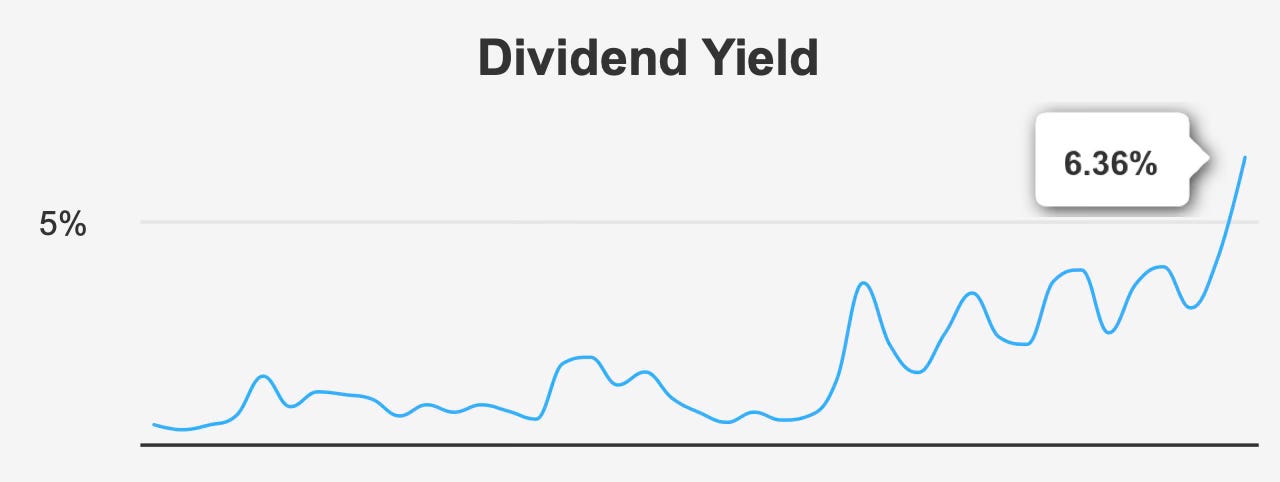

The company’s dividend policy is clearly shareholder-oriented. The quarterly dividend recently increased from $0.2894 to $0.30 per share, continuing a multi-year pattern of steady growth.

Over five years, the dividend has grown at a rate of 10.8%, moderating to 5.0% over three years and expected to expand around 5–6% annually going forward.

With a forward yield of 6.4%, the stock offers income roughly double the sector median near 3.2%. On the surface, the payout appears highly attractive.

More importantly, coverage is adequate. The payout ratio of 37.0% and dividend coverage ratio of 2.29 indicate a substantial earnings buffer. In isolation, these figures suggest a safe dividend.

The issue lies in trend rather than level.

Dividend safety ultimately depends on the durability of free cash flow, and HP’s growth outlook is modest. Forecast earnings expansion remains minimal, implying dividend growth will gradually converge toward earnings growth — roughly mid-single digits.

Additionally, declining operating margins and weakening revenue per share over multiple years introduce risk that future coverage may compress if hardware demand softens further.

Therefore, the dividend today appears sustainable, but its long-term reliability depends on stabilization of a mature industry rather than expansion of a growing one.

This distinction matters: the payout is covered by current earnings, yet not strongly protected against structural decline.

Valuation: Low Multiples Reflect a Mature Business Rather Than a Bargain Opportunity

HP trades at valuation levels typically associated with distressed or shrinking businesses.

The trailing P/E ratio stands near 6.9x versus a ten-year median of 9.5x, while forward earnings trade around 6.0x. Enterprise value to EBITDA sits at 5.8x compared with a historical median of 7.9x, and the price-to-sales ratio of 0.32 is at a decade low.

Price to free cash flow near 6.2x also sits below historical norms.

Taken together, these metrics would normally suggest undervaluation. Yet intrinsic value calculations indicate otherwise, placing fair value far below the current share price.

The explanation lies in growth expectations.

Markets often assign low multiples not because a company is cheap but because its future earnings power is expected to erode. The declining analyst price targets — falling from $27.78 to $23.97 — support this interpretation.

The valuation therefore reflects a business transitioning from growth to managed decline: stable cash generation but limited reinvestment opportunity.

For income investors, the low multiple should be interpreted as compensation for risk rather than margin of safety.

Risk Assessment & Capital Structure Considerations

The company’s balance sheet and operational risks are central to evaluating dividend reliability.

Debt-to-EBITDA stands at 2.63, a manageable but meaningful level of leverage. Combined with an Altman Z-score of 1.56, the firm sits in a statistical distress zone, implying elevated financial risk under adverse conditions.

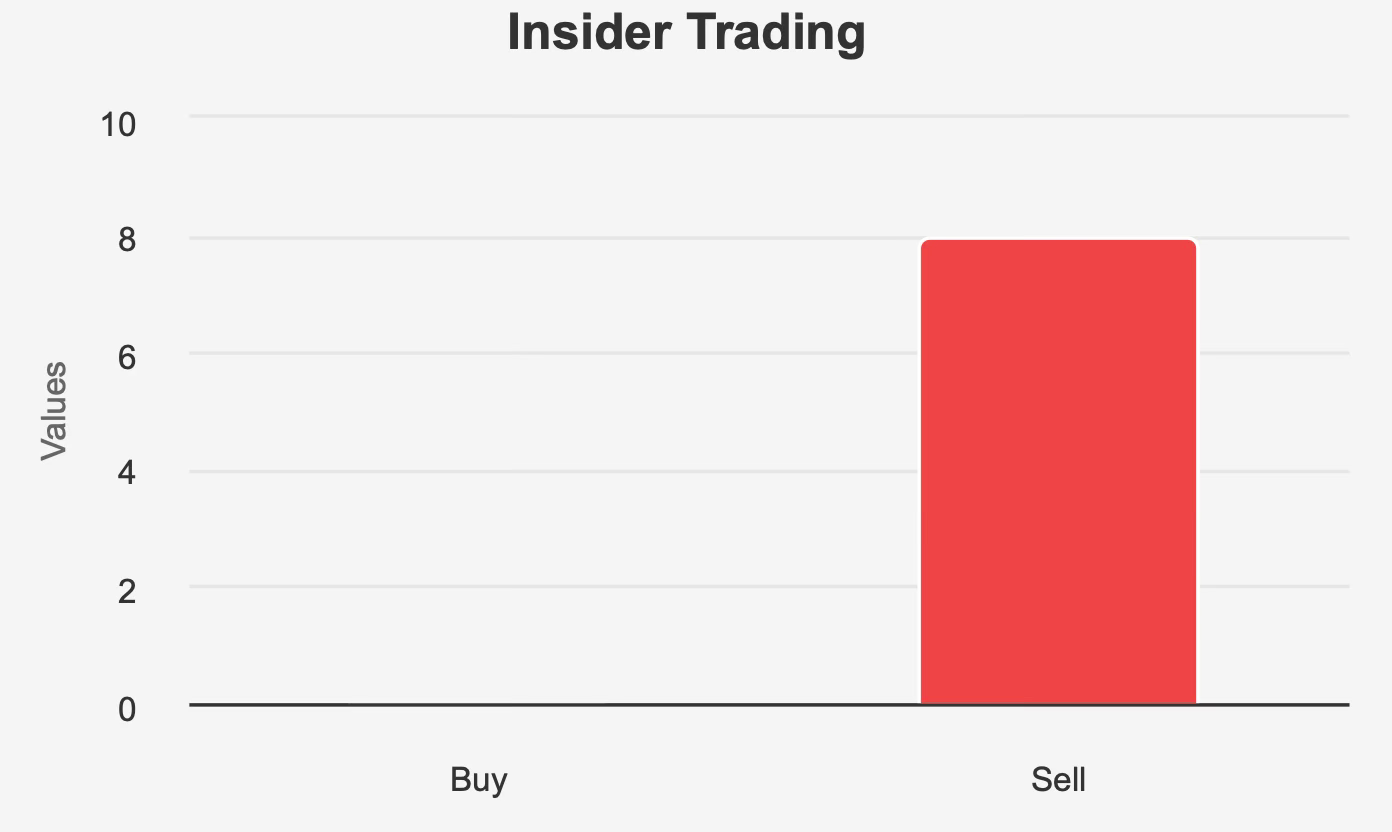

Insider behavior adds caution. Over the past year, eight insider sales occurred with no insider purchases, including nearly 92,000 shares sold in the past three months. While insider ownership is only 0.8%, the persistent selling trend suggests limited confidence in near-term upside.

Operational indicators also show pressure. Operating margins have declined roughly 2% annually over five years, and patent filings are projected to fall to just one in 2026, hinting at slowing innovation activity.

On the positive side, institutional ownership of 82.9% provides some stability, and financial reporting quality appears reliable with a Beneish score indicating low manipulation risk.

The resulting risk profile is asymmetric: limited upside due to weak growth, but meaningful downside if earnings weaken.

Final Assessment

HP Inc. represents a classic income stock dilemma.

The dividend is well covered, grows modestly, and provides an above-average yield. Cash flow remains sufficient, profitability exceeds cost of capital, and valuation multiples are low.

Yet the underlying business shows characteristics of gradual structural erosion — declining margins, limited growth, reduced innovation activity, and elevated financial risk indicators.

This creates a paradox. The dividend appears safe in the near term but uncertain over the long term. Investors are effectively exchanging growth and capital preservation for current income.

For investors prioritizing immediate yield and willing to accept potential capital deterioration, the stock may function as a tactical income holding.

For long-term dividend growth investors seeking durable purchasing power, the combination of weak intrinsic value support and structural industry pressure reduces its attractiveness.

In practical terms, the market is pricing HP not as a growing company but as a distributing company — one returning cash because reinvestment opportunities are limited.

The yield is real. The sustainability beyond a full business cycle is less certain.