Caterpillar Inc.: Premium Franchise, Premium Price

Durable Operating Strength and Dividend Discipline Confront Valuation Extremes

Investment Thesis: Durable Global Industrial Leader Trading at an Unsustainable Premium

Caterpillar Inc. CAT 0.00%↑ stands as the world’s leading manufacturer of construction and mining equipment, off-highway diesel and natural gas engines, industrial gas turbines, and diesel-electric locomotives. With operations spanning approximately 190 countries and supported by an independent dealer network of more than 150 dealers operating roughly 2,800 facilities, the company maintains a globally balanced revenue base. Construction exposure skews more domestic, while the resource industries, energy, and transportation segments exhibit broader international diversification. Market share approaches 20% across many product categories, underscoring Caterpillar’s entrenched competitive positioning.

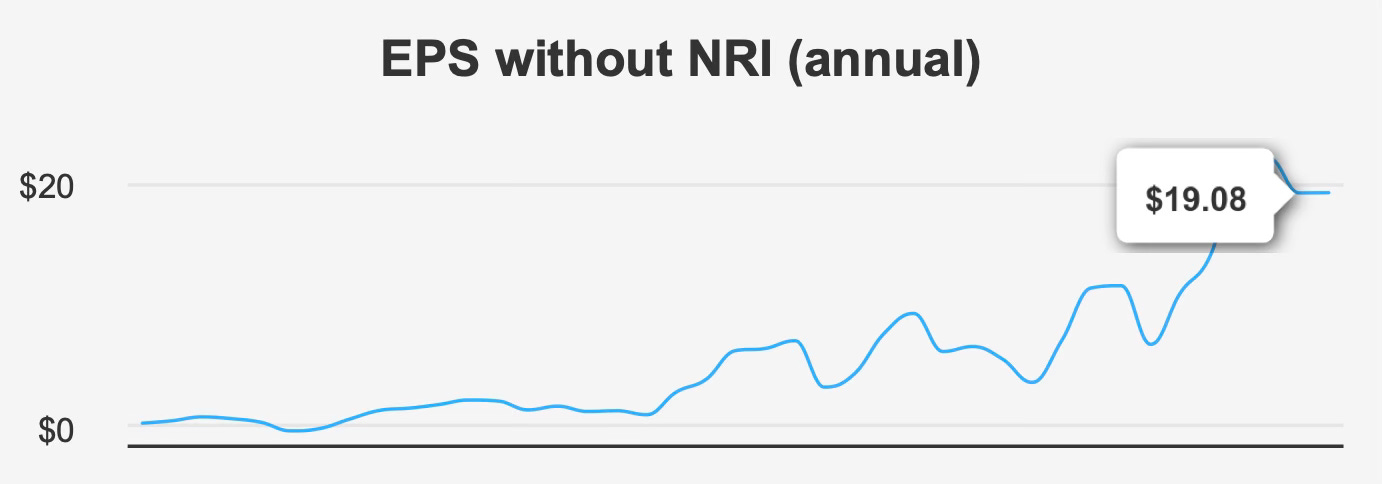

Operationally, the company has delivered consistent growth and disciplined capital allocation. Over the past five years, earnings per share excluding non-recurring items have compounded at 25.2% annually, with a 10-year compound rate of 17.3%. Revenue growth has also been steady, advancing at 13.3% over five years and 7.4% over ten. These figures confirm that Caterpillar is not merely cyclical, but structurally positioned to benefit from infrastructure investment, equipment replacement cycles, and technological modernization.

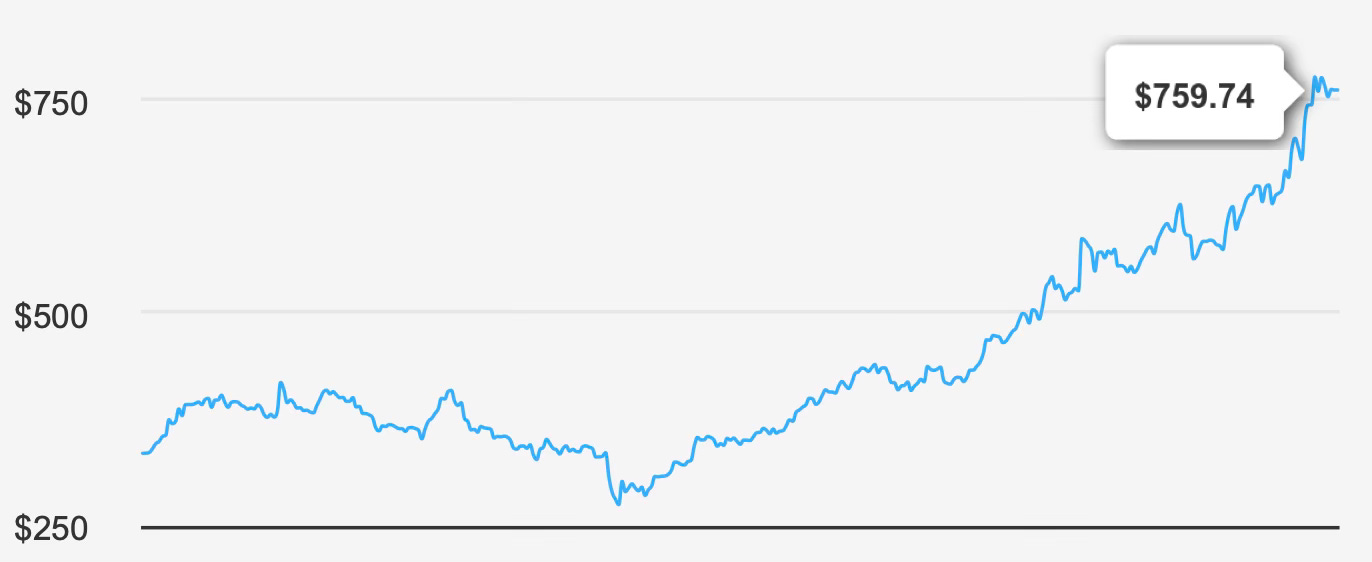

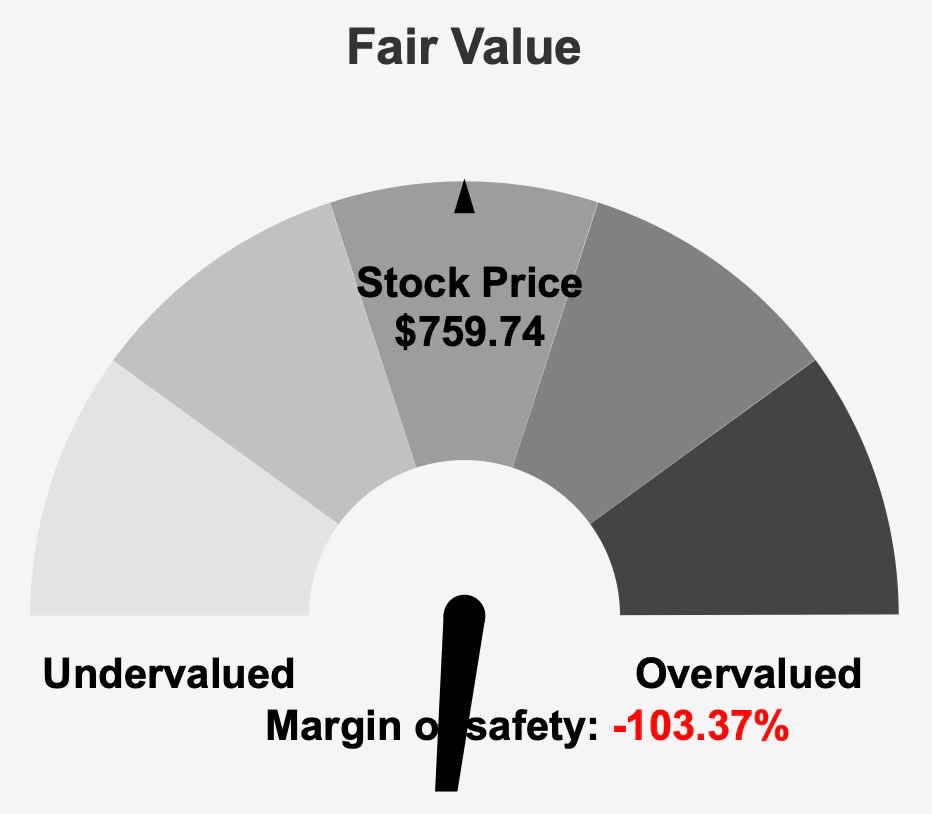

Yet despite these strengths, valuation now defines the investment debate. Shares trade at $759, while intrinsic value is estimated at $373.55. The resulting margin of safety stands at -103.4%, indicating that the market price is more than double the estimated fair value. This extreme disconnect materially shifts the risk-reward balance. Even high-quality industrial franchises struggle to justify such pricing without sustained above-trend growth.

Caterpillar’s long-term fundamentals remain solid. However, at current levels, investors are paying a premium that leaves little room for execution risk or macroeconomic moderation.

2. Earnings Momentum & Profitability Trends

Caterpillar’s most recent quarterly performance illustrates ongoing operational stability. For the quarter ending December 31, 2025, earnings per share excluding non-recurring items reached $5.16, modestly above the prior quarter’s $4.95 and slightly ahead of $5.14 recorded in the comparable period last year. Revenue per share improved meaningfully to $40.80 from $37.46 in the prior quarter, reflecting continued top-line resilience.

Margin discipline remains evident. Gross margin stands at 31.8%, consistent with the five-year median, though below the 10-year high of 36.0%. This stability suggests effective cost control despite fluctuations in raw material pricing and supply chain dynamics. The ability to sustain gross margins near long-term medians during a volatile operating backdrop reinforces Caterpillar’s pricing power and operational efficiency.

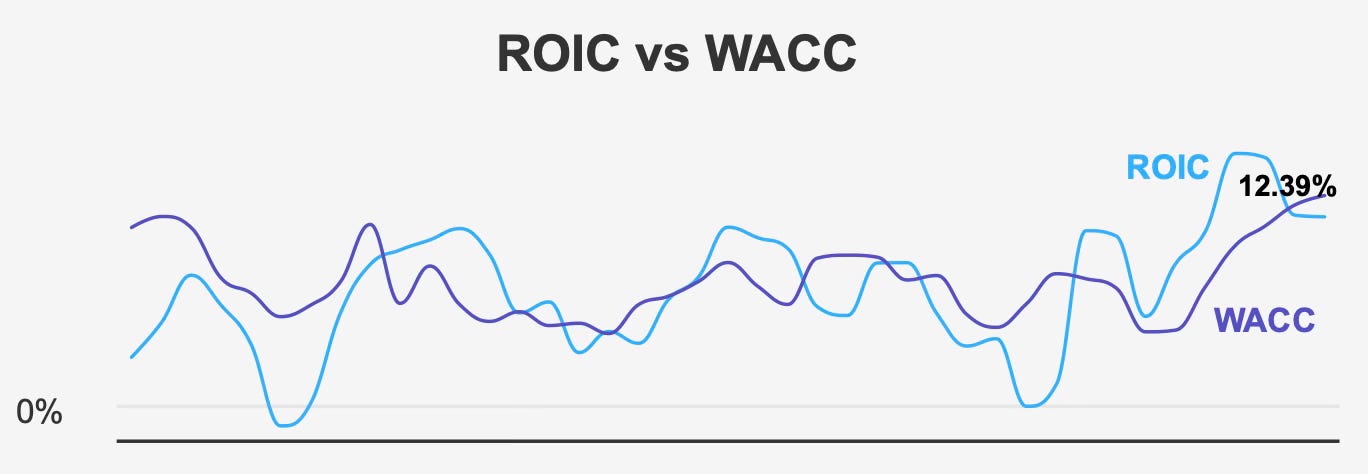

From a capital efficiency standpoint, historical performance has been constructive. Over the past five years, median return on invested capital measured 12.5%, exceeding a weighted average cost of capital of 10.5%. That spread indicates consistent economic value creation during the period. Currently, however, ROIC stands at 12.39% while WACC has risen to 13.78%, implying that near-term returns are trailing capital costs. While this may reflect cyclical factors or rising financing costs, it bears monitoring. Sustained divergence could weigh on long-term value creation.

Return on equity remains exceptionally strong at 45.24%, demonstrating efficient utilization of shareholder capital. The company’s ongoing share repurchase program further amplifies per-share metrics. Over the past year, Caterpillar reduced its share count by 2.6%, closely aligned with its 10-year average buyback rate of 2.4%. This steady repurchase cadence supports earnings growth and reinforces management’s commitment to shareholder returns.

Looking forward, analysts project revenue to expand from $73.9 billion in 2026 to $85.9 billion by 2028. Earnings per share are estimated at $22.73 for the next fiscal year and $27.42 the following year. These projections imply continued earnings momentum, albeit at a more moderate pace than the exceptional five-year historical CAGR. Industry forecasts call for approximately 4% annual growth over the next decade, reflecting a normalization of expansion rates after a period of elevated demand.

The earnings trajectory remains favorable, but growth expectations embedded in the current share price appear far more aggressive than consensus forecasts suggest.

3. Dividend Profile & Sustainability

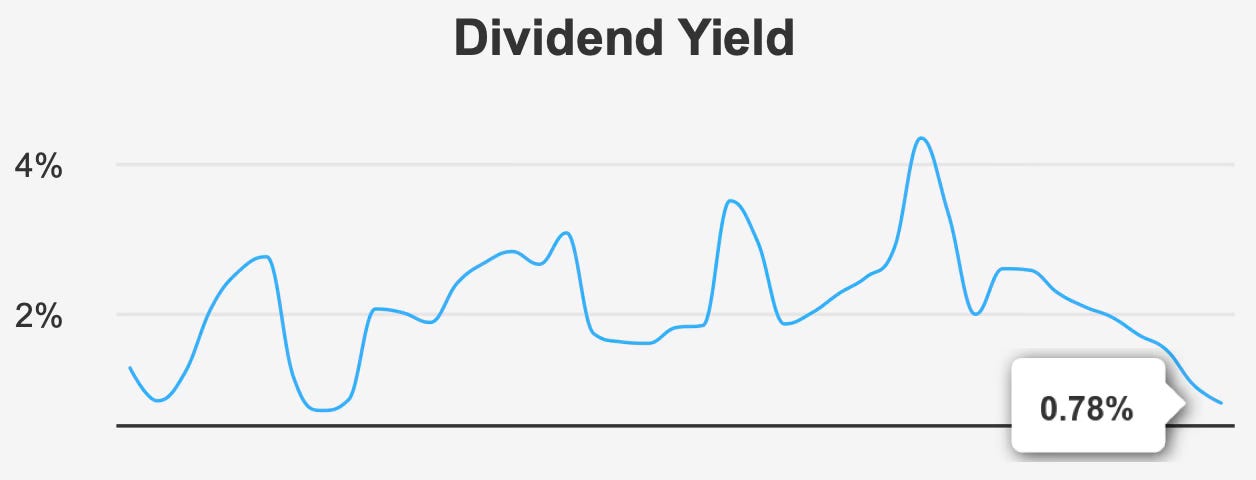

Caterpillar’s dividend profile reflects consistency rather than high yield. The forward dividend yield stands at 0.8%, near a 10-year low. For income-oriented investors, the current yield is modest. However, the company compensates through steady growth and conservative payout management.

The most recent quarterly dividend increased from $1.41 to $1.51 per share, reinforcing the company’s commitment to annual dividend expansion. Over the past five years, dividend growth has averaged 7.5%, while the three-year growth rate is slightly higher at 8.1%. Forecasted dividend growth of 6.3% over the next three to five years suggests continued, though measured, increases.

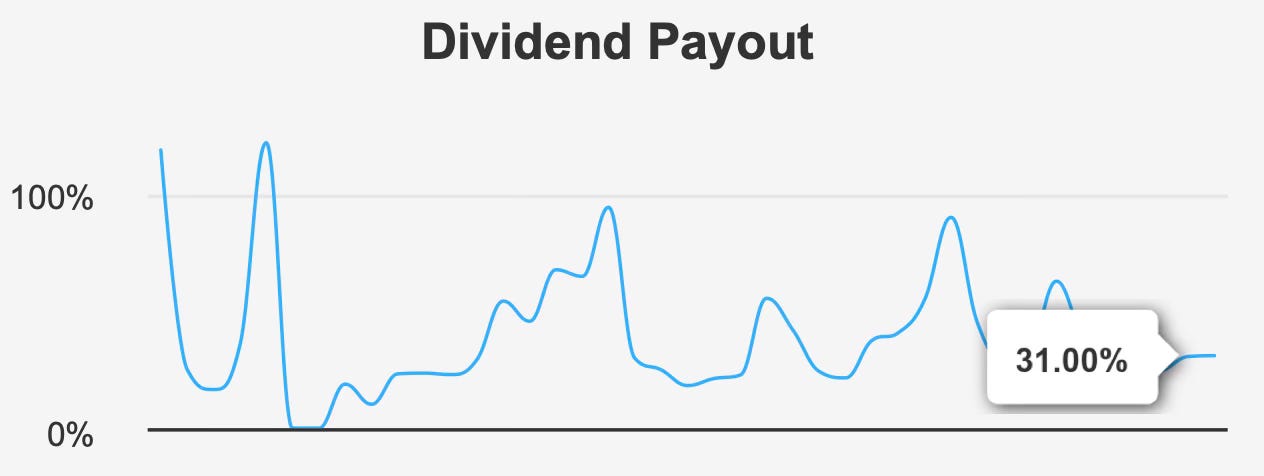

Importantly, dividend sustainability metrics remain solid. The payout ratio is 31%, providing significant headroom for both reinvestment and future dividend growth. Dividend coverage stands at 3.22x, offering an additional cushion should operating conditions soften.

Balance sheet leverage is manageable, though not conservative. Debt-to-EBITDA measures 3.03x, placing the company at the higher end of moderate leverage within the industrial sector. Nonetheless, financial stability indicators are strong. An Altman Z-score of 4.96 signals low bankruptcy risk, and a Beneish M-Score of -2.47 suggests low probability of earnings manipulation.

Caterpillar’s dividend policy reflects disciplined capital allocation. Management balances share repurchases and dividend growth without overextending leverage. While the yield itself is modest, the dividend appears secure and positioned for continued expansion in line with earnings growth.

For investors seeking durable dividend growth rather than high immediate income, the profile remains credible. However, the valuation premium significantly compresses the effective yield on new capital deployed at current prices.

4. Valuation Analysis: Elevated Multiples Relative to Intrinsic Value and Historical Norms

Valuation represents the most pressing concern. At $759.74 per share, Caterpillar trades at a substantial premium to its estimated intrinsic value of $373.55. The implied negative margin of safety of -103.4% suggests that investors are pricing in optimistic assumptions well beyond base-case forecasts.

Forward earnings are valued at 33.6x, materially above the 10-year median of 18.4x. On an enterprise basis, trailing EV/EBITDA stands at 27.0x, approaching its 10-year high of 27.7x. These multiples indicate that the market is assigning near-peak valuation levels to the business.

Other valuation metrics reinforce the same conclusion. The price-to-sales ratio of 5.3x sits close to its 10-year high of 5.4x. Price-to-book measures 16.6x, again near the upper bound of its historical range. Price-to-free-cash-flow of 48.0x reflects a substantial premium placed on the company’s cash generation.

While analyst price targets have trended upward, with the latest target at $699.04, even that figure sits below the current market price. The divergence between intrinsic value and market pricing introduces asymmetric downside risk should growth expectations moderate.

It is not uncommon for high-quality industrial leaders to command premium multiples during favorable economic cycles. However, valuation must ultimately reconcile with earnings power. At present levels, Caterpillar’s multiples imply sustained above-trend expansion and minimal macro disruption—assumptions that may prove demanding over a full economic cycle.

5. Risk Assessment & Capital Structure Considerations

Caterpillar’s risk profile is mixed but generally stable. Financially, the company is sound. The Altman Z-score of 4.96 signals low credit risk, and leverage at 3.03x Debt-to-EBITDA remains within manageable bounds. High institutional ownership of 71.95% suggests confidence among large asset managers, while insider ownership remains limited at 1%.

However, insider activity presents a noteworthy trend. Over the past three months, there have been 13 insider sales and no purchases. Over six months, 20 sales were recorded against a single buy, and over the past year, 22 sales compared with three buys. In the most recent three-month period alone, 155,369 shares were sold across 13 transactions. While insider selling does not inherently signal fundamental deterioration, the absence of insider buying at elevated valuation levels may reinforce concerns about limited near-term upside.

Liquidity remains strong, with daily trading volume of approximately 2.0 million shares compared to a two-month average of 2.7 million. Roughly 24.2% of trading volume occurs in dark pools, suggesting meaningful institutional participation.

Government contract activity has fluctuated meaningfully, peaking at $195.4 million in 2022, declining in 2023, then projected to rise sharply to $380.9 million in 2024 and $418.9 million in 2025 before falling to $46.0 million in 2026. Similarly, patent filings were stable between 340 and 362 annually from 2021 through 2025 before a projected drop to 50 in 2026. While these forward projections may reflect strategic shifts, they underscore potential variability in revenue sources and innovation cadence.

The primary risk, however, remains valuation compression. Should earnings growth revert toward the projected long-term industry rate of roughly 4%, multiple contraction could materially impact total returns even if operational performance remains sound.

Final Assessment

Caterpillar is a high-quality industrial franchise with durable competitive advantages, disciplined capital allocation, and a credible dividend growth record. Earnings momentum remains positive, profitability metrics are strong, and financial stability is not in question. The company has historically generated economic value, and its balance sheet supports continued shareholder returns.

Yet the investment case is constrained by valuation. With shares trading at $759 against an intrinsic value of $373.55, investors are paying more than twice estimated fair value. Forward multiples near historical peaks leave limited margin for error. Even steady mid-single-digit revenue growth and high-single-digit dividend growth may not justify current pricing.

For long-term dividend investors, Caterpillar remains fundamentally attractive—but not at any price. At present levels, the stock reflects optimism that exceeds reasonable expectations embedded in consensus growth forecasts.

Operational strength alone does not eliminate valuation risk. Until the price better aligns with intrinsic value and historical valuation norms, the risk-reward profile appears unfavorable despite the company’s enduring quality.