Cardinal Energy: High Yield, Thin Margin of Safety

A closer look at the sustainability of a 7% dividend amid declining earnings and stretched valuation.

Investment Thesis: A High Dividend Yield Supported by Commodity Cash Flow but Challenged by Earnings Stagnation and Valuation Premium

Cardinal Energy Ltd operates as an oil-focused Canadian exploration and production company with operations concentrated in Alberta, British Columbia, and Saskatchewan. The company generates the majority of its revenue from crude oil, natural gas, and natural gas liquids, positioning it directly within the cyclical dynamics of commodity-driven energy markets.

At first glance, Cardinal Energy’s dividend profile appears attractive for income-oriented investors. The stock offers a forward dividend yield of roughly 7.1%, placing it above many traditional income opportunities across the energy sector. The company also distributes dividends monthly, a structure that tends to appeal to investors seeking regular cash flow. However, beneath this headline yield lies a more complicated financial picture that raises questions about sustainability and valuation.

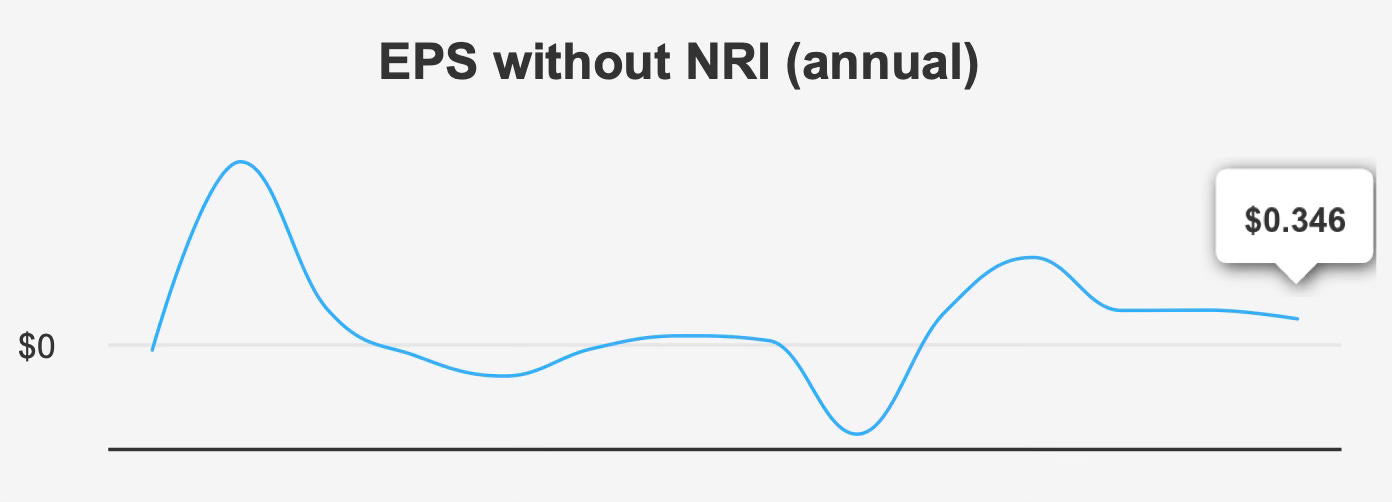

The most significant issue is the absence of long-term earnings growth. Over both the past five-year and ten-year periods, annual earnings per share excluding non-recurring items have effectively remained flat. This stagnation limits the company’s ability to organically expand dividend payments or support rising distributions without relying on elevated payout ratios.

Revenue growth offers a somewhat more positive backdrop. Sales have grown at an annualized rate of approximately 8.7% over the past five years, though the longer ten-year trajectory shows only about 0.6% annual expansion. Forecasts suggest revenue may rise from roughly $342.8 million in 2025 to about $392 million by 2027, implying moderate growth tied largely to production levels and commodity pricing.

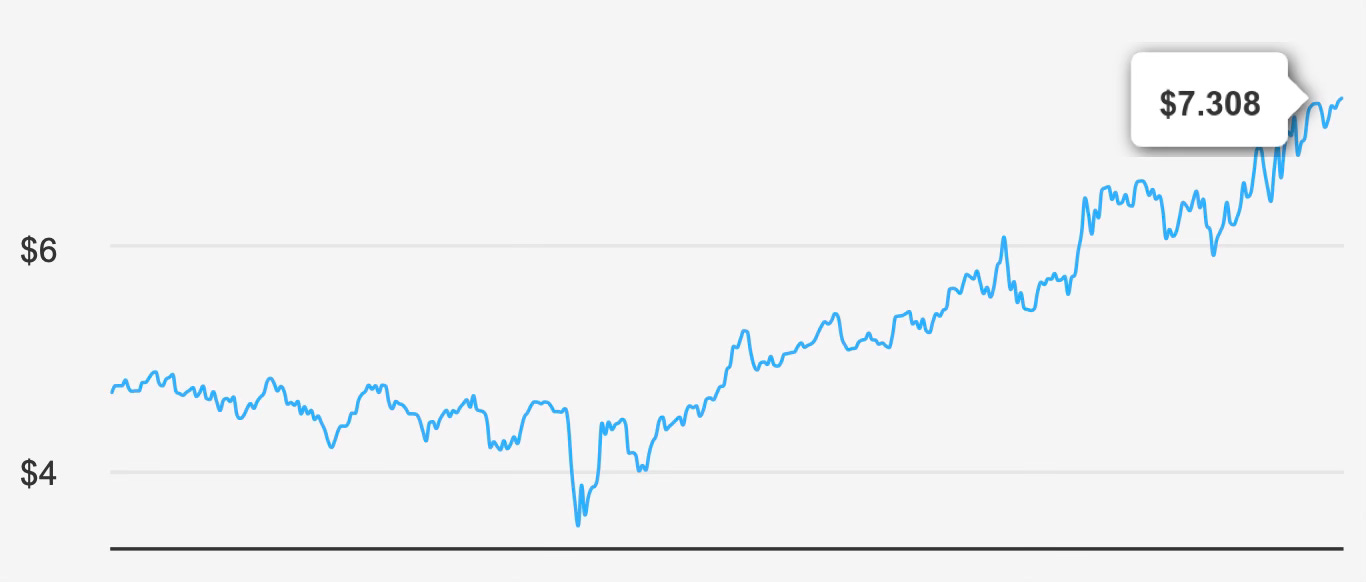

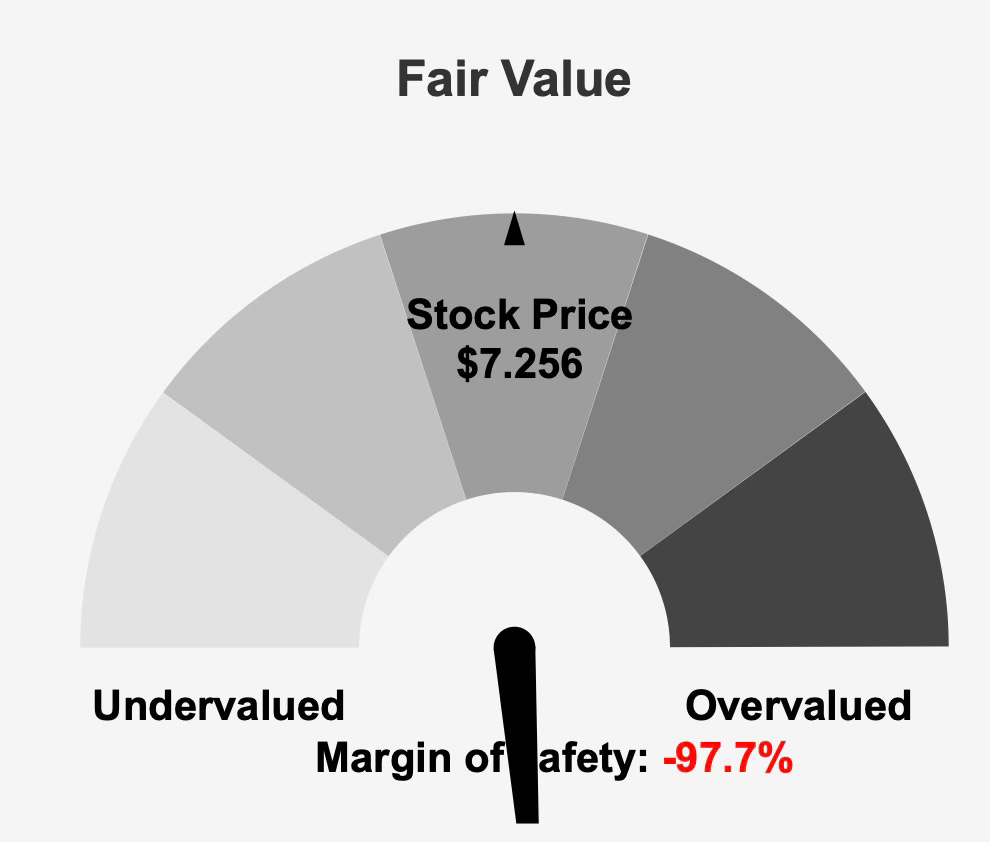

Despite this modest growth outlook, the market currently prices Cardinal Energy at levels that appear difficult to justify based on underlying fundamentals. The shares trade around $7 while estimated intrinsic value stands near $3.67, implying a deeply negative margin of safety. Such a gap indicates that the market may be assigning a premium to the company’s income characteristics despite weakening earnings momentum.

The result is a stock that combines appealing income with structural concerns. While commodity exposure and disciplined capital management may continue to support cash flow, the combination of stagnant earnings, elevated payout ratios, and stretched valuation metrics significantly weakens the long-term investment case.

For investors focused primarily on stable and growing dividends rather than current yield alone, these dynamics require careful scrutiny.

Earnings Momentum and Profitability Trends

Recent operating performance highlights the pressures facing Cardinal Energy’s earnings profile. In the quarter ending September 30, 2025, the company reported earnings per share excluding non-recurring items of $0.063, declining from $0.074 in the previous quarter and down sharply from $0.122 recorded in the same period a year earlier. Diluted earnings per share came in slightly higher at $0.065, but the broader trend still points toward declining profitability.

Revenue per share followed a similar pattern. The most recent quarterly figure of $0.571 slipped from $0.582 in the prior quarter and from $0.687 in the year-earlier period. This downward trajectory indicates that recent operating performance has not kept pace with earlier results, potentially reflecting commodity price volatility, operational costs, or production dynamics.

Margins reinforce this view of modest erosion in profitability. Gross margin for the quarter reached 62.3%, below the company’s five-year median of 64.2% and meaningfully under its ten-year high of roughly 66.0%. Although still robust relative to many industries, the decline suggests that operational efficiency or commodity pricing may be placing pressure on profitability.

Capital allocation has included consistent share repurchases, though the magnitude has been relatively modest. Over the past decade, the company has repurchased about 11.1% of its shares outstanding. During the past year alone, the buyback ratio stood near 0.9%. These repurchases can support earnings per share by reducing the share count, yet the declining EPS trend suggests that buybacks alone have not been sufficient to offset broader earnings pressures.

Looking forward, earnings forecasts remain cautious. Analysts expect earnings per share to reach approximately $0.286 in the next fiscal year before declining to roughly $0.206 in the following year. This projected contraction partially explains the elevated forward valuation multiples currently embedded in the stock price.

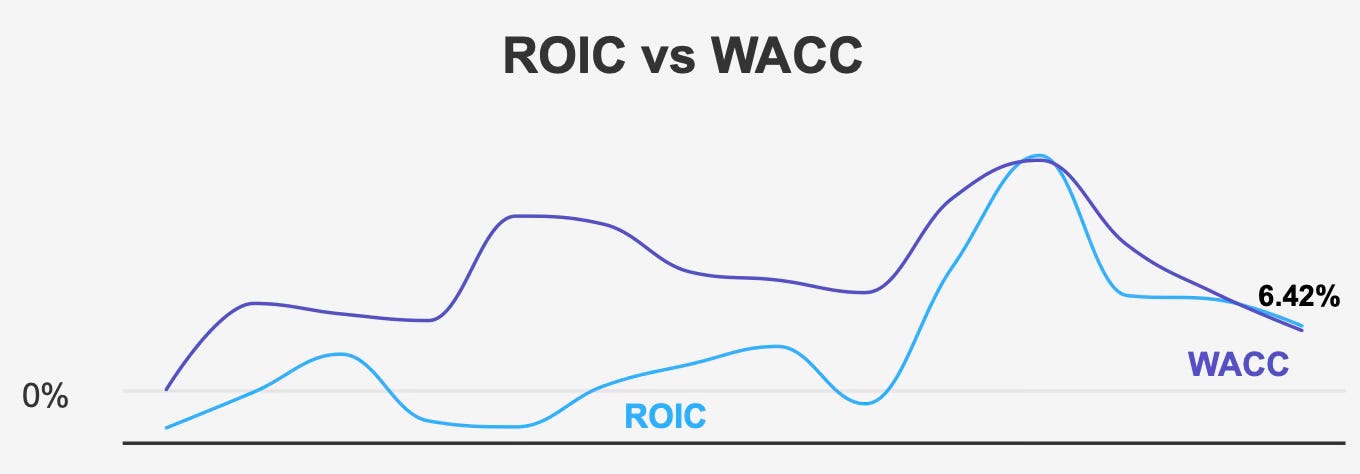

Despite these concerns, the company has shown some improvement in capital efficiency. Historically, Cardinal Energy generated returns on invested capital below its cost of capital. Over the past five years, median ROIC of about 9.4% trailed a median weighted average cost of capital near 14.6%, implying that the business was not consistently generating economic value during that period.

More recently, however, the relationship has improved. Current ROIC stands near 6.5% while WACC has declined to approximately 6.0%. Although the spread remains modest, the shift suggests that Cardinal Energy is once again generating returns slightly above its cost of capital. This improvement likely reflects a combination of reduced financing costs and adjustments to capital allocation.

While the margin between ROIC and WACC is thin, the reversal is nevertheless a positive development and indicates incremental progress in capital discipline.

Dividend Profile and Long-Term Sustainability of Shareholder Distributions

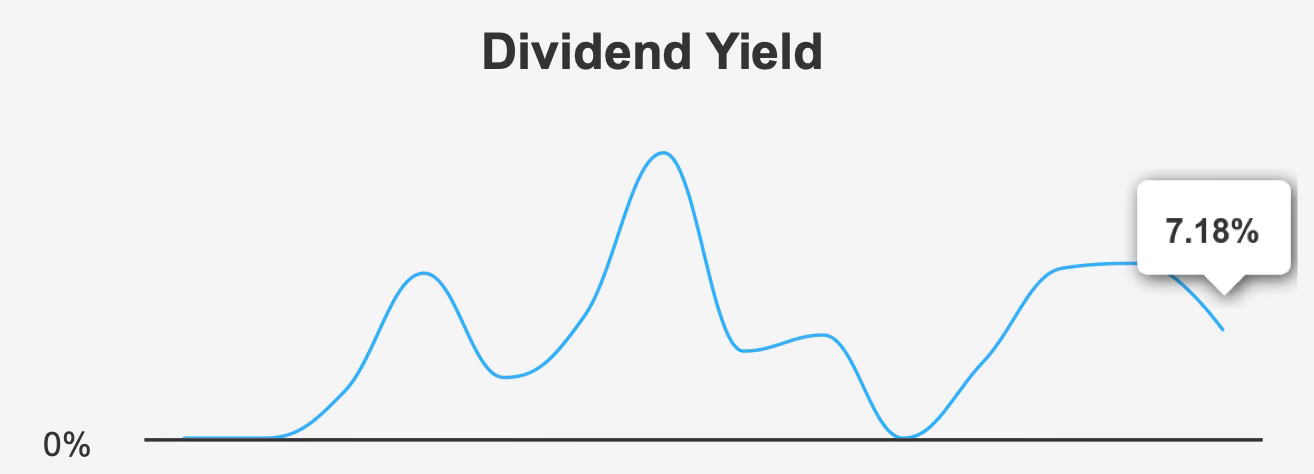

The most prominent feature of Cardinal Energy’s investment appeal is its dividend yield. At roughly 7.18% on a forward basis, the distribution provides a level of income that exceeds many traditional dividend sectors. The company pays dividends monthly, and the most recent ex-dividend date occurred on February 27, 2026, with payment scheduled for March 16, 2026.

However, the sustainability of this income stream is less certain when examined through the lens of payout ratios and growth history.

Dividend growth has been effectively nonexistent. Over both the three-year and five-year periods, the dividend growth rate stands at 0%. In other words, while the company has maintained its dividend, it has not increased it during that time. For long-term dividend investors who rely on income growth to offset inflation, this stagnation significantly reduces the attractiveness of the payout.

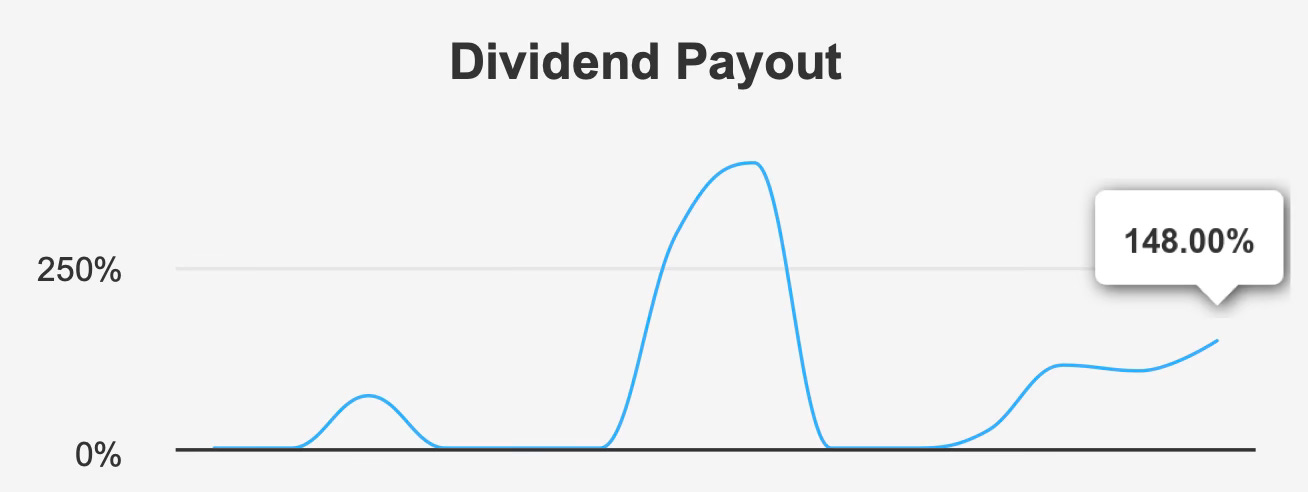

The payout ratio is even more concerning. Cardinal Energy currently distributes roughly 148% of its earnings as dividends, well above the historical median payout ratio of about 101%. A payout ratio above 100% indicates that the company is paying more in dividends than it generates in earnings, meaning the distribution must be supported either by cash reserves, borrowing, or favorable commodity conditions.

Dividend coverage metrics reinforce this concern. The company’s dividend coverage ratio is approximately 0.66, suggesting that current earnings are insufficient to fully fund the dividend.

On the positive side, the balance sheet remains relatively manageable. Debt to EBITDA stands at about 1.0x, indicating that the company carries modest leverage and retains capacity to service its debt obligations. This low leverage provides a buffer that could help maintain the dividend during temporary earnings fluctuations.

Nevertheless, relying on balance sheet flexibility rather than earnings growth is not a sustainable long-term dividend strategy. Unless profitability improves meaningfully, the company may eventually face pressure to reduce the payout or maintain it indefinitely without growth.

For income investors, the distinction between a high yield and a sustainable yield is critical. In Cardinal Energy’s case, the current yield is attractive, but the absence of earnings growth and the elevated payout ratio create meaningful long-term risk.

Valuation Analysis: Market Pricing Reflects Optimism That Appears Disconnected from Fundamental Earnings Trends

Despite the earnings challenges and payout concerns discussed above, Cardinal Energy currently trades at valuation levels that imply a much more optimistic outlook.

The shares recently traded around $7.26, substantially above an estimated intrinsic value of approximately $3.67. This gap translates to a margin of safety of about −97.7%, suggesting the stock may be significantly overvalued relative to its fundamental earnings capacity.

Traditional valuation multiples reinforce this assessment. The stock trades at roughly 21.3x trailing earnings, a level that sits above the company’s long-term median and close to its historical highs. Forward valuation appears even more demanding, with the forward P/E ratio reaching approximately 37.7x. This elevated multiple suggests that investors may be anticipating stronger earnings growth than current forecasts support.

Enterprise value metrics tell a similar story. Cardinal Energy currently trades at about 9.4x EV/EBITDA, more than double its ten-year median of roughly 3.7x. Such a sharp divergence from historical norms indicates that the market is assigning a premium valuation relative to the company’s historical profitability profile.

Additional valuation measures further highlight the premium pricing. The price-to-sales ratio of approximately 2.8x exceeds the company’s long-term median, while the price-to-book ratio near 1.8x approaches historical highs. These figures collectively suggest that investors are paying a relatively elevated price for each dollar of revenue and book value.

Importantly, these valuation premiums appear difficult to justify given the company’s stagnant earnings history and lack of dividend growth. While a strong commodity environment could temporarily support cash flow and valuations, the current pricing leaves little margin for error should energy markets weaken or operational performance decline further.

In essence, the market appears to be valuing Cardinal Energy more like a growth-oriented energy producer than a mature income-oriented operator with flat earnings.

Risk Assessment and Capital Structure Considerations

Cardinal Energy’s risk profile reflects a combination of moderate financial stability and operational challenges.

From a balance sheet perspective, leverage remains manageable. The company’s debt-to-EBITDA ratio of approximately 1.02 indicates relatively conservative borrowing levels compared with many exploration and production peers. This modest leverage provides financial flexibility and reduces the likelihood of liquidity stress during cyclical downturns.

However, recent financing activity introduces additional considerations. The company issued approximately CAD 162.7 million in long-term debt, increasing its overall debt burden even though leverage metrics remain within reasonable levels.

Operational efficiency indicators also highlight potential concerns. The company’s Piotroski F-Score stands at 3, a relatively weak reading that suggests declining profitability or financial efficiency across several accounting metrics.

Financial stability metrics present a mixed picture. The Altman Z-Score of roughly 2.37 places the company in a financial “grey zone.” While this score does not indicate immediate distress, it suggests that financial resilience is not particularly strong relative to more robust companies.

Ownership structure adds another layer of complexity. Insider ownership currently stands at 0%, meaning company executives and directors do not hold shares in the business. This lack of insider ownership is relatively uncommon and may raise questions regarding alignment between management and shareholder interests. Institutional ownership remains modest at roughly 6.5%, indicating limited participation from large investment funds.

Liquidity conditions also warrant attention. Average daily trading volume over the past two months has been about 55,000 shares, while recent trading volume has fallen to roughly 12,000 shares. Lower liquidity can increase volatility and widen bid-ask spreads, particularly during periods of market stress.

Taken together, these factors suggest that while Cardinal Energy does not face immediate balance sheet risk, its broader financial profile contains enough cautionary indicators to justify a more conservative valuation than the market currently assigns.

Final Assessment

Cardinal Energy presents a classic income-oriented investment dilemma: an attractive dividend yield supported by commodity-driven cash flow but challenged by stagnant earnings and elevated payout ratios.

The company’s 7.1% dividend yield and monthly distribution structure provide immediate income appeal. Its balance sheet remains relatively conservative, with leverage levels that appear manageable and capable of supporting short-term dividend stability.

However, the fundamental picture raises several red flags. Earnings have stagnated for years, recent profitability trends are weakening, and the dividend payout ratio has climbed to roughly 148%. These factors collectively suggest that the current dividend may not be sustainably supported by earnings over the long term.

Valuation adds another layer of concern. Trading near $7 while intrinsic value estimates sit around $3.67, the stock appears significantly overvalued relative to its fundamental performance. Elevated multiples across earnings, revenue, and enterprise value metrics reinforce the view that the market may be pricing in optimism that the company has yet to deliver.

For investors focused strictly on income, the dividend may remain attractive in the short term, particularly if energy prices remain supportive. However, the combination of weak earnings growth, stretched valuation, and a payout ratio above 100% introduces meaningful long-term risk.

In its current form, Cardinal Energy appears better suited for investors willing to accept elevated risk in exchange for high current income. For more conservative dividend investors seeking sustainable income growth and a clear margin of safety, the stock’s fundamentals and valuation suggest caution remains warranted.