Broadcom: Exceptional Business, Insufficient Yield

A premier semiconductor and infrastructure software franchise trading well ahead of fundamentals

1. Investment Thesis: A High-Quality Cash-Flow Compounder Trading Beyond Its Fundamental Value

Broadcom AVGO 0.00%↑ stands among the most financially disciplined large-cap technology companies, combining semiconductor scale with enterprise infrastructure software recurring revenue. The company has evolved through consolidation — integrating legacy Broadcom and Avago in chips and later adding VMware, CA Technologies, Symantec, and Brocade — into a hybrid hardware-software platform capable of producing unusually stable cash generation for a cyclical industry.

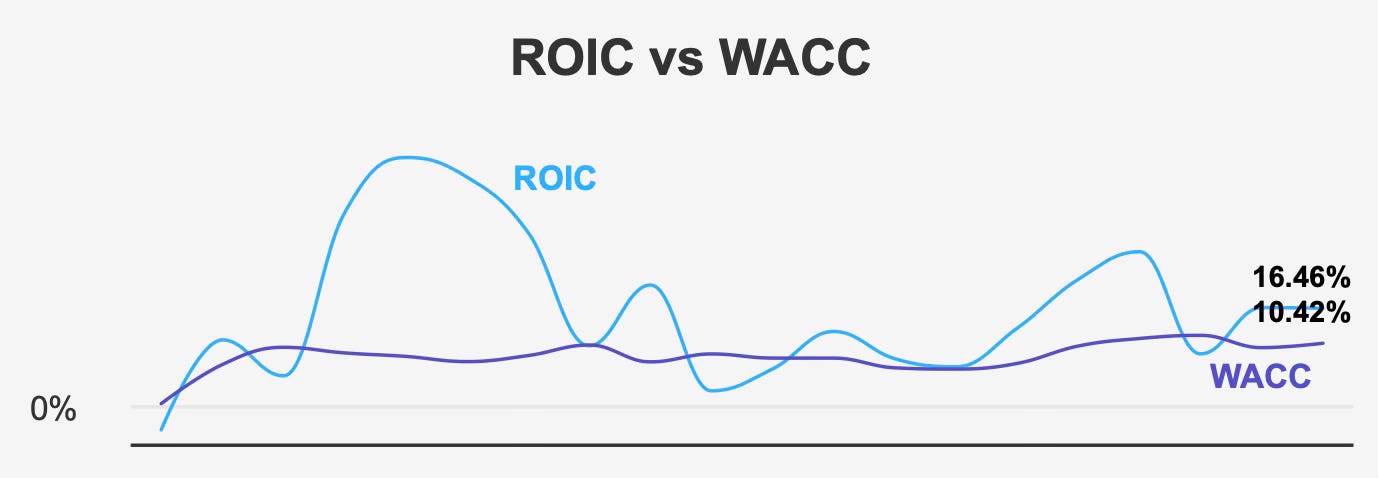

Operationally, the business exhibits the core attributes long-term dividend investors seek: durable demand exposure across computing and connectivity, meaningful participation in AI accelerators, and pricing power reflected in margins approaching the top end of the semiconductor sector. These qualities allow Broadcom to generate returns on invested capital of 16.5% against a cost of capital of 10.4%, meaning it consistently creates economic value rather than merely expanding revenue.

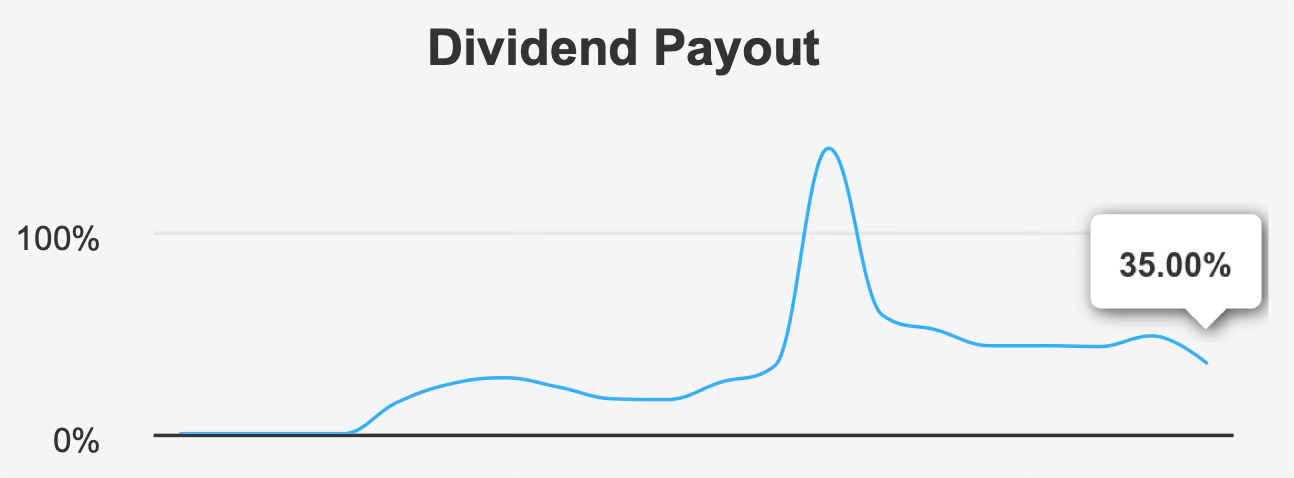

The dividend profile reinforces this strength. Over the past five years the distribution has compounded at 12.9%, supported by a modest payout ratio of 35%. The company therefore grows income while preserving capital flexibility — a hallmark of sustainable dividend growth companies rather than yield-maximizers.

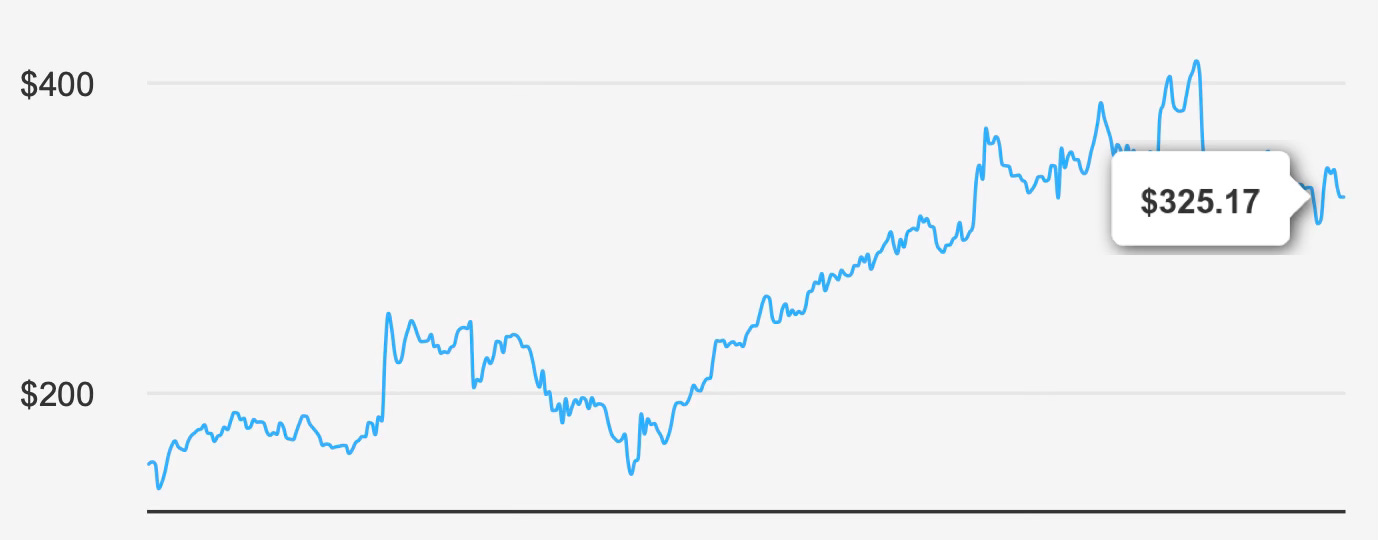

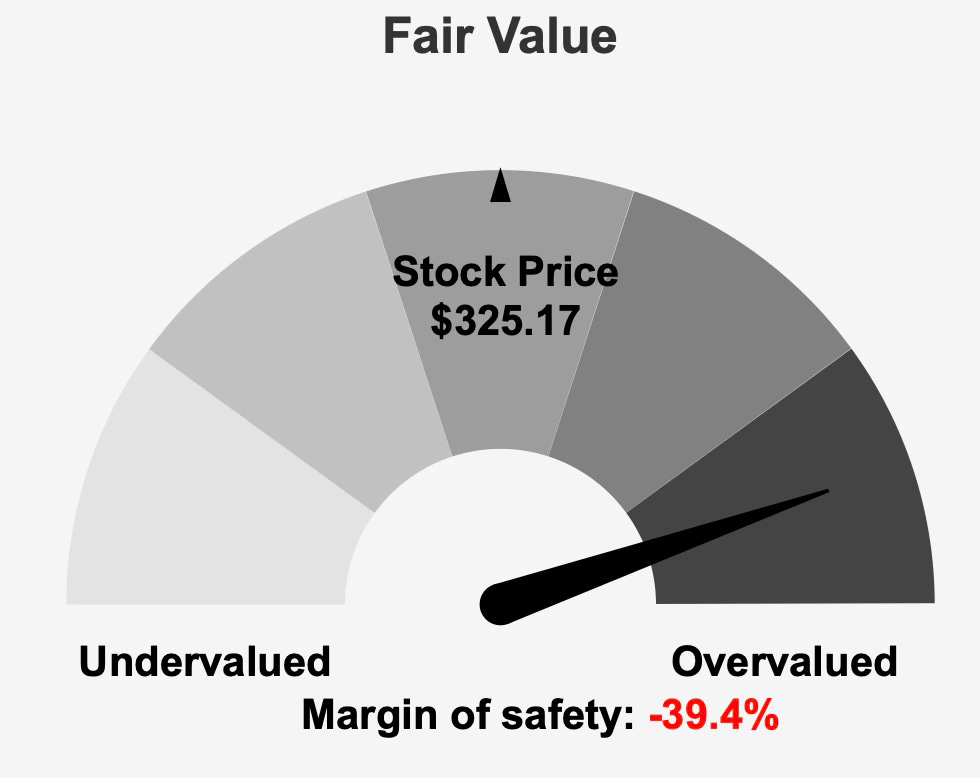

However, the investment case separates sharply between business quality and stock attractiveness. The current share price near $325 sits materially above an intrinsic value estimate of $233.25, leaving a negative margin of safety of roughly 39%.

The conclusion is not that Broadcom is a weak company — it is structurally one of the strongest franchises in large-cap technology — but that today’s valuation already capitalizes years of expected growth. Investors are effectively paying in advance for future execution, leaving limited protection against normal cyclical volatility.

For dividend investors, this distinction matters: the company remains an excellent dividend grower, but presently a poor entry point.

2. Earnings Momentum & Profitability Trends

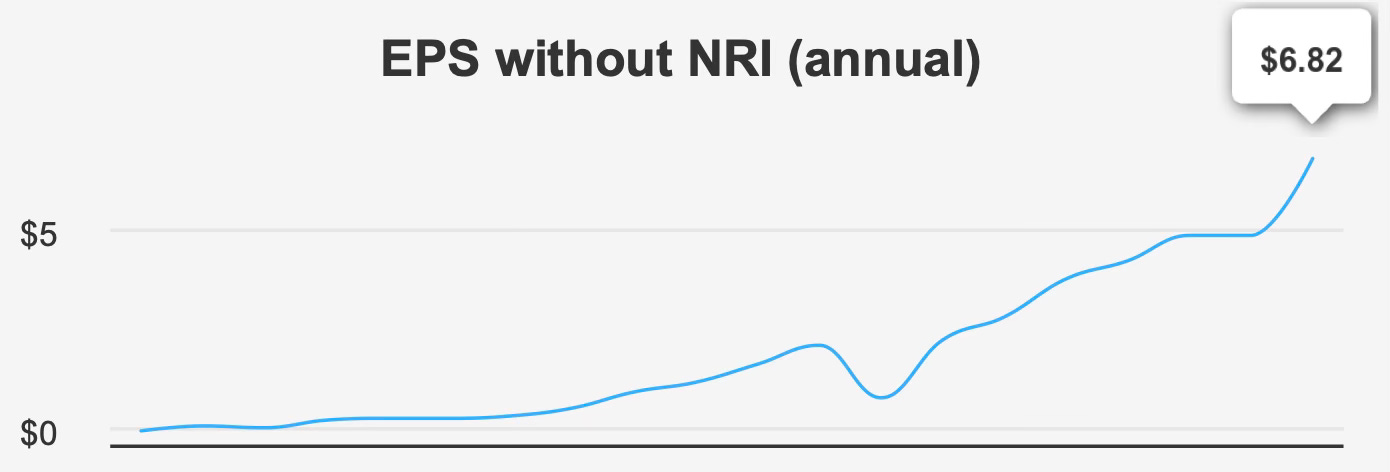

Recent operating performance confirms the company’s strong execution. In the quarter ending October 31, 2025, earnings per share excluding non-recurring items reached $1.95, up from $1.69 sequentially and $1.42 year-over-year.

This growth fits a longer pattern. Over five years, EPS expanded at a 17.7% annualized rate and nearly 19.6% over ten years — unusually steady for a semiconductor company, where earnings typically swing with cycles.

Revenue per share followed the same trajectory, climbing to $3.685 from $3.282 the prior quarter and $2.912 the prior year.

Two structural factors explain this stability.

First, margins remain elevated. Gross margin stands at 67.8%, slightly above its five-year median of 66.6% and near the high end of its historical range that has peaked around 68.9%. Semiconductor firms rarely sustain margins this close to historical highs without pricing power or differentiated products.

Second, capital efficiency is exceptional. The company produces a return on equity of 32.0% while maintaining a spread between ROIC and WACC of roughly six percentage points. This indicates not just profitability but disciplined investment allocation — a key determinant of long-term dividend durability.

Share repurchases also contribute to per-share growth. Over the past year the buyback ratio of −1.2% indicates a reduction in shares outstanding, modestly amplifying earnings per share.

Forward expectations remain ambitious. Analysts project EPS of $8.036 for fiscal 2026 and $12.439 the following year. Revenue forecasts imply significant expansion toward $97.1 billion in 2026 and $166.3 billion by 2028.

Even the industry backdrop is supportive. The semiconductor sector is expected to grow about 6% annually over the next decade, giving Broadcom a favorable structural tailwind while its AI-related custom chips potentially allow it to outgrow the sector.

The key takeaway is that earnings strength is real, not speculative. Broadcom demonstrates operational consistency rare among semiconductor peers. The valuation concern therefore does not arise from weak fundamentals but from how much future growth the market already prices in.

3. Dividend Profile & Sustainability

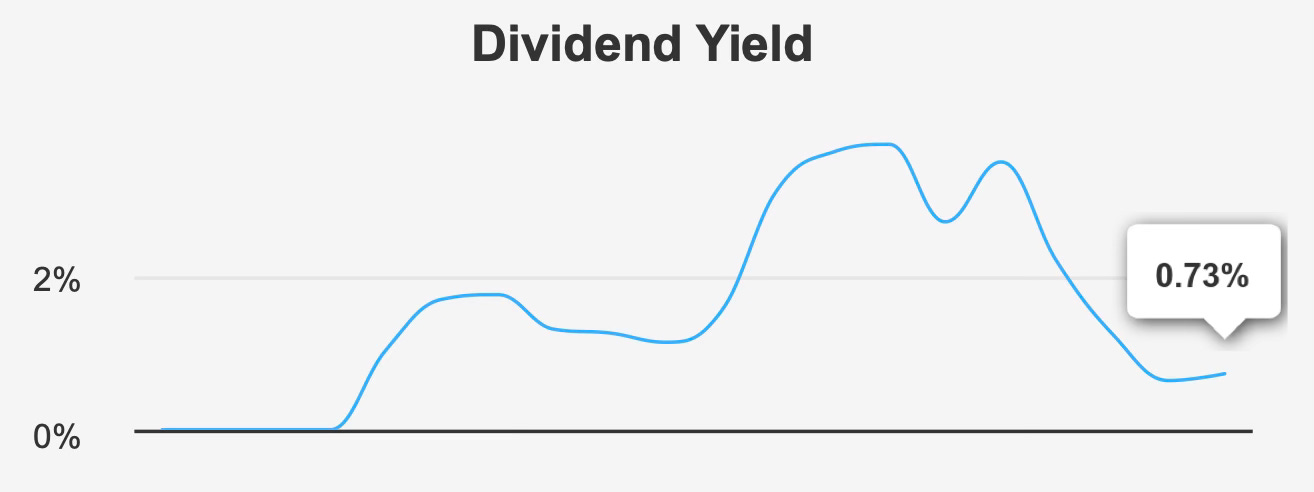

Broadcom’s dividend strategy prioritizes growth rather than yield. The forward yield sits at 0.73%, modest compared with traditional income sectors but typical for technology companies prioritizing capital appreciation alongside income.

What distinguishes the company is reliability of growth. Both three- and five-year dividend growth rates are 12.9%, and the most recent quarterly payment increased from $0.59 to $0.65 per share.

The sustainability of that growth is supported by payout discipline. The dividend consumes only 35% of earnings, leaving substantial reinvestment capacity.

Coverage remains comfortable as well. Dividend coverage of 2.02x indicates earnings exceed distributions by roughly double, providing resilience during cyclical downturns.

Balance sheet leverage also supports stability. Debt-to-EBITDA stands at 1.88, low for a technology firm with acquisition history and comfortably serviceable from operating cash flow.

Future growth expectations align with the past. Forecast dividend growth of about 12.3% over the next three to five years suggests management intends to maintain its established capital return policy.

Timing details reinforce regularity. The most recent ex-dividend date was December 22, 2025 with payment on December 31, and the next is expected near March 20, 2026 assuming a consistent quarterly schedule.

Overall, Broadcom fits the profile of a dividend compounder rather than an income stock. Investors buying today are not purchasing yield — they are purchasing rising income over time. The question therefore becomes valuation, not sustainability.

4. Valuation: Market Expectations Already Discounting Years of Strong Execution

The most challenging aspect of the investment case is valuation. The shares trade around $325 compared with an intrinsic value estimate of $233.25, leaving approximately 39% downside to fair value under current assumptions.

Traditional multiples reinforce the same conclusion.

The trailing P/E ratio sits at 68.3x, well above the ten-year median of 42.1x. Even using forward earnings, the ratio compresses only to 32.3x — still above historical norms.

Enterprise valuation tells a similar story. EV/EBITDA of 46.2x compares to a decade median near 18.2x, implying a substantial premium for expected growth.

Revenue valuation appears particularly stretched. Price-to-sales of 24.7x exceeds the long-term median of 6.9x, indicating investors value each dollar of sales at more than triple its historical multiple.

Analyst targets reach approximately $453.89, suggesting optimism about future growth trajectories. Yet the gap between price and intrinsic value implies that positive outcomes must not only occur — they must exceed already elevated expectations.

In essence, the market prices Broadcom not as a cyclical semiconductor company but as a near-perpetual growth platform. While the business quality supports premium valuation, the magnitude of the premium reduces margin of safety.

Dividend investors typically rely on valuation discipline to protect long-term income returns. Buying excellent companies at excessive valuations historically lowers future total returns even when dividends grow steadily. Broadcom exemplifies that dynamic today.

5. Risk Assessment & Capital Structure Considerations

Financial risk remains low. The company carries a Piotroski F-Score of 7 and an Altman Z-Score of 11.45, both indicating strong financial health and minimal distress probability.

Accounting quality appears reliable as well, with a Beneish M-Score of −1.86 suggesting low likelihood of earnings manipulation.

Operational risks exist but are manageable. Asset growth of 21.3% outpacing revenue growth of 18.2% could indicate declining efficiency if sustained. Additionally, a favorable tax rate supporting recent earnings may not persist indefinitely.

Ownership patterns also offer signals. Insider ownership is minimal at 0.04% and insider selling materially outweighs purchases over the past year. Institutional ownership near 76.9% suggests professional investor confidence but also increases sensitivity to sentiment shifts.

Liquidity shows some tightening, with daily trading volume around 18.2 million compared to a two-month average of 32.3 million, potentially amplifying price swings.

Finally, government contract revenue volatility and declining patent filings in recent years highlight reliance on large projects and strategic shifts rather than steady organic innovation metrics.

None of these risks threaten solvency or dividend safety. Instead, they primarily matter because valuation leaves little room for operational disappointments.

Final Assessment

Broadcom represents a textbook high-quality dividend growth company. It combines strong returns on capital, stable margins, disciplined payout policy, and double-digit dividend growth supported by real earnings expansion. Financial risk is low, balance sheet leverage is manageable, and long-term industry demand remains favorable.

Yet investment quality depends not only on business quality but on entry price.

At a share price materially above intrinsic value and trading far above historical valuation ranges across earnings, sales, and EBITDA, the stock already reflects an optimistic future. The dividend is reliable, but the expected return from today’s valuation is constrained.

For existing shareholders, the company remains a compelling long-term compounder worth holding due to its durable growth and dividend trajectory.

For new dividend investors, patience is warranted. The business deserves a premium valuation — just not the current one.

In short: an exceptional company, a dependable dividend grower, and presently an unattractive purchase price.