Blackstone: High Yield, Thin Coverage

A dividend powered by realizations rather than durable cash generation

1. Investment Thesis: A Global Alternative Asset Giant Offering Income but Lacking Economic Value Creation

Blackstone BX 0.00%↑ stands as the largest alternative asset manager globally, overseeing $1.242 trillion in assets under management and $906.2 billion in fee-earning assets as of September 2025. Its scale spans private equity, real estate and real assets, private credit, and other alternatives, with institutional investors representing 84% of capital and high-net-worth channels accounting for the remaining 16%. The firm’s diversified platform and global footprint across 25 offices position it structurally as a dominant allocator of private capital rather than a cyclical niche manager.

From a dividend investor’s perspective, this positioning matters. Asset managers tied to long-duration capital pools typically enjoy predictable fee income, and Blackstone’s business model partially reflects that stability. However, the company’s distributions remain closely tied to realizations, performance fees, and market cycles rather than recurring free cash flow. This distinction explains why Blackstone often offers above-market yields while simultaneously showing elevated payout ratios.

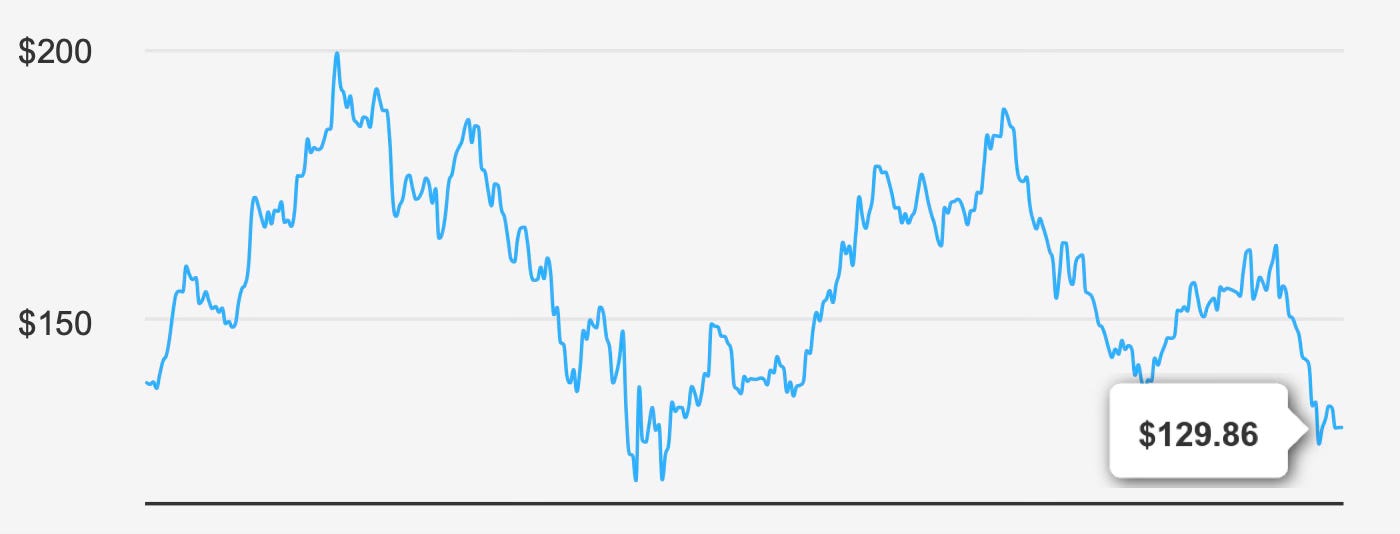

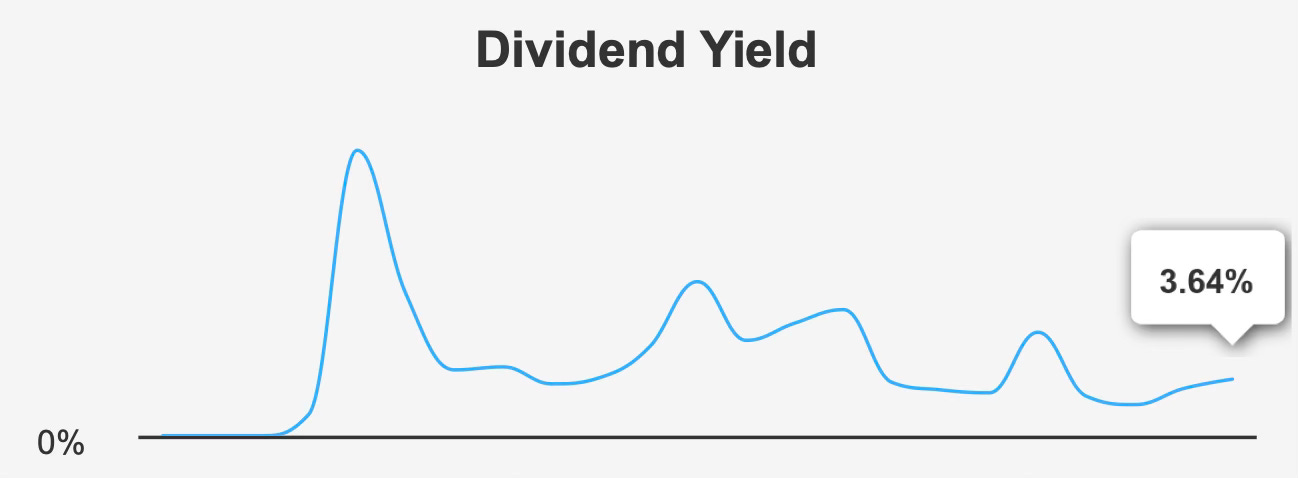

At a current share price of $129 and a market capitalization of $101.7 billion, the stock offers a forward dividend yield of 3.6%. On the surface, this yield appears attractive within financials, especially given the company’s long-term growth record. Five-year dividend growth of 15.1% demonstrates the firm’s ability to increase distributions during favorable market conditions.

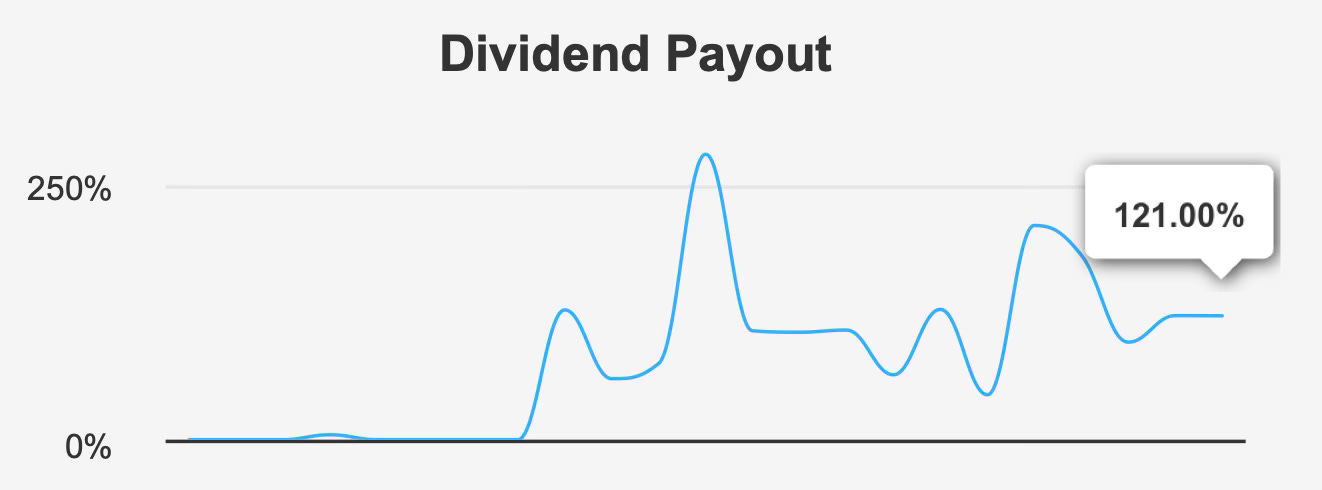

Yet the yield comes with a structural tradeoff. The payout ratio sits at 121.0%, meaning the company distributes more than it earns. Dividend coverage is 0.83, reinforcing that payments rely partly on variable income streams rather than durable operating profits. This transforms the dividend from a traditional compounding income stream into a distribution tied to capital market cycles.

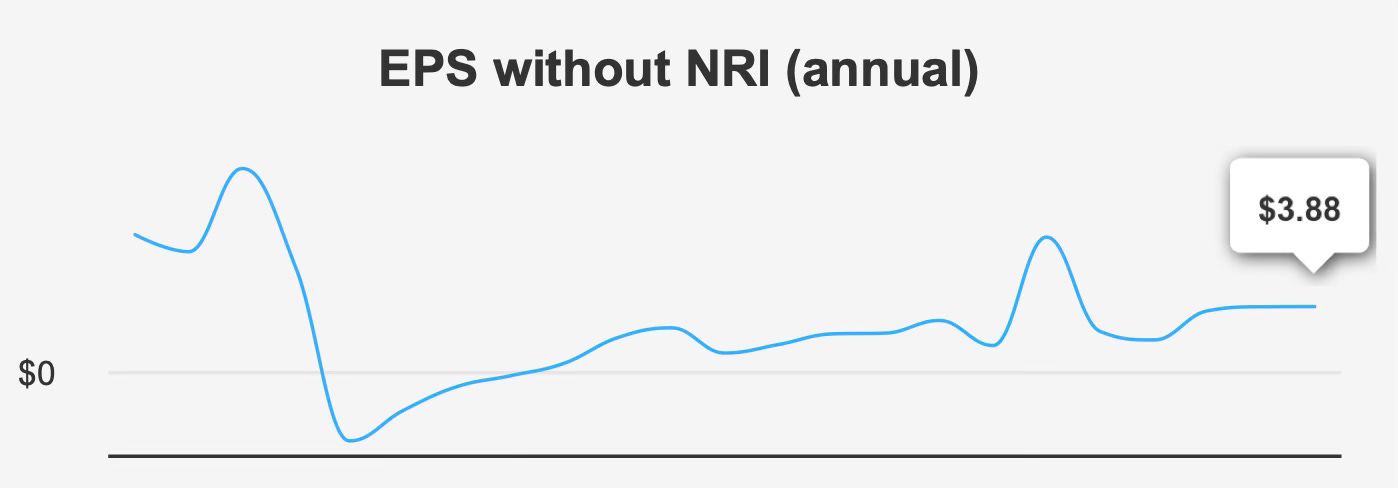

Growth expectations remain respectable. Analysts project earnings per share of $6.375 for 2026 and $7.954 for 2027, alongside revenue estimates rising from $15.86 billion in 2026 to $21.10 billion by 2028. Industry forecasts suggest 5–7% long-term growth, consistent with mature asset managers rather than early-stage financial franchises.

However, a deeper economic lens complicates the investment story. The firm’s return on invested capital is reported at 0.00% over both five- and ten-year periods, while its weighted average cost of capital stands at 13.09% currently and 10.81% on a five-year median basis. In simple terms, the company has not generated returns exceeding its financing cost. Despite strong accounting profitability, the business has not created measurable economic value.

The investment thesis therefore rests on a contradiction: Blackstone is operationally successful and financially profitable, but economically inefficient. Investors are effectively paid income for accepting earnings variability and valuation risk.

For dividend-focused investors, the central question is not whether Blackstone can grow — it likely can — but whether its distributions represent stable shareholder returns or cyclical capital recycling.

2. Earnings Momentum & Profitability Trends

Blackstone’s recent operating performance reflects the recovery phase typical of alternative asset managers following weaker transaction markets. Fourth-quarter 2025 earnings per share excluding non-recurring items reached $1.30, rising sharply from $0.80 in the prior quarter and $0.92 a year earlier. Revenue per share also improved to $4.77 from $3.43 in Q3 2025 and $3.52 in Q4 2024.

This improvement signals transaction activity returning rather than structural margin expansion. Over longer periods, annual EPS growth has been modest: a 0.8% compound annual rate over five years and 7.0% over ten years. The longer horizon confirms the firm can grow earnings across cycles, while the shorter horizon shows sensitivity to capital markets.

Revenue growth supports this interpretation. Five-year revenue growth stands at 5.8%, and ten-year growth at 10.2%. These figures indicate a maturing franchise transitioning from rapid scaling to steady expansion.

Capital allocation has contributed meaningfully to per-share results. The company reduced shares outstanding by 1.9% over the past year and averaged a 2.5% annual reduction over the past decade. Buybacks have therefore supplemented earnings growth, partially offsetting slower operating expansion.

However, profitability metrics present a nuanced picture. Blackstone reports a strong return on equity of 36.3%, suggesting efficient use of shareholder capital from an accounting perspective. Yet the absence of positive ROIC relative to WACC implies earnings rely heavily on leverage structures, performance fee timing, and accounting classifications rather than persistent economic profit generation.

This disconnect is typical of alternative asset managers structured around fee and performance income. Accounting profits can appear robust, but capital efficiency becomes difficult to measure due to fund structures and carried interest timing.

Looking forward, expected earnings growth toward nearly $8 per share by 2027 indicates improving realization cycles. If achieved, the firm should restore stronger dividend coverage. But history shows such cycles fluctuate rather than trend linearly.

In summary, Blackstone’s earnings trajectory reflects cyclical recovery layered on top of steady structural expansion. Investors should interpret growth projections as environment-dependent rather than guaranteed compounding.

3. Dividend Profile & Sustainability

Blackstone’s dividend is best understood as a distribution policy rather than a traditional corporate dividend. The firm distributes a large portion of realized earnings, leading to elevated growth during strong markets and stagnation during weak ones.

Over five years, dividend growth reached 15.1%, demonstrating expansion alongside asset growth and transaction activity. Yet the three-year growth rate turned slightly negative at -1.1%, reflecting the recent slowdown in realizations across private markets.

The most recent quarterly dividend was $1.49 per share. With a forward yield of 3.6%, the stock sits slightly below its 10-year median yield of 3.9%, suggesting valuation remains relatively full despite a cyclical earnings dip.

The central concern is sustainability. The payout ratio of 121.0% indicates distributions exceed earnings, and coverage of 0.83 confirms insufficient earnings support. While this is not unusual for alternative asset managers in softer environments, it prevents the dividend from functioning as a bond-like income stream.

Future dividend growth expectations of 30.8% appear optimistic and implicitly rely on earnings normalization rather than operational improvement. The upcoming ex-dividend date of February 9, 2026 and payout date of February 17, 2026 reinforce the regular distribution schedule but do not resolve the underlying coverage question.

For income investors, the dividend behaves like a variable income instrument. Payments rise meaningfully during strong capital markets and compress during slow deal environments. The yield compensates for that volatility.

Therefore, Blackstone’s dividend should be viewed as opportunistic income rather than dependable compounding income.

4. Valuation: Market Pricing Implies Stability Despite Cyclical Economics

At $129 per share, Blackstone trades above its calculated intrinsic value of $96.50, representing a negative margin of safety of roughly 34.6%. The market therefore prices the company as a premium franchise despite evidence of inconsistent economic returns.

The valuation gap is notable because investors are effectively paying for scale and brand strength rather than demonstrated capital efficiency. Price-to-book and price-to-earnings ratios are near multi-year lows, indicating the market has already adjusted downward from higher optimism. Yet the stock still trades at a level that assumes sustained earnings growth and stable distributions.

Dividend yield also supports this interpretation. The 3.6% forward yield is approaching a two-year high, meaning price weakness has modestly improved income appeal. However, the yield remains below long-term historical levels, suggesting investors continue to award a quality premium to the business.

Institutional ownership of 69.0% reinforces this premium perception. Large investors appear willing to hold the stock as a core alternative asset exposure, which stabilizes valuation multiples relative to more cyclical financial companies.

In effect, the market treats Blackstone less like a traditional asset manager and more like a financial infrastructure platform. The valuation assumes continued growth in private markets allocations globally and sustained fee-earning asset expansion.

The risk emerges if earnings fail to meet projected growth toward nearly $8 per share by 2027. In that case, valuation compression could occur without a corresponding dividend cushion due to limited coverage.

Thus, the stock is not expensive purely on relative multiples, but expensive relative to economic value creation and dividend safety.

5. Risk Assessment & Capital Structure Considerations

Risk in Blackstone is not driven primarily by leverage but by earnings composition. The company has issued debt in recent years, yet overall debt levels remain acceptable. The greater concern lies in distributing more than earned while operating in a cyclical revenue model.

Operational efficiency also raises questions. Revenue per share has declined over the past three years even as assets expanded, suggesting scale has not fully translated into per-share productivity.

Economic value metrics reinforce the concern. With ROIC at 0.00% and WACC above 10%, capital deployment does not consistently generate value beyond financing costs. This undermines long-term compounding despite high accounting profitability.

Financial quality indicators partially offset these concerns. A Piotroski F-Score of 7 suggests strong balance sheet and operating fundamentals, while the Beneish M-Score indicates low earnings manipulation risk.

Trading characteristics show heavy institutional involvement. Daily trading volume exceeds 5.7 million shares, and a dark pool index near 66.9% suggests large institutional participation. Liquidity is strong but may contribute to volatility during macro shifts.

Insider activity has been neutral, with equal buy and sell transactions over the past year and insider ownership of 1.01%. The absence of strong insider conviction reinforces the view that the stock is fairly priced rather than deeply undervalued.

Overall, the risk profile is not bankruptcy risk but income reliability risk. Investors face the possibility of fluctuating distributions and valuation compression rather than balance-sheet distress.

Final Assessment

Blackstone offers an appealing income yield backed by one of the strongest alternative asset platforms globally. The firm’s scale, diversified strategies, and institutional client base support continued growth and relevance within global capital markets.

However, the investment case differs from traditional dividend equities. The payout exceeds earnings, economic returns trail capital costs, and distributions depend heavily on transaction cycles. The dividend therefore behaves more like a participation payout than a guaranteed cash stream.

At current pricing above intrinsic value, investors are paying for brand strength and long-term industry positioning rather than demonstrable economic value creation. Expected earnings recovery could justify the valuation, but failure to achieve projected growth would expose downside without strong dividend protection.

Blackstone suits investors seeking variable income linked to private market activity rather than stable dividend compounding. The yield compensates for volatility, but not for valuation risk.

For long-term dividend portfolios prioritizing reliability, the stock remains less attractive. For investors comfortable with cyclical income tied to capital markets, it may serve as a supplemental yield holding rather than a core income position.