Becton Dickinson & Co. (BDX) Dividend Equity Report

Steady cash flows, improving capital efficiency, and a modest valuation discount in a defensive healthcare franchise

Investment Thesis: Durable Healthcare Franchise with Improving Capital Returns Trading Below Intrinsic Value

Becton Dickinson & Co. (BDX) operates at the center of global healthcare infrastructure as the world’s largest manufacturer and distributor of medical surgical products, including needles, syringes, sharps-disposal units, diagnostic instruments, and cell-imaging systems. Its scale and diversification provide structural resilience. On a 2025 sales basis following the spinoff, BD Medical Essentials accounted for 34% of revenue, Interventional represented 28%, Connected Care 25%, and Biopharma 13%. International markets contributed 43% of total revenue, reinforcing the company’s global footprint.

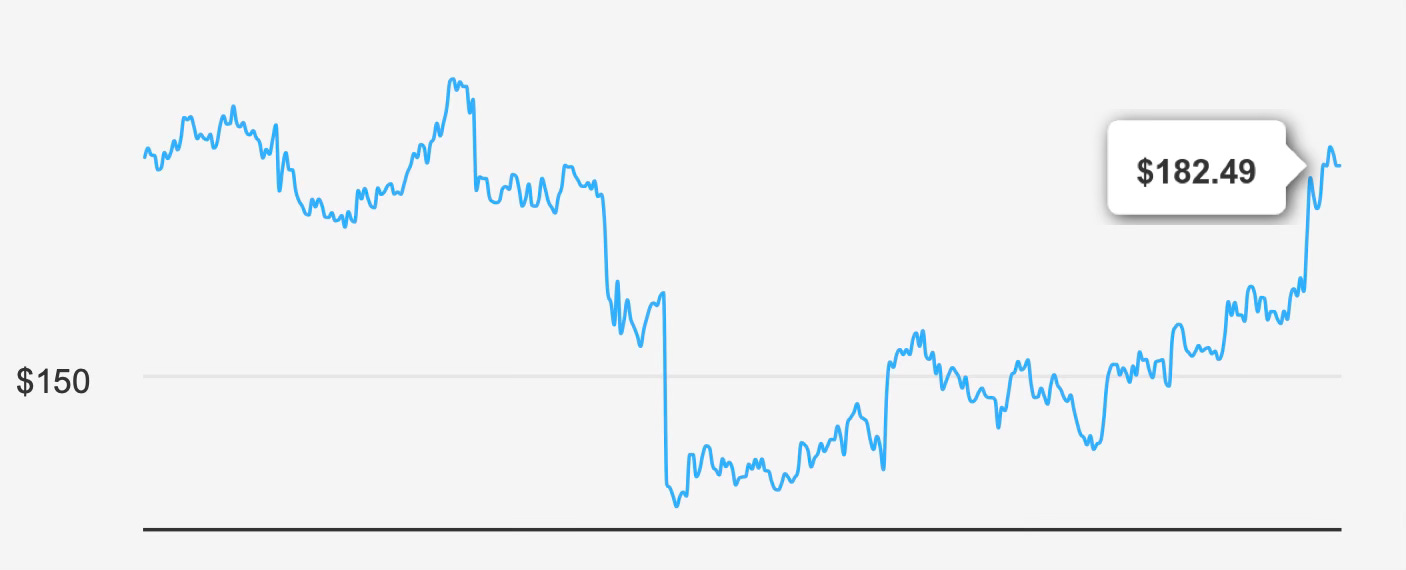

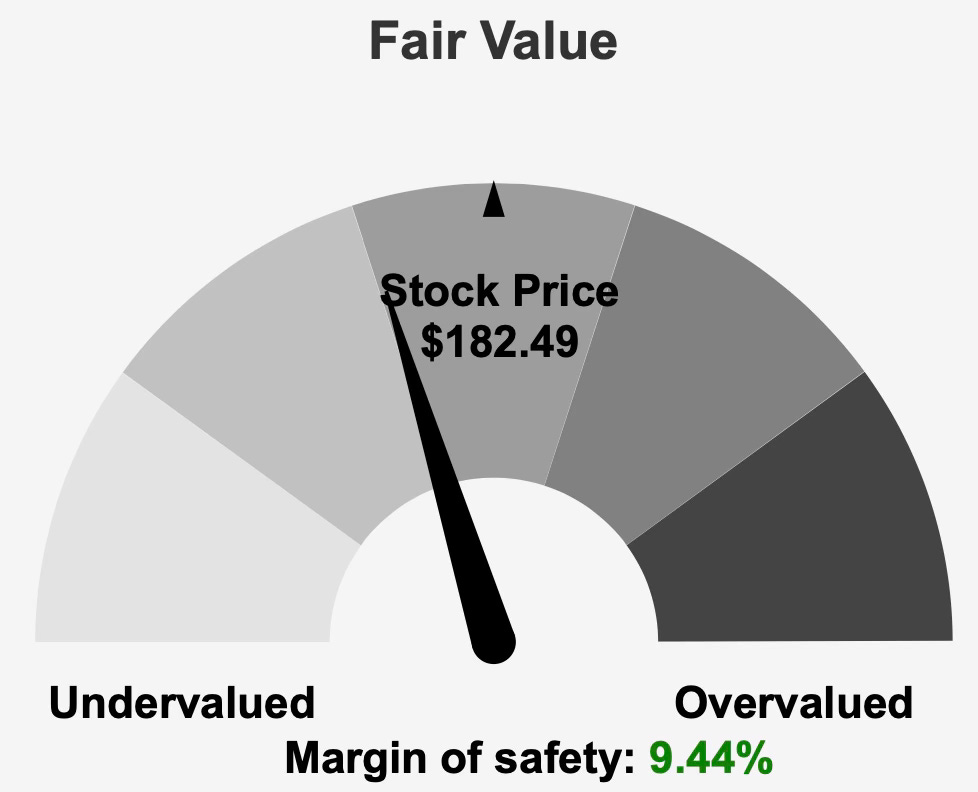

At a current price of $182, BDX carries a market capitalization of $51.91 billion and trades modestly below its estimated intrinsic value of $201.52. This implies a margin of safety of 9.4%, positioning the shares as modestly undervalued relative to fundamental worth. The stock is rated Hold with a low risk profile, reflecting a balance between operational durability and moderate leverage.

Long-term growth has been steady rather than explosive. Over the past five years, overall growth has averaged 5.4%, with revenue compounding at 4.7% annually. The 10-year revenue growth rate stands at 3.5%. These figures align closely with the broader medical devices industry’s expected 4–5% annual growth over the next decade. BDX’s outlook remains consistent with sector dynamics rather than materially exceeding them.

In this context, the investment case rests on three pillars: stable mid-single-digit growth, incremental improvement in capital efficiency, and a valuation that sits slightly below historical norms. For long-term income-oriented investors seeking predictability over acceleration, BDX offers a defensively positioned franchise with measured upside potential.

2. Earnings Momentum & Profitability Trends

BDX’s most recent quarterly results for the period ending December 2025 illustrate both cyclical softness and year-over-year improvement. EPS excluding non-recurring items was $2.91, down from $3.95 in the prior quarter but slightly higher than $3.43 in the same quarter a year earlier. Diluted EPS came in at $1.34, compared with $1.72 sequentially and $1.04 year over year.

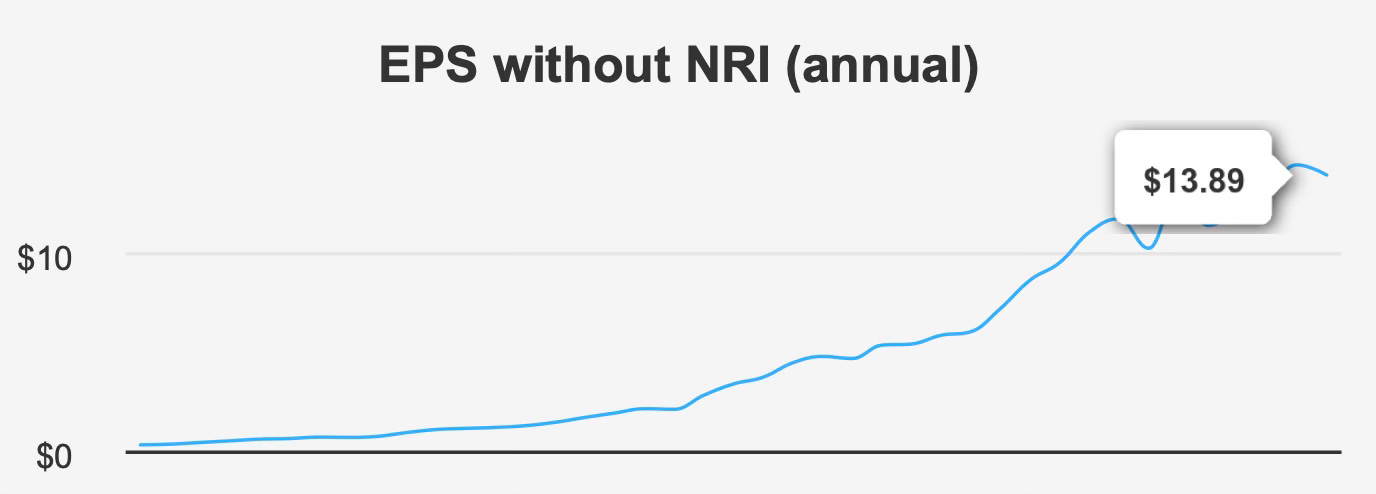

Revenue per share declined sequentially to $18.374 from $20.458 but improved from $17.797 in the prior-year period. While quarterly volatility reflects timing and operational dynamics, the longer-term picture remains stable. The five-year CAGR for annual EPS without non-recurring items is 5.3%, with a 10-year CAGR of 5.7%. These figures confirm a consistent mid-single-digit earnings trajectory.

Profitability metrics provide additional context. Gross margin stands at 46.1%, above the five-year median of 45.1%, indicating incremental operational efficiency despite uneven quarterly earnings. The company has demonstrated the ability to preserve pricing discipline and manage input costs within a competitive and regulated industry.

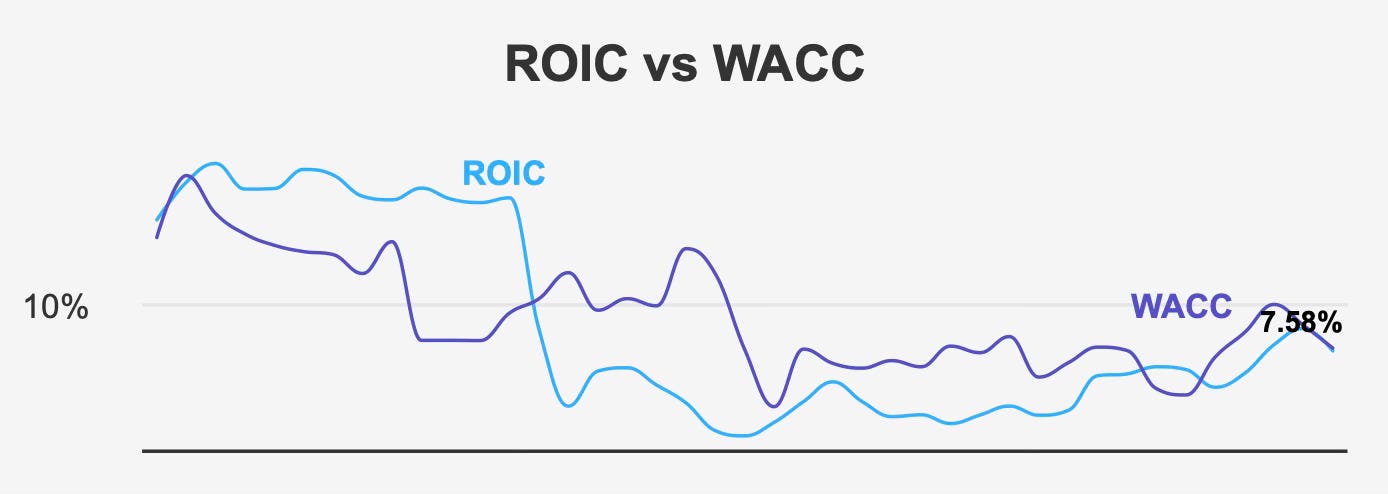

Capital efficiency has improved meaningfully. Current return on invested capital (ROIC) is 5.8%, exceeding the weighted average cost of capital (WACC) of 4.6%. This spread confirms positive economic value creation. Importantly, this represents a turnaround from the five-year median comparison, where ROIC of 5.0% trailed the five-year median WACC of 5.2%. The present reversal suggests improved capital allocation and operating discipline.

Return on equity has also edged higher, rising to 6.9% from a five-year median of 6.6%. While not indicative of high-return structural advantages, it reflects incremental improvement in profitability relative to shareholder equity.

Share repurchases have been modest. Over the past year, the buyback ratio was 0.8%, implying a small reduction in shares outstanding. Over three years, the ratio was slightly negative at -0.2%, indicating minimal net reduction. While repurchases have provided marginal EPS support, capital returns remain primarily dividend-driven rather than buyback-led.

Looking ahead, analysts project revenue of $19,317 million in 2026, rising to $19,724 million in 2027 and $20,492 million in 2028. EPS is estimated at $6.297 next fiscal year and $7.490 the following year. These projections imply steady earnings acceleration and partially explain the compression in forward valuation multiples. The next earnings release, scheduled for May 1, 2026, will be important in confirming the trajectory.

Overall, BDX’s earnings profile is not characterized by rapid expansion but by consistency, margin stability, and improving capital returns.

3. Dividend Profile & Sustainability

BDX’s dividend characteristics are aligned with its broader financial profile: steady, measured, and well-covered.

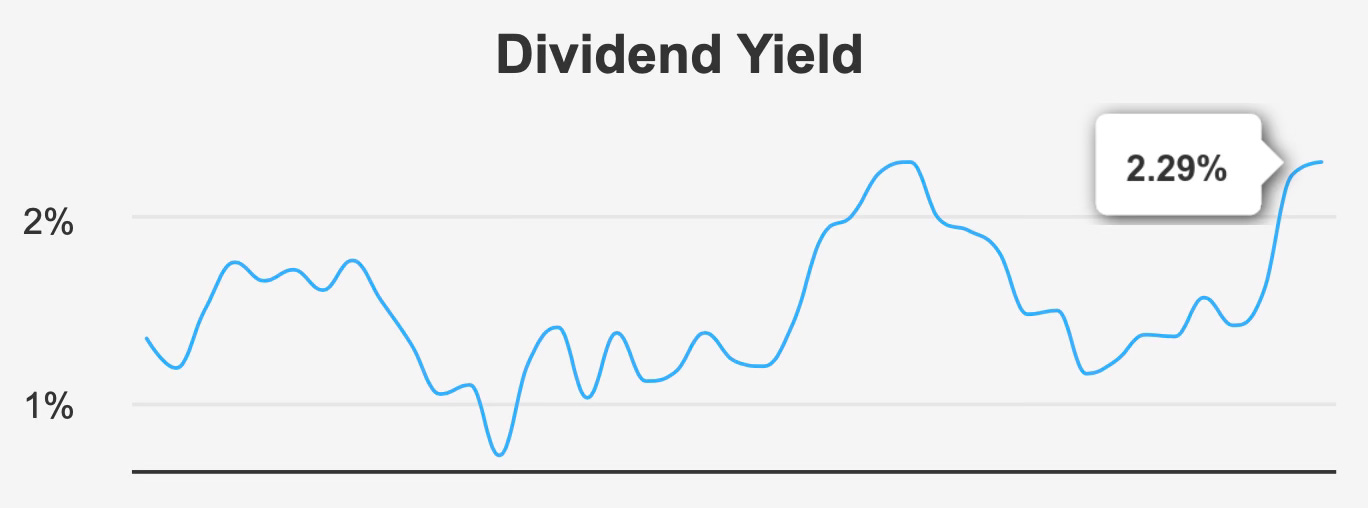

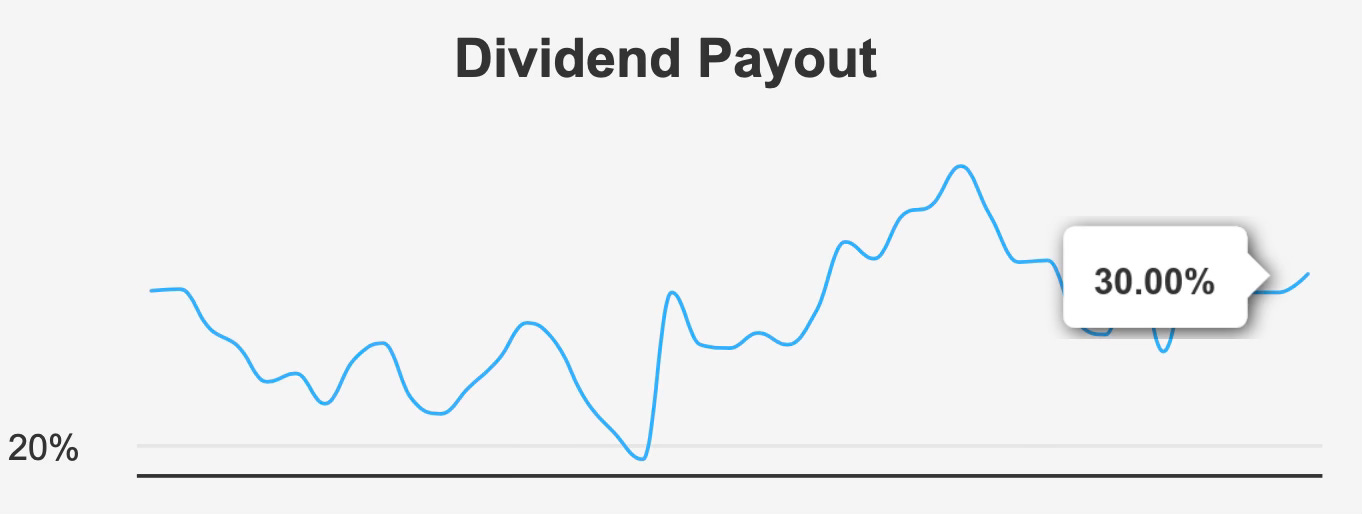

The forward dividend yield stands at 2.3%, supported by a quarterly dividend of $1.05. The payout ratio is 30.0%, indicating substantial headroom for continued increases. Dividend coverage is 1.47, reinforcing the sustainability of current distributions.

Dividend growth has historically tracked earnings growth. The five-year dividend growth rate is 5.4%, while the three-year rate is 6.1%. This cadence aligns closely with EPS growth trends and reflects a disciplined capital allocation approach. However, forward dividend growth is estimated at 1.8%, suggesting a potential deceleration relative to historical averages. This moderation may reflect cautious financial management amid leverage considerations and industry dynamics.

The next ex-dividend date is March 10, 2026, with payment scheduled for March 31, 2026. Given the quarterly schedule, the subsequent ex-dividend date is projected for June 10, 2026.

Leverage remains an important factor in dividend assessment. Debt-to-EBITDA stands at 3.87, placing BDX in a moderate leverage range. While manageable, this level warrants monitoring, particularly in a rising rate environment or if earnings growth were to soften.

Importantly, the payout ratio has remained consistent around its 10-year median, reinforcing the stability of the dividend policy. The company’s ability to generate ROIC above WACC further supports the durability of cash flows funding shareholder returns.

For dividend-focused investors, BDX offers a combination of moderate yield, disciplined payout policy, and a track record of mid-single-digit growth, albeit with signs of potential near-term moderation.

4. Valuation: Discount to Historical Multiples Supported by Forward Earnings Acceleration

At $182.49, BDX trades below its intrinsic value estimate of $201.52, offering a 9.4% margin of safety. While not deeply discounted, this valuation gap suggests moderate upside if operational execution continues.

On a trailing basis, the P/E ratio is 29.8x, below the 10-year median of 36.3x. The forward P/E compresses sharply to 14.7x, reflecting expectations for earnings expansion. This differential between trailing and forward multiples highlights the market’s anticipation of improved profitability.

EV/EBITDA stands at 14.0x, compared with a 10-year median of 16.4x. Similarly, the P/S ratio of 2.4x sits below its 10-year median of 2.9x, and the P/B ratio of 2.1x trails the 10-year median of 2.3x. Price-to-free-cash-flow is 19.9x, close to the 10-year median of 20.4x, suggesting that free cash flow valuation remains broadly in line with historical norms.

Taken collectively, these metrics indicate that BDX trades modestly below its long-term valuation averages. The discount is not dramatic, but it is consistent across multiple measures.

Analyst sentiment remains constructive, with a price target of $202.36, closely aligned with intrinsic value estimates. The relative stability of these targets suggests confidence in the company’s medium-term outlook.

Valuation, therefore, appears balanced: not a clear bargain, but moderately attractive relative to historical norms and supported by projected earnings growth.

5. Risk Assessment & Capital Structure Considerations

While operational fundamentals remain sound, risk factors deserve attention.

Over the past three years, BDX issued $2.2 billion in new debt. The Altman Z-score of 2.04 places the company in the grey zone, indicating some financial stress but not signaling imminent distress. Combined with a Debt-to-EBITDA ratio of 3.87, leverage represents the primary balance sheet consideration.

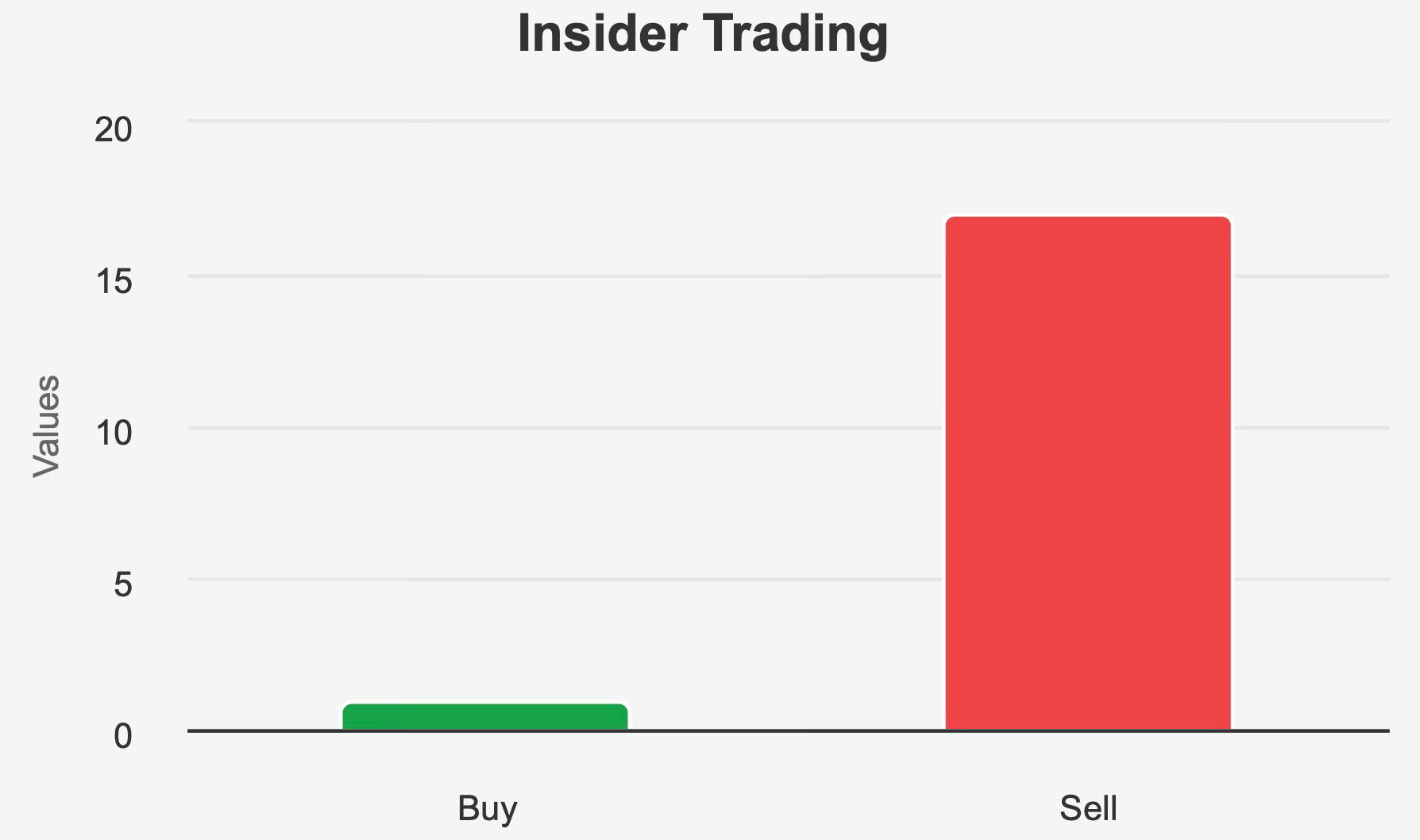

Insider activity skews negative. Over the last 12 months, there were 17 insider sales compared with one purchase. In the last six months, insiders executed 10 sales and no purchases, with six sales occurring in the last three months. Insider ownership stands at 0.59%, while institutional ownership is 94.07%. Although high institutional participation provides stability, sustained insider selling may raise questions about near-term confidence.

From a quality standpoint, the Piotroski F-Score of 7 signals solid financial health, and the Beneish M-Score of -2.64 indicates a low probability of earnings manipulation. Operating margins are expanding, and revenue and earnings growth remain predictable.

Liquidity is strong, with average daily trading volume of 2,894,912 shares, above the two-month average of 2,664,845. However, a Dark Pool Index of 37.0% suggests a significant portion of trading occurs off-exchange, which can influence short-term price discovery.

Government contract revenue has shown volatility, peaking at $154,698,807 in 2022, declining through 2024, recovering to $108,770,972 in 2025, and projected to fall sharply to $17,265,577 in 2026. Patent filings increased steadily to 293 in 2025 before a projected decline to 33 in 2026. These shifts may reflect strategic changes or cyclical adjustments.

Collectively, the risk profile is moderate. Leverage and insider selling temper enthusiasm, but financial quality metrics and stable institutional support mitigate structural concerns.

Final Assessment

Becton Dickinson represents a stable, globally diversified healthcare franchise generating steady mid-single-digit earnings growth and modest dividend expansion. Current ROIC exceeding WACC confirms positive value creation, and gross margins remain above historical medians.

The dividend yield of 2.3%, supported by a 30.0% payout ratio, appears sustainable, though forward growth may slow to approximately 1.8%. Leverage at 3.87x Debt-to-EBITDA warrants monitoring but remains manageable.

Valuation metrics sit modestly below historical averages, with a 9.4% margin of safety relative to intrinsic value and a forward P/E of 14.7x suggesting earnings acceleration. While not a deep value opportunity, the shares appear reasonably priced for long-term investors seeking dependable income and defensive exposure.

In sum, BDX offers measured upside, durable cash flows, and disciplined capital allocation. For income-focused portfolios prioritizing stability over rapid growth, the stock remains a credible, low-risk holding trading at a modest discount to intrinsic value.