Automatic Data Processing (ADP): Dividend Strength Amid Valuation Tension

A high-quality dividend franchise trading at a premium to intrinsic value

Investment Thesis: Durable Dividend Franchise Trading Well Above Intrinsic Value

Automatic Data Processing ADP 0.00%↑ operates one of the most entrenched human capital management platforms globally, serving over 1.1 million clients and paying more than 42 million workers across 140 countries. Its scale, recurring revenue base, and deep integration into payroll and HR workflows create meaningful switching costs and structural resilience. These attributes have supported steady earnings expansion and consistent dividend growth over time.

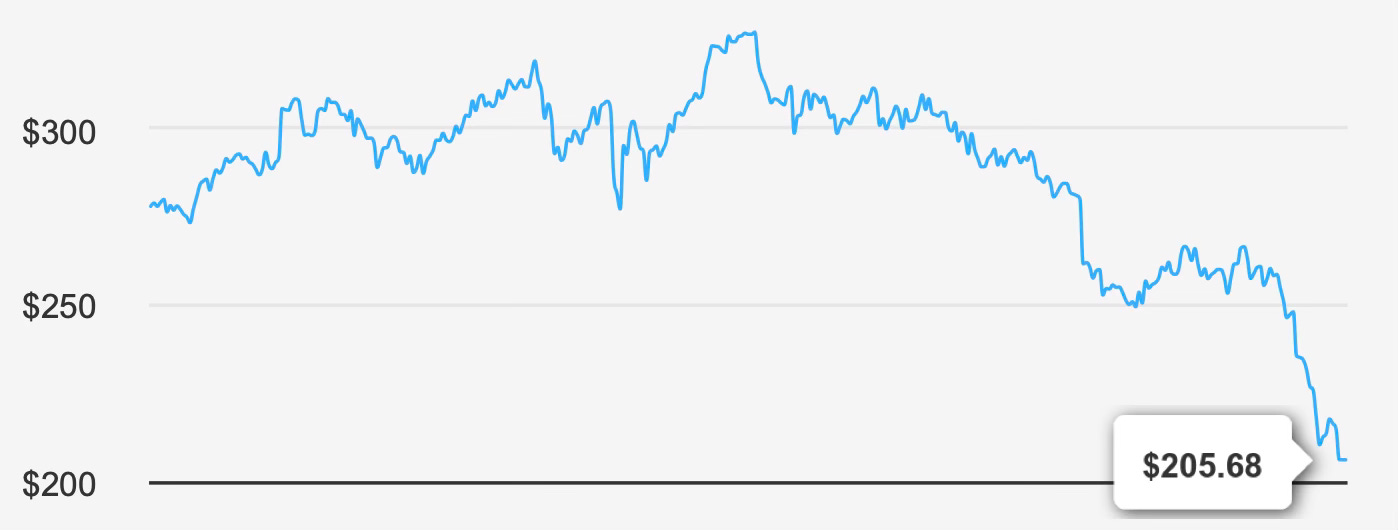

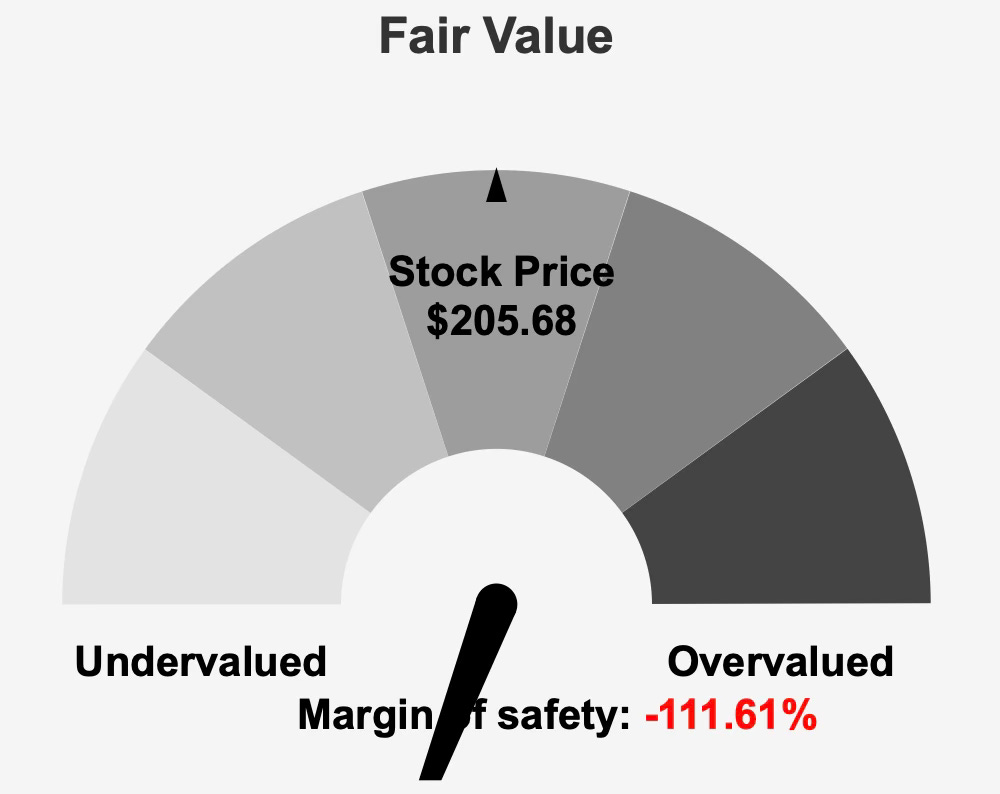

However, the current investment case is defined less by operational durability and more by valuation disconnect. With shares trading at $205 against an intrinsic value estimate of $97.19, the implied margin of safety stands at -111.6%. Despite attractive dividend characteristics and healthy earnings momentum, the stock appears materially overextended relative to its underlying valuation framework.

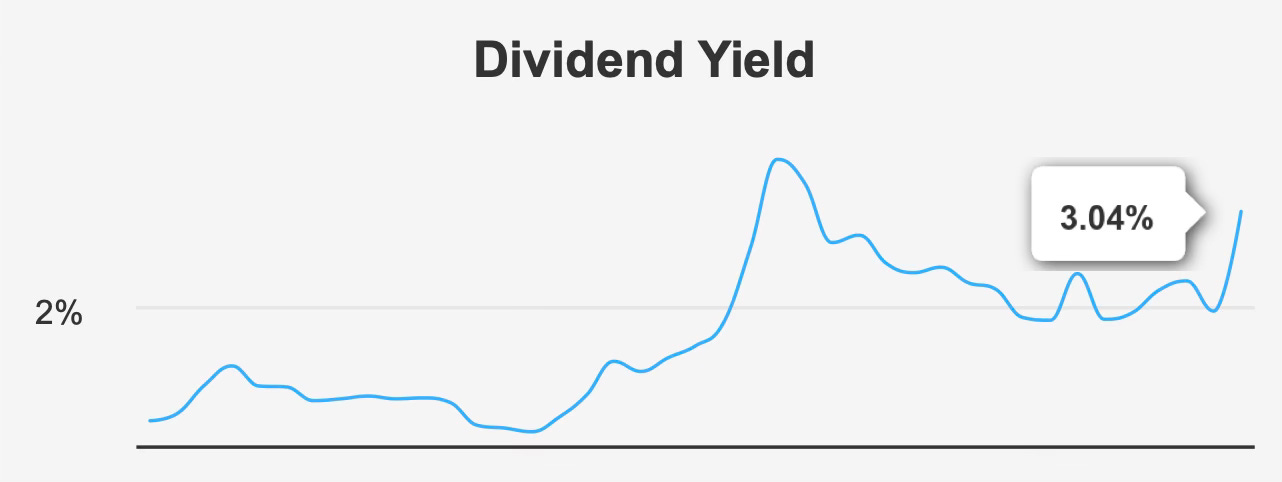

ADP’s forward dividend yield of 3.3% is meaningfully above its historical median yield of 2.0%, reflecting a more income-attractive entry point compared with prior years. Yet that yield expansion stems primarily from price compression rather than a fundamental undervaluation relative to intrinsic worth. While certain multiples sit near historical lows, the broader valuation assessment suggests limited downside protection at current levels.

The investment thesis therefore centers on a high-quality dividend franchise with durable earnings power, but one that currently trades without sufficient margin of safety to justify aggressive capital deployment. For long-term income investors, the business remains attractive; for valuation-disciplined buyers, patience appears warranted.

Earnings Momentum & Profitability Trends: Consistent Expansion with Improving Capital Efficiency Signals

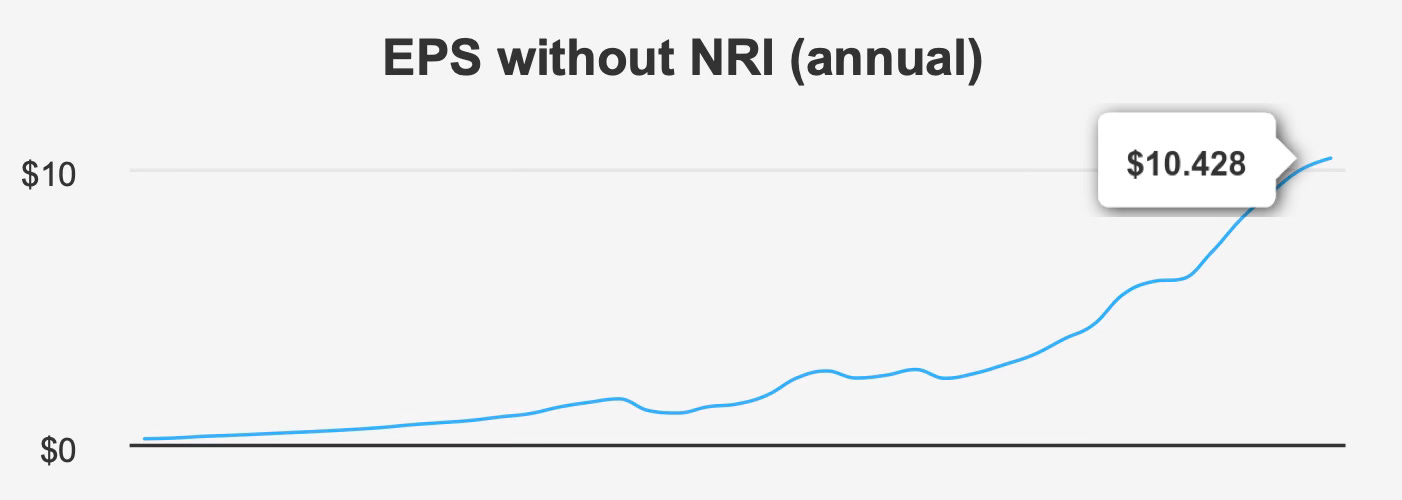

ADP’s earnings trajectory remains steady and disciplined. In the quarter ending December 2025, EPS excluding non-recurring items reached $2.62, up from $2.49 in the prior quarter and $2.35 in the same period last year. Revenue per share rose to $13.24 from $12.73 sequentially and $12.34 year over year, reflecting stable top-line progression.

Over the past five years, EPS has compounded at 12.3% annually, with a 10-year CAGR of 13.3%. That consistency underscores the structural strength of ADP’s recurring revenue model and its ability to convert client retention into durable profit growth. Revenue has expanded at a 5-year CAGR of 8.8% and a 10-year CAGR of 7.9%, indicating steady but not explosive growth—precisely the profile one expects from a mature, scaled platform business.

Margin performance has strengthened meaningfully. Gross margin reached 46.0% in the latest quarter, marking a decade high and comfortably above the 10-year median of 42.5%. Operating leverage and pricing discipline appear to be supporting incremental profitability, reinforcing earnings stability.

Capital allocation through buybacks has been measured. Over the past year, ADP repurchased shares equivalent to 1.0% of outstanding shares. While modest, this activity contributes incrementally to EPS growth. Over the past decade, buyback intensity has varied, peaking at 4.2%, suggesting management deploys repurchases opportunistically rather than mechanically.

Looking forward, consensus expectations call for revenue of $21,798.9 million by mid-2026, rising to $24,390.2 million by mid-2028. EPS is projected at $10.96 for fiscal 2026 and $11.94 for 2027. These estimates imply continued mid-single-digit revenue growth and high-single-digit to low-double-digit earnings expansion—consistent with ADP’s historical cadence.

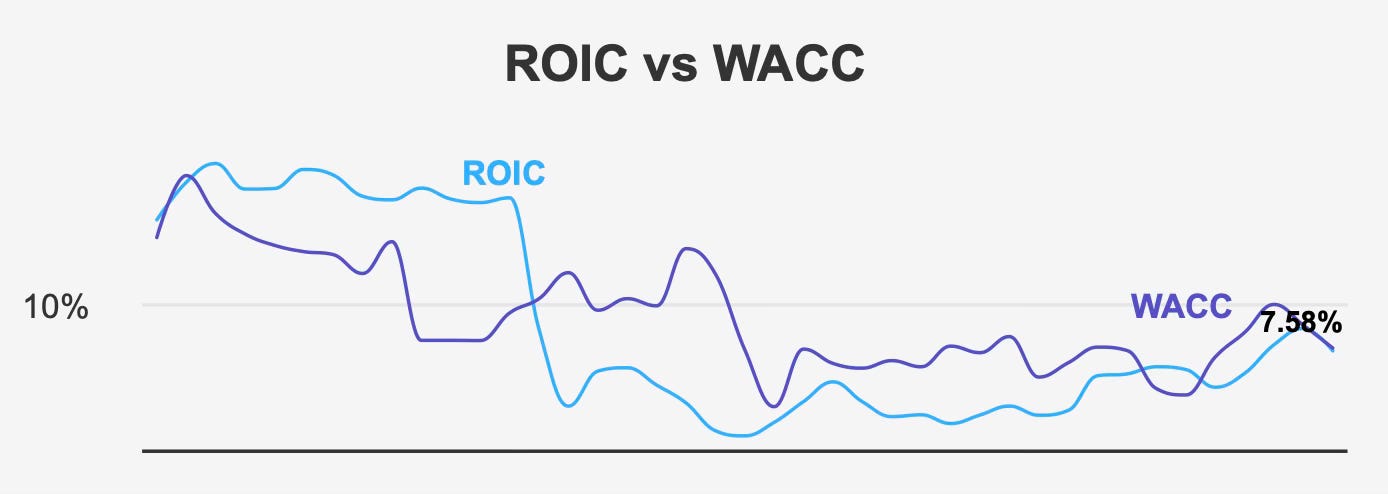

From a capital efficiency standpoint, the picture is more nuanced. The five-year median return on invested capital stands at 6.6%, with the current figure at 7.6%. While this marks improvement, it remains slightly below the five-year median weighted average cost of capital of 8.5%. The current WACC of 7.7% narrows that gap considerably, suggesting marginal economic value creation in the most recent period.

Return on equity tells a different story. Current ROE stands at 70.9%, within a 10-year range of 32.1% to 101.3%. The divergence between ROE and ROIC indicates leverage amplification, rather than purely operational superiority, as a driver of shareholder returns. While this is not inherently problematic, it reinforces the importance of disciplined balance sheet management.

Overall, earnings quality and growth remain solid, with modest but improving signals on capital efficiency. The business continues to perform with predictability.

Dividend Profile & Sustainability: Growth Track Record Supported by Conservative Leverage

ADP’s dividend remains a core component of its investment appeal. The company recently raised its quarterly dividend to $1.70 per share, continuing a multi-decade pattern of annual increases. The 5-year dividend growth rate of 12.2% and 3-year growth rate of 14.1% reflect sustained commitment to returning capital.

At current levels, the forward dividend yield of 3.04% sits near a 10-year high and materially above the historical median yield of 2.0%. That elevated yield provides income investors with a more attractive entry point compared with prior valuation peaks.

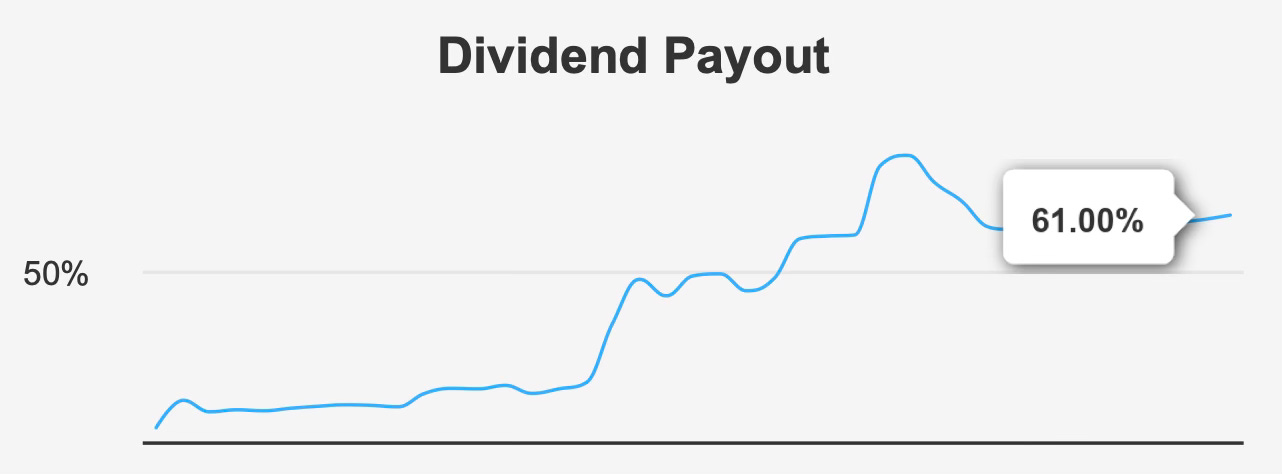

Dividend sustainability appears solid. The payout ratio stands at 61.0%, leaving room for continued increases without stressing cash flow. Dividend coverage of 1.65x supports this view, indicating adequate earnings support.

Balance sheet strength reinforces dividend durability. ADP’s debt-to-EBITDA ratio of 0.66 remains comfortably below the 2.0 threshold often associated with conservative leverage. While the company has issued $977.2 million in debt over the past three years, leverage metrics remain manageable.

Future dividend growth is estimated at 7.2%, slower than recent double-digit increases but aligned with expected earnings expansion. This moderation is consistent with a maturing growth profile rather than deterioration.

The next ex-dividend date is March 13, 2026, with payment scheduled for April 1, 2026. For income-focused investors, the combination of elevated yield, steady growth, and conservative leverage remains compelling—even if valuation considerations temper enthusiasm.

Valuation Analysis: Multiple Compression Near Historical Lows Yet Intrinsic Value Gap Persists

At $205.68 per share, ADP trades meaningfully above its intrinsic value estimate of $97.19. The implied margin of safety of -111.6% signals that current pricing embeds substantial optimism relative to discounted cash flow assumptions.

From a relative multiple perspective, valuation appears more nuanced. The forward P/E ratio of 18.7x sits near the lower end of its 10-year range, with a historical low of 19.8x. The trailing EV/EBITDA multiple of 13.0x also aligns with its decade low. Similarly, the price-to-sales ratio of 3.9x and price-to-free-cash-flow multiple of 20.0x reside near the lower ends of their historical bands.

These compressed multiples may initially suggest relative attractiveness. However, when contrasted with intrinsic value estimates, they fail to offset the broader overvaluation signal. Multiples being near cyclical lows does not inherently imply undervaluation if the underlying intrinsic framework indicates a materially lower fair value.

Price-to-book stands at 13.0x, compared with a 10-year low of 8.7x, indicating that equity valuation remains elevated relative to historical troughs.

Analyst sentiment has moderated. The latest price target of $276.80 represents a decline from $293.51 three months prior, signaling tempered expectations. While targets remain above current pricing, downward revisions often precede recalibrated growth assumptions.

In summary, while several relative metrics sit near historical lows, the intrinsic value assessment dominates the valuation discussion. Absent a material acceleration in growth or expansion in capital efficiency, current pricing offers limited valuation support.

Risk Assessment & Capital Structure Considerations: Economic Value Creation and Insider Signals Require Monitoring

ADP’s risk profile is mixed. The Altman Z-score of 1.58 places the company in the distress zone, indicating elevated bankruptcy risk within a two-year framework. While this reading contrasts with the company’s strong liquidity and stable earnings, it nonetheless warrants attention.

Insider activity adds a layer of caution. Over the past 12 months, there were 26 insider sales and no purchases. Insider ownership stands at 2.2%, while institutional ownership is 82.3%. The persistent selling trend may reflect valuation perceptions rather than operational weakness, but it reduces alignment signals at current prices.

Liquidity remains strong, with average daily trading volume of 5,717,499 shares, well above the two-month average of 2,842,239 shares. A Dark Pool Index of 70.7% indicates substantial institutional trading in non-public venues, suggesting active large-scale participation.

Government contract value increased from $7,920 million in 2018 to $10,021 million in 2023, with projections reaching $22,085 million by 2025. This expansion underscores ADP’s positioning within public-sector engagements and may offer incremental growth support.

Patent activity remains limited, with one patent granted in each of 2016, 2017, and 2023, indicating a focused but narrow innovation footprint.

While operating margins are expanding and earnings manipulation risk appears low based on forensic indicators, the combination of economic value creation concerns, insider selling, and intrinsic valuation gaps shapes the broader risk framework.

Final Assessment

Automatic Data Processing remains a high-quality dividend compounder supported by recurring revenue, global scale, disciplined capital allocation, and consistent earnings growth. Dividend growth has been robust, leverage remains conservative, and near-term earnings expectations imply continued stability.

However, at $205 per share against an intrinsic value of $97, the absence of margin of safety overshadows operational strength. Even though several valuation multiples sit near historical lows, they do not reconcile the intrinsic valuation gap.

For existing long-term income investors, ADP’s dividend stability and moderate growth outlook justify continued holding. For new capital, patience appears prudent. A more compelling entry point would require either meaningful price correction or clear evidence of sustainably higher growth and capital efficiency.

In its current state, ADP represents a strong business priced beyond conservative valuation parameters—an income-oriented franchise where quality is evident, but valuation discipline remains paramount.