ARMOUR Residential REIT: High Yield at the Crossroads of Capital Discipline

Evaluating Dividend Sustainability, Earnings Recovery, and Valuation Risk at 16% Yield

Investment Thesis: A High-Yield Mortgage REIT Confronting Structural Return Challenges

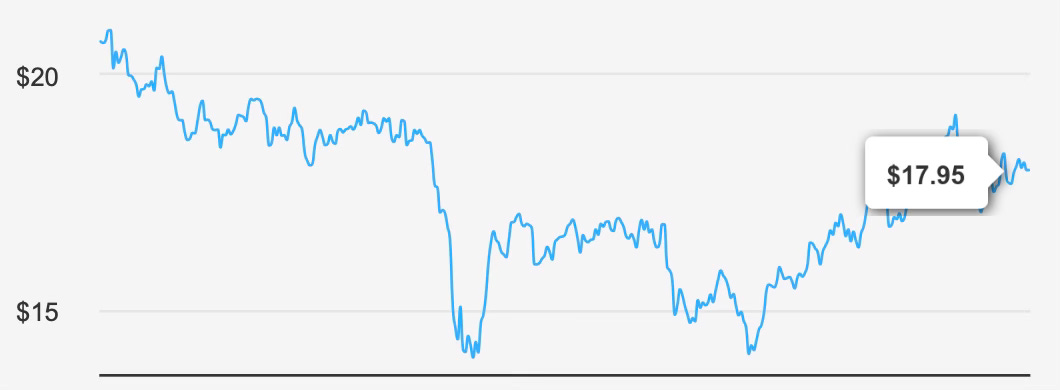

ARMOUR Residential REIT Inc ARR 0.00%↑ operates in the U.S. agency mortgage market, investing primarily in fixed-rate, adjustable-rate, and hybrid residential mortgage-backed securities issued or guaranteed by government-sponsored entities and Ginnie Mae. The portfolio also includes U.S. Treasury securities and money market instruments. At a recent share price of $17 and a market capitalization of $2.01 billion, the company sits squarely within the publicly traded agency mortgage REIT universe.

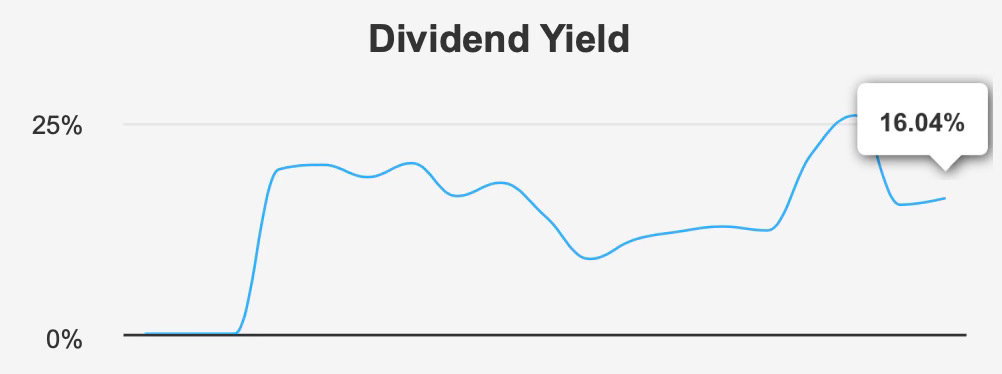

The investment case begins with yield. ARR currently offers a forward dividend yield of 16.0%, placing it among the highest-yielding securities in its peer group. That level of income is immediately compelling, particularly for investors seeking cash flow in a higher-rate environment. However, yield alone does not define quality. The durability of that payout depends on earnings stability, capital discipline, and the ability to generate returns above the cost of capital.

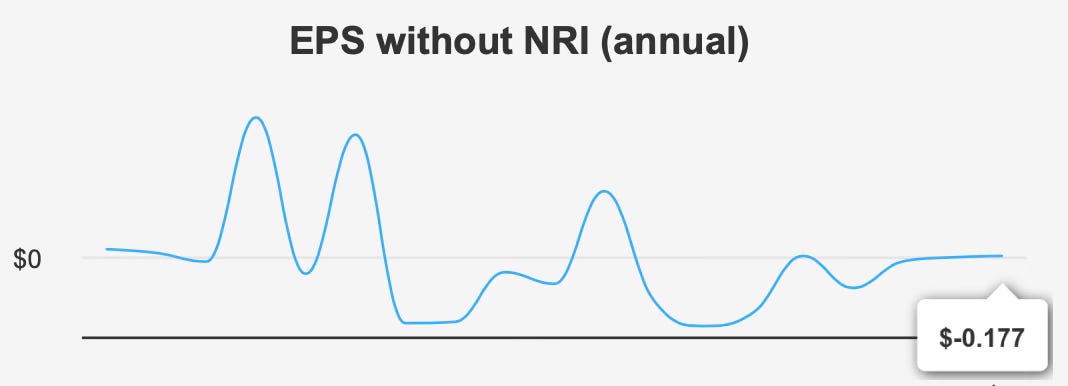

Recent quarterly results show a marked rebound. For the quarter ended September 30, 2025, earnings per share excluding non-recurring items reached $1.478, representing a 24.7% increase year over year and a significant recovery from the prior quarter’s loss of $0.96. Diluted EPS came in slightly higher at $1.49. Revenue per share improved to $1.538 from a negative $0.863 in the preceding quarter. These results suggest that portfolio performance has stabilized after a period of volatility.

Yet the broader historical record is less encouraging. While the five-year compound annual growth rate for annual EPS excluding non-recurring items stands at 44.1%, the ten-year CAGR is flat. Revenue growth over both five- and ten-year periods is 0.0%. This pattern reflects cyclical rebounds rather than sustained expansion.

More importantly, structural return metrics remain weak. Return on invested capital has been 0.0% over both five- and ten-year horizons, while the five-year median weighted average cost of capital is 11.8% and the current WACC stands at 14.0%. When capital earns less than it costs, long-term value creation becomes elusive. The core investment debate, therefore, centers on whether recent earnings momentum can evolve into consistent economic returns.

2. Earnings Momentum & Profitability Trends: Improving Results Amid Persistent Capital Efficiency Gaps

The most recent quarter marked a meaningful shift in direction. EPS excluding non-recurring items rose to $1.478, reversing prior losses and demonstrating improved operating conditions. The 24.7% year-over-year increase underscores a tangible recovery in spread performance and portfolio positioning.

Looking ahead, analysts project revenue of $154 million in 2025, rising to $340.54 million by 2027. Estimated EPS for the next two fiscal years stands at $1.420 and $2.963, respectively. If achieved, those projections would represent a substantial strengthening in earnings power and suggest that the recent rebound may extend beyond a single quarter.

However, profitability quality must be viewed through the lens of capital efficiency. Gross margin metrics are reported at 0.0% across various historical measures, reflecting the structural accounting characteristics of mortgage REITs rather than traditional operating margin dynamics. More telling is the persistent gap between returns and capital costs. A 0.0% ROIC against a WACC of 11.8% to 14.0% implies that incremental capital has not translated into economic value.

Return on equity has recently reached 3.95%. While positive, this level remains modest relative to the company’s cost of capital. Without a sustained improvement in asset yields, funding costs, or portfolio leverage efficiency, closing this gap will remain challenging.

Capital allocation trends further complicate the picture. The one-year share buyback ratio stands at -102.7%, indicating net issuance rather than repurchases. Over the past decade, the ratio is -24.2%, signaling long-term dilution. For a REIT reliant on equity markets, disciplined issuance is critical. Repeated dilution can offset earnings gains and limit per-share growth, even during periods of operational improvement.

In short, earnings momentum has returned. Whether that momentum translates into consistent economic returns remains uncertain.

3. Dividend Profile & Sustainability: Elevated Yield Supported by Volatile History

ARR’s dividend profile reflects a clear tension between current yield and historical contraction. The forward dividend yield of 16.04% is among the highest in the sector, offering substantial income for shareholders willing to accept volatility.

However, dividend growth trends tell a different story. Over the past five years, the dividend has declined at an annualized rate of 19.4%, and over three years the decline stands at 21.7%. Rather than expanding distributions, the company has reduced them in response to earnings and portfolio pressures.

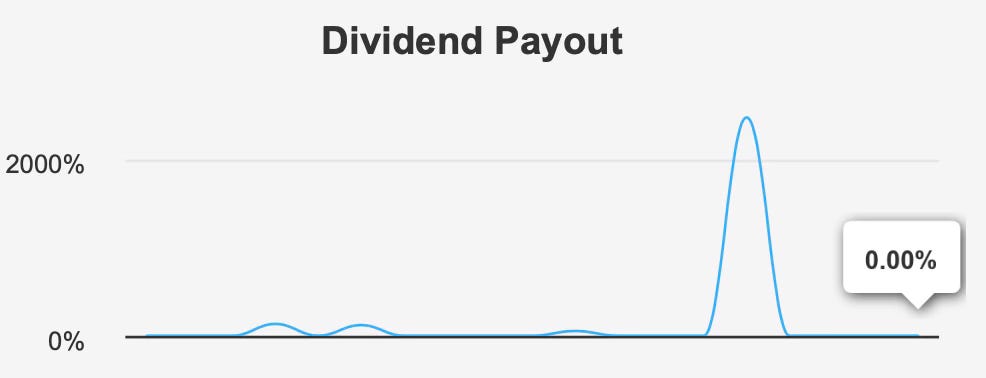

The payout ratio adds further complexity. While the current dividend payout ratio is reported at 0.0%, the ten-year median payout ratio is 112.8%, with a historical high of 125.0%. Paying out more than earnings over extended periods raises questions about long-term sustainability and capital discipline. Dividend coverage is currently negative at -0.02, reinforcing that coverage metrics are not robust.

Looking forward, the forecasted three- to five-year dividend growth rate is 0.0%, suggesting no expected increase in distributions. The next ex-dividend date is February 17, 2026, with payment scheduled for February 27, 2026, consistent with the company’s monthly distribution structure.

An important counterbalance is the balance sheet. ARR reports no debt. In an environment characterized by interest rate volatility, the absence of leverage reduces refinancing risk and interest expense pressure. This debt-free position enhances financial flexibility and may provide resilience during periods of market stress.

Overall, the dividend appears sustainable in the near term, particularly if projected earnings materialize. However, historical contraction and inconsistent payout ratios suggest that the 16.0% yield should not be viewed as permanently secure.

4. Valuation: Trading Near Historical Price-to-Book Highs Without Clear Return Expansion

Valuation for mortgage REITs is typically anchored to book value and earnings capacity. ARR currently trades at a price-to-book ratio of 0.94, approaching its ten-year high of 1.01. While still below parity, the stock is near the upper end of its historical range, limiting the margin of safety.

The share price is also close to its one-year high, indicating that recent earnings improvements may already be reflected in the market’s expectations. Without a structural improvement in return metrics, additional multiple expansion appears constrained.

Liquidity remains stable. Daily trading volume averages 3,102,055 shares, slightly below the two-month average of 3,433,865 shares. The Dark Pool Index stands at 57.7%, indicating that more than half of trading activity occurs off-exchange. While not inherently negative, elevated dark pool participation can affect price transparency and short-term volatility.

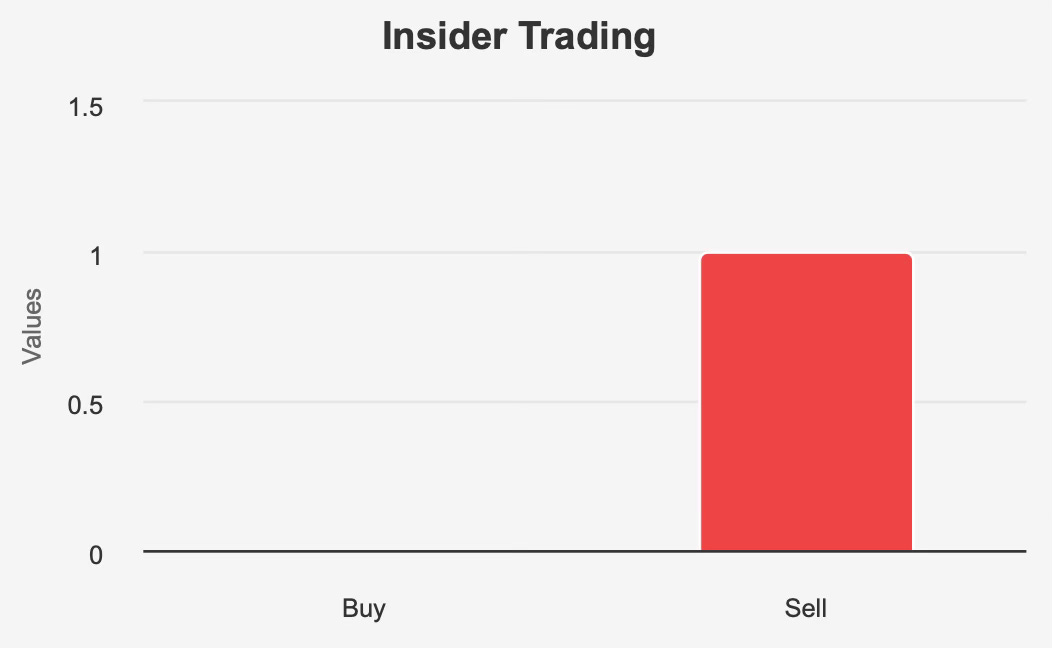

Ownership dynamics show institutional ownership at 55.7%, while insider ownership is 0.38%. Over the past year, insider activity included one sale of 6,833 shares and no purchases. Limited insider participation may reduce perceived alignment, though institutional presence can provide stability.

At 0.94x book value, ARR is neither deeply discounted nor clearly overvalued. Instead, valuation appears balanced but leaves limited room for operational missteps. Future performance will depend on sustained earnings delivery and capital efficiency improvements.

5. Risk Assessment & Capital Structure Considerations

The principal risk facing ARR is structural value destruction. A sustained ROIC of 0.0% against a WACC as high as 14.0% indicates that capital has not generated returns commensurate with its cost. Unless portfolio economics improve meaningfully, this gap may persist.

Dilution risk is another consideration. A one-year buyback ratio of -102.7% highlights significant net issuance. Over a decade, the -24.2% figure reinforces that equity dilution has been a recurring feature. For income-focused investors, per-share stability matters as much as aggregate earnings.

Dividend volatility also remains a material risk. A five-year annualized decline of 19.4% demonstrates that distributions can contract during challenging environments.

Offsetting these concerns is the absence of debt. With no reported leverage, ARR avoids the refinancing and covenant risks that can pressure other REITs during downturns. This clean balance sheet provides a degree of downside protection and strategic flexibility.

The next earnings report is scheduled for April 23, 2026. Delivery against projected EPS of $1.420 and $2.963 will be critical in determining whether the current recovery is sustainable.

Final Assessment

ARMOUR Residential REIT presents a compelling income profile alongside meaningful structural challenges. A 16.0% forward yield and improving quarterly earnings create near-term appeal. Revenue projections rising toward $340.54 million by 2027 and stronger EPS estimates suggest that operating conditions may be stabilizing.

However, the company’s historical inability to generate returns above its cost of capital remains a central concern. Dividend growth has been negative, payout ratios have exceeded earnings in the past, and share issuance has diluted equity over time.

Trading at 0.94x book value and near historical valuation highs, ARR offers limited valuation cushion. The absence of debt strengthens the balance sheet, but sustainable long-term value will require consistent earnings coverage and improved capital efficiency.

For investors prioritizing immediate income and willing to accept volatility, ARR may serve as a tactical allocation. For long-term investors seeking durable compounding driven by economic value creation, a more cautious approach appears warranted until return metrics demonstrate sustained improvement.