Apple Hospitality REIT (APLE): High Yield at a Discounted Valuation Amid Structural Return Pressures

Assessing Dividend Sustainability, Capital Efficiency, and Balance Sheet Risk in a Moderately Leveraged Lodging REIT

Investment Thesis: Discounted Lodging REIT Offering Elevated Yield with Constrained Value Creation Dynamics

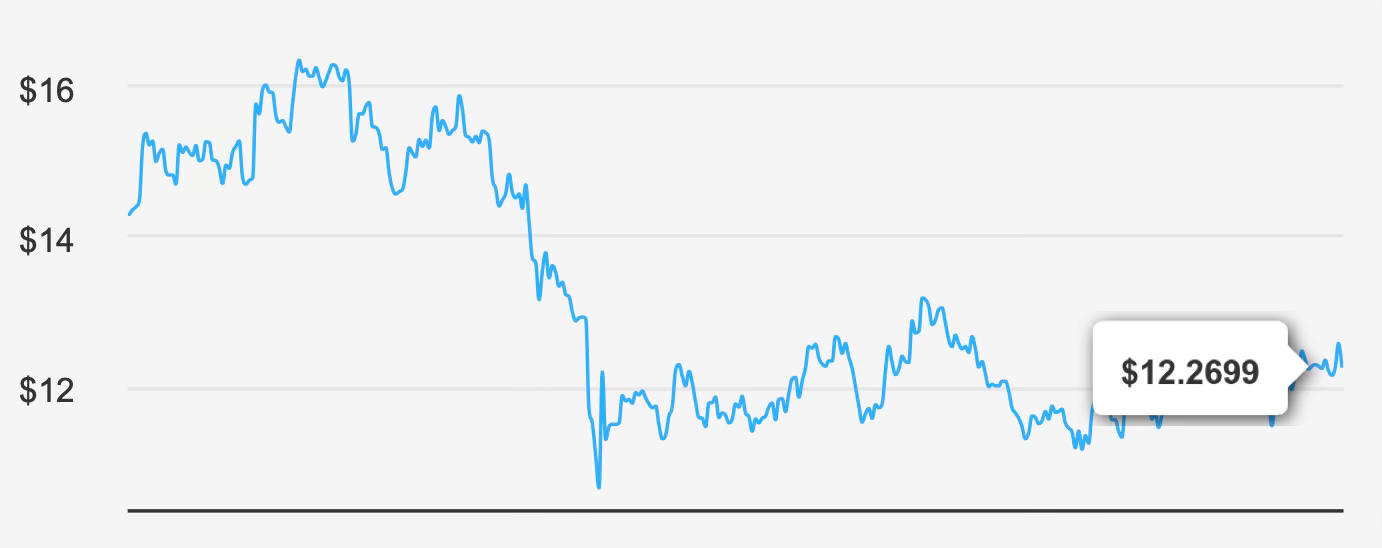

Apple Hospitality REIT APLE 0.00%↑ is currently trading at $12 per share with a market capitalization of approximately $2.88 billion. The stock carries an estimated intrinsic value of $15.37, implying a margin of safety of 20.7%. On valuation alone, the shares appear modestly undervalued. The forward dividend yield stands at 7.9%, positioning the company as an income-oriented opportunity within the REIT sector.

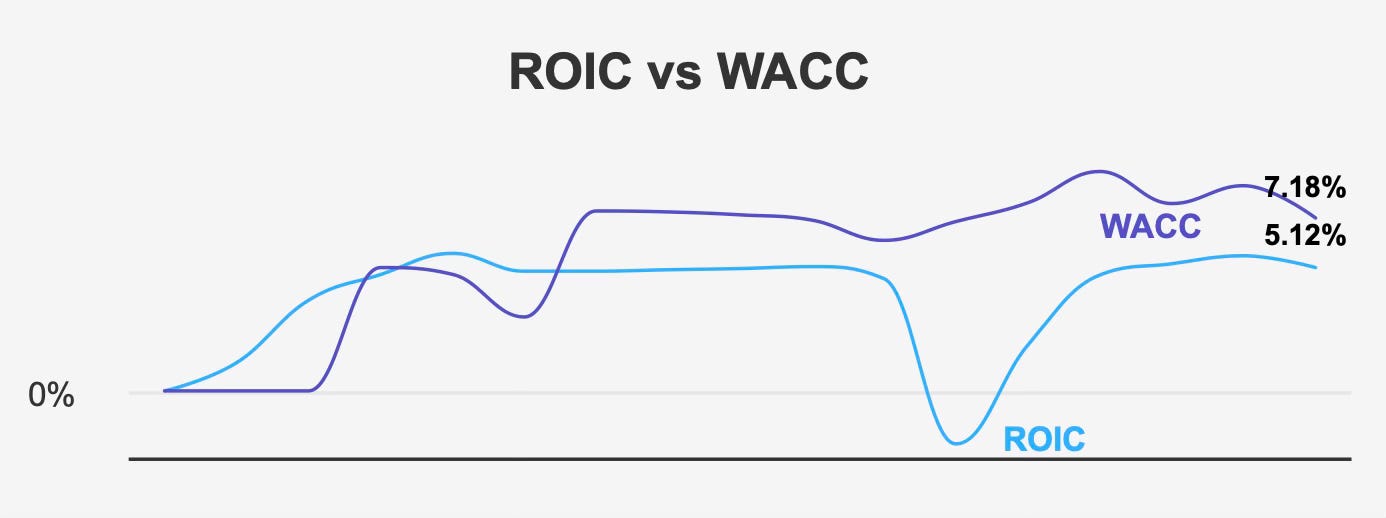

However, the investment case requires careful qualification. While valuation and yield are compelling on the surface, the company’s capital efficiency metrics reveal structural challenges. Over the past five years, median return on invested capital has been 4.8%, well below the 7.8% weighted average cost of capital. The most recent figures show ROIC at 5.1% versus a WACC of 7.2%. This persistent spread indicates that the company has not consistently generated economic value above its financing costs.

Operational momentum has also been uneven. Earnings per share excluding non-recurring items declined to $0.216 in the most recent quarter, down from $0.27 in the prior quarter and below $0.242 in the comparable quarter last year. Revenue per share edged down sequentially to $1.577 from $1.617 but remained essentially flat year over year.

The core question for long-term dividend investors is whether the current valuation discount sufficiently compensates for muted growth, capital return inefficiencies, and elevated payout risk. The answer depends on one’s tolerance for leverage and cyclicality in the lodging sector.

Earnings Momentum & Profitability Trends: Moderating Growth Against Margin Compression

Apple Hospitality operates exclusively in the U.S. lodging sector, focusing on upscale service hotels under Marriott and Hilton brands. Its revenue base is entirely derived from hotel operations, making performance closely tied to travel demand and macroeconomic conditions.

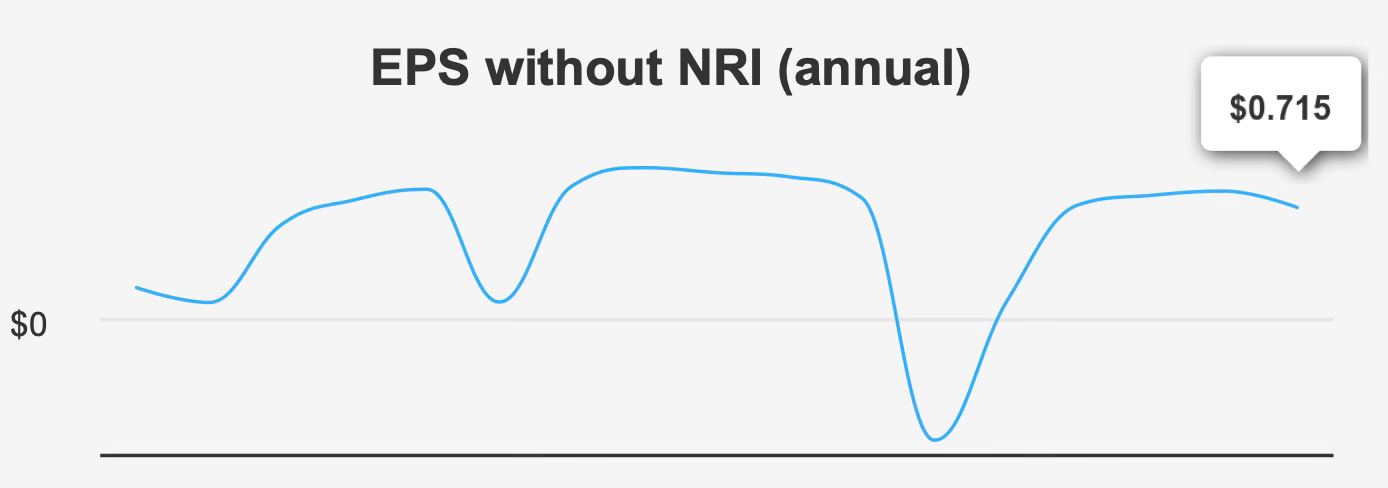

Over longer time horizons, growth has been modest. Five-year revenue growth stands at 8.5%, while ten-year revenue growth has averaged just 0.8%. Annual EPS without non-recurring items has posted a five-year compound annual growth rate of 0.0%, indicating that earnings expansion has effectively stalled over that period.

In the most recent quarter ended September 30, 2025, diluted EPS was $0.21, down from $0.27 in the prior quarter. The decline reflects softer operating leverage and margin compression. Gross margin came in at 34.0%, below the five-year median of 35.6% and the ten-year median of 36.7%. While not a dramatic deterioration, the direction is notable and consistent with a more normalized post-recovery lodging environment.

Analyst expectations point to modest stabilization rather than acceleration. EPS is projected at $0.71 for fiscal 2026, rising slightly to $0.74 the following year. Revenue is expected to grow from $1,409.1 million in 2025 to $1,470.9 million by 2027. This represents gradual top-line expansion rather than a cyclical surge.

Share count dynamics have provided limited support. Over the past year, the company achieved a 1.3% buyback ratio, reflecting a minor reduction in outstanding shares. Over longer periods, however, net buyback ratios have been negative, suggesting dilution has outweighed repurchases historically.

The broader industry outlook suggests moderate hospitality sector growth over the next decade. For Apple Hospitality, this likely translates into steady but unspectacular earnings progression unless operational efficiencies improve meaningfully.

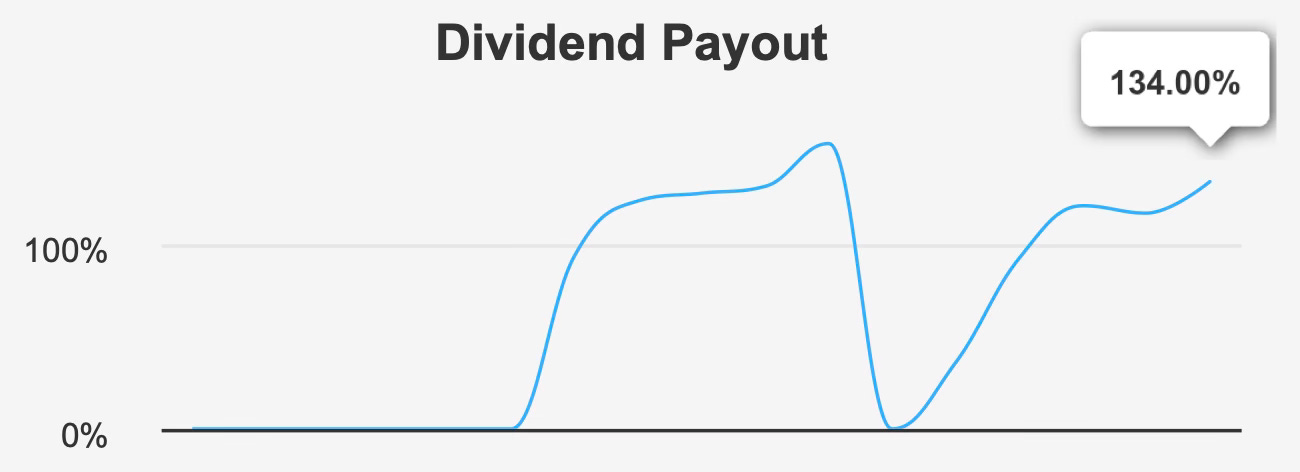

Dividend Profile & Sustainability: Attractive Yield Offset by Elevated Payout Risk

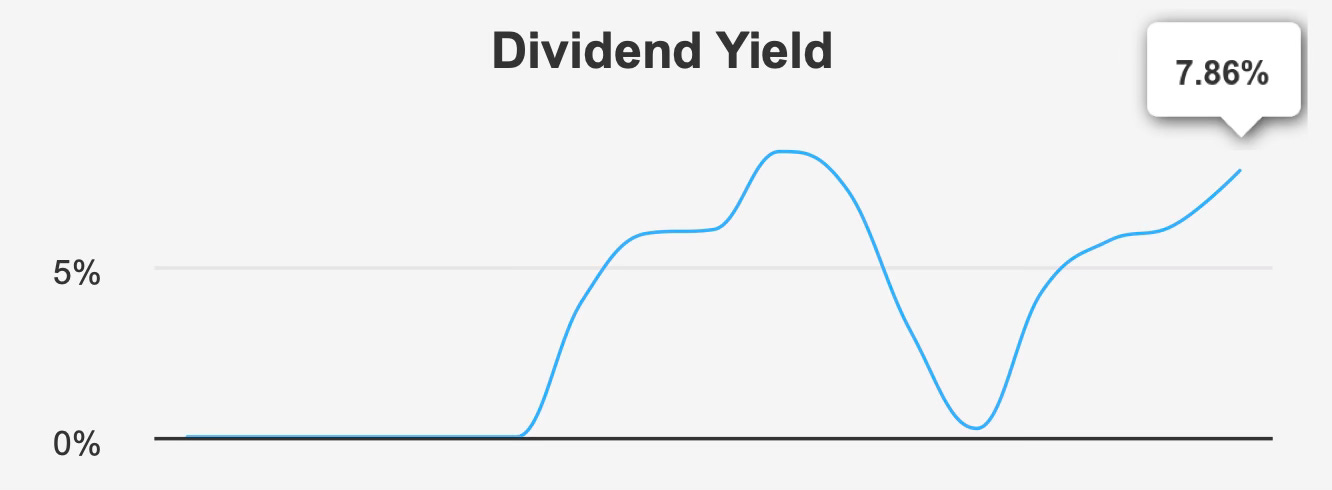

Income is the primary attraction here. The forward dividend yield of 7.9% is near five-year highs and stands out within the REIT universe. The company has delivered strong recent dividend growth, with a five-year growth rate of 20.1% and a three-year rate of 188.4%. These figures reflect recovery-driven normalization following pandemic-era cuts rather than purely organic expansion.

Looking ahead, dividend growth expectations are far more restrained. The projected forward growth rate is just 0.8%, signaling a likely plateau.

The more pressing concern is coverage. The current dividend payout ratio stands at 134%, well above the ten-year historical median of 101.2%. Dividend coverage is 0.76x, indicating earnings do not fully cover distributions. While REITs often rely on funds from operations metrics rather than GAAP EPS, the elevated payout ratio still underscores tight coverage conditions.

The quarterly dividend per share remains at $0.08, with the most recent ex-dividend date on February 27, 2026, and the payout scheduled for March 16, 2026. Consistency in payment timing supports income reliability, but sustainability ultimately depends on stabilizing earnings and cash flow.

Leverage adds another dimension. Debt-to-EBITDA stands at 3.6x, placing the company in a moderate risk category. While not excessive for a lodging REIT, leverage must be assessed in conjunction with return spreads. With ROIC below WACC, incremental debt-funded investment does not currently enhance shareholder value.

The dividend remains attractive for income-focused investors, but its sustainability hinges on maintaining operating performance without further margin compression.

Valuation Analysis: Discount to Intrinsic Value Supported by Sub-Median Trading Multiples

At $12.19 per share, Apple Hospitality trades below its estimated intrinsic value of $15.37, implying a 20.7% margin of safety. From a multiple perspective, the valuation appears reasonable relative to historical norms.

The forward P/E ratio is 16.6x, closely aligned with the trailing P/E of 16.7x. Over the past decade, the company’s P/E has ranged from 7.0x to 230.6x, with a median of 21.5x. The current multiple sits meaningfully below that median, suggesting valuation compression rather than earnings exuberance.

Enterprise value to EBITDA stands at 10.0x, below the ten-year median of 12.8x. This indicates the stock is trading at a discount relative to its historical operating valuation benchmarks. The price-to-book ratio of 0.9x is also below the ten-year median of 1.1x, implying the shares are priced below book value.

Analyst coverage is limited, with only one analyst providing a price target of $13.14. That target sits modestly above the current price but below intrinsic value estimates, suggesting tempered external expectations.

Taken together, valuation metrics consistently indicate the shares trade below historical norms and below estimated intrinsic value. The discount likely reflects concerns around return on capital, payout sustainability, and financial stability rather than short-term earnings risk.

Risk Assessment & Capital Structure Considerations: Leverage, Return Spread Deficits, and Financial Stress Indicators

Risk evaluation reveals more pronounced concerns.

Over the past three years, long-term debt issuance totaled $187.0 million, increasing leverage and reducing financial flexibility. Although the debt-to-EBITDA ratio of 3.6x remains manageable, the broader financial health picture warrants scrutiny.

The Altman Z-score stands at 1.06, placing the company in the distress zone and signaling heightened bankruptcy risk within a two-year horizon. While this model can be imperfect for REITs, the reading is materially weak and should not be dismissed outright.

The return spread remains negative, with ROIC below WACC. This structural gap indicates capital deployment has not generated value above cost of capital. Without improvement, growth initiatives may dilute rather than enhance returns.

On the positive side, insider behavior has been supportive. Over the past year, there were 13 insider purchases and no insider sales. One purchase occurred in the last three months, and three over the past six months. Insider ownership stands at 3.0%, while institutional ownership is high at 83.9%. Persistent insider buying may signal internal confidence, though it does not eliminate structural financial concerns.

The Beneish M-Score of -2.71 suggests a low probability of earnings manipulation. Liquidity remains adequate, with daily trading volume of 1.4 million shares, though below the two-month average of 2.1 million shares. A Dark Pool Index of 55.5% indicates substantial institutional trading activity off-exchange.

Collectively, the risk profile is best characterized as moderate to elevated. The balance sheet is not overextended, but financial stress indicators and capital inefficiency temper the attractiveness of the valuation discount.

Final Assessment

Apple Hospitality REIT presents a nuanced opportunity.

On valuation grounds, the shares appear modestly undervalued. Trading at 0.9x book value, 10.0x EV/EBITDA, and 16.6x forward earnings, the stock sits below historical medians and below estimated intrinsic value. The 20.7% margin of safety provides a measurable cushion.

The dividend yield of 7.9% is compelling, particularly for income-oriented investors seeking current cash flow. Insider buying and strong institutional ownership add incremental confidence.

Yet the company’s structural return profile raises legitimate caution. ROIC remains below WACC, payout ratios exceed sustainable thresholds, and the Altman Z-score signals financial fragility. Earnings growth projections are incremental rather than transformative.

For investors prioritizing income and valuation discipline, Apple Hospitality may merit consideration within a diversified REIT allocation. However, expectations should be calibrated toward stable yield rather than capital appreciation driven by expanding returns on invested capital.

The stock’s appeal ultimately rests on whether management can stabilize margins, improve capital efficiency, and align payout policy more closely with earnings power. Until return spreads turn positive, the discount appears justified — though potentially attractive for patient, income-focused shareholders willing to accept moderate risk.