Agree Realty Corporation: Dividend Stability Meets Capital Discipline Questions

A Close Examination of Growth Durability, Payout Risk, and Valuation at Fair Value

Investment Thesis: Durable Retail Net-Lease Platform Trading at Intrinsic Value

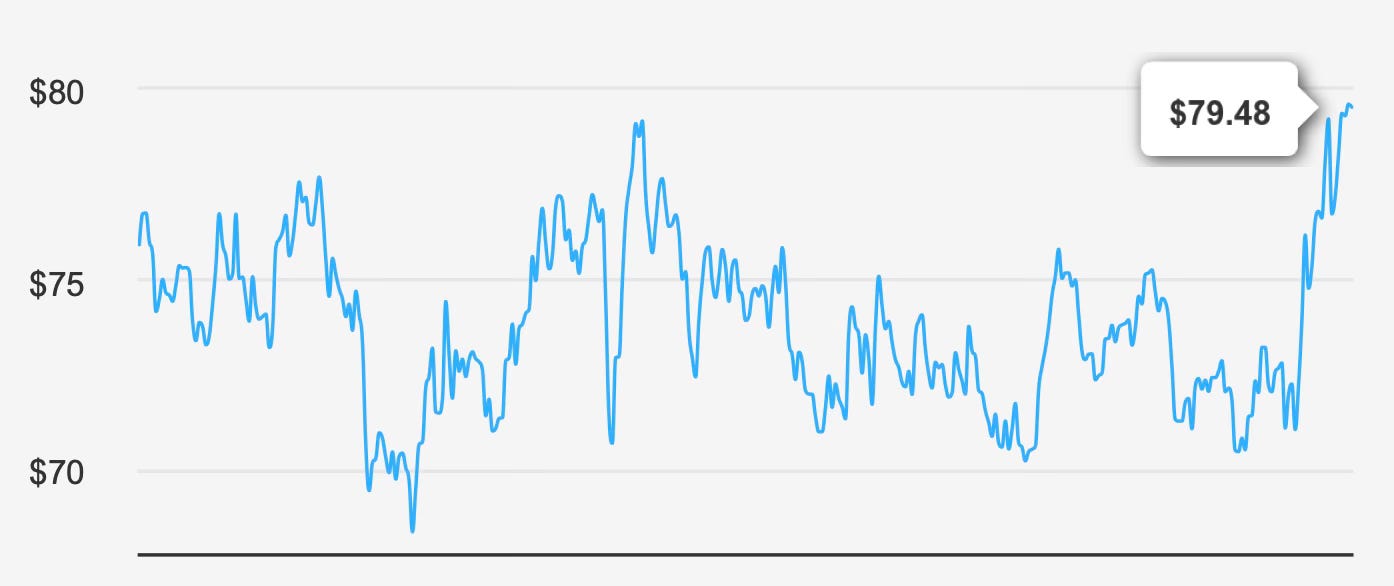

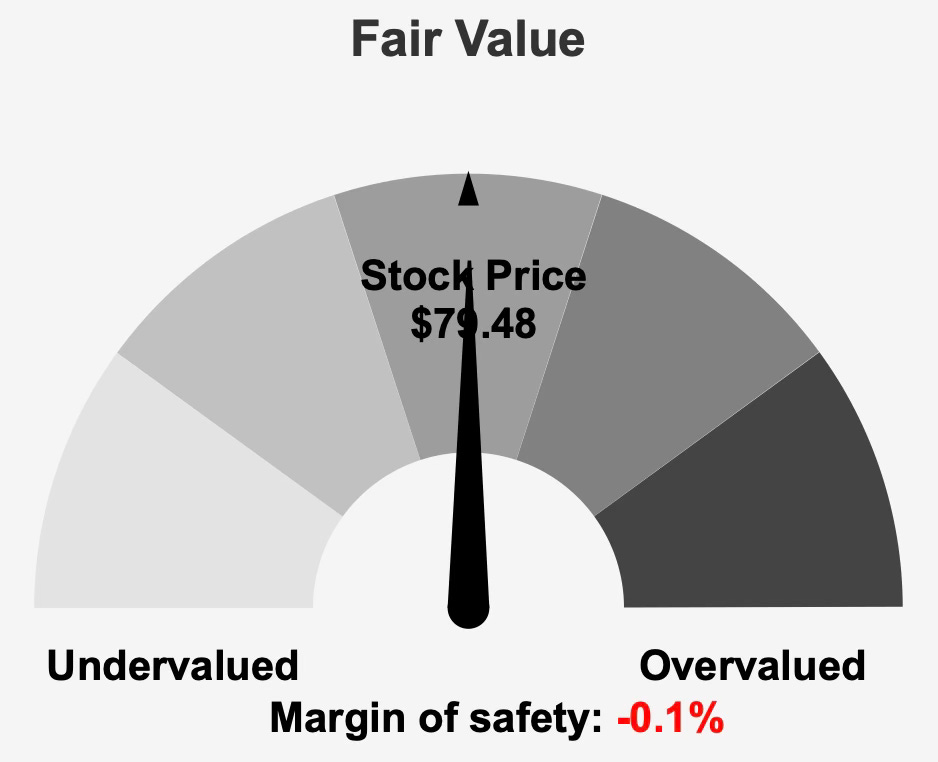

Agree Realty Corporation ADC 0.00%↑ operates as a fully integrated retail-focused net-lease REIT, owning, acquiring, developing, and managing properties leased to industry tenants including Walmart, 7-Eleven, Wawa, and Gerber Collision. With a market capitalization of $9.54 billion and a current share price of $79, the stock trades almost exactly at its calculated intrinsic value of $79.39, leaving a margin of safety of -0.1%.

The core investment case rests on three pillars: steady top-line expansion, disciplined share repurchases, and a competitive dividend yield supported by long-term growth in revenue. Over the past five years, revenue has compounded at 7.0%, and over ten years at 5.7%, reflecting consistent portfolio expansion. Analysts expect revenue to continue climbing, reaching $791.46 million in 2026, $852.82 million in 2027, and $956.2 million in 2028.

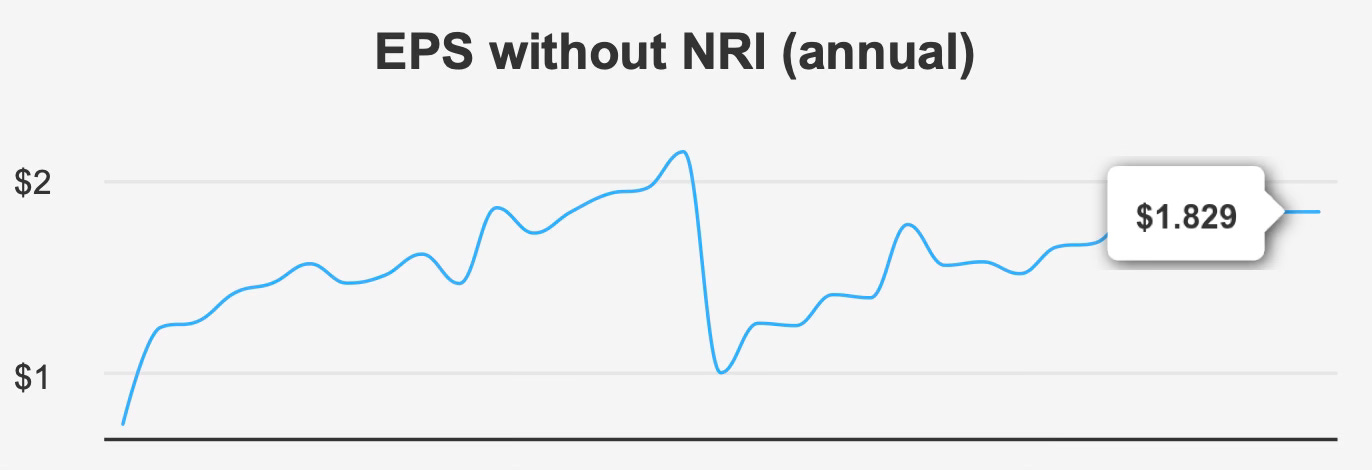

At the earnings level, growth has been steady but modest. Five-year and ten-year EPS without non-recurring items (NRI) compounded at 1.0% and 1.3%, respectively. While that pace is not rapid, it demonstrates resilience through varying economic cycles. Importantly, share count reduction has enhanced per-share metrics. Over the past decade, the company repurchased 20.1% of shares outstanding, with a 1-year buyback ratio of -11.9% and a three-year median of -14.6%. This sustained capital return policy has supported EPS even as operating margins experienced mild pressure.

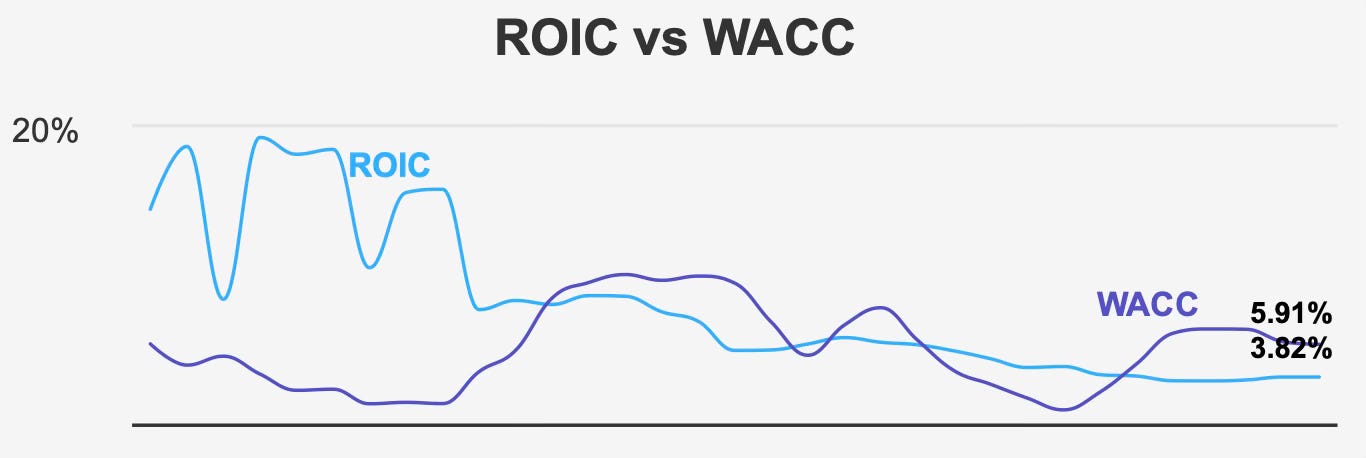

The challenge lies not in growth consistency, but in capital efficiency. Return on invested capital stands at 3.82%, below the weighted average cost of capital of 5.91%. That gap suggests expansion has not yet translated into economic value creation. For long-term dividend investors, this dynamic introduces an important balancing act: revenue and asset growth are evident, but incremental capital has not consistently earned above its cost.

With the stock trading at intrinsic value and valuation multiples near historical medians, the investment thesis is less about re-rating potential and more about execution. Continued revenue growth and disciplined capital allocation must translate into improved returns on capital to justify sustained dividend expansion.

2. Earnings Momentum & Profitability Trends

In the quarter ended December 31, 2025, ADC reported EPS without NRI of $0.465, modestly below the $0.468 recorded in Q3 2025 but above the $0.406 earned in Q4 2024. Diluted EPS reached $0.47, reflecting effective cost management despite margin compression. Revenue per share increased to $1.741 from $1.533 a year earlier, maintaining a consistent upward trajectory.

Gross margin in the latest quarter measured 86.5%, slightly below the five-year median of 87.8% and the ten-year median of 87.7%. The compression is not severe, but it reinforces a broader pattern: profitability has not meaningfully expanded even as assets have grown.

Capital efficiency remains the more pressing concern. Current ROIC of 3.82% trails WACC of 5.91%. Over the past five years, the median ROIC was 3.63%, while median WACC stood at 6.62%. Even at its ten-year peak of 5.49%, ROIC has struggled to consistently exceed capital costs. The ten-year low of 3.57% highlights how narrow the improvement band has been.

Operating margin has declined at an average rate of 2.5% per year, suggesting incremental acquisitions and developments have not meaningfully improved profitability. Additionally, asset growth has averaged 19.6% annually, significantly outpacing revenue growth of 7.0%. That divergence may indicate balance sheet expansion is running ahead of organic revenue generation.

Still, forward estimates remain constructive. Analysts project EPS of 2.035 for fiscal 2026 and 2.260 for fiscal 2027. If achieved, that progression would mark a return to moderate earnings momentum, supported by forecast revenue expansion toward $956.2 million by 2028.

In sum, earnings growth is stable but not accelerating. The key variable is whether incremental investment can narrow the ROIC–WACC gap, converting asset growth into genuine economic profit.

3. Dividend Profile & Sustainability

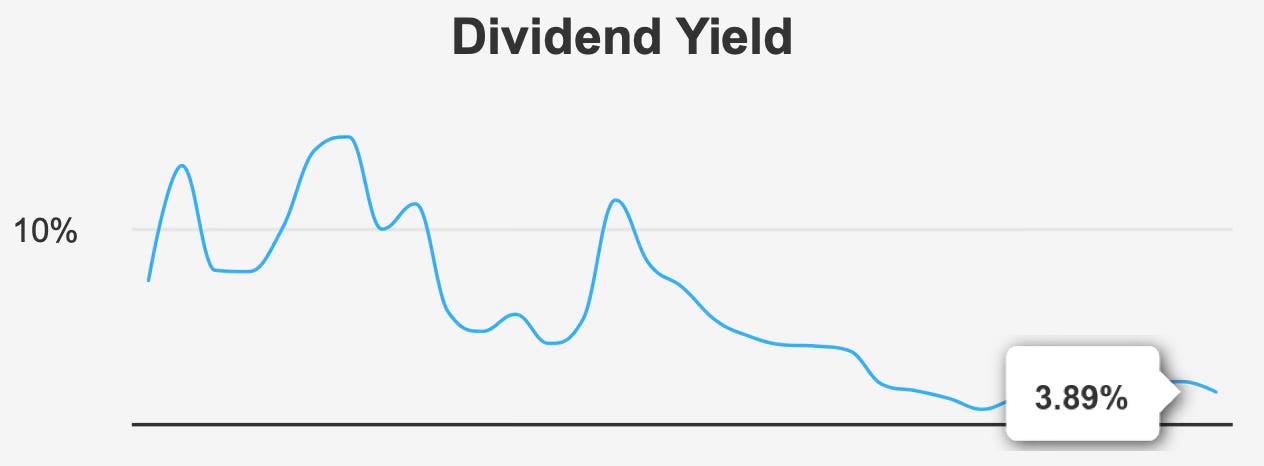

ADC’s dividend remains central to its investment appeal. The forward yield stands at 3.89%, marginally above the ten-year median of 3.95%, positioning the stock competitively within the REIT income universe. The most recent quarterly dividend of $0.262 reflects continued commitment to shareholder returns. The next ex-dividend date is February 27, 2026, with payment scheduled for March 13, 2026.

Dividend growth has been steady but moderating. Over the past five years, distributions have grown at a 5.0% annual rate, while the three-year growth rate is 3.2%. Forecast growth for the next three to five years is projected at 2.6%, signaling a gradual slowdown consistent with more measured earnings expansion.

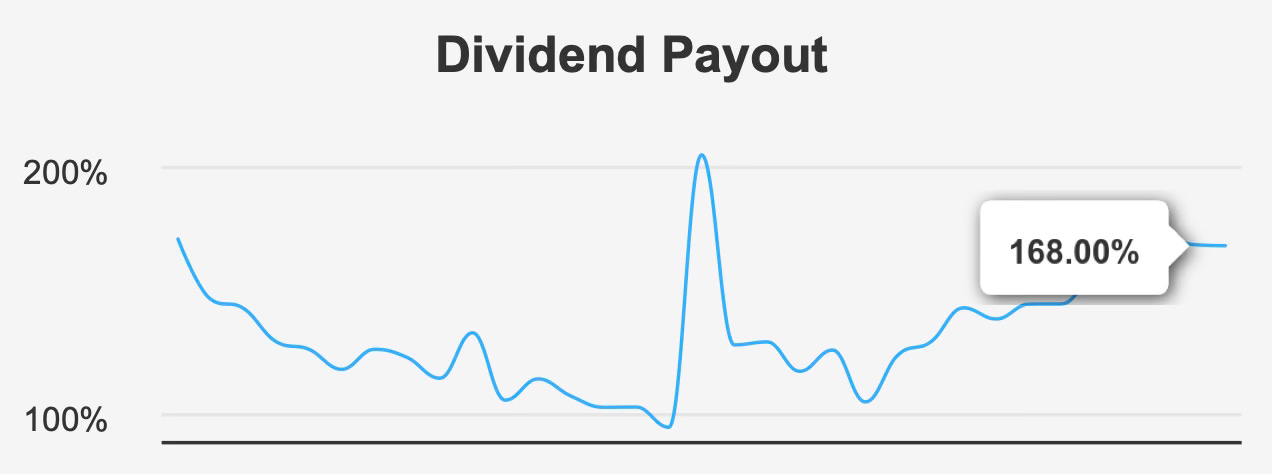

The more material issue is payout sustainability. The current dividend payout ratio is 168.0%, well above the ten-year median of approximately 101.4%. Dividend coverage stands at 0.57, indicating distributions materially exceed earnings. While REIT accounting often differs from traditional payout calculations, the elevated ratio nevertheless constrains flexibility.

Leverage compounds the concern. Debt-to-EBITDA stands at 5.61, above the 4.0 threshold commonly viewed as high financial risk. Over the past three years, ADC issued $1.3 billion in debt, reflecting continued capital deployment. While leverage is not uncommon in the REIT structure, the combination of elevated payout and rising debt reduces the margin for operational missteps.

Notably, the dividend yield is at a three-year low despite the payout increase, suggesting the share price has appreciated relative to distribution growth. This dynamic limits yield-based upside unless earnings accelerate.

Taken together, the dividend remains attractive in nominal yield terms, but sustainability hinges on improving coverage and stabilizing leverage metrics. Without meaningful expansion in earnings or cash flow, dividend growth is likely to remain modest.

4. Valuation Analysis: Fair Value Pricing Leaves Limited Margin for Error

ADC currently trades at $79, nearly identical to its intrinsic value estimate of $79.39. The resulting margin of safety of -0.1% underscores how tightly aligned market pricing is with underlying valuation assumptions.

The forward P/E ratio of 36.8x sits slightly above its ten-year median of 36.6x, reflecting a valuation in line with historical norms. EV/EBITDA stands at 21.8x compared with a ten-year median of 20.2x, indicating a modest premium. Price-to-book of 1.56x is close to its long-term median of 1.60x, suggesting asset valuation remains consistent with historical levels. Price-to-free-cash-flow of 17.5x is marginally below the ten-year median of 17.9x, while price-to-sales of 12.2x compares to a median of 12.6x.

None of these multiples imply material undervaluation or excess exuberance. Rather, they suggest a business priced appropriately relative to its own history. Analyst price targets reinforce that view, with a consensus target of $81.85 across 20 ratings, implying limited upside from current levels.

When valuation offers little cushion, performance execution becomes paramount. Any disappointment in earnings growth or further deterioration in capital efficiency could quickly compress multiples. Conversely, sustained revenue expansion combined with improved returns on capital could justify maintaining current valuation levels.

In short, ADC appears fairly valued. The absence of a meaningful discount shifts the investment case toward income reliability rather than capital appreciation.

5. Risk Assessment & Capital Structure Considerations

Risk factors center on leverage, capital efficiency, and payout coverage. The ROIC of 3.82% relative to WACC of 5.91% signals that incremental investment has not consistently generated economic value. Persistent underperformance against cost of capital raises long-term strategic questions.

The Altman Z-score of 1.72 suggests financial distress risk remains present, though not acute. Continued debt issuance totaling $1.3 billion over three years reinforces balance sheet expansion as a primary funding mechanism.

Insider behavior provides a counterpoint. Over the past twelve months, 11 insider buy transactions were recorded, with no selling activity. Seven purchases occurred in the past six months and three within the last three months. Insider ownership stands at 1.88%, complemented by institutional ownership of 111.71%. This alignment suggests internal confidence despite capital structure concerns.

Liquidity conditions appear adequate under normal trading volumes. The two-month average daily volume of 1,278,709 shares supports reasonable market depth, though recent daily volume of 114,391 indicates temporarily lighter activity. A Dark Pool Index of 47.07% implies nearly half of trading occurs off-exchange, potentially influencing price discovery dynamics.

Operating risks include declining operating margins and asset growth that materially outpaces revenue growth. If revenue expansion does not catch up to asset deployment, returns on capital may remain pressured.

Overall risk is moderate. The company benefits from stable tenant relationships and predictable revenue streams, but leverage and payout metrics require careful monitoring.

Final Assessment

Agree Realty Corporation presents a disciplined, retail-focused net-lease platform with consistent revenue growth and a competitive 3.96% forward dividend yield. The business demonstrates steady top-line expansion and meaningful share repurchases, having reduced share count by 20.1% over the past decade.

However, capital efficiency remains the central constraint. ROIC of 3.82% continues to trail WACC of 5.91%, indicating expansion has not yet translated into economic value creation. A dividend payout ratio of 168.0% and Debt-to-EBITDA of 5.61 limit financial flexibility, particularly in a higher-rate environment.

Valuation reflects these trade-offs. At $79 per share and trading essentially at intrinsic value, ADC offers little margin for error. Multiples cluster near historical medians, reinforcing the view that the market has appropriately priced both strengths and risks.

For income-oriented investors seeking stable yield with moderate growth, ADC remains a viable holding. Yet without a discount to intrinsic value or a clear inflection in capital returns, the stock warrants a measured stance. Continued monitoring of earnings growth, dividend coverage, and leverage trends will determine whether the current fair valuation evolves into opportunity—or constraint—over the coming years.