AGNC Investment Corp Dividend Review: Income Appeal Amid Economic Value Pressures

Evaluating Sustainability, Capital Efficiency, and Risk in a Leveraged Mortgage REIT

Investment Thesis: High Current Income Supported by Trading Liquidity, Constrained by Structural Value Creation Challenges

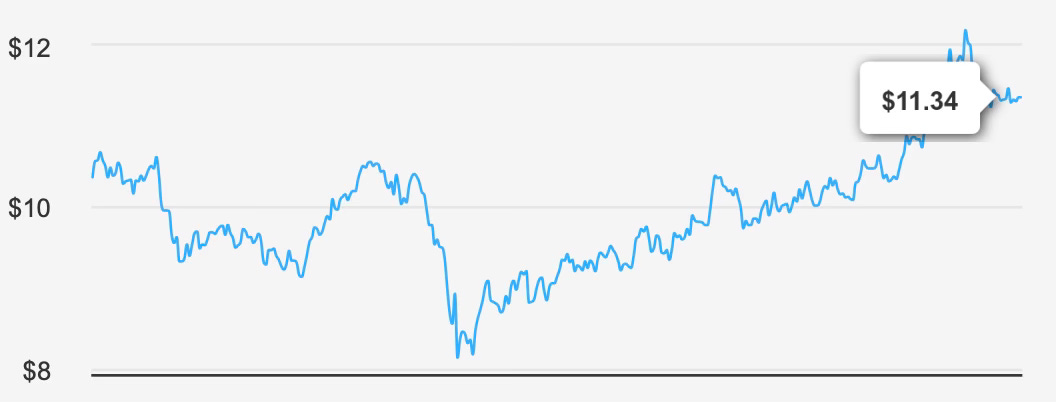

AGNC Investment Corp AGNC 0.00%↑ operates as a mortgage REIT focused primarily on agency residential mortgage-backed securities guaranteed by U.S. government-sponsored enterprises and federal agencies. At a recent price of $11, the company carries a market capitalization of $12.57 billion and currently offers a forward dividend yield of 12.7%.

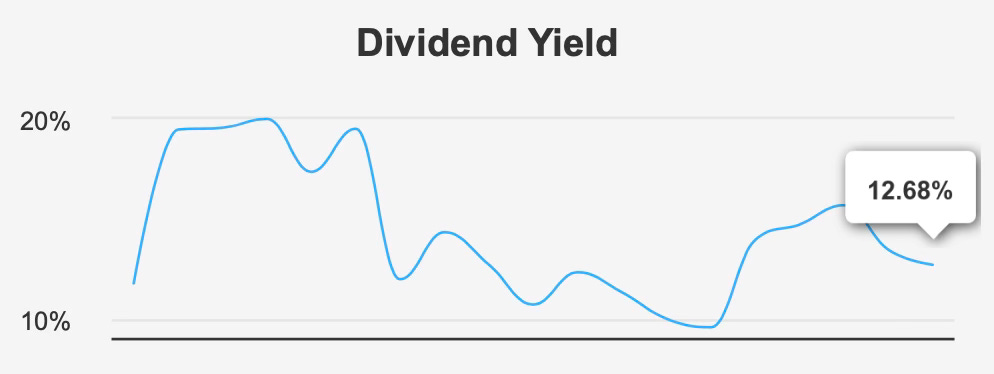

The core appeal of AGNC is straightforward: it is positioned as a high-income vehicle within the REIT sector, supported by monthly distributions and substantial trading liquidity. The forward yield of 12.7% stands materially above typical equity income alternatives and closely aligns with its 10-year median yield of 12.4%, suggesting the market continues to value the company primarily on income generation rather than growth.

However, beneath the surface, structural concerns are evident. Over the past five years, dividend growth has declined at an annualized rate of -5.2%, and revenue growth has been flat over both five- and ten-year periods. This stagnation reflects the inherent cyclicality and rate sensitivity of the mortgage REIT model.

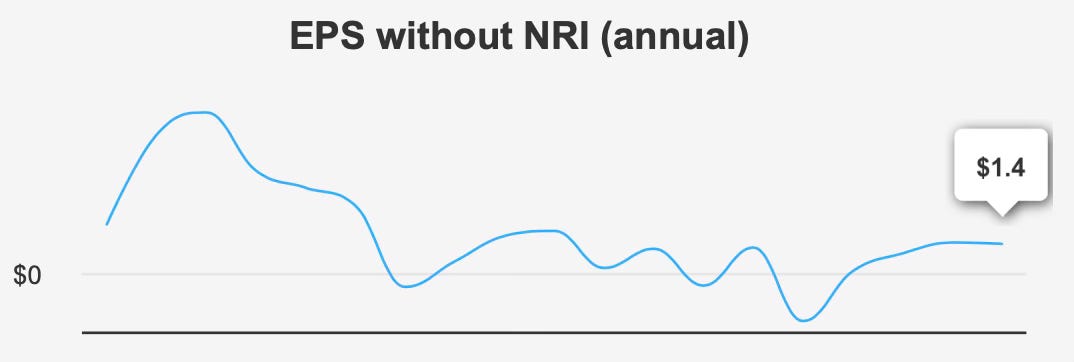

Recent earnings improvement has stabilized near-term sentiment, and analysts project EPS of $1.485 in the next fiscal year, followed by $1.308 in the subsequent year. While this suggests near-term resilience, AGNC’s long-run economic value creation remains under pressure due to its inability to generate returns above its cost of capital.

The investment case therefore rests on whether investors are being adequately compensated—via yield—for accepting persistent capital efficiency challenges and dividend sustainability risk.

Earnings Momentum & Profitability Trends

AGNC delivered a meaningful rebound in late 2025. Fourth-quarter EPS excluding non-recurring items reached $0.83, up from $0.72 in the prior quarter and dramatically higher than $0.10 in the same quarter a year earlier. This represents a clear recovery from the negative $0.17 reported in Q2 2025, indicating improved spread dynamics and portfolio performance.

Revenue per share followed a similar trajectory, rising to $0.909 in Q4 2025 from $0.791 in Q3 and $0.174 in Q4 2024. The sequential and year-over-year improvement suggests stabilization in interest rate volatility and asset pricing conditions that had previously pressured book value and earnings.

Despite this rebound, structural profitability metrics remain weak. Over the past five years, AGNC’s median return on invested capital stands at 0.0%, while its weighted average cost of capital averaged 22.3%. The current WACC is even higher at 35.8%, far exceeding returns generated on invested capital.

This gap between ROIC and WACC indicates persistent economic value destruction. Even with a return on equity of 15.5%, the firm’s capital structure and funding costs limit its ability to convert accounting profitability into true economic gains.

Industry forecasts suggest moderate long-term growth of approximately 5–6% over the next decade. While stable, this outlook does not materially alter the capital efficiency profile. The expected revenue projection of $1,741.59 million in 2026 provides incremental visibility but does not imply transformational growth.

In essence, AGNC has demonstrated earnings momentum recovery, but it has yet to demonstrate durable economic value creation.

Dividend Profile & Sustainability

AGNC’s dividend remains the central feature of the investment case. The forward yield of 12.7% is compelling on an absolute basis and remains close to its 10-year median of 12.4%. Over the past decade, yield levels have fluctuated widely between 7.7% and 20.6%, underscoring the volatility inherent in the payout structure.

Dividend growth has stalled. The five-year dividend growth rate stands at -5.2%, while the three-year growth rate is flat at 0.0%. Management appears to have shifted from growth toward preservation, maintaining distributions despite earnings variability.

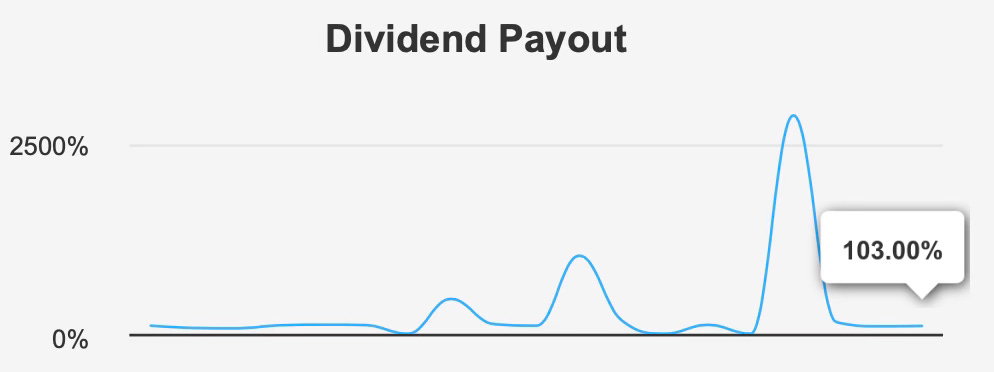

The dividend payout ratio currently sits at 103%, with dividend coverage at 0.97. This indicates that distributions slightly exceed earnings, a situation that can be sustained temporarily but leaves little margin for error.

The company pays dividends monthly, with the next ex-dividend date noted as February 27, 2026, and payment scheduled for March 10, 2026. Such frequency enhances the stock’s attractiveness for income-oriented investors seeking consistent cash flow.

However, forward expectations suggest no dividend growth over the next three to five years. Absent meaningful improvement in spread income or capital efficiency, distributions are likely to remain flat.

For income investors, the yield compensates for risk—but sustainability depends heavily on stable net interest margins and disciplined capital management.

Valuation Analysis: Income Premium Pricing Versus Economic Return Deficit

At $11 per share, AGNC trades near its three-year high, while the dividend yield is near a three-year low. This inverse relationship implies that price appreciation has outpaced income expansion.

The company is rated as a “Strong Buy” in the referenced valuation framework, though intrinsic value is listed at $0, indicating insufficient data for traditional discounted cash flow assessment. As such, valuation is more yield-driven than asset-value driven.

Given projected EPS of $1.485 next year and $1.308 the following year, the market appears to be discounting a near-term earnings peak followed by modest normalization. The absence of long-term revenue growth and the persistent ROIC–WACC gap suggest that multiple expansion is unlikely without structural improvement.

The forward yield of 12.7% effectively serves as the primary valuation anchor. Historically, when AGNC’s yield compresses toward the lower end of its 7.7%–20.6% historical band, subsequent total returns tend to moderate unless supported by improving fundamentals.

Therefore, while income remains attractive, valuation does not appear deeply discounted relative to historical yield norms.

Risk Assessment & Capital Structure Considerations

Risk factors are pronounced. AGNC’s Piotroski F-Score of 3 indicates potential operational weakness. Combined with a payout ratio exceeding 100%, this raises legitimate concerns about dividend resilience in adverse rate environments.

Insider activity further complicates the picture. Over the past year, 825,397 shares have been sold by insiders with no corresponding purchases. In the last three months alone, there were four sales and zero purchases; over six months, six sales; and over twelve months, fifteen sales. Insider ownership stands at just 0.52%, compared with institutional ownership of 35.79%.

This pattern does not necessarily imply deteriorating fundamentals, but it does suggest limited insider alignment with shareholders at current prices.

On the positive side, AGNC demonstrates strong interest coverage, suggesting the company can meet its debt obligations comfortably. The Beneish M-Score of -2.51 indicates a low likelihood of earnings manipulation, providing reassurance regarding financial statement integrity.

Liquidity is robust. Daily trading volume of 22,932,236 exceeds the two-month average of 20,430,954 by approximately 12.2%. This depth enhances tradability and reduces liquidity risk. However, a Dark Pool Index of 56.8% indicates that more than half of trading activity occurs off-exchange, potentially limiting price transparency.

The absence of a reported Debt-to-EBITDA ratio limits precise leverage analysis, but mortgage REIT structures inherently depend on significant leverage, amplifying sensitivity to rate movements.

Collectively, risks center on capital efficiency, payout sustainability, insider sentiment, and interest rate volatility.

Final Assessment

AGNC Investment Corp presents a clear income-oriented profile. A forward yield of 12.7%, monthly distributions, and strong trading liquidity make it attractive for investors prioritizing current cash flow. Recent earnings momentum has improved near-term sentiment, with Q4 2025 EPS rebounding meaningfully and analyst projections supporting continued profitability in the coming year.

Yet structural concerns persist. A five-year median ROIC of 0.0% against a WACC that has averaged 22.3% and currently stands at 35.8% signals persistent economic value destruction. Dividend growth has been negative over five years, and the payout ratio above 100% leaves limited flexibility.

At current levels, AGNC appears appropriately priced for income rather than undervalued for growth. Total return potential will likely depend on rate stability, spread management, and disciplined capital allocation rather than multiple expansion.

For income-focused investors comfortable with rate sensitivity and capital structure complexity, AGNC may serve as a high-yield allocation within a diversified portfolio. For investors seeking durable economic value creation and dividend growth, the structural gap between ROIC and cost of capital warrants caution.